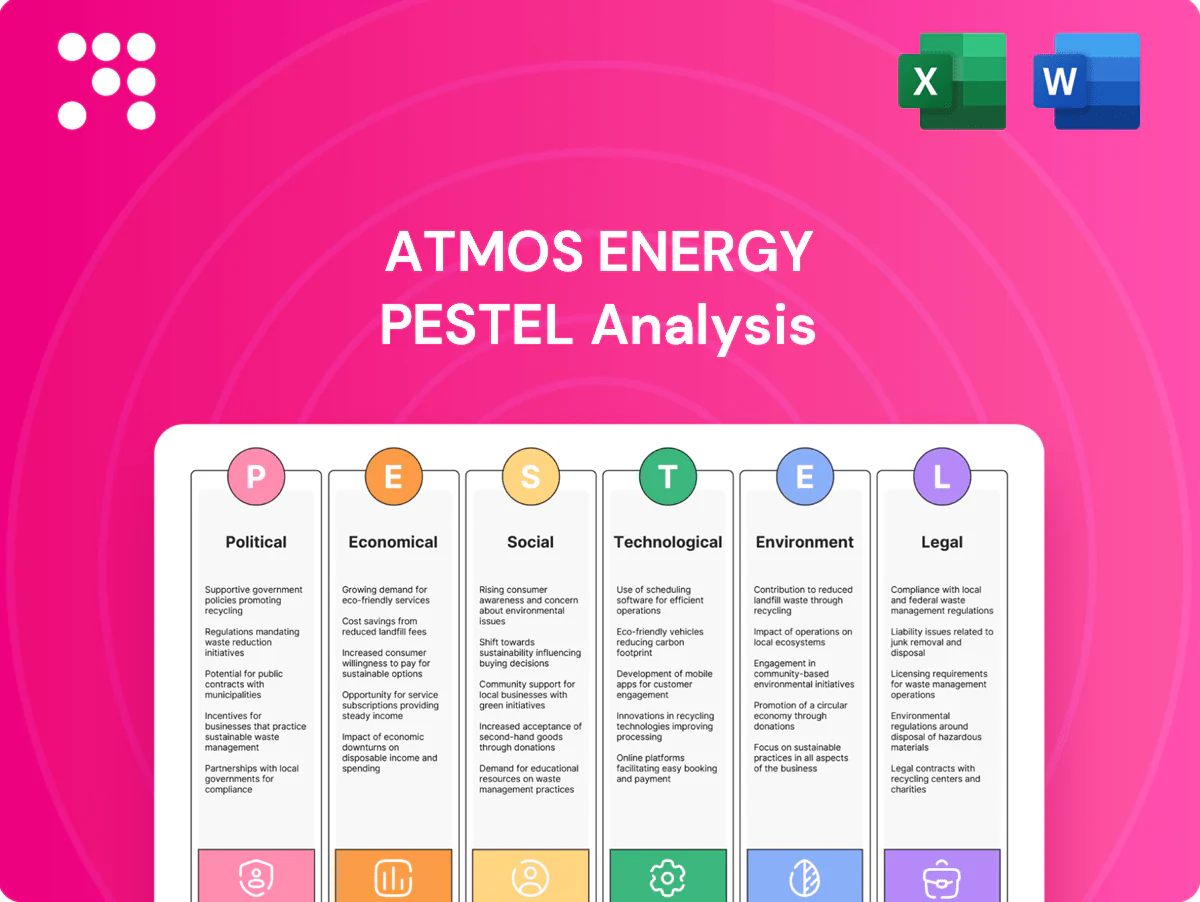

Atmos Energy PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, and environmental forces are reshaping Atmos Energy and what that means for risk and growth. Our concise PESTLE highlights regulatory, market, and technological pressures you need to know. Buy the full analysis for a detailed, actionable report with ready-to-use templates.

Political factors

State utility oversight

Atmos Energy’s rates and service standards are set at the state level by public utility commissions — 50 states plus DC — making state-level politics central to pricing and reliability. Shifts in political leadership can tilt commissions toward consumer relief or toward approving infrastructure investment and cost recovery. Maintaining stable regulatory relationships is essential for Atmos to secure timely recovery of capital spending and avoid earnings erosion.

Energy transition policies

State and municipal decarbonization agendas are reshaping demand and allowable utility investments, pressuring Atmos Energy—which serves about 3.1 million customers across eight states—to adapt capital plans. Electrification incentives from the 2022 Inflation Reduction Act and rising building performance standards can slow customer growth in gas heating. Concurrently, policy alignment on low‑carbon gas and RNG or hydrogen credits could create new revenue streams and eligible investments.

Infrastructure funding support

Political backing for resilience and safety programs enables regulators to approve cost-recovery riders and accelerated replacement mechanisms that improve cash flow for utility projects. Atmos Energy, serving about 3 million customers across eight states and roughly 90,000 miles of pipeline, can leverage federal and state grants or tax incentives to lower net capital burden. Shifts in fiscal priorities at state or federal levels could, however, tighten access to such public support and slow replacement schedules.

Local permitting dynamics

County and city councils directly control pipeline permits, street opening approvals and construction schedules, affecting Atmos Energy’s deployment across about 3 million customers in eight states (Atmos Energy 2024 reporting). Community pushback has caused multi-month delays and higher contractor/relocation costs on specific projects. Proactive stakeholder engagement and early permitting coordination reduce political friction and timetable risk.

- Permitting control: county/city councils

- Risk: multi-month delays, higher project costs

- Mitigation: early stakeholder engagement, coordinated permits

Geopolitical energy stance

National policy on domestic gas production and interstate infrastructure shapes Atmos Energy’s supply reliability, with US natural gas production reaching record levels in 2023 per EIA, supporting system resilience.

Federal and state support for North American gas and pipeline permitting has bolstered regional availability and helped stabilize domestic pricing since the US became the world’s top LNG exporter in 2022.

Adverse policy shifts or tighter permitting could raise volatility and procurement risk, increasing exposure to spot market price swings and supply interruptions.

- Policy influence: interstate permitting affects reliability

- Regional support: US top LNG exporter (2022) aids stability

- Risk: adverse shifts elevate volatility and procurement risk

Regulated gas service in 8 states serves ≈3.1M — politics, decarbonization, RNG

Atmos Energy’s state-regulated rates across eight states (≈3.1 million customers, Atmos 2024) make state politics decisive for cost recovery and earnings. Decarbonization policies and IRA incentives (2022) pressure demand for gas but create RNG/hydrogen credit opportunities. Local permitting delays raise project costs and timeline risk; federal support and record US gas production (EIA 2023) aid supply resilience.

| Metric | Value |

|---|---|

| Customers (2024) | ≈3.1M |

| Service states | 8 |

| Pipeline mileage | ≈90,000 mi |

| US gas record | 2023 (EIA) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Atmos Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into detailed, company-specific subpoints. Backed by current data and forward-looking insights, the analysis supports executives and investors in identifying regulatory risks, market opportunities and scenario-driven strategies.

Condensed Atmos Energy PESTLE highlights regulatory, economic, environmental and technological risks and opportunities in a single, easy-to-scan snapshot, helping teams make faster strategic decisions and align stakeholders without wading through lengthy reports.

Economic factors

Interest rate sensitivity

As a capital-intensive regulated gas utility (ATO), Atmos Energy’s earnings and customer rates are highly sensitive to financing costs; the US federal funds rate of 5.25–5.50% in mid-2025 raises borrowing costs and can pressure allowed ROE outcomes in rate cases. Higher rates increase debt service and may slow growth in rate base recoveries, while lower rates support accelerated system modernization and capital deployment.

Commodity price pass-through

Gas costs are largely passed through via purchased gas adjustment riders, limiting supplier margin exposure; EIA 2024 Henry Hub averaged about 2.83/MMBtu while 2022 spikes above 9/MMBtu demonstrated material customer bill impacts. Volatility elevates delinquencies, bad debt and political scrutiny. Robust hedging and storage strategies are pivotal to stabilizing bills.

Regional growth patterns

Population and industrial expansion in Atmos Energy service territories—Atmos serves about 3 million customers—support higher throughput and new connections; Texas population grew ~1.2% in 2023, fueling demand. Economic slowdowns (US GDP growth 2.5% in 2024) can curb commercial use and construction activity. A diversified customer mix across residential, commercial and industrial segments helps buffer cyclical impacts.

Labor and materials inflation

Rising costs for steel, plastic pipe, compressors and contract labor are tightening Atmos Energys capex budgets, increasing unit project costs and extending payback timelines.

Regulatory inflation escalators often lag actual input cost increases, creating timing mismatches that compress margins until rate cases catch up.

Active supply-chain management and multi-year procurement contracts help moderate volatility, secure materials and lock pricing to protect near-term capital plans.

- capex pressure

- regulatory lag

- procurement hedging

Weather-driven demand

Heating degree days drive Atmos Energy seasonal volumes and cash timing for its ~3 million customers; NOAA noted winter 2023–24 was warmer than the 1991–2020 average, compressing delivered volumes and shifting revenue into off-peak periods. Warmer winters can compress margins even where decoupling exists, while weather normalization adjustments and storage management mitigate earnings volatility.

- HDD sensitivity: major driver of monthly volumes

- Decoupling reduces but does not eliminate margin compression in warm winters

- Storage and normalization mechanisms optimize revenue timing and volatility

Regulated gas service in 8 states serves ≈3.1M — politics, decarbonization, RNG

Atmos Energy (≈3.0M customers) faces higher financing costs with US federal funds 5.25–5.50% (mid‑2025), pressuring debt service and rate-case ROE outcomes. 2024 Henry Hub averaged $2.83/MMBtu; gas pass-through limits margin but volatility raises delinquencies. Texas population +1.2% (2023) supports demand; warmer 2023–24 winter cut volumes per NOAA.

| Metric | Value | Near-term impact |

|---|---|---|

| Customers | ≈3,000,000 | Base demand |

| Fed funds | 5.25–5.50% | Higher capex cost |

| Henry Hub 2024 | $2.83/MMBtu | Pass-through volatility |

Preview the Actual Deliverable

Atmos Energy PESTLE Analysis

The preview shown here is the exact Atmos Energy PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, and environmental forces are reshaping Atmos Energy and what that means for risk and growth. Our concise PESTLE highlights regulatory, market, and technological pressures you need to know. Buy the full analysis for a detailed, actionable report with ready-to-use templates.

Political factors

State utility oversight

Atmos Energy’s rates and service standards are set at the state level by public utility commissions — 50 states plus DC — making state-level politics central to pricing and reliability. Shifts in political leadership can tilt commissions toward consumer relief or toward approving infrastructure investment and cost recovery. Maintaining stable regulatory relationships is essential for Atmos to secure timely recovery of capital spending and avoid earnings erosion.

Energy transition policies

State and municipal decarbonization agendas are reshaping demand and allowable utility investments, pressuring Atmos Energy—which serves about 3.1 million customers across eight states—to adapt capital plans. Electrification incentives from the 2022 Inflation Reduction Act and rising building performance standards can slow customer growth in gas heating. Concurrently, policy alignment on low‑carbon gas and RNG or hydrogen credits could create new revenue streams and eligible investments.

Infrastructure funding support

Political backing for resilience and safety programs enables regulators to approve cost-recovery riders and accelerated replacement mechanisms that improve cash flow for utility projects. Atmos Energy, serving about 3 million customers across eight states and roughly 90,000 miles of pipeline, can leverage federal and state grants or tax incentives to lower net capital burden. Shifts in fiscal priorities at state or federal levels could, however, tighten access to such public support and slow replacement schedules.

Local permitting dynamics

County and city councils directly control pipeline permits, street opening approvals and construction schedules, affecting Atmos Energy’s deployment across about 3 million customers in eight states (Atmos Energy 2024 reporting). Community pushback has caused multi-month delays and higher contractor/relocation costs on specific projects. Proactive stakeholder engagement and early permitting coordination reduce political friction and timetable risk.

- Permitting control: county/city councils

- Risk: multi-month delays, higher project costs

- Mitigation: early stakeholder engagement, coordinated permits

Geopolitical energy stance

National policy on domestic gas production and interstate infrastructure shapes Atmos Energy’s supply reliability, with US natural gas production reaching record levels in 2023 per EIA, supporting system resilience.

Federal and state support for North American gas and pipeline permitting has bolstered regional availability and helped stabilize domestic pricing since the US became the world’s top LNG exporter in 2022.

Adverse policy shifts or tighter permitting could raise volatility and procurement risk, increasing exposure to spot market price swings and supply interruptions.

- Policy influence: interstate permitting affects reliability

- Regional support: US top LNG exporter (2022) aids stability

- Risk: adverse shifts elevate volatility and procurement risk

Regulated gas service in 8 states serves ≈3.1M — politics, decarbonization, RNG

Atmos Energy’s state-regulated rates across eight states (≈3.1 million customers, Atmos 2024) make state politics decisive for cost recovery and earnings. Decarbonization policies and IRA incentives (2022) pressure demand for gas but create RNG/hydrogen credit opportunities. Local permitting delays raise project costs and timeline risk; federal support and record US gas production (EIA 2023) aid supply resilience.

| Metric | Value |

|---|---|

| Customers (2024) | ≈3.1M |

| Service states | 8 |

| Pipeline mileage | ≈90,000 mi |

| US gas record | 2023 (EIA) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Atmos Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into detailed, company-specific subpoints. Backed by current data and forward-looking insights, the analysis supports executives and investors in identifying regulatory risks, market opportunities and scenario-driven strategies.

Condensed Atmos Energy PESTLE highlights regulatory, economic, environmental and technological risks and opportunities in a single, easy-to-scan snapshot, helping teams make faster strategic decisions and align stakeholders without wading through lengthy reports.

Economic factors

Interest rate sensitivity

As a capital-intensive regulated gas utility (ATO), Atmos Energy’s earnings and customer rates are highly sensitive to financing costs; the US federal funds rate of 5.25–5.50% in mid-2025 raises borrowing costs and can pressure allowed ROE outcomes in rate cases. Higher rates increase debt service and may slow growth in rate base recoveries, while lower rates support accelerated system modernization and capital deployment.

Commodity price pass-through

Gas costs are largely passed through via purchased gas adjustment riders, limiting supplier margin exposure; EIA 2024 Henry Hub averaged about 2.83/MMBtu while 2022 spikes above 9/MMBtu demonstrated material customer bill impacts. Volatility elevates delinquencies, bad debt and political scrutiny. Robust hedging and storage strategies are pivotal to stabilizing bills.

Regional growth patterns

Population and industrial expansion in Atmos Energy service territories—Atmos serves about 3 million customers—support higher throughput and new connections; Texas population grew ~1.2% in 2023, fueling demand. Economic slowdowns (US GDP growth 2.5% in 2024) can curb commercial use and construction activity. A diversified customer mix across residential, commercial and industrial segments helps buffer cyclical impacts.

Labor and materials inflation

Rising costs for steel, plastic pipe, compressors and contract labor are tightening Atmos Energys capex budgets, increasing unit project costs and extending payback timelines.

Regulatory inflation escalators often lag actual input cost increases, creating timing mismatches that compress margins until rate cases catch up.

Active supply-chain management and multi-year procurement contracts help moderate volatility, secure materials and lock pricing to protect near-term capital plans.

- capex pressure

- regulatory lag

- procurement hedging

Weather-driven demand

Heating degree days drive Atmos Energy seasonal volumes and cash timing for its ~3 million customers; NOAA noted winter 2023–24 was warmer than the 1991–2020 average, compressing delivered volumes and shifting revenue into off-peak periods. Warmer winters can compress margins even where decoupling exists, while weather normalization adjustments and storage management mitigate earnings volatility.

- HDD sensitivity: major driver of monthly volumes

- Decoupling reduces but does not eliminate margin compression in warm winters

- Storage and normalization mechanisms optimize revenue timing and volatility

Regulated gas service in 8 states serves ≈3.1M — politics, decarbonization, RNG

Atmos Energy (≈3.0M customers) faces higher financing costs with US federal funds 5.25–5.50% (mid‑2025), pressuring debt service and rate-case ROE outcomes. 2024 Henry Hub averaged $2.83/MMBtu; gas pass-through limits margin but volatility raises delinquencies. Texas population +1.2% (2023) supports demand; warmer 2023–24 winter cut volumes per NOAA.

| Metric | Value | Near-term impact |

|---|---|---|

| Customers | ≈3,000,000 | Base demand |

| Fed funds | 5.25–5.50% | Higher capex cost |

| Henry Hub 2024 | $2.83/MMBtu | Pass-through volatility |

Preview the Actual Deliverable

Atmos Energy PESTLE Analysis

The preview shown here is the exact Atmos Energy PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after checkout.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, and environmental forces are reshaping Atmos Energy and what that means for risk and growth. Our concise PESTLE highlights regulatory, market, and technological pressures you need to know. Buy the full analysis for a detailed, actionable report with ready-to-use templates.

Political factors

State utility oversight

Atmos Energy’s rates and service standards are set at the state level by public utility commissions — 50 states plus DC — making state-level politics central to pricing and reliability. Shifts in political leadership can tilt commissions toward consumer relief or toward approving infrastructure investment and cost recovery. Maintaining stable regulatory relationships is essential for Atmos to secure timely recovery of capital spending and avoid earnings erosion.

Energy transition policies

State and municipal decarbonization agendas are reshaping demand and allowable utility investments, pressuring Atmos Energy—which serves about 3.1 million customers across eight states—to adapt capital plans. Electrification incentives from the 2022 Inflation Reduction Act and rising building performance standards can slow customer growth in gas heating. Concurrently, policy alignment on low‑carbon gas and RNG or hydrogen credits could create new revenue streams and eligible investments.

Infrastructure funding support

Political backing for resilience and safety programs enables regulators to approve cost-recovery riders and accelerated replacement mechanisms that improve cash flow for utility projects. Atmos Energy, serving about 3 million customers across eight states and roughly 90,000 miles of pipeline, can leverage federal and state grants or tax incentives to lower net capital burden. Shifts in fiscal priorities at state or federal levels could, however, tighten access to such public support and slow replacement schedules.

Local permitting dynamics

County and city councils directly control pipeline permits, street opening approvals and construction schedules, affecting Atmos Energy’s deployment across about 3 million customers in eight states (Atmos Energy 2024 reporting). Community pushback has caused multi-month delays and higher contractor/relocation costs on specific projects. Proactive stakeholder engagement and early permitting coordination reduce political friction and timetable risk.

- Permitting control: county/city councils

- Risk: multi-month delays, higher project costs

- Mitigation: early stakeholder engagement, coordinated permits

Geopolitical energy stance

National policy on domestic gas production and interstate infrastructure shapes Atmos Energy’s supply reliability, with US natural gas production reaching record levels in 2023 per EIA, supporting system resilience.

Federal and state support for North American gas and pipeline permitting has bolstered regional availability and helped stabilize domestic pricing since the US became the world’s top LNG exporter in 2022.

Adverse policy shifts or tighter permitting could raise volatility and procurement risk, increasing exposure to spot market price swings and supply interruptions.

- Policy influence: interstate permitting affects reliability

- Regional support: US top LNG exporter (2022) aids stability

- Risk: adverse shifts elevate volatility and procurement risk

Regulated gas service in 8 states serves ≈3.1M — politics, decarbonization, RNG

Atmos Energy’s state-regulated rates across eight states (≈3.1 million customers, Atmos 2024) make state politics decisive for cost recovery and earnings. Decarbonization policies and IRA incentives (2022) pressure demand for gas but create RNG/hydrogen credit opportunities. Local permitting delays raise project costs and timeline risk; federal support and record US gas production (EIA 2023) aid supply resilience.

| Metric | Value |

|---|---|

| Customers (2024) | ≈3.1M |

| Service states | 8 |

| Pipeline mileage | ≈90,000 mi |

| US gas record | 2023 (EIA) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Atmos Energy across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into detailed, company-specific subpoints. Backed by current data and forward-looking insights, the analysis supports executives and investors in identifying regulatory risks, market opportunities and scenario-driven strategies.

Condensed Atmos Energy PESTLE highlights regulatory, economic, environmental and technological risks and opportunities in a single, easy-to-scan snapshot, helping teams make faster strategic decisions and align stakeholders without wading through lengthy reports.

Economic factors

Interest rate sensitivity

As a capital-intensive regulated gas utility (ATO), Atmos Energy’s earnings and customer rates are highly sensitive to financing costs; the US federal funds rate of 5.25–5.50% in mid-2025 raises borrowing costs and can pressure allowed ROE outcomes in rate cases. Higher rates increase debt service and may slow growth in rate base recoveries, while lower rates support accelerated system modernization and capital deployment.

Commodity price pass-through

Gas costs are largely passed through via purchased gas adjustment riders, limiting supplier margin exposure; EIA 2024 Henry Hub averaged about 2.83/MMBtu while 2022 spikes above 9/MMBtu demonstrated material customer bill impacts. Volatility elevates delinquencies, bad debt and political scrutiny. Robust hedging and storage strategies are pivotal to stabilizing bills.

Regional growth patterns

Population and industrial expansion in Atmos Energy service territories—Atmos serves about 3 million customers—support higher throughput and new connections; Texas population grew ~1.2% in 2023, fueling demand. Economic slowdowns (US GDP growth 2.5% in 2024) can curb commercial use and construction activity. A diversified customer mix across residential, commercial and industrial segments helps buffer cyclical impacts.

Labor and materials inflation

Rising costs for steel, plastic pipe, compressors and contract labor are tightening Atmos Energys capex budgets, increasing unit project costs and extending payback timelines.

Regulatory inflation escalators often lag actual input cost increases, creating timing mismatches that compress margins until rate cases catch up.

Active supply-chain management and multi-year procurement contracts help moderate volatility, secure materials and lock pricing to protect near-term capital plans.

- capex pressure

- regulatory lag

- procurement hedging

Weather-driven demand

Heating degree days drive Atmos Energy seasonal volumes and cash timing for its ~3 million customers; NOAA noted winter 2023–24 was warmer than the 1991–2020 average, compressing delivered volumes and shifting revenue into off-peak periods. Warmer winters can compress margins even where decoupling exists, while weather normalization adjustments and storage management mitigate earnings volatility.

- HDD sensitivity: major driver of monthly volumes

- Decoupling reduces but does not eliminate margin compression in warm winters

- Storage and normalization mechanisms optimize revenue timing and volatility

Regulated gas service in 8 states serves ≈3.1M — politics, decarbonization, RNG

Atmos Energy (≈3.0M customers) faces higher financing costs with US federal funds 5.25–5.50% (mid‑2025), pressuring debt service and rate-case ROE outcomes. 2024 Henry Hub averaged $2.83/MMBtu; gas pass-through limits margin but volatility raises delinquencies. Texas population +1.2% (2023) supports demand; warmer 2023–24 winter cut volumes per NOAA.

| Metric | Value | Near-term impact |

|---|---|---|

| Customers | ≈3,000,000 | Base demand |

| Fed funds | 5.25–5.50% | Higher capex cost |

| Henry Hub 2024 | $2.83/MMBtu | Pass-through volatility |

Preview the Actual Deliverable

Atmos Energy PESTLE Analysis

The preview shown here is the exact Atmos Energy PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after checkout.