Astra PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and tech trends are shaping Astra’s strategic outlook with our concise PESTLE snapshot. This 3–5 minute read reveals key external risks and opportunities you can act on today. For the full, editable deep-dive—download the complete PESTLE analysis now and make decisions with confidence.

Political factors

Policy stability and election cycles

Indonesia’s 14 February 2024 elections and the subsequent Prabowo administration reshuffle have already shifted policy emphasis across autos, mining and plantations, with auto sales around 1.0 million units in 2023 reflecting market sensitivity to incentives. Cabinet changes can quickly alter fuel and export subsidies, import rules and infrastructure budget allocations, impacting capital expenditure timelines. Astra must scenario-plan for regulatory continuity versus recalibration and intensify stakeholder engagement to protect licenses and incentives across administrations.

Industrial policy and local content (TKDN)

Local content mandates (TKDN) shape sourcing for vehicles, heavy equipment and ICT, raising input costs short-term but boosting supplier ecosystems and public tender eligibility. Astra can leverage scale to localize components and negotiate offsets, supporting Indonesia’s ~276.4 million population market (2024). Non-compliance risks procurement exclusion and administrative penalties under national procurement rules.

Infrastructure push and state partnerships

Government-led roads, ports and the IKN new capital drive strong demand for heavy equipment and logistics, with IKN funding reported at IDR 466 trillion through 2024 supporting construction and transport works. Public–private partnerships expand financing and concession models, unlocking longer-term revenue streams for equipment leasing and toll/logistics operators. Close coordination with state-owned enterprises accelerates project pipelines and contract awards. Policy delays or budget reallocations can defer revenue recognition and fleet utilization.

Energy transition and subsidy reform

Fuel and electricity subsidy adjustments alter vehicle demand and operating costs; Indonesia's subsidy cuts since 2022 pushed transport fuel costs up an estimated 8–12% in 2023, compressing margins in transport and agribusiness. Stronger policy support for EVs and renewables and Indonesia's EV targets for 2025 can re-shape Astra’s automotive and power portfolios, and early alignment secures incentives and tax breaks.

- Subsidy cuts: higher opex, margin squeeze

- EV/renewable incentives: portfolio shift opportunity

- Transport/agri: most exposed to sudden cuts

- Early compliance: access to fiscal incentives

Trade policy and regional integration

Trade policy shapes Astra’s supply chain: intra-ASEAN tariffs on parts are typically 0–5% while non-ASEAN vehicle tariffs can reach ~40%, affecting component flows and pricing; Indonesia produced ~1.2M vehicles in 2024, keeping regional assembly scale relevant. Protectionist moves favor local assembly but often raise input costs and sourcing complexity. Harmonized ASEAN standards and FTAs enable export scaling; active monitoring of WTO/FTA shifts reduces disruption risk.

- Tariff range: intra-ASEAN 0–5%, outside up to ~40%

- Indonesia production 2024: ~1.2M vehicles — supports regional assembly

- Harmonized standards boost parts exports; monitor WTO/FTA changes to mitigate supply shocks

Policy shift fuels IKN IDR 466T equipment demand; EV incentives create 2025 window

Political shifts since Feb 2024 (Prabowo cabinet) affect subsidies, tariffs and infrastructure spend, with IKN funding IDR 466T driving equipment demand. TKDN raises sourcing costs but secures tenders; non‑ASEAN tariffs up to ~40% favor local assembly. Indonesia produced ~1.2M vehicles in 2024; EV targets for 2025 create incentive windows.

| Metric | Value |

|---|---|

| IKN funding | IDR 466T (2024) |

| Vehicle prod | ~1.2M (2024) |

| Population | ~276.4M (2024) |

What is included in the product

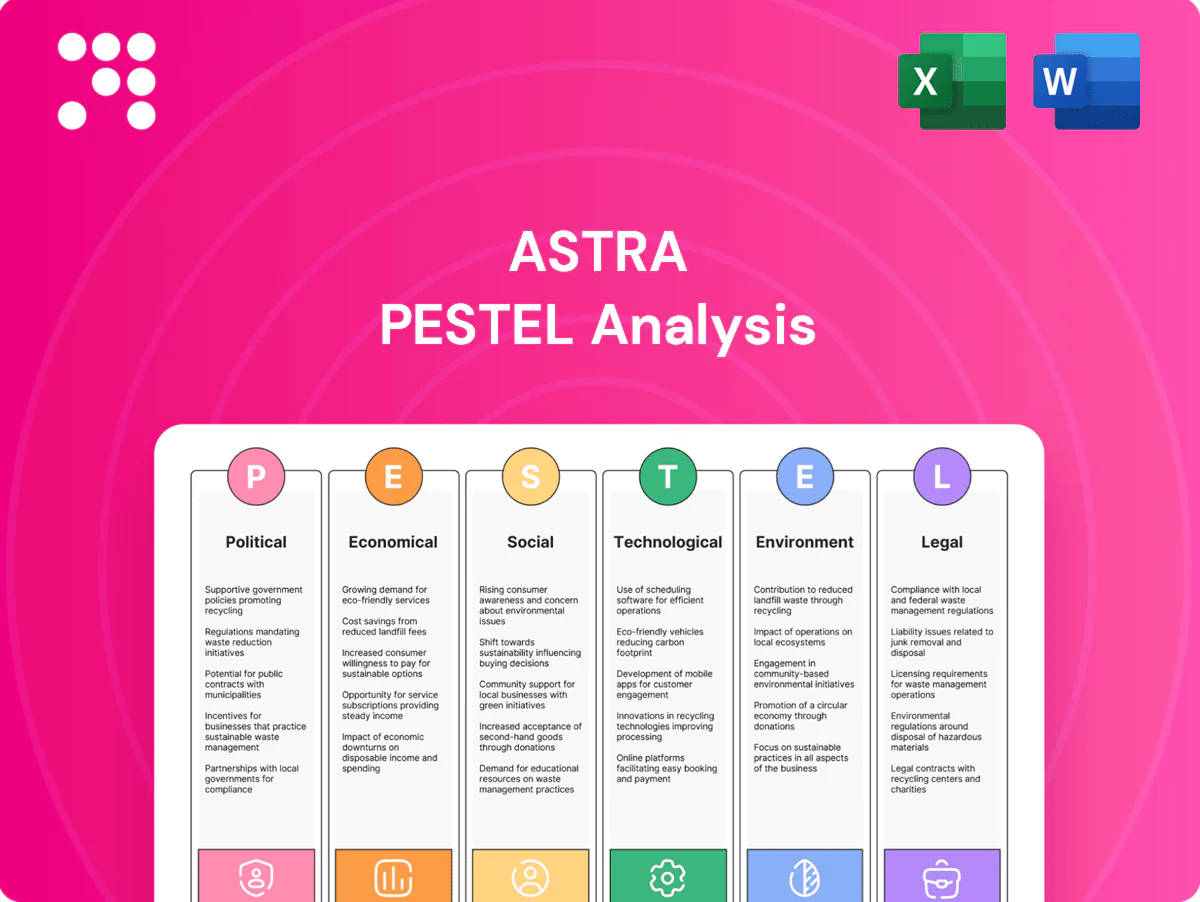

Explores how macro-environmental factors uniquely affect Astra across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends and region-specific insights to identify risks and opportunities and support executives, investors, and strategists in scenario planning and decision-making.

Astra's PESTLE delivers a clean, visually segmented summary of external factors for quick interpretation in meetings, easily editable with notes for local context and exportable for PowerPoint or team sharing to streamline risk discussions and strategic alignment.

Economic factors

GDP growth and middle-class expansion

Indonesia GDP expanded about 5.2% in 2024 with household consumption ~55% of GDP, underpinning autos, finance and retail services.

Rising incomes and a middle-class swell have pushed vehicle penetration—motorcycle fleets exceed 110 million—boosting Astra’s OEM and financing volumes.

Cyclical slowdowns in 2023–24 curtailed discretionary purchases and loan origination, with credit growth moderating to roughly 8–10% in 2024.

Astra’s diversified footprint across automotive, financial services and heavy equipment smooths revenue through cycles.

Commodity cycles (coal, CPO, metals)

Heavy equipment, mining services and agribusiness earnings at Astra closely track commodity cycles: Indonesia supplies about 60% of global CPO, while thermal coal spot prices swung roughly USD 80–200/ton in 2022–24, driving capex and parts demand in upcycles and pressuring utilization in downcycles. Hedging programs and flexible capex plans have been used to buffer volatility, and vertical integration into upstream processing stabilizes cash flow and margins across cycles.

Currency and interest rate volatility

Rupiah swings — roughly IDR15,000–16,000 per USD in 2024–mid‑2025 — raise costs for imported components and increase FX debt servicing pressures for Astra group units. Elevated BI policy rates (around 6.0% in mid‑2025) tighten consumer credit and slow auto financing growth. Strong pricing and ALM discipline have preserved spreads in Astra Financial, while local supplier development lowers FX exposure and import dependency.

Credit penetration and financial inclusion

Underbanked segments (about 31% of Indonesian adults unbanked per World Bank Global Findex 2021) present clear growth for auto and microfinance; digital onboarding and machine‑learning risk models enable scalable, lower-cost origination. Weak macro conditions lift NPL pressure—Indonesia gross banking NPL ~3% in 2023 (OJK)—so prudent provisioning is needed to protect ROE.

- Opportunity: large underbanked base (~31%)

- Scale: digital onboarding + ML risk models

- Risk: macro stress → NPLs (~3% in 2023)

- Mitigation: balanced growth with prudent provisioning to sustain ROE

Infrastructure investment and logistics costs

Improved connectivity in Indonesia lowers Astra’s distribution costs and expands addressable markets, with logistics costs estimated at about 23% of GDP (World Bank range, recent years), reducing unit transportation cost for autos and plantations. Large infrastructure project cycles drive lumpy heavy-equipment demand and capex timing; delays raise working capital needs and inventory days.

- Connectivity cuts unit distribution cost

- 23% of GDP: national logistics burden

- Project cycles = lumpy equipment demand

- Delays → higher working capital/inventory days

Policy shift fuels IKN IDR 466T equipment demand; EV incentives create 2025 window

Indonesia GDP +5.2% in 2024 with household consumption ~55% of GDP supporting autos and services. Motorcycle fleet >110m and rising middle class boost OEM and finance; credit growth ~8–10% in 2024. BI rate ~6.0% mid‑2025 tightens auto credit; unbanked ~31% offers expansion via digital lending.

| Metric | Value |

|---|---|

| GDP growth 2024 | 5.2% |

| Household share | ~55% |

| Motorcycles | >110m |

| Credit growth 2024 | 8–10% |

| BI rate mid‑2025 | ~6.0% |

| Unbanked adults | ~31% |

Same Document Delivered

Astra PESTLE Analysis

The preview shown here is the exact Astra PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with complete content and no placeholders or teasers. After checkout you’ll be able to download this identical document immediately, exactly as displayed.

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and tech trends are shaping Astra’s strategic outlook with our concise PESTLE snapshot. This 3–5 minute read reveals key external risks and opportunities you can act on today. For the full, editable deep-dive—download the complete PESTLE analysis now and make decisions with confidence.

Political factors

Policy stability and election cycles

Indonesia’s 14 February 2024 elections and the subsequent Prabowo administration reshuffle have already shifted policy emphasis across autos, mining and plantations, with auto sales around 1.0 million units in 2023 reflecting market sensitivity to incentives. Cabinet changes can quickly alter fuel and export subsidies, import rules and infrastructure budget allocations, impacting capital expenditure timelines. Astra must scenario-plan for regulatory continuity versus recalibration and intensify stakeholder engagement to protect licenses and incentives across administrations.

Industrial policy and local content (TKDN)

Local content mandates (TKDN) shape sourcing for vehicles, heavy equipment and ICT, raising input costs short-term but boosting supplier ecosystems and public tender eligibility. Astra can leverage scale to localize components and negotiate offsets, supporting Indonesia’s ~276.4 million population market (2024). Non-compliance risks procurement exclusion and administrative penalties under national procurement rules.

Infrastructure push and state partnerships

Government-led roads, ports and the IKN new capital drive strong demand for heavy equipment and logistics, with IKN funding reported at IDR 466 trillion through 2024 supporting construction and transport works. Public–private partnerships expand financing and concession models, unlocking longer-term revenue streams for equipment leasing and toll/logistics operators. Close coordination with state-owned enterprises accelerates project pipelines and contract awards. Policy delays or budget reallocations can defer revenue recognition and fleet utilization.

Energy transition and subsidy reform

Fuel and electricity subsidy adjustments alter vehicle demand and operating costs; Indonesia's subsidy cuts since 2022 pushed transport fuel costs up an estimated 8–12% in 2023, compressing margins in transport and agribusiness. Stronger policy support for EVs and renewables and Indonesia's EV targets for 2025 can re-shape Astra’s automotive and power portfolios, and early alignment secures incentives and tax breaks.

- Subsidy cuts: higher opex, margin squeeze

- EV/renewable incentives: portfolio shift opportunity

- Transport/agri: most exposed to sudden cuts

- Early compliance: access to fiscal incentives

Trade policy and regional integration

Trade policy shapes Astra’s supply chain: intra-ASEAN tariffs on parts are typically 0–5% while non-ASEAN vehicle tariffs can reach ~40%, affecting component flows and pricing; Indonesia produced ~1.2M vehicles in 2024, keeping regional assembly scale relevant. Protectionist moves favor local assembly but often raise input costs and sourcing complexity. Harmonized ASEAN standards and FTAs enable export scaling; active monitoring of WTO/FTA shifts reduces disruption risk.

- Tariff range: intra-ASEAN 0–5%, outside up to ~40%

- Indonesia production 2024: ~1.2M vehicles — supports regional assembly

- Harmonized standards boost parts exports; monitor WTO/FTA changes to mitigate supply shocks

Policy shift fuels IKN IDR 466T equipment demand; EV incentives create 2025 window

Political shifts since Feb 2024 (Prabowo cabinet) affect subsidies, tariffs and infrastructure spend, with IKN funding IDR 466T driving equipment demand. TKDN raises sourcing costs but secures tenders; non‑ASEAN tariffs up to ~40% favor local assembly. Indonesia produced ~1.2M vehicles in 2024; EV targets for 2025 create incentive windows.

| Metric | Value |

|---|---|

| IKN funding | IDR 466T (2024) |

| Vehicle prod | ~1.2M (2024) |

| Population | ~276.4M (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Astra across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends and region-specific insights to identify risks and opportunities and support executives, investors, and strategists in scenario planning and decision-making.

Astra's PESTLE delivers a clean, visually segmented summary of external factors for quick interpretation in meetings, easily editable with notes for local context and exportable for PowerPoint or team sharing to streamline risk discussions and strategic alignment.

Economic factors

GDP growth and middle-class expansion

Indonesia GDP expanded about 5.2% in 2024 with household consumption ~55% of GDP, underpinning autos, finance and retail services.

Rising incomes and a middle-class swell have pushed vehicle penetration—motorcycle fleets exceed 110 million—boosting Astra’s OEM and financing volumes.

Cyclical slowdowns in 2023–24 curtailed discretionary purchases and loan origination, with credit growth moderating to roughly 8–10% in 2024.

Astra’s diversified footprint across automotive, financial services and heavy equipment smooths revenue through cycles.

Commodity cycles (coal, CPO, metals)

Heavy equipment, mining services and agribusiness earnings at Astra closely track commodity cycles: Indonesia supplies about 60% of global CPO, while thermal coal spot prices swung roughly USD 80–200/ton in 2022–24, driving capex and parts demand in upcycles and pressuring utilization in downcycles. Hedging programs and flexible capex plans have been used to buffer volatility, and vertical integration into upstream processing stabilizes cash flow and margins across cycles.

Currency and interest rate volatility

Rupiah swings — roughly IDR15,000–16,000 per USD in 2024–mid‑2025 — raise costs for imported components and increase FX debt servicing pressures for Astra group units. Elevated BI policy rates (around 6.0% in mid‑2025) tighten consumer credit and slow auto financing growth. Strong pricing and ALM discipline have preserved spreads in Astra Financial, while local supplier development lowers FX exposure and import dependency.

Credit penetration and financial inclusion

Underbanked segments (about 31% of Indonesian adults unbanked per World Bank Global Findex 2021) present clear growth for auto and microfinance; digital onboarding and machine‑learning risk models enable scalable, lower-cost origination. Weak macro conditions lift NPL pressure—Indonesia gross banking NPL ~3% in 2023 (OJK)—so prudent provisioning is needed to protect ROE.

- Opportunity: large underbanked base (~31%)

- Scale: digital onboarding + ML risk models

- Risk: macro stress → NPLs (~3% in 2023)

- Mitigation: balanced growth with prudent provisioning to sustain ROE

Infrastructure investment and logistics costs

Improved connectivity in Indonesia lowers Astra’s distribution costs and expands addressable markets, with logistics costs estimated at about 23% of GDP (World Bank range, recent years), reducing unit transportation cost for autos and plantations. Large infrastructure project cycles drive lumpy heavy-equipment demand and capex timing; delays raise working capital needs and inventory days.

- Connectivity cuts unit distribution cost

- 23% of GDP: national logistics burden

- Project cycles = lumpy equipment demand

- Delays → higher working capital/inventory days

Policy shift fuels IKN IDR 466T equipment demand; EV incentives create 2025 window

Indonesia GDP +5.2% in 2024 with household consumption ~55% of GDP supporting autos and services. Motorcycle fleet >110m and rising middle class boost OEM and finance; credit growth ~8–10% in 2024. BI rate ~6.0% mid‑2025 tightens auto credit; unbanked ~31% offers expansion via digital lending.

| Metric | Value |

|---|---|

| GDP growth 2024 | 5.2% |

| Household share | ~55% |

| Motorcycles | >110m |

| Credit growth 2024 | 8–10% |

| BI rate mid‑2025 | ~6.0% |

| Unbanked adults | ~31% |

Same Document Delivered

Astra PESTLE Analysis

The preview shown here is the exact Astra PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with complete content and no placeholders or teasers. After checkout you’ll be able to download this identical document immediately, exactly as displayed.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and tech trends are shaping Astra’s strategic outlook with our concise PESTLE snapshot. This 3–5 minute read reveals key external risks and opportunities you can act on today. For the full, editable deep-dive—download the complete PESTLE analysis now and make decisions with confidence.

Political factors

Policy stability and election cycles

Indonesia’s 14 February 2024 elections and the subsequent Prabowo administration reshuffle have already shifted policy emphasis across autos, mining and plantations, with auto sales around 1.0 million units in 2023 reflecting market sensitivity to incentives. Cabinet changes can quickly alter fuel and export subsidies, import rules and infrastructure budget allocations, impacting capital expenditure timelines. Astra must scenario-plan for regulatory continuity versus recalibration and intensify stakeholder engagement to protect licenses and incentives across administrations.

Industrial policy and local content (TKDN)

Local content mandates (TKDN) shape sourcing for vehicles, heavy equipment and ICT, raising input costs short-term but boosting supplier ecosystems and public tender eligibility. Astra can leverage scale to localize components and negotiate offsets, supporting Indonesia’s ~276.4 million population market (2024). Non-compliance risks procurement exclusion and administrative penalties under national procurement rules.

Infrastructure push and state partnerships

Government-led roads, ports and the IKN new capital drive strong demand for heavy equipment and logistics, with IKN funding reported at IDR 466 trillion through 2024 supporting construction and transport works. Public–private partnerships expand financing and concession models, unlocking longer-term revenue streams for equipment leasing and toll/logistics operators. Close coordination with state-owned enterprises accelerates project pipelines and contract awards. Policy delays or budget reallocations can defer revenue recognition and fleet utilization.

Energy transition and subsidy reform

Fuel and electricity subsidy adjustments alter vehicle demand and operating costs; Indonesia's subsidy cuts since 2022 pushed transport fuel costs up an estimated 8–12% in 2023, compressing margins in transport and agribusiness. Stronger policy support for EVs and renewables and Indonesia's EV targets for 2025 can re-shape Astra’s automotive and power portfolios, and early alignment secures incentives and tax breaks.

- Subsidy cuts: higher opex, margin squeeze

- EV/renewable incentives: portfolio shift opportunity

- Transport/agri: most exposed to sudden cuts

- Early compliance: access to fiscal incentives

Trade policy and regional integration

Trade policy shapes Astra’s supply chain: intra-ASEAN tariffs on parts are typically 0–5% while non-ASEAN vehicle tariffs can reach ~40%, affecting component flows and pricing; Indonesia produced ~1.2M vehicles in 2024, keeping regional assembly scale relevant. Protectionist moves favor local assembly but often raise input costs and sourcing complexity. Harmonized ASEAN standards and FTAs enable export scaling; active monitoring of WTO/FTA shifts reduces disruption risk.

- Tariff range: intra-ASEAN 0–5%, outside up to ~40%

- Indonesia production 2024: ~1.2M vehicles — supports regional assembly

- Harmonized standards boost parts exports; monitor WTO/FTA changes to mitigate supply shocks

Policy shift fuels IKN IDR 466T equipment demand; EV incentives create 2025 window

Political shifts since Feb 2024 (Prabowo cabinet) affect subsidies, tariffs and infrastructure spend, with IKN funding IDR 466T driving equipment demand. TKDN raises sourcing costs but secures tenders; non‑ASEAN tariffs up to ~40% favor local assembly. Indonesia produced ~1.2M vehicles in 2024; EV targets for 2025 create incentive windows.

| Metric | Value |

|---|---|

| IKN funding | IDR 466T (2024) |

| Vehicle prod | ~1.2M (2024) |

| Population | ~276.4M (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Astra across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-backed trends and region-specific insights to identify risks and opportunities and support executives, investors, and strategists in scenario planning and decision-making.

Astra's PESTLE delivers a clean, visually segmented summary of external factors for quick interpretation in meetings, easily editable with notes for local context and exportable for PowerPoint or team sharing to streamline risk discussions and strategic alignment.

Economic factors

GDP growth and middle-class expansion

Indonesia GDP expanded about 5.2% in 2024 with household consumption ~55% of GDP, underpinning autos, finance and retail services.

Rising incomes and a middle-class swell have pushed vehicle penetration—motorcycle fleets exceed 110 million—boosting Astra’s OEM and financing volumes.

Cyclical slowdowns in 2023–24 curtailed discretionary purchases and loan origination, with credit growth moderating to roughly 8–10% in 2024.

Astra’s diversified footprint across automotive, financial services and heavy equipment smooths revenue through cycles.

Commodity cycles (coal, CPO, metals)

Heavy equipment, mining services and agribusiness earnings at Astra closely track commodity cycles: Indonesia supplies about 60% of global CPO, while thermal coal spot prices swung roughly USD 80–200/ton in 2022–24, driving capex and parts demand in upcycles and pressuring utilization in downcycles. Hedging programs and flexible capex plans have been used to buffer volatility, and vertical integration into upstream processing stabilizes cash flow and margins across cycles.

Currency and interest rate volatility

Rupiah swings — roughly IDR15,000–16,000 per USD in 2024–mid‑2025 — raise costs for imported components and increase FX debt servicing pressures for Astra group units. Elevated BI policy rates (around 6.0% in mid‑2025) tighten consumer credit and slow auto financing growth. Strong pricing and ALM discipline have preserved spreads in Astra Financial, while local supplier development lowers FX exposure and import dependency.

Credit penetration and financial inclusion

Underbanked segments (about 31% of Indonesian adults unbanked per World Bank Global Findex 2021) present clear growth for auto and microfinance; digital onboarding and machine‑learning risk models enable scalable, lower-cost origination. Weak macro conditions lift NPL pressure—Indonesia gross banking NPL ~3% in 2023 (OJK)—so prudent provisioning is needed to protect ROE.

- Opportunity: large underbanked base (~31%)

- Scale: digital onboarding + ML risk models

- Risk: macro stress → NPLs (~3% in 2023)

- Mitigation: balanced growth with prudent provisioning to sustain ROE

Infrastructure investment and logistics costs

Improved connectivity in Indonesia lowers Astra’s distribution costs and expands addressable markets, with logistics costs estimated at about 23% of GDP (World Bank range, recent years), reducing unit transportation cost for autos and plantations. Large infrastructure project cycles drive lumpy heavy-equipment demand and capex timing; delays raise working capital needs and inventory days.

- Connectivity cuts unit distribution cost

- 23% of GDP: national logistics burden

- Project cycles = lumpy equipment demand

- Delays → higher working capital/inventory days

Policy shift fuels IKN IDR 466T equipment demand; EV incentives create 2025 window

Indonesia GDP +5.2% in 2024 with household consumption ~55% of GDP supporting autos and services. Motorcycle fleet >110m and rising middle class boost OEM and finance; credit growth ~8–10% in 2024. BI rate ~6.0% mid‑2025 tightens auto credit; unbanked ~31% offers expansion via digital lending.

| Metric | Value |

|---|---|

| GDP growth 2024 | 5.2% |

| Household share | ~55% |

| Motorcycles | >110m |

| Credit growth 2024 | 8–10% |

| BI rate mid‑2025 | ~6.0% |

| Unbanked adults | ~31% |

Same Document Delivered

Astra PESTLE Analysis

The preview shown here is the exact Astra PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with complete content and no placeholders or teasers. After checkout you’ll be able to download this identical document immediately, exactly as displayed.