Athene Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

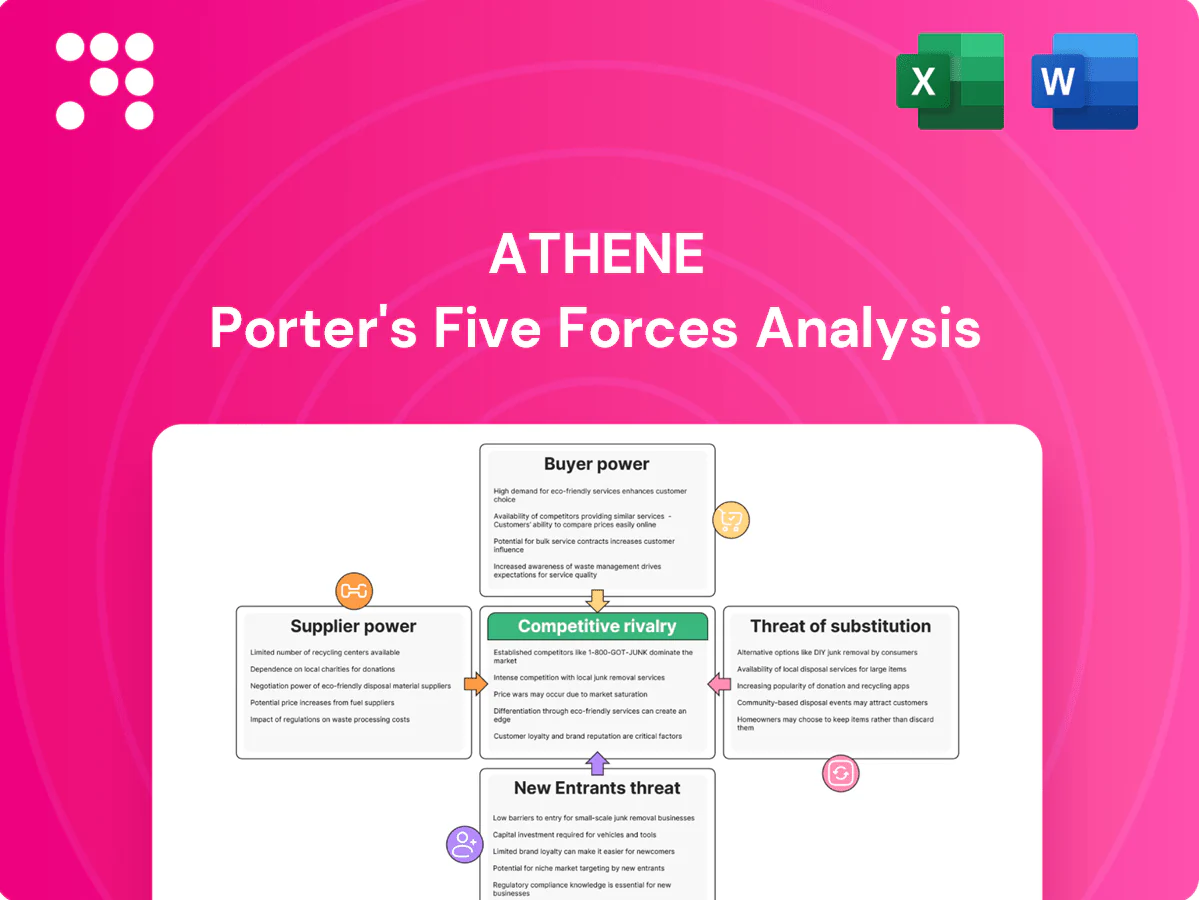

Athene’s Porter’s Five Forces Analysis distills the insurer’s competitive landscape, highlighting buyer and supplier power, barriers to entry, rivalry, and substitute threats. It examines capital intensity, regulatory pressure, and distribution channel influence shaping margins and growth. The findings point to strategic levers for risk mitigation and value creation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Athene’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital and liquidity providers

Athene depends on wholesale funding, FHLB advances and cash markets to manage liquidity and growth, supporting roughly $270 billion of invested assets as of 2024. When credit tightens, higher cost of capital compresses spreads and returns on new business. Diversified funding sources and investment-grade ratings have reduced single-counterparty concentration. Macro cycles, however, can rapidly shift supplier power upward and raise funding costs.

Asset origination and managers

Athene’s yields depend on access to private credit, ABS and specialty assets sourced via external managers and partners, and scarcity can push manager fees higher and compress net spread. Competition for assets has tightened as private debt AUM expanded to roughly $1.3 trillion in 2024, boosting supplier leverage. Athene’s affiliated manager pipeline and sponsor scale—Apollo reported about $678 billion AUM in 2024—partially cushions this risk.

Reinsurance and retrocession counterparties

Third‑party reinsurance and retrocession pricing and capacity directly affect Athene’s capital efficiency and risk transfer; global reinsurance rates rose about 10% in 2024, tightening cost of capital and transfer economics. In volatile markets reinsurers demand higher margins and tighter terms, compressing Athene’s spread. Diversifying counterparties reduces dependency, while regulatory scrutiny of affiliated reinsurance alters bargaining leverage.

Technology, admin platforms, and data vendors

- High switching costs

- Vendor concentration

- Long contracts

- In-house mitigation

Specialized talent and advisory

Specialized actuarial, ALM and risk talent is scarce and cyclical, increasing supplier power for Athene; the tight 2024 U.S. labor market (unemployment ~3.8%) amplified wage inflation and retention-package costs, raising operating expenses and dependence on external advisors (legal, compliance).

- Actuarial/ALM scarcity raises wages and turnover risk

- Retention packages and wage inflation drive costs

- External advisors add fixed, cyclical regulatory spend

Wholesale funding stress, scarce private credit and rising reinsurance rates squeeze yields

Athene relies on wholesale funding, FHLB and cash markets for about $270B invested assets (2024); funding cost spikes compress spreads. Private credit/ABS scarcity (private debt AUM ~$1.3T in 2024) and manager fees pressure yield; Apollo AUM ~$678B cushions access. Reinsurance rates rose ~10% in 2024; vendor and talent scarcity (US unemployment ~3.8% in 2024) raise supplier leverage.

| Metric | 2024 value |

|---|---|

| Invested assets | $270B |

| Private debt AUM | $1.3T |

| Apollo AUM | $678B |

| Reinsurance rates | +10% |

| US unemployment | 3.8% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Athene. Evaluates supplier and buyer power, identifies disruptive threats and substitutes, and highlights barriers protecting incumbency; fully editable for reports and decks.

Athene Porter's Five Forces delivers a one-sheet, customizable view of competitive pressure—toggle inputs, generate an instant spider chart, and copy-ready visuals to relieve analysis bottlenecks and speed confident strategic decisions.

Customers Bargaining Power

Rate-sensitive retail annuity buyers

Rate-sensitive retail annuity buyers intensely compare credited rates, caps, and bonuses across carriers; transparent rate sheets and online aggregators heighten price sensitivity. Surrender schedules—commonly 5–10 years—curb in-force switching but do not deter purchase-level shopping. With the 10-year Treasury near 4.5% in 2024, buyer leverage on new business pricing increased materially.

Intermediated distribution (IMOs, banks, advisors)

Distributors (IMOs, banks, advisors) steer product flow, negotiate compensation and marketing support, and gatekeep shelf space and training access, boosting buyer power; in 2024 intermediated channels handled the majority of U.S. retail annuity sales per LIMRA. Carriers thus compete on service, speed and product breadth to win placement. Concentrated IMOs can extract concessions and prefer carriers offering strong back-office support.

Pension risk transfer sponsors

Corporate plan sponsors run competitive auctions that commonly draw 5–10 insurers, keeping pricing margins tight and terms highly standardized. Large deals, typically exceeding $1 billion, amplify buyer bargaining power through scale and portfolio leverage. Pricing spreads in the market are often single-digit basis points, so execution certainty and AA/A-rated balance sheet strength differentiate insurers but do not eliminate sponsor leverage.

Reinsurance ceding companies

Reinsurance ceding companies wield strong bargaining power as primary insurers can shop ceded blocks on price and collateral; Athene, with over $300 billion of invested assets in 2024, faces counterparties that route deal flow by economic terms and ratings.

Sophisticated buyers demand transparency and bespoke structures, pushing reinsurers to offer tailored collateral and reporting; deal allocation often favors counterparties with A‑range or higher ratings.

- Shopability: price + collateral

- Deal flow: terms + counterparty strength

- Sophistication: transparency + bespoke

- Negotiating power: elevated

Policyholder protections and switching frictions

Regulatory disclosures such as NAIC annuity buyer guides improve transparency and support buyer power at sale, while surrender charges commonly run 5–10% in early years and tax rules make post-issue mobility costly; industry lapse rates historically cluster around 4–7% (2024 estimates), so leverage is strongest at point of sale and weakens later, with product complexity both obstructing and enabling negotiation.

- Disclosure: NAIC/state rules boost comparability

- Surrender charges: 5–10% early years

- Tax impact: taxes on gains deter switching

- Timing: highest buyer leverage at sale

- Complexity: can reduce or increase negotiation power

Rate-sensitive annuity buyers boost purchases as 10y Treasury ~4.5% (2024)

Retail annuity buyers are highly rate-sensitive; with the 10-year Treasury ~4.5% in 2024 purchase leverage rose while surrender schedules (5–10 years) and taxes limit post-issue switching. Distributors (IMOs, banks, advisors) control shelf space—LIMRA shows intermediated channels drove the majority of 2024 U.S. retail annuity sales—raising buyer power. Corporate sponsors run auctions (often $1bn+), and reinsurers negotiate on price/collateral; Athene held >$300bn AUM in 2024.

| Metric | 2024 Value |

|---|---|

| 10y Treasury | ~4.5% |

| Surrender charges | 5–10% |

| Lapse rates | 4–7% |

| Athene AUM | >$300bn |

Preview the Actual Deliverable

Athene Porter's Five Forces Analysis

You’re previewing the exact Athene Porter’s Five Forces Analysis you will receive after purchase—no samples or placeholders. This professionally written, fully formatted document is ready for immediate download and use the moment you buy. No edits or setup required; the file shown is the deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Athene’s Porter’s Five Forces Analysis distills the insurer’s competitive landscape, highlighting buyer and supplier power, barriers to entry, rivalry, and substitute threats. It examines capital intensity, regulatory pressure, and distribution channel influence shaping margins and growth. The findings point to strategic levers for risk mitigation and value creation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Athene’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital and liquidity providers

Athene depends on wholesale funding, FHLB advances and cash markets to manage liquidity and growth, supporting roughly $270 billion of invested assets as of 2024. When credit tightens, higher cost of capital compresses spreads and returns on new business. Diversified funding sources and investment-grade ratings have reduced single-counterparty concentration. Macro cycles, however, can rapidly shift supplier power upward and raise funding costs.

Asset origination and managers

Athene’s yields depend on access to private credit, ABS and specialty assets sourced via external managers and partners, and scarcity can push manager fees higher and compress net spread. Competition for assets has tightened as private debt AUM expanded to roughly $1.3 trillion in 2024, boosting supplier leverage. Athene’s affiliated manager pipeline and sponsor scale—Apollo reported about $678 billion AUM in 2024—partially cushions this risk.

Reinsurance and retrocession counterparties

Third‑party reinsurance and retrocession pricing and capacity directly affect Athene’s capital efficiency and risk transfer; global reinsurance rates rose about 10% in 2024, tightening cost of capital and transfer economics. In volatile markets reinsurers demand higher margins and tighter terms, compressing Athene’s spread. Diversifying counterparties reduces dependency, while regulatory scrutiny of affiliated reinsurance alters bargaining leverage.

Technology, admin platforms, and data vendors

- High switching costs

- Vendor concentration

- Long contracts

- In-house mitigation

Specialized talent and advisory

Specialized actuarial, ALM and risk talent is scarce and cyclical, increasing supplier power for Athene; the tight 2024 U.S. labor market (unemployment ~3.8%) amplified wage inflation and retention-package costs, raising operating expenses and dependence on external advisors (legal, compliance).

- Actuarial/ALM scarcity raises wages and turnover risk

- Retention packages and wage inflation drive costs

- External advisors add fixed, cyclical regulatory spend

Wholesale funding stress, scarce private credit and rising reinsurance rates squeeze yields

Athene relies on wholesale funding, FHLB and cash markets for about $270B invested assets (2024); funding cost spikes compress spreads. Private credit/ABS scarcity (private debt AUM ~$1.3T in 2024) and manager fees pressure yield; Apollo AUM ~$678B cushions access. Reinsurance rates rose ~10% in 2024; vendor and talent scarcity (US unemployment ~3.8% in 2024) raise supplier leverage.

| Metric | 2024 value |

|---|---|

| Invested assets | $270B |

| Private debt AUM | $1.3T |

| Apollo AUM | $678B |

| Reinsurance rates | +10% |

| US unemployment | 3.8% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Athene. Evaluates supplier and buyer power, identifies disruptive threats and substitutes, and highlights barriers protecting incumbency; fully editable for reports and decks.

Athene Porter's Five Forces delivers a one-sheet, customizable view of competitive pressure—toggle inputs, generate an instant spider chart, and copy-ready visuals to relieve analysis bottlenecks and speed confident strategic decisions.

Customers Bargaining Power

Rate-sensitive retail annuity buyers

Rate-sensitive retail annuity buyers intensely compare credited rates, caps, and bonuses across carriers; transparent rate sheets and online aggregators heighten price sensitivity. Surrender schedules—commonly 5–10 years—curb in-force switching but do not deter purchase-level shopping. With the 10-year Treasury near 4.5% in 2024, buyer leverage on new business pricing increased materially.

Intermediated distribution (IMOs, banks, advisors)

Distributors (IMOs, banks, advisors) steer product flow, negotiate compensation and marketing support, and gatekeep shelf space and training access, boosting buyer power; in 2024 intermediated channels handled the majority of U.S. retail annuity sales per LIMRA. Carriers thus compete on service, speed and product breadth to win placement. Concentrated IMOs can extract concessions and prefer carriers offering strong back-office support.

Pension risk transfer sponsors

Corporate plan sponsors run competitive auctions that commonly draw 5–10 insurers, keeping pricing margins tight and terms highly standardized. Large deals, typically exceeding $1 billion, amplify buyer bargaining power through scale and portfolio leverage. Pricing spreads in the market are often single-digit basis points, so execution certainty and AA/A-rated balance sheet strength differentiate insurers but do not eliminate sponsor leverage.

Reinsurance ceding companies

Reinsurance ceding companies wield strong bargaining power as primary insurers can shop ceded blocks on price and collateral; Athene, with over $300 billion of invested assets in 2024, faces counterparties that route deal flow by economic terms and ratings.

Sophisticated buyers demand transparency and bespoke structures, pushing reinsurers to offer tailored collateral and reporting; deal allocation often favors counterparties with A‑range or higher ratings.

- Shopability: price + collateral

- Deal flow: terms + counterparty strength

- Sophistication: transparency + bespoke

- Negotiating power: elevated

Policyholder protections and switching frictions

Regulatory disclosures such as NAIC annuity buyer guides improve transparency and support buyer power at sale, while surrender charges commonly run 5–10% in early years and tax rules make post-issue mobility costly; industry lapse rates historically cluster around 4–7% (2024 estimates), so leverage is strongest at point of sale and weakens later, with product complexity both obstructing and enabling negotiation.

- Disclosure: NAIC/state rules boost comparability

- Surrender charges: 5–10% early years

- Tax impact: taxes on gains deter switching

- Timing: highest buyer leverage at sale

- Complexity: can reduce or increase negotiation power

Rate-sensitive annuity buyers boost purchases as 10y Treasury ~4.5% (2024)

Retail annuity buyers are highly rate-sensitive; with the 10-year Treasury ~4.5% in 2024 purchase leverage rose while surrender schedules (5–10 years) and taxes limit post-issue switching. Distributors (IMOs, banks, advisors) control shelf space—LIMRA shows intermediated channels drove the majority of 2024 U.S. retail annuity sales—raising buyer power. Corporate sponsors run auctions (often $1bn+), and reinsurers negotiate on price/collateral; Athene held >$300bn AUM in 2024.

| Metric | 2024 Value |

|---|---|

| 10y Treasury | ~4.5% |

| Surrender charges | 5–10% |

| Lapse rates | 4–7% |

| Athene AUM | >$300bn |

Preview the Actual Deliverable

Athene Porter's Five Forces Analysis

You’re previewing the exact Athene Porter’s Five Forces Analysis you will receive after purchase—no samples or placeholders. This professionally written, fully formatted document is ready for immediate download and use the moment you buy. No edits or setup required; the file shown is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Athene’s Porter’s Five Forces Analysis distills the insurer’s competitive landscape, highlighting buyer and supplier power, barriers to entry, rivalry, and substitute threats. It examines capital intensity, regulatory pressure, and distribution channel influence shaping margins and growth. The findings point to strategic levers for risk mitigation and value creation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Athene’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Capital and liquidity providers

Athene depends on wholesale funding, FHLB advances and cash markets to manage liquidity and growth, supporting roughly $270 billion of invested assets as of 2024. When credit tightens, higher cost of capital compresses spreads and returns on new business. Diversified funding sources and investment-grade ratings have reduced single-counterparty concentration. Macro cycles, however, can rapidly shift supplier power upward and raise funding costs.

Asset origination and managers

Athene’s yields depend on access to private credit, ABS and specialty assets sourced via external managers and partners, and scarcity can push manager fees higher and compress net spread. Competition for assets has tightened as private debt AUM expanded to roughly $1.3 trillion in 2024, boosting supplier leverage. Athene’s affiliated manager pipeline and sponsor scale—Apollo reported about $678 billion AUM in 2024—partially cushions this risk.

Reinsurance and retrocession counterparties

Third‑party reinsurance and retrocession pricing and capacity directly affect Athene’s capital efficiency and risk transfer; global reinsurance rates rose about 10% in 2024, tightening cost of capital and transfer economics. In volatile markets reinsurers demand higher margins and tighter terms, compressing Athene’s spread. Diversifying counterparties reduces dependency, while regulatory scrutiny of affiliated reinsurance alters bargaining leverage.

Technology, admin platforms, and data vendors

- High switching costs

- Vendor concentration

- Long contracts

- In-house mitigation

Specialized talent and advisory

Specialized actuarial, ALM and risk talent is scarce and cyclical, increasing supplier power for Athene; the tight 2024 U.S. labor market (unemployment ~3.8%) amplified wage inflation and retention-package costs, raising operating expenses and dependence on external advisors (legal, compliance).

- Actuarial/ALM scarcity raises wages and turnover risk

- Retention packages and wage inflation drive costs

- External advisors add fixed, cyclical regulatory spend

Wholesale funding stress, scarce private credit and rising reinsurance rates squeeze yields

Athene relies on wholesale funding, FHLB and cash markets for about $270B invested assets (2024); funding cost spikes compress spreads. Private credit/ABS scarcity (private debt AUM ~$1.3T in 2024) and manager fees pressure yield; Apollo AUM ~$678B cushions access. Reinsurance rates rose ~10% in 2024; vendor and talent scarcity (US unemployment ~3.8% in 2024) raise supplier leverage.

| Metric | 2024 value |

|---|---|

| Invested assets | $270B |

| Private debt AUM | $1.3T |

| Apollo AUM | $678B |

| Reinsurance rates | +10% |

| US unemployment | 3.8% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Athene. Evaluates supplier and buyer power, identifies disruptive threats and substitutes, and highlights barriers protecting incumbency; fully editable for reports and decks.

Athene Porter's Five Forces delivers a one-sheet, customizable view of competitive pressure—toggle inputs, generate an instant spider chart, and copy-ready visuals to relieve analysis bottlenecks and speed confident strategic decisions.

Customers Bargaining Power

Rate-sensitive retail annuity buyers

Rate-sensitive retail annuity buyers intensely compare credited rates, caps, and bonuses across carriers; transparent rate sheets and online aggregators heighten price sensitivity. Surrender schedules—commonly 5–10 years—curb in-force switching but do not deter purchase-level shopping. With the 10-year Treasury near 4.5% in 2024, buyer leverage on new business pricing increased materially.

Intermediated distribution (IMOs, banks, advisors)

Distributors (IMOs, banks, advisors) steer product flow, negotiate compensation and marketing support, and gatekeep shelf space and training access, boosting buyer power; in 2024 intermediated channels handled the majority of U.S. retail annuity sales per LIMRA. Carriers thus compete on service, speed and product breadth to win placement. Concentrated IMOs can extract concessions and prefer carriers offering strong back-office support.

Pension risk transfer sponsors

Corporate plan sponsors run competitive auctions that commonly draw 5–10 insurers, keeping pricing margins tight and terms highly standardized. Large deals, typically exceeding $1 billion, amplify buyer bargaining power through scale and portfolio leverage. Pricing spreads in the market are often single-digit basis points, so execution certainty and AA/A-rated balance sheet strength differentiate insurers but do not eliminate sponsor leverage.

Reinsurance ceding companies

Reinsurance ceding companies wield strong bargaining power as primary insurers can shop ceded blocks on price and collateral; Athene, with over $300 billion of invested assets in 2024, faces counterparties that route deal flow by economic terms and ratings.

Sophisticated buyers demand transparency and bespoke structures, pushing reinsurers to offer tailored collateral and reporting; deal allocation often favors counterparties with A‑range or higher ratings.

- Shopability: price + collateral

- Deal flow: terms + counterparty strength

- Sophistication: transparency + bespoke

- Negotiating power: elevated

Policyholder protections and switching frictions

Regulatory disclosures such as NAIC annuity buyer guides improve transparency and support buyer power at sale, while surrender charges commonly run 5–10% in early years and tax rules make post-issue mobility costly; industry lapse rates historically cluster around 4–7% (2024 estimates), so leverage is strongest at point of sale and weakens later, with product complexity both obstructing and enabling negotiation.

- Disclosure: NAIC/state rules boost comparability

- Surrender charges: 5–10% early years

- Tax impact: taxes on gains deter switching

- Timing: highest buyer leverage at sale

- Complexity: can reduce or increase negotiation power

Rate-sensitive annuity buyers boost purchases as 10y Treasury ~4.5% (2024)

Retail annuity buyers are highly rate-sensitive; with the 10-year Treasury ~4.5% in 2024 purchase leverage rose while surrender schedules (5–10 years) and taxes limit post-issue switching. Distributors (IMOs, banks, advisors) control shelf space—LIMRA shows intermediated channels drove the majority of 2024 U.S. retail annuity sales—raising buyer power. Corporate sponsors run auctions (often $1bn+), and reinsurers negotiate on price/collateral; Athene held >$300bn AUM in 2024.

| Metric | 2024 Value |

|---|---|

| 10y Treasury | ~4.5% |

| Surrender charges | 5–10% |

| Lapse rates | 4–7% |

| Athene AUM | >$300bn |

Preview the Actual Deliverable

Athene Porter's Five Forces Analysis

You’re previewing the exact Athene Porter’s Five Forces Analysis you will receive after purchase—no samples or placeholders. This professionally written, fully formatted document is ready for immediate download and use the moment you buy. No edits or setup required; the file shown is the deliverable.