Asure Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Asure's Porter's Five Forces Analysis reveals competitive intensity across supplier power, buyer power, entrant threats, substitute risk, and rivalry, highlighting where margins and strategy are most vulnerable. It synthesizes market structure, regulatory tailwinds, and platform differentiation to show how Asure can defend pricing and pursue growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Asure’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud hosts

Asure depends on hyperscale IaaS for uptime, storage and compute, while AWS (≈32% market share) and Azure (≈23%) concentrate bargaining power (Canalys 2023/24). Vendors can push pricing or contract terms that squeeze Asure’s margins and SLAs; outages or price shifts have direct impact. Multi-cloud adoption (92% of enterprises per Flexera 2024) or reserved instances (up to ~72% savings on AWS) mitigate risk but migration costs remain high.

Regulatory data and tax engines

Accurate payroll tax tables, filings, and updates rely on specialized content providers and government feeds; the US alone has over 10,000 payroll tax jurisdictions, concentrating supplier importance. Fewer credible data vendors raise switching costs and supplier power, since errors can trigger penalties and interest that may equal 100% of unpaid trust-fund taxes. Long-term vendor partnerships secure SLA performance but reduce negotiation flexibility and price leverage.

Payments and banking rails

Payments and banking rails for payroll funding, ACH and paycards depend on sponsor banks and processors; ACH volumes exceeded 30 billion transactions by 2024 (NACHA), concentrating routing power. Compliance, risk screening and float management let processors extract higher fees and stricter terms, with fee packages often ranging broadly by risk and volume. Volume growth can unlock better pricing tiers, but SMB payroll volatility and churn limit supplier bargaining power. Maintaining redundancy across multiple processors reduces concentration risk and supplier leverage.

Benefits carriers and brokers

- EDI standard: HIPAA X12 834

- Top 5 carriers ≈70% market share (2024)

- Certification increases switching cost

- Preferred deals boost distribution but limit flexibility

Specialized developers and integrations

HCM platforms require domain-skilled engineers and deep integrations with ERPs, ATS, and time devices, and scarcity of such talent plus high-demand ISV connectors strengthens supplier bargaining power; LinkedIn and industry reports in 2024 noted continued developer demand. Wage inflation and partner certification fees add cost pressure, while investing in robust APIs and SDKs can reduce dependency over time.

- High integration complexity

- Scarce domain talent

- Rising wage/certification costs

- APIs/SDKs lower long-term supplier risk

Suppliers dominate: hyperscale cloud, payment rails and carriers concentrate pricing power

Suppliers wield high power: hyperscale IaaS (AWS ≈32%, Azure ≈23% Canalys 2024) and payments rails (ACH >30B txns 2024) can push pricing/SLAs, while payroll tax data (10,000+ US jurisdictions) and top5 carriers (~70% market share 2024) concentrate vendor leverage. Multi-cloud (92% enterprises Flexera 2024), reserved instances and processor redundancy mitigate but do not eliminate switching costs and certification friction.

| Supplier | 2024 Metric |

|---|---|

| Hyperscale IaaS | AWS 32% / Azure 23% |

| Multi-cloud | 92% enterprises |

| ACH | >30B txns |

| Payroll jurisdictions | >10,000 US |

| Top carriers | ~70% market |

What is included in the product

Tailored Porter's Five Forces analysis for Asure that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—supported by industry context and strategic implications for pricing, profitability, and market positioning.

A single-sheet, customizable Five Forces tool that converts complex market pressures into an intuitive spider chart and copy-ready visuals, letting teams quickly model scenarios, update data without code, and embed results into decks or dashboards.

Customers Bargaining Power

SMB price sensitivity

Small and mid-sized clients, part of the roughly 33.2 million US small businesses in 2024, are highly cost-conscious and benchmark per-employee-per-month pricing across vendors. Transparent online pricing amplifies negotiation leverage, driving demands for discounts, bundles, and annual prepay to improve close rates. Churn risk rises when perceived ROI falls, making retention-sensitive pricing critical.

Abundant alternatives

Buyers can choose ADP, Paychex, Paylocity, Paycom, Gusto, Rippling and others, creating abundant alternatives that erode Asure’s pricing leverage. Core payroll feature parity in 2024 further reduces product differentiation, pushing competition toward price and service in RFPs. For SMBs, references and online reviews (G2/Capterra) now sway deal outcomes more than brand alone.

Moderate switching costs

Data migration and year-to-date carryovers create measurable friction but are manageable with change management; 2024 surveys indicate about 30% of migrations are timed to quarter or year-end windows, which eases switching. Free migration offers lower barriers and strengthens buyer leverage, while integration-driven lock-in remains substantially higher for multi-module users.

Demand for compliance assurance

SMBs increasingly demand guarantees on tax filings, wage garnishments and ACA reporting, turning liability-shift clauses and error indemnification into primary negotiation points; in 2024 an estimated 64% of SMB buyers required contractual indemnities for payroll/compliance failures. Buyers now push for strict SLAs and rapid support response, while vendors with proven 2024 compliance track records secure fewer concessions.

Service quality expectations

- Support speed

- Implementation timelines

- Named reps & onboarding

- NPS impacts renewals

SMB buyers force discounts; 64% demand indemnities, 30% time migrations

SMB buyers (33.2M US small businesses in 2024) exert strong price and SLA pressure, leveraging transparent pricing and vendor parity to demand discounts, bundles and indemnities; 64% required contractual indemnities in 2024. About 30% of migrations align to quarter/year-end reducing switching friction, while competition from ADP, Paychex, Paylocity, Paycom, Gusto and Rippling limits Asure’s pricing power.

| Metric | 2024 |

|---|---|

| US SMBs | 33.2M |

| Buyer indemnity demand | 64% |

| Migrations timed | 30% |

| Named alternatives | 6 |

Preview the Actual Deliverable

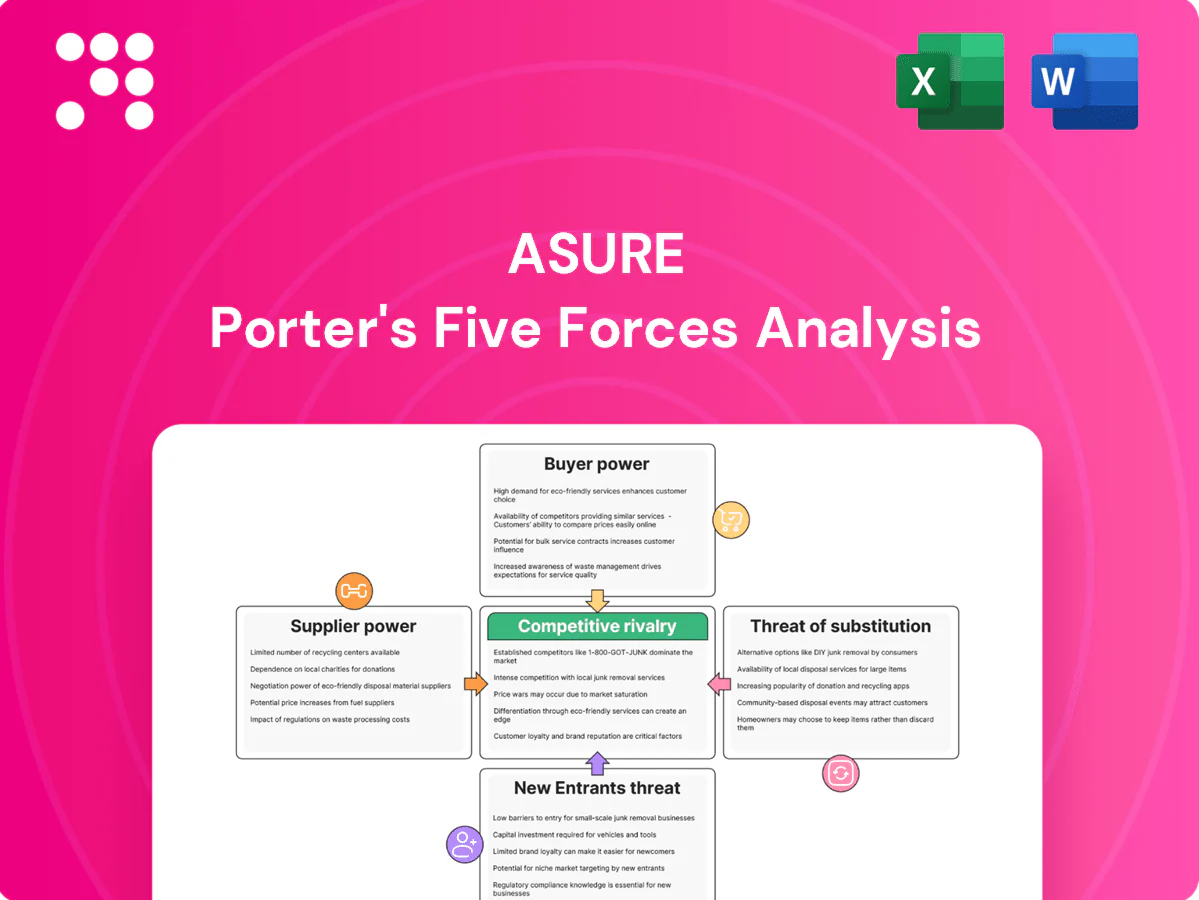

Asure Porter's Five Forces Analysis

This preview shows the exact Asure Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is the fully formatted, final document ready for immediate download and use. What you see here is what you get upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Asure's Porter's Five Forces Analysis reveals competitive intensity across supplier power, buyer power, entrant threats, substitute risk, and rivalry, highlighting where margins and strategy are most vulnerable. It synthesizes market structure, regulatory tailwinds, and platform differentiation to show how Asure can defend pricing and pursue growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Asure’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud hosts

Asure depends on hyperscale IaaS for uptime, storage and compute, while AWS (≈32% market share) and Azure (≈23%) concentrate bargaining power (Canalys 2023/24). Vendors can push pricing or contract terms that squeeze Asure’s margins and SLAs; outages or price shifts have direct impact. Multi-cloud adoption (92% of enterprises per Flexera 2024) or reserved instances (up to ~72% savings on AWS) mitigate risk but migration costs remain high.

Regulatory data and tax engines

Accurate payroll tax tables, filings, and updates rely on specialized content providers and government feeds; the US alone has over 10,000 payroll tax jurisdictions, concentrating supplier importance. Fewer credible data vendors raise switching costs and supplier power, since errors can trigger penalties and interest that may equal 100% of unpaid trust-fund taxes. Long-term vendor partnerships secure SLA performance but reduce negotiation flexibility and price leverage.

Payments and banking rails

Payments and banking rails for payroll funding, ACH and paycards depend on sponsor banks and processors; ACH volumes exceeded 30 billion transactions by 2024 (NACHA), concentrating routing power. Compliance, risk screening and float management let processors extract higher fees and stricter terms, with fee packages often ranging broadly by risk and volume. Volume growth can unlock better pricing tiers, but SMB payroll volatility and churn limit supplier bargaining power. Maintaining redundancy across multiple processors reduces concentration risk and supplier leverage.

Benefits carriers and brokers

- EDI standard: HIPAA X12 834

- Top 5 carriers ≈70% market share (2024)

- Certification increases switching cost

- Preferred deals boost distribution but limit flexibility

Specialized developers and integrations

HCM platforms require domain-skilled engineers and deep integrations with ERPs, ATS, and time devices, and scarcity of such talent plus high-demand ISV connectors strengthens supplier bargaining power; LinkedIn and industry reports in 2024 noted continued developer demand. Wage inflation and partner certification fees add cost pressure, while investing in robust APIs and SDKs can reduce dependency over time.

- High integration complexity

- Scarce domain talent

- Rising wage/certification costs

- APIs/SDKs lower long-term supplier risk

Suppliers dominate: hyperscale cloud, payment rails and carriers concentrate pricing power

Suppliers wield high power: hyperscale IaaS (AWS ≈32%, Azure ≈23% Canalys 2024) and payments rails (ACH >30B txns 2024) can push pricing/SLAs, while payroll tax data (10,000+ US jurisdictions) and top5 carriers (~70% market share 2024) concentrate vendor leverage. Multi-cloud (92% enterprises Flexera 2024), reserved instances and processor redundancy mitigate but do not eliminate switching costs and certification friction.

| Supplier | 2024 Metric |

|---|---|

| Hyperscale IaaS | AWS 32% / Azure 23% |

| Multi-cloud | 92% enterprises |

| ACH | >30B txns |

| Payroll jurisdictions | >10,000 US |

| Top carriers | ~70% market |

What is included in the product

Tailored Porter's Five Forces analysis for Asure that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—supported by industry context and strategic implications for pricing, profitability, and market positioning.

A single-sheet, customizable Five Forces tool that converts complex market pressures into an intuitive spider chart and copy-ready visuals, letting teams quickly model scenarios, update data without code, and embed results into decks or dashboards.

Customers Bargaining Power

SMB price sensitivity

Small and mid-sized clients, part of the roughly 33.2 million US small businesses in 2024, are highly cost-conscious and benchmark per-employee-per-month pricing across vendors. Transparent online pricing amplifies negotiation leverage, driving demands for discounts, bundles, and annual prepay to improve close rates. Churn risk rises when perceived ROI falls, making retention-sensitive pricing critical.

Abundant alternatives

Buyers can choose ADP, Paychex, Paylocity, Paycom, Gusto, Rippling and others, creating abundant alternatives that erode Asure’s pricing leverage. Core payroll feature parity in 2024 further reduces product differentiation, pushing competition toward price and service in RFPs. For SMBs, references and online reviews (G2/Capterra) now sway deal outcomes more than brand alone.

Moderate switching costs

Data migration and year-to-date carryovers create measurable friction but are manageable with change management; 2024 surveys indicate about 30% of migrations are timed to quarter or year-end windows, which eases switching. Free migration offers lower barriers and strengthens buyer leverage, while integration-driven lock-in remains substantially higher for multi-module users.

Demand for compliance assurance

SMBs increasingly demand guarantees on tax filings, wage garnishments and ACA reporting, turning liability-shift clauses and error indemnification into primary negotiation points; in 2024 an estimated 64% of SMB buyers required contractual indemnities for payroll/compliance failures. Buyers now push for strict SLAs and rapid support response, while vendors with proven 2024 compliance track records secure fewer concessions.

Service quality expectations

- Support speed

- Implementation timelines

- Named reps & onboarding

- NPS impacts renewals

SMB buyers force discounts; 64% demand indemnities, 30% time migrations

SMB buyers (33.2M US small businesses in 2024) exert strong price and SLA pressure, leveraging transparent pricing and vendor parity to demand discounts, bundles and indemnities; 64% required contractual indemnities in 2024. About 30% of migrations align to quarter/year-end reducing switching friction, while competition from ADP, Paychex, Paylocity, Paycom, Gusto and Rippling limits Asure’s pricing power.

| Metric | 2024 |

|---|---|

| US SMBs | 33.2M |

| Buyer indemnity demand | 64% |

| Migrations timed | 30% |

| Named alternatives | 6 |

Preview the Actual Deliverable

Asure Porter's Five Forces Analysis

This preview shows the exact Asure Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is the fully formatted, final document ready for immediate download and use. What you see here is what you get upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Asure's Porter's Five Forces Analysis reveals competitive intensity across supplier power, buyer power, entrant threats, substitute risk, and rivalry, highlighting where margins and strategy are most vulnerable. It synthesizes market structure, regulatory tailwinds, and platform differentiation to show how Asure can defend pricing and pursue growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Asure’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud hosts

Asure depends on hyperscale IaaS for uptime, storage and compute, while AWS (≈32% market share) and Azure (≈23%) concentrate bargaining power (Canalys 2023/24). Vendors can push pricing or contract terms that squeeze Asure’s margins and SLAs; outages or price shifts have direct impact. Multi-cloud adoption (92% of enterprises per Flexera 2024) or reserved instances (up to ~72% savings on AWS) mitigate risk but migration costs remain high.

Regulatory data and tax engines

Accurate payroll tax tables, filings, and updates rely on specialized content providers and government feeds; the US alone has over 10,000 payroll tax jurisdictions, concentrating supplier importance. Fewer credible data vendors raise switching costs and supplier power, since errors can trigger penalties and interest that may equal 100% of unpaid trust-fund taxes. Long-term vendor partnerships secure SLA performance but reduce negotiation flexibility and price leverage.

Payments and banking rails

Payments and banking rails for payroll funding, ACH and paycards depend on sponsor banks and processors; ACH volumes exceeded 30 billion transactions by 2024 (NACHA), concentrating routing power. Compliance, risk screening and float management let processors extract higher fees and stricter terms, with fee packages often ranging broadly by risk and volume. Volume growth can unlock better pricing tiers, but SMB payroll volatility and churn limit supplier bargaining power. Maintaining redundancy across multiple processors reduces concentration risk and supplier leverage.

Benefits carriers and brokers

- EDI standard: HIPAA X12 834

- Top 5 carriers ≈70% market share (2024)

- Certification increases switching cost

- Preferred deals boost distribution but limit flexibility

Specialized developers and integrations

HCM platforms require domain-skilled engineers and deep integrations with ERPs, ATS, and time devices, and scarcity of such talent plus high-demand ISV connectors strengthens supplier bargaining power; LinkedIn and industry reports in 2024 noted continued developer demand. Wage inflation and partner certification fees add cost pressure, while investing in robust APIs and SDKs can reduce dependency over time.

- High integration complexity

- Scarce domain talent

- Rising wage/certification costs

- APIs/SDKs lower long-term supplier risk

Suppliers dominate: hyperscale cloud, payment rails and carriers concentrate pricing power

Suppliers wield high power: hyperscale IaaS (AWS ≈32%, Azure ≈23% Canalys 2024) and payments rails (ACH >30B txns 2024) can push pricing/SLAs, while payroll tax data (10,000+ US jurisdictions) and top5 carriers (~70% market share 2024) concentrate vendor leverage. Multi-cloud (92% enterprises Flexera 2024), reserved instances and processor redundancy mitigate but do not eliminate switching costs and certification friction.

| Supplier | 2024 Metric |

|---|---|

| Hyperscale IaaS | AWS 32% / Azure 23% |

| Multi-cloud | 92% enterprises |

| ACH | >30B txns |

| Payroll jurisdictions | >10,000 US |

| Top carriers | ~70% market |

What is included in the product

Tailored Porter's Five Forces analysis for Asure that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—supported by industry context and strategic implications for pricing, profitability, and market positioning.

A single-sheet, customizable Five Forces tool that converts complex market pressures into an intuitive spider chart and copy-ready visuals, letting teams quickly model scenarios, update data without code, and embed results into decks or dashboards.

Customers Bargaining Power

SMB price sensitivity

Small and mid-sized clients, part of the roughly 33.2 million US small businesses in 2024, are highly cost-conscious and benchmark per-employee-per-month pricing across vendors. Transparent online pricing amplifies negotiation leverage, driving demands for discounts, bundles, and annual prepay to improve close rates. Churn risk rises when perceived ROI falls, making retention-sensitive pricing critical.

Abundant alternatives

Buyers can choose ADP, Paychex, Paylocity, Paycom, Gusto, Rippling and others, creating abundant alternatives that erode Asure’s pricing leverage. Core payroll feature parity in 2024 further reduces product differentiation, pushing competition toward price and service in RFPs. For SMBs, references and online reviews (G2/Capterra) now sway deal outcomes more than brand alone.

Moderate switching costs

Data migration and year-to-date carryovers create measurable friction but are manageable with change management; 2024 surveys indicate about 30% of migrations are timed to quarter or year-end windows, which eases switching. Free migration offers lower barriers and strengthens buyer leverage, while integration-driven lock-in remains substantially higher for multi-module users.

Demand for compliance assurance

SMBs increasingly demand guarantees on tax filings, wage garnishments and ACA reporting, turning liability-shift clauses and error indemnification into primary negotiation points; in 2024 an estimated 64% of SMB buyers required contractual indemnities for payroll/compliance failures. Buyers now push for strict SLAs and rapid support response, while vendors with proven 2024 compliance track records secure fewer concessions.

Service quality expectations

- Support speed

- Implementation timelines

- Named reps & onboarding

- NPS impacts renewals

SMB buyers force discounts; 64% demand indemnities, 30% time migrations

SMB buyers (33.2M US small businesses in 2024) exert strong price and SLA pressure, leveraging transparent pricing and vendor parity to demand discounts, bundles and indemnities; 64% required contractual indemnities in 2024. About 30% of migrations align to quarter/year-end reducing switching friction, while competition from ADP, Paychex, Paylocity, Paycom, Gusto and Rippling limits Asure’s pricing power.

| Metric | 2024 |

|---|---|

| US SMBs | 33.2M |

| Buyer indemnity demand | 64% |

| Migrations timed | 30% |

| Named alternatives | 6 |

Preview the Actual Deliverable

Asure Porter's Five Forces Analysis

This preview shows the exact Asure Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is the fully formatted, final document ready for immediate download and use. What you see here is what you get upon payment.