Atlantic Union Bank Business Model Canvas

Regional Bank Business Model Canvas: Customer Value, Revenue Streams, and Scaling Insights

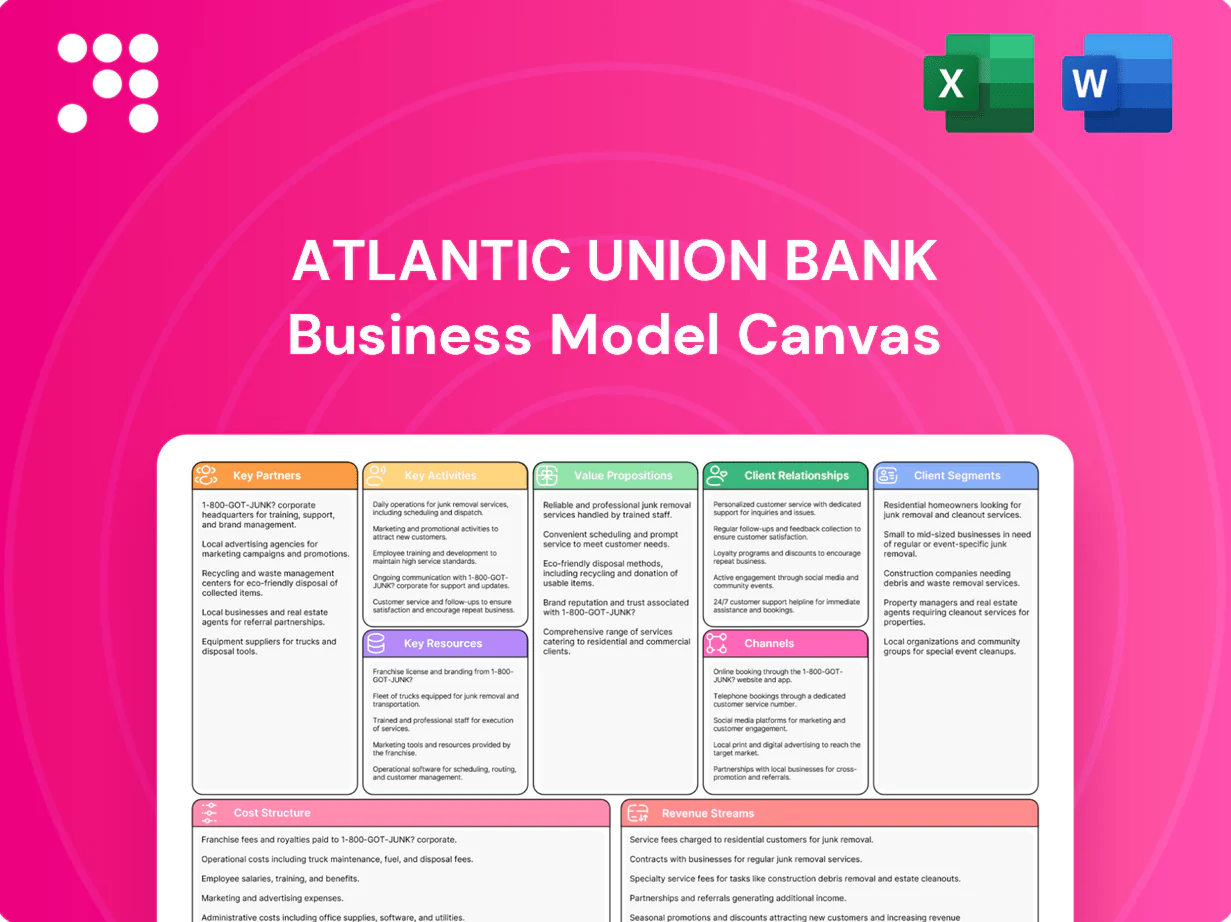

Explore Atlantic Union Bank’s Business Model Canvas to uncover how it creates customer value, scales regional market share, and optimizes revenue streams. This concise, professional canvas maps customer segments, channels, partnerships, and cost structure—ready for benchmarking or investor decks. Download the full Word/Excel files for a section-by-section strategic guide you can apply immediately.

Partnerships

Fintech and core banking vendors

Fintech and core banking vendors supply Atlantic Union with core processing, digital banking platforms, fraud analytics and payments rails, enabling rapid feature rollout and regulatory-grade uptime often contracted at 99.9%–99.99%. Co-development with vendors shortens time-to-market and lowers capex through shared roadmaps and staff integration. Strict SLAs and phased integration roadmaps align technology delivery with customer expectations.

Correspondent banks and liquidity providers

Correspondent banks and liquidity providers enable Atlantic Union Bank to clear wires, execute foreign exchange, and access off-balance-sheet liquidity, lowering funding costs and enhancing treasury functions; Atlantic Union reported total assets of $21.3 billion in 2024, improving pricing on wholesale funding by several basis points. Access to broader networks expands product scope and client reach, while shared credit lines and contingent facilities distribute risk and stabilize operations during stress.

Mortgage, insurance, and investment distributors

Third-party distributors help Atlantic Union Bank originate, service, and cross-sell mortgages, insurance, and wealth products, broadening noninterest fee income without owning every value-chain step.

Co-branded solutions increase customer stickiness and cross-sell rates; Atlantic Union, with roughly $29 billion in assets in 2024, leverages partners to extend reach.

Revenue-sharing arrangements align incentives, typically tying partner compensation to origination, servicing, and AUM growth.

Local community and public sector partners

Local engagement with municipalities, chambers and nonprofits strengthens trust and helped Atlantic Union Bank attract stable public deposits, supporting lending pipelines tied to municipal projects; as of 2024 the bank reported roughly 18.6 billion in deposits, underpinning community lending.

Community investment partners advance CRA goals through targeted financing and measurable impact, while deep local ties differentiate Atlantic Union from national banks in relationship-driven markets.

- Municipal engagement → steady public deposits

- Public projects → predictable lending pipeline

- CRA partnerships → measurable community impact

- Local ties → competitive differentiation

Regulatory, compliance, and audit advisors

Regulatory, compliance, and audit advisors ensure Atlantic Union Bank (AUB), a regional bank with roughly $34.4 billion in assets (2024), adheres to federal and state banking rules while strengthening BSA/AML, fair lending, and cybersecurity risk frameworks.

Independent reviews and audits improve internal controls and exam readiness, reducing remediation costs and regulatory penalties.

External guidance also accelerates compliant product launches by aligning new offerings with supervisory expectations and reducing time-to-market.

- External experts: federal/state rule adherence

- BSA/AML, fair lending, cybersecurity: enhanced frameworks

- Independent reviews: better controls & exam readiness

- Guidance: faster, compliant product launches

Fintech-led digital bank: $34.4B, 99.9%–99.99% SLAs

Fintech and core vendors deliver digital banking, fraud analytics and 99.9%–99.99% SLAs enabling faster launches. Correspondent banks and liquidity providers lower wholesale funding costs and support treasury functions for Atlantic Union (assets $34.4B; deposits $18.6B in 2024). Distributors, municipal and CRA partners broaden fee income, stabilize public deposits and expand community lending pipelines.

| Metric | 2024 |

|---|---|

| Total assets | $34.4B |

| Total deposits | $18.6B |

| Tech SLAs | 99.9%–99.99% |

What is included in the product

A comprehensive, pre-written business model tailored to Atlantic Union Bank’s strategy, covering nine BMC blocks—customer segments, channels, value propositions, revenue streams, key resources/activities, partnerships, cost structure, and customer relationships—with SWOT-linked insights on competitive advantages for presentations and investor discussions.

High-level view of Atlantic Union Bank’s business model with editable cells to quickly identify core banking components, streamline strategic planning, and save hours of formatting for boardrooms or teams.

Activities

Deposit gathering and relationship banking

Proactive acquisition of checking and savings accounts fuels Atlantic Union Bank’s low-cost funding, with deposits roughly $17 billion in 2024 supporting lending and liquidity. Relationship managers deepen share of wallet via personalized commercial and consumer outreach, increasing cross-sell rates. Competitive pricing, targeted promotions, and branch/digital service focus drive retention. Robust KYC and AML processes ensure compliant, efficient onboarding.

Credit underwriting and portfolio management

Rigorous underwriting supports Atlantic Union Bank’s consumer, mortgage, and commercial lending, with credit policies tightened through 2024 to limit default exposure. Ongoing monitoring and stress testing manage concentration and credit risk, keeping nonperforming assets near industry lows in 2024. Pricing balances risk-adjusted return and market competitiveness. Dedicated workout and servicing teams handle delinquencies and recoveries.

Digital and branch channel operations

Operate mobile, online, ATM, and a roughly 200-branch network across VA, NC, and MD, supporting Atlantic Union Bank's ~28 billion USD in assets (2024); optimize staffing and self-service to raise efficiency and lower operating expense ratios; ensure high availability, security, and usability with multi-factor auth and 99.9% uptime targets; continuously enhance channels driven by user feedback and usage analytics.

Treasury, ALM, and liquidity management

Align asset-liability durations, hedges and liquidity buffers to protect net interest margin in the 2024 rate environment (Fed funds 5.25-5.50%, 10-yr ~4.2%). Monitor interest rate risk and diversify the funding mix between core deposits and wholesale sources. Execute securities portfolio strategies for income and balance-sheet flexibility. Use regular stress tests to shape contingency funding plans.

- Duration and hedge calibration

- Funding mix monitoring

- Securities for income/liquidity

- Stress-test driven contingencies

Compliance, risk, and cybersecurity

Maintain robust regulatory compliance and operational resilience frameworks covering BSA/AML, model and vendor risk, and layered cyber defenses, with continuous monitoring of alerts and mandatory staff training to reduce breach and compliance incidents. Rapid incident response and audit readiness minimize downtime and regulatory penalties. Integration with enterprise risk management ensures controls scale with growth.

- BSA/AML monitoring

- Model & vendor risk management

- Cyber defenses & alert monitoring

- Staff training & rapid incident response

Deposits $17B and strict underwriting protect NIM

Proactive deposit acquisition and relationship management drive low‑cost funding (deposits ~$17B in 2024) to support diversified lending; rigorous underwriting, monitoring and workout teams keep credit risk controlled. Branch/digital operations (~200 branches) and tech investments focus on efficiency and uptime; ALM, hedging and stress tests protect NIM in a 2024 rate backdrop. Compliance, BSA/AML and cyber controls ensure regulatory resilience.

| Metric | 2024 |

|---|---|

| Deposits | $17B |

| Assets | $28B |

| Branches | ~200 |

| Fed funds | 5.25-5.50% |

| 10‑yr | ~4.2% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Atlantic Union Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview shows the same structured, editable file included in your download. When you complete your order you'll get the full, ready-to-use document in Word and Excel formats.

Regional Bank Business Model Canvas: Customer Value, Revenue Streams, and Scaling Insights

Explore Atlantic Union Bank’s Business Model Canvas to uncover how it creates customer value, scales regional market share, and optimizes revenue streams. This concise, professional canvas maps customer segments, channels, partnerships, and cost structure—ready for benchmarking or investor decks. Download the full Word/Excel files for a section-by-section strategic guide you can apply immediately.

Partnerships

Fintech and core banking vendors

Fintech and core banking vendors supply Atlantic Union with core processing, digital banking platforms, fraud analytics and payments rails, enabling rapid feature rollout and regulatory-grade uptime often contracted at 99.9%–99.99%. Co-development with vendors shortens time-to-market and lowers capex through shared roadmaps and staff integration. Strict SLAs and phased integration roadmaps align technology delivery with customer expectations.

Correspondent banks and liquidity providers

Correspondent banks and liquidity providers enable Atlantic Union Bank to clear wires, execute foreign exchange, and access off-balance-sheet liquidity, lowering funding costs and enhancing treasury functions; Atlantic Union reported total assets of $21.3 billion in 2024, improving pricing on wholesale funding by several basis points. Access to broader networks expands product scope and client reach, while shared credit lines and contingent facilities distribute risk and stabilize operations during stress.

Mortgage, insurance, and investment distributors

Third-party distributors help Atlantic Union Bank originate, service, and cross-sell mortgages, insurance, and wealth products, broadening noninterest fee income without owning every value-chain step.

Co-branded solutions increase customer stickiness and cross-sell rates; Atlantic Union, with roughly $29 billion in assets in 2024, leverages partners to extend reach.

Revenue-sharing arrangements align incentives, typically tying partner compensation to origination, servicing, and AUM growth.

Local community and public sector partners

Local engagement with municipalities, chambers and nonprofits strengthens trust and helped Atlantic Union Bank attract stable public deposits, supporting lending pipelines tied to municipal projects; as of 2024 the bank reported roughly 18.6 billion in deposits, underpinning community lending.

Community investment partners advance CRA goals through targeted financing and measurable impact, while deep local ties differentiate Atlantic Union from national banks in relationship-driven markets.

- Municipal engagement → steady public deposits

- Public projects → predictable lending pipeline

- CRA partnerships → measurable community impact

- Local ties → competitive differentiation

Regulatory, compliance, and audit advisors

Regulatory, compliance, and audit advisors ensure Atlantic Union Bank (AUB), a regional bank with roughly $34.4 billion in assets (2024), adheres to federal and state banking rules while strengthening BSA/AML, fair lending, and cybersecurity risk frameworks.

Independent reviews and audits improve internal controls and exam readiness, reducing remediation costs and regulatory penalties.

External guidance also accelerates compliant product launches by aligning new offerings with supervisory expectations and reducing time-to-market.

- External experts: federal/state rule adherence

- BSA/AML, fair lending, cybersecurity: enhanced frameworks

- Independent reviews: better controls & exam readiness

- Guidance: faster, compliant product launches

Fintech-led digital bank: $34.4B, 99.9%–99.99% SLAs

Fintech and core vendors deliver digital banking, fraud analytics and 99.9%–99.99% SLAs enabling faster launches. Correspondent banks and liquidity providers lower wholesale funding costs and support treasury functions for Atlantic Union (assets $34.4B; deposits $18.6B in 2024). Distributors, municipal and CRA partners broaden fee income, stabilize public deposits and expand community lending pipelines.

| Metric | 2024 |

|---|---|

| Total assets | $34.4B |

| Total deposits | $18.6B |

| Tech SLAs | 99.9%–99.99% |

What is included in the product

A comprehensive, pre-written business model tailored to Atlantic Union Bank’s strategy, covering nine BMC blocks—customer segments, channels, value propositions, revenue streams, key resources/activities, partnerships, cost structure, and customer relationships—with SWOT-linked insights on competitive advantages for presentations and investor discussions.

High-level view of Atlantic Union Bank’s business model with editable cells to quickly identify core banking components, streamline strategic planning, and save hours of formatting for boardrooms or teams.

Activities

Deposit gathering and relationship banking

Proactive acquisition of checking and savings accounts fuels Atlantic Union Bank’s low-cost funding, with deposits roughly $17 billion in 2024 supporting lending and liquidity. Relationship managers deepen share of wallet via personalized commercial and consumer outreach, increasing cross-sell rates. Competitive pricing, targeted promotions, and branch/digital service focus drive retention. Robust KYC and AML processes ensure compliant, efficient onboarding.

Credit underwriting and portfolio management

Rigorous underwriting supports Atlantic Union Bank’s consumer, mortgage, and commercial lending, with credit policies tightened through 2024 to limit default exposure. Ongoing monitoring and stress testing manage concentration and credit risk, keeping nonperforming assets near industry lows in 2024. Pricing balances risk-adjusted return and market competitiveness. Dedicated workout and servicing teams handle delinquencies and recoveries.

Digital and branch channel operations

Operate mobile, online, ATM, and a roughly 200-branch network across VA, NC, and MD, supporting Atlantic Union Bank's ~28 billion USD in assets (2024); optimize staffing and self-service to raise efficiency and lower operating expense ratios; ensure high availability, security, and usability with multi-factor auth and 99.9% uptime targets; continuously enhance channels driven by user feedback and usage analytics.

Treasury, ALM, and liquidity management

Align asset-liability durations, hedges and liquidity buffers to protect net interest margin in the 2024 rate environment (Fed funds 5.25-5.50%, 10-yr ~4.2%). Monitor interest rate risk and diversify the funding mix between core deposits and wholesale sources. Execute securities portfolio strategies for income and balance-sheet flexibility. Use regular stress tests to shape contingency funding plans.

- Duration and hedge calibration

- Funding mix monitoring

- Securities for income/liquidity

- Stress-test driven contingencies

Compliance, risk, and cybersecurity

Maintain robust regulatory compliance and operational resilience frameworks covering BSA/AML, model and vendor risk, and layered cyber defenses, with continuous monitoring of alerts and mandatory staff training to reduce breach and compliance incidents. Rapid incident response and audit readiness minimize downtime and regulatory penalties. Integration with enterprise risk management ensures controls scale with growth.

- BSA/AML monitoring

- Model & vendor risk management

- Cyber defenses & alert monitoring

- Staff training & rapid incident response

Deposits $17B and strict underwriting protect NIM

Proactive deposit acquisition and relationship management drive low‑cost funding (deposits ~$17B in 2024) to support diversified lending; rigorous underwriting, monitoring and workout teams keep credit risk controlled. Branch/digital operations (~200 branches) and tech investments focus on efficiency and uptime; ALM, hedging and stress tests protect NIM in a 2024 rate backdrop. Compliance, BSA/AML and cyber controls ensure regulatory resilience.

| Metric | 2024 |

|---|---|

| Deposits | $17B |

| Assets | $28B |

| Branches | ~200 |

| Fed funds | 5.25-5.50% |

| 10‑yr | ~4.2% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Atlantic Union Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview shows the same structured, editable file included in your download. When you complete your order you'll get the full, ready-to-use document in Word and Excel formats.

Original: $10.00

-65%$10.00

$3.50Description

Regional Bank Business Model Canvas: Customer Value, Revenue Streams, and Scaling Insights

Explore Atlantic Union Bank’s Business Model Canvas to uncover how it creates customer value, scales regional market share, and optimizes revenue streams. This concise, professional canvas maps customer segments, channels, partnerships, and cost structure—ready for benchmarking or investor decks. Download the full Word/Excel files for a section-by-section strategic guide you can apply immediately.

Partnerships

Fintech and core banking vendors

Fintech and core banking vendors supply Atlantic Union with core processing, digital banking platforms, fraud analytics and payments rails, enabling rapid feature rollout and regulatory-grade uptime often contracted at 99.9%–99.99%. Co-development with vendors shortens time-to-market and lowers capex through shared roadmaps and staff integration. Strict SLAs and phased integration roadmaps align technology delivery with customer expectations.

Correspondent banks and liquidity providers

Correspondent banks and liquidity providers enable Atlantic Union Bank to clear wires, execute foreign exchange, and access off-balance-sheet liquidity, lowering funding costs and enhancing treasury functions; Atlantic Union reported total assets of $21.3 billion in 2024, improving pricing on wholesale funding by several basis points. Access to broader networks expands product scope and client reach, while shared credit lines and contingent facilities distribute risk and stabilize operations during stress.

Mortgage, insurance, and investment distributors

Third-party distributors help Atlantic Union Bank originate, service, and cross-sell mortgages, insurance, and wealth products, broadening noninterest fee income without owning every value-chain step.

Co-branded solutions increase customer stickiness and cross-sell rates; Atlantic Union, with roughly $29 billion in assets in 2024, leverages partners to extend reach.

Revenue-sharing arrangements align incentives, typically tying partner compensation to origination, servicing, and AUM growth.

Local community and public sector partners

Local engagement with municipalities, chambers and nonprofits strengthens trust and helped Atlantic Union Bank attract stable public deposits, supporting lending pipelines tied to municipal projects; as of 2024 the bank reported roughly 18.6 billion in deposits, underpinning community lending.

Community investment partners advance CRA goals through targeted financing and measurable impact, while deep local ties differentiate Atlantic Union from national banks in relationship-driven markets.

- Municipal engagement → steady public deposits

- Public projects → predictable lending pipeline

- CRA partnerships → measurable community impact

- Local ties → competitive differentiation

Regulatory, compliance, and audit advisors

Regulatory, compliance, and audit advisors ensure Atlantic Union Bank (AUB), a regional bank with roughly $34.4 billion in assets (2024), adheres to federal and state banking rules while strengthening BSA/AML, fair lending, and cybersecurity risk frameworks.

Independent reviews and audits improve internal controls and exam readiness, reducing remediation costs and regulatory penalties.

External guidance also accelerates compliant product launches by aligning new offerings with supervisory expectations and reducing time-to-market.

- External experts: federal/state rule adherence

- BSA/AML, fair lending, cybersecurity: enhanced frameworks

- Independent reviews: better controls & exam readiness

- Guidance: faster, compliant product launches

Fintech-led digital bank: $34.4B, 99.9%–99.99% SLAs

Fintech and core vendors deliver digital banking, fraud analytics and 99.9%–99.99% SLAs enabling faster launches. Correspondent banks and liquidity providers lower wholesale funding costs and support treasury functions for Atlantic Union (assets $34.4B; deposits $18.6B in 2024). Distributors, municipal and CRA partners broaden fee income, stabilize public deposits and expand community lending pipelines.

| Metric | 2024 |

|---|---|

| Total assets | $34.4B |

| Total deposits | $18.6B |

| Tech SLAs | 99.9%–99.99% |

What is included in the product

A comprehensive, pre-written business model tailored to Atlantic Union Bank’s strategy, covering nine BMC blocks—customer segments, channels, value propositions, revenue streams, key resources/activities, partnerships, cost structure, and customer relationships—with SWOT-linked insights on competitive advantages for presentations and investor discussions.

High-level view of Atlantic Union Bank’s business model with editable cells to quickly identify core banking components, streamline strategic planning, and save hours of formatting for boardrooms or teams.

Activities

Deposit gathering and relationship banking

Proactive acquisition of checking and savings accounts fuels Atlantic Union Bank’s low-cost funding, with deposits roughly $17 billion in 2024 supporting lending and liquidity. Relationship managers deepen share of wallet via personalized commercial and consumer outreach, increasing cross-sell rates. Competitive pricing, targeted promotions, and branch/digital service focus drive retention. Robust KYC and AML processes ensure compliant, efficient onboarding.

Credit underwriting and portfolio management

Rigorous underwriting supports Atlantic Union Bank’s consumer, mortgage, and commercial lending, with credit policies tightened through 2024 to limit default exposure. Ongoing monitoring and stress testing manage concentration and credit risk, keeping nonperforming assets near industry lows in 2024. Pricing balances risk-adjusted return and market competitiveness. Dedicated workout and servicing teams handle delinquencies and recoveries.

Digital and branch channel operations

Operate mobile, online, ATM, and a roughly 200-branch network across VA, NC, and MD, supporting Atlantic Union Bank's ~28 billion USD in assets (2024); optimize staffing and self-service to raise efficiency and lower operating expense ratios; ensure high availability, security, and usability with multi-factor auth and 99.9% uptime targets; continuously enhance channels driven by user feedback and usage analytics.

Treasury, ALM, and liquidity management

Align asset-liability durations, hedges and liquidity buffers to protect net interest margin in the 2024 rate environment (Fed funds 5.25-5.50%, 10-yr ~4.2%). Monitor interest rate risk and diversify the funding mix between core deposits and wholesale sources. Execute securities portfolio strategies for income and balance-sheet flexibility. Use regular stress tests to shape contingency funding plans.

- Duration and hedge calibration

- Funding mix monitoring

- Securities for income/liquidity

- Stress-test driven contingencies

Compliance, risk, and cybersecurity

Maintain robust regulatory compliance and operational resilience frameworks covering BSA/AML, model and vendor risk, and layered cyber defenses, with continuous monitoring of alerts and mandatory staff training to reduce breach and compliance incidents. Rapid incident response and audit readiness minimize downtime and regulatory penalties. Integration with enterprise risk management ensures controls scale with growth.

- BSA/AML monitoring

- Model & vendor risk management

- Cyber defenses & alert monitoring

- Staff training & rapid incident response

Deposits $17B and strict underwriting protect NIM

Proactive deposit acquisition and relationship management drive low‑cost funding (deposits ~$17B in 2024) to support diversified lending; rigorous underwriting, monitoring and workout teams keep credit risk controlled. Branch/digital operations (~200 branches) and tech investments focus on efficiency and uptime; ALM, hedging and stress tests protect NIM in a 2024 rate backdrop. Compliance, BSA/AML and cyber controls ensure regulatory resilience.

| Metric | 2024 |

|---|---|

| Deposits | $17B |

| Assets | $28B |

| Branches | ~200 |

| Fed funds | 5.25-5.50% |

| 10‑yr | ~4.2% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Atlantic Union Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview shows the same structured, editable file included in your download. When you complete your order you'll get the full, ready-to-use document in Word and Excel formats.