Atlantic Union Bank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

This snapshot highlights Atlantic Union Bank’s competitive pressures, from regional rivalry to digital disruptors, but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to the bank. Gain the actionable insights needed to inform investments, strategy, or presentations—get the consultant-grade report now.

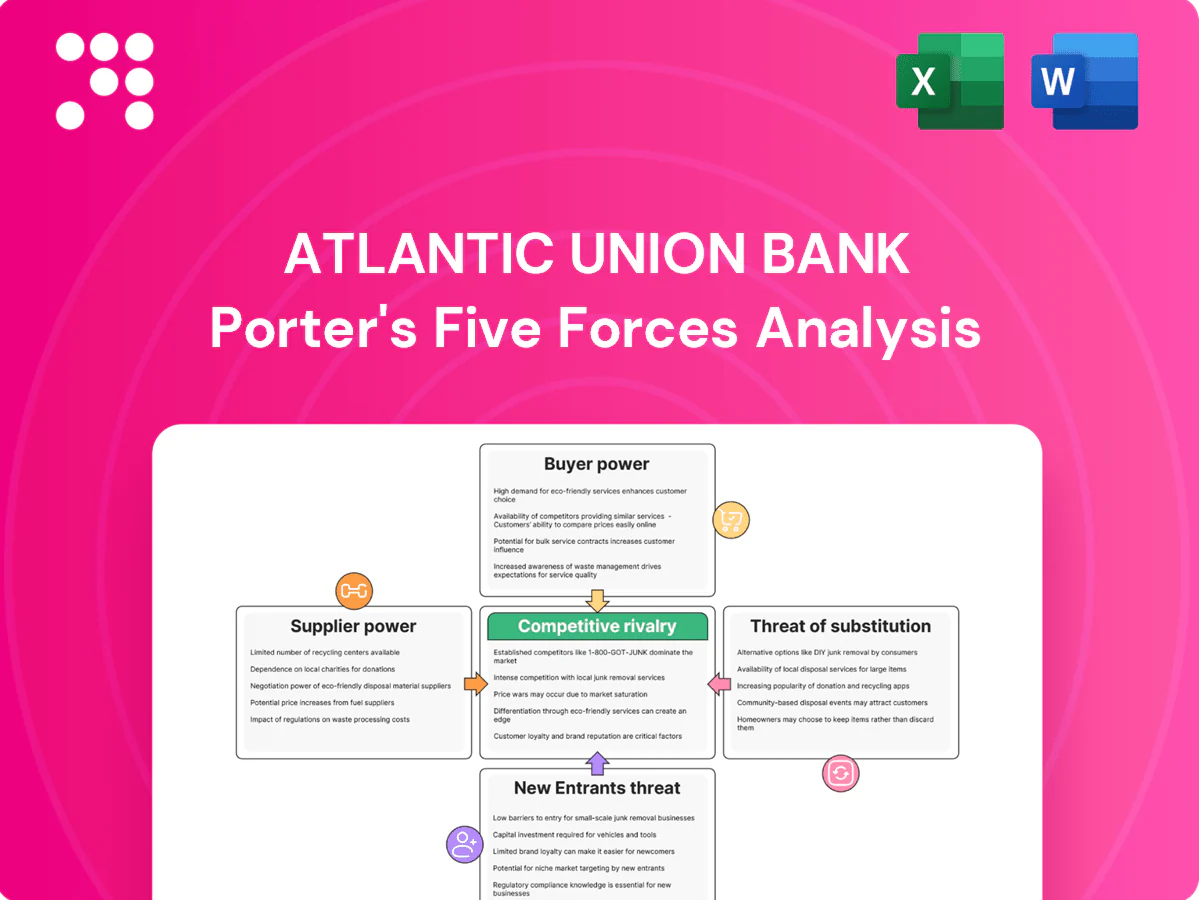

Suppliers Bargaining Power

Concentrated core tech vendors

Atlantic Union Bank depends on a small set of core banking processors, digital banking platforms and payments networks with limited alternatives, increasing vendor leverage and raising switching costs and lock-in. Contract renegotiations and system upgrades are often costly and time-consuming, complicating migration. As a regional bank, scale provides some pricing and service leverage but does not eliminate dependency on concentrated tech vendors.

Funding from deposits and wholesale

Depositors provide Atlantic Union Bank low-cost core funding but can push rates higher in tight liquidity, raising funding costs and compressing margins. Wholesale providers like the FHLB and brokered CDs acquire leverage in stressed markets, applying haircuts and covenants that increase funding rigidity. A diversified funding mix reduces single-source dependency, while strong liquidity management and deep counterparty relationships mitigate sudden spikes in supplier power.

Talent and compliance expertise

Skilled bankers, credit officers and compliance staff remain scarce, giving labor suppliers notable negotiating power for Atlantic Union Bank. Regulatory complexity in Virginia, North Carolina and Maryland raises premiums for experienced hires, reflected in 2024 financial-services wage inflation around 4–6%. Rising retention packages and signing bonuses, often adding 10–20% to base pay, can pressure margins. Investment in training and culture reduces dependency on costly external recruiting.

Data, cybersecurity, and cloud providers

Data, cybersecurity, and cloud services pose critical supplier power for Atlantic Union Bank as a few enterprise vendors dominate infrastructure: in 2024 AWS, Microsoft Azure and Google Cloud held roughly 33%, 23% and 11% of cloud IaaS respectively, concentrating risk and fraud-control dependencies. Security certifications and custom integrations raise switching costs, while incident-response SLAs and pricing often favor providers; adopting multi-vendor architectures and selective in-house controls can rebalance leverage.

- Concentration: top three cloud providers ≈67% share

- Switching costs: certification + integration overhead

- Provider advantage: SLAs/pricing tilt to vendors

- Mitigation: multi-vendor + in-house controls

Card networks and payments rails

Card networks and ACH rails wield strong supplier power: Visa and Mastercard handle roughly 80% of card volume in the US, setting interchange and network rules that limit Atlantic Union Bank’s bargaining on fees and mandates; ACH operators processed about 31 billion payments in 2023, reinforcing standardized fee and compliance regimes. Interchange dynamics (commonly 1–2% on credit) and regulatory compliance constrain pricing flexibility, while higher volumes and routing/product mix optimization offer partial offset.

- Visa/Mastercard ~80% combined card volume

- ACH ~31B payments in 2023

- Interchange typically 1–2% on credit

- Volume, product mix, routing optimization mitigate fee pressure

Concentrated cloud and card networks raise costs — diversify vendors, controls, funding

Supplier power is high: concentrated cloud vendors (AWS 33%, Azure 23%, GCP 11% in 2024) and card networks (Visa/Mastercard ~80% volume) set pricing and SLAs, raising switching costs. Depositors and wholesale funders (FHLB, brokered CDs) can push funding costs in stress; 2024 wage inflation in financial services ~4–6% boosts labor costs. Multi-vendor, in-house controls and funding diversification mitigate risk.

| Item | Metric |

|---|---|

| Cloud share (2024) | AWS 33% / Azure 23% / GCP 11% |

| Card volume | Visa+MC ~80% |

| ACH (2023) | 31B payments |

| Wage inflation (2024) | 4–6% |

What is included in the product

Tailored exclusively for Atlantic Union Bank, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks specific to its regional banking footprint. It evaluates supplier and buyer power, threat of substitutes and entrants, and identifies disruptive forces that could erode market share.

One-sheet Porter's Five Forces for Atlantic Union Bank — clear, customizable pressure levels with an instant spider chart to pinpoint competitive pain points and guide strategic actions.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors compare savings and CD rates across banks and fintechs—online platforms advertised yields above 4% in 2024 while the federal funds rate was near 5.25%, heightening customer bargaining power. In rising-rate cycles customers demand higher yields or move funds, forcing Atlantic Union to balance retention with margin protection. Relationship bundling (mortgages, wealth, payments) reduces pure rate shopping and stabilizes deposit costs.

Commercial and government clients

Large commercial and government clients negotiate aggressively on pricing, covenants and ancillary services, leveraging relationships with regional and national banks; their switching costs are moderate because onboarding and liquidity setups are complex but often justified by materially better terms. These clients routinely solicit competitive bids, so Atlantic Union’s tailored treasury solutions and fast service responsiveness are key defenses to preserve spreads and fee income.

Digital-first retail users

Digital-first retail users now expect seamless mobile experiences, instant payments, and low fees; 85% of US consumers used mobile banking in 2024, raising baseline expectations. Poor UX quickly drives churn to neobanks and big-bank apps with superior interfaces. Fee- and rate-comparison tools make pricing highly transparent, while continuous app enhancements narrow experience gaps and reduce customer leverage.

Mortgage and small-business borrowers

Mortgage and small-business borrowers shop aggressively across banks, credit unions and non-bank lenders; points, quoted rates and speed of closing are primary differentiators. Pre-approvals and streamlined underwriting lower switching incentives, yet local relationship banking remains influential in AUB’s Virginia/North Carolina footprint; AUB assets ~30 billion and 30-year fixed ~7.0% (Freddie Mac, 2024).

- Competitive shopping across channels

- Rate/points/turnaround drive wins

- Pre-approvals curb churn

- Local relationships boost retention

Wealth and investment clients

Wealth and investment clients benchmark fees and performance against robo and wirehouse options; robo-advisors held roughly $1.4 trillion AUM in 2024, increasing price transparency. Open-architecture products raise comparability and buyer power. Holistic planning and bank integration can justify premium pricing when fiduciary standards and transparency drive retention.

- Robo AUM ~ $1.4T (2024)

- Average advisory fee ~0.85% (industry)

- Open architecture increases switch propensity

- Fiduciary duty and transparency = retention

Depositors chase >4%; fed ~5.25%

Customers wield high bargaining power: depositors chased >4% online yields while fed funds were ~5.25% (2024), digital UX expectations rose with 85% mobile banking adoption, and large commercial clients demand bespoke pricing. Wealth clients compare robo AUM ~$1.4T; mortgages face 7.0% 30-year rates, pressuring margins.

| Metric | 2024 |

|---|---|

| Fed funds | ~5.25% |

| Online yields | >4% |

| Mobile users | 85% |

| Robo AUM | $1.4T |

Same Document Delivered

Atlantic Union Bank Porter's Five Forces Analysis

This preview shows the exact Atlantic Union Bank Porter’s Five Forces analysis you’ll receive—no placeholders, no mockups. The full document is professionally formatted, ready for immediate download upon purchase. What you see here is precisely the deliverable you’ll get.

Go Beyond the Preview—Access the Full Strategic Report

This snapshot highlights Atlantic Union Bank’s competitive pressures, from regional rivalry to digital disruptors, but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to the bank. Gain the actionable insights needed to inform investments, strategy, or presentations—get the consultant-grade report now.

Suppliers Bargaining Power

Concentrated core tech vendors

Atlantic Union Bank depends on a small set of core banking processors, digital banking platforms and payments networks with limited alternatives, increasing vendor leverage and raising switching costs and lock-in. Contract renegotiations and system upgrades are often costly and time-consuming, complicating migration. As a regional bank, scale provides some pricing and service leverage but does not eliminate dependency on concentrated tech vendors.

Funding from deposits and wholesale

Depositors provide Atlantic Union Bank low-cost core funding but can push rates higher in tight liquidity, raising funding costs and compressing margins. Wholesale providers like the FHLB and brokered CDs acquire leverage in stressed markets, applying haircuts and covenants that increase funding rigidity. A diversified funding mix reduces single-source dependency, while strong liquidity management and deep counterparty relationships mitigate sudden spikes in supplier power.

Talent and compliance expertise

Skilled bankers, credit officers and compliance staff remain scarce, giving labor suppliers notable negotiating power for Atlantic Union Bank. Regulatory complexity in Virginia, North Carolina and Maryland raises premiums for experienced hires, reflected in 2024 financial-services wage inflation around 4–6%. Rising retention packages and signing bonuses, often adding 10–20% to base pay, can pressure margins. Investment in training and culture reduces dependency on costly external recruiting.

Data, cybersecurity, and cloud providers

Data, cybersecurity, and cloud services pose critical supplier power for Atlantic Union Bank as a few enterprise vendors dominate infrastructure: in 2024 AWS, Microsoft Azure and Google Cloud held roughly 33%, 23% and 11% of cloud IaaS respectively, concentrating risk and fraud-control dependencies. Security certifications and custom integrations raise switching costs, while incident-response SLAs and pricing often favor providers; adopting multi-vendor architectures and selective in-house controls can rebalance leverage.

- Concentration: top three cloud providers ≈67% share

- Switching costs: certification + integration overhead

- Provider advantage: SLAs/pricing tilt to vendors

- Mitigation: multi-vendor + in-house controls

Card networks and payments rails

Card networks and ACH rails wield strong supplier power: Visa and Mastercard handle roughly 80% of card volume in the US, setting interchange and network rules that limit Atlantic Union Bank’s bargaining on fees and mandates; ACH operators processed about 31 billion payments in 2023, reinforcing standardized fee and compliance regimes. Interchange dynamics (commonly 1–2% on credit) and regulatory compliance constrain pricing flexibility, while higher volumes and routing/product mix optimization offer partial offset.

- Visa/Mastercard ~80% combined card volume

- ACH ~31B payments in 2023

- Interchange typically 1–2% on credit

- Volume, product mix, routing optimization mitigate fee pressure

Concentrated cloud and card networks raise costs — diversify vendors, controls, funding

Supplier power is high: concentrated cloud vendors (AWS 33%, Azure 23%, GCP 11% in 2024) and card networks (Visa/Mastercard ~80% volume) set pricing and SLAs, raising switching costs. Depositors and wholesale funders (FHLB, brokered CDs) can push funding costs in stress; 2024 wage inflation in financial services ~4–6% boosts labor costs. Multi-vendor, in-house controls and funding diversification mitigate risk.

| Item | Metric |

|---|---|

| Cloud share (2024) | AWS 33% / Azure 23% / GCP 11% |

| Card volume | Visa+MC ~80% |

| ACH (2023) | 31B payments |

| Wage inflation (2024) | 4–6% |

What is included in the product

Tailored exclusively for Atlantic Union Bank, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks specific to its regional banking footprint. It evaluates supplier and buyer power, threat of substitutes and entrants, and identifies disruptive forces that could erode market share.

One-sheet Porter's Five Forces for Atlantic Union Bank — clear, customizable pressure levels with an instant spider chart to pinpoint competitive pain points and guide strategic actions.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors compare savings and CD rates across banks and fintechs—online platforms advertised yields above 4% in 2024 while the federal funds rate was near 5.25%, heightening customer bargaining power. In rising-rate cycles customers demand higher yields or move funds, forcing Atlantic Union to balance retention with margin protection. Relationship bundling (mortgages, wealth, payments) reduces pure rate shopping and stabilizes deposit costs.

Commercial and government clients

Large commercial and government clients negotiate aggressively on pricing, covenants and ancillary services, leveraging relationships with regional and national banks; their switching costs are moderate because onboarding and liquidity setups are complex but often justified by materially better terms. These clients routinely solicit competitive bids, so Atlantic Union’s tailored treasury solutions and fast service responsiveness are key defenses to preserve spreads and fee income.

Digital-first retail users

Digital-first retail users now expect seamless mobile experiences, instant payments, and low fees; 85% of US consumers used mobile banking in 2024, raising baseline expectations. Poor UX quickly drives churn to neobanks and big-bank apps with superior interfaces. Fee- and rate-comparison tools make pricing highly transparent, while continuous app enhancements narrow experience gaps and reduce customer leverage.

Mortgage and small-business borrowers

Mortgage and small-business borrowers shop aggressively across banks, credit unions and non-bank lenders; points, quoted rates and speed of closing are primary differentiators. Pre-approvals and streamlined underwriting lower switching incentives, yet local relationship banking remains influential in AUB’s Virginia/North Carolina footprint; AUB assets ~30 billion and 30-year fixed ~7.0% (Freddie Mac, 2024).

- Competitive shopping across channels

- Rate/points/turnaround drive wins

- Pre-approvals curb churn

- Local relationships boost retention

Wealth and investment clients

Wealth and investment clients benchmark fees and performance against robo and wirehouse options; robo-advisors held roughly $1.4 trillion AUM in 2024, increasing price transparency. Open-architecture products raise comparability and buyer power. Holistic planning and bank integration can justify premium pricing when fiduciary standards and transparency drive retention.

- Robo AUM ~ $1.4T (2024)

- Average advisory fee ~0.85% (industry)

- Open architecture increases switch propensity

- Fiduciary duty and transparency = retention

Depositors chase >4%; fed ~5.25%

Customers wield high bargaining power: depositors chased >4% online yields while fed funds were ~5.25% (2024), digital UX expectations rose with 85% mobile banking adoption, and large commercial clients demand bespoke pricing. Wealth clients compare robo AUM ~$1.4T; mortgages face 7.0% 30-year rates, pressuring margins.

| Metric | 2024 |

|---|---|

| Fed funds | ~5.25% |

| Online yields | >4% |

| Mobile users | 85% |

| Robo AUM | $1.4T |

Same Document Delivered

Atlantic Union Bank Porter's Five Forces Analysis

This preview shows the exact Atlantic Union Bank Porter’s Five Forces analysis you’ll receive—no placeholders, no mockups. The full document is professionally formatted, ready for immediate download upon purchase. What you see here is precisely the deliverable you’ll get.

Description

Go Beyond the Preview—Access the Full Strategic Report

This snapshot highlights Atlantic Union Bank’s competitive pressures, from regional rivalry to digital disruptors, but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to the bank. Gain the actionable insights needed to inform investments, strategy, or presentations—get the consultant-grade report now.

Suppliers Bargaining Power

Concentrated core tech vendors

Atlantic Union Bank depends on a small set of core banking processors, digital banking platforms and payments networks with limited alternatives, increasing vendor leverage and raising switching costs and lock-in. Contract renegotiations and system upgrades are often costly and time-consuming, complicating migration. As a regional bank, scale provides some pricing and service leverage but does not eliminate dependency on concentrated tech vendors.

Funding from deposits and wholesale

Depositors provide Atlantic Union Bank low-cost core funding but can push rates higher in tight liquidity, raising funding costs and compressing margins. Wholesale providers like the FHLB and brokered CDs acquire leverage in stressed markets, applying haircuts and covenants that increase funding rigidity. A diversified funding mix reduces single-source dependency, while strong liquidity management and deep counterparty relationships mitigate sudden spikes in supplier power.

Talent and compliance expertise

Skilled bankers, credit officers and compliance staff remain scarce, giving labor suppliers notable negotiating power for Atlantic Union Bank. Regulatory complexity in Virginia, North Carolina and Maryland raises premiums for experienced hires, reflected in 2024 financial-services wage inflation around 4–6%. Rising retention packages and signing bonuses, often adding 10–20% to base pay, can pressure margins. Investment in training and culture reduces dependency on costly external recruiting.

Data, cybersecurity, and cloud providers

Data, cybersecurity, and cloud services pose critical supplier power for Atlantic Union Bank as a few enterprise vendors dominate infrastructure: in 2024 AWS, Microsoft Azure and Google Cloud held roughly 33%, 23% and 11% of cloud IaaS respectively, concentrating risk and fraud-control dependencies. Security certifications and custom integrations raise switching costs, while incident-response SLAs and pricing often favor providers; adopting multi-vendor architectures and selective in-house controls can rebalance leverage.

- Concentration: top three cloud providers ≈67% share

- Switching costs: certification + integration overhead

- Provider advantage: SLAs/pricing tilt to vendors

- Mitigation: multi-vendor + in-house controls

Card networks and payments rails

Card networks and ACH rails wield strong supplier power: Visa and Mastercard handle roughly 80% of card volume in the US, setting interchange and network rules that limit Atlantic Union Bank’s bargaining on fees and mandates; ACH operators processed about 31 billion payments in 2023, reinforcing standardized fee and compliance regimes. Interchange dynamics (commonly 1–2% on credit) and regulatory compliance constrain pricing flexibility, while higher volumes and routing/product mix optimization offer partial offset.

- Visa/Mastercard ~80% combined card volume

- ACH ~31B payments in 2023

- Interchange typically 1–2% on credit

- Volume, product mix, routing optimization mitigate fee pressure

Concentrated cloud and card networks raise costs — diversify vendors, controls, funding

Supplier power is high: concentrated cloud vendors (AWS 33%, Azure 23%, GCP 11% in 2024) and card networks (Visa/Mastercard ~80% volume) set pricing and SLAs, raising switching costs. Depositors and wholesale funders (FHLB, brokered CDs) can push funding costs in stress; 2024 wage inflation in financial services ~4–6% boosts labor costs. Multi-vendor, in-house controls and funding diversification mitigate risk.

| Item | Metric |

|---|---|

| Cloud share (2024) | AWS 33% / Azure 23% / GCP 11% |

| Card volume | Visa+MC ~80% |

| ACH (2023) | 31B payments |

| Wage inflation (2024) | 4–6% |

What is included in the product

Tailored exclusively for Atlantic Union Bank, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks specific to its regional banking footprint. It evaluates supplier and buyer power, threat of substitutes and entrants, and identifies disruptive forces that could erode market share.

One-sheet Porter's Five Forces for Atlantic Union Bank — clear, customizable pressure levels with an instant spider chart to pinpoint competitive pain points and guide strategic actions.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors compare savings and CD rates across banks and fintechs—online platforms advertised yields above 4% in 2024 while the federal funds rate was near 5.25%, heightening customer bargaining power. In rising-rate cycles customers demand higher yields or move funds, forcing Atlantic Union to balance retention with margin protection. Relationship bundling (mortgages, wealth, payments) reduces pure rate shopping and stabilizes deposit costs.

Commercial and government clients

Large commercial and government clients negotiate aggressively on pricing, covenants and ancillary services, leveraging relationships with regional and national banks; their switching costs are moderate because onboarding and liquidity setups are complex but often justified by materially better terms. These clients routinely solicit competitive bids, so Atlantic Union’s tailored treasury solutions and fast service responsiveness are key defenses to preserve spreads and fee income.

Digital-first retail users

Digital-first retail users now expect seamless mobile experiences, instant payments, and low fees; 85% of US consumers used mobile banking in 2024, raising baseline expectations. Poor UX quickly drives churn to neobanks and big-bank apps with superior interfaces. Fee- and rate-comparison tools make pricing highly transparent, while continuous app enhancements narrow experience gaps and reduce customer leverage.

Mortgage and small-business borrowers

Mortgage and small-business borrowers shop aggressively across banks, credit unions and non-bank lenders; points, quoted rates and speed of closing are primary differentiators. Pre-approvals and streamlined underwriting lower switching incentives, yet local relationship banking remains influential in AUB’s Virginia/North Carolina footprint; AUB assets ~30 billion and 30-year fixed ~7.0% (Freddie Mac, 2024).

- Competitive shopping across channels

- Rate/points/turnaround drive wins

- Pre-approvals curb churn

- Local relationships boost retention

Wealth and investment clients

Wealth and investment clients benchmark fees and performance against robo and wirehouse options; robo-advisors held roughly $1.4 trillion AUM in 2024, increasing price transparency. Open-architecture products raise comparability and buyer power. Holistic planning and bank integration can justify premium pricing when fiduciary standards and transparency drive retention.

- Robo AUM ~ $1.4T (2024)

- Average advisory fee ~0.85% (industry)

- Open architecture increases switch propensity

- Fiduciary duty and transparency = retention

Depositors chase >4%; fed ~5.25%

Customers wield high bargaining power: depositors chased >4% online yields while fed funds were ~5.25% (2024), digital UX expectations rose with 85% mobile banking adoption, and large commercial clients demand bespoke pricing. Wealth clients compare robo AUM ~$1.4T; mortgages face 7.0% 30-year rates, pressuring margins.

| Metric | 2024 |

|---|---|

| Fed funds | ~5.25% |

| Online yields | >4% |

| Mobile users | 85% |

| Robo AUM | $1.4T |

Same Document Delivered

Atlantic Union Bank Porter's Five Forces Analysis

This preview shows the exact Atlantic Union Bank Porter’s Five Forces analysis you’ll receive—no placeholders, no mockups. The full document is professionally formatted, ready for immediate download upon purchase. What you see here is precisely the deliverable you’ll get.