Atmosfera Gestao & Higienizacao de Texteis SA Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

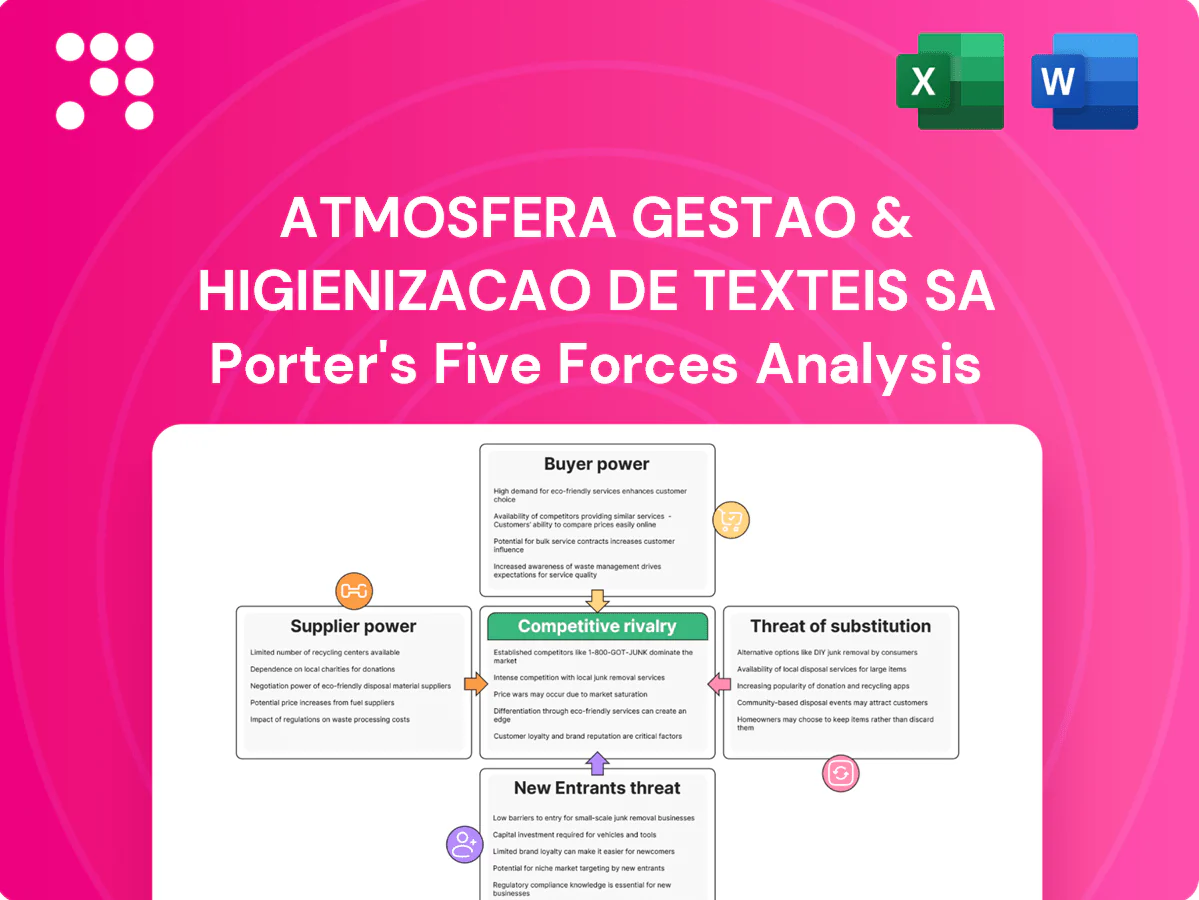

Atmosfera Gestao & Higienizacao de Texteis SA faces moderate buyer power, localized supplier leverage, and niche-scale rivalry shaped by service contracts and regulatory hygiene standards. Threats from new entrants and substitutes hinge on tech-driven efficiency and chemical compliance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Utility and energy dependence

Industrial laundering is energy- and water-intensive, with utilities representing up to 40% of operating costs in commercial laundry operations, so electricity, gas or water price spikes directly compress margins. Tariff surges of 20–30% in recent regional episodes have squeezed profitability, while long-term energy contracts and efficiency upgrades (heat recovery, low‑flow systems) can partially mitigate exposure. Local monopoly utilities or constrained infrastructure further increase supplier leverage.

Detergents and chemicals vendors

In 2024 specialized detergents, disinfectants and enzymes meeting EN 14476/EN 13727 and local health approvals are required for healthcare-grade textile hygiene, constraining supplier choice. A limited pool of certified vendors raises switching costs, though bulk contracts and dual-sourcing lower supply disruption risk. Regulatory-approved chemistries narrow alternatives and input price pass-through depends on client contract structures and CPI-linked clauses.

Textile and linen sourcing

Quality, durability and lifecycle cost of linens and workwear for Atmosfera hinge directly on textile suppliers, with cotton and polyester making up roughly 24% and 52% of global fiber consumption respectively (2024), so price or supply swings materially affect unit costs. Geopolitical risks and raw-material volatility drive availability and pricing, while vendor-managed inventory and framework agreements are used to stabilize supply. Custom specs and branded items raise dependency on selected mills and limit supplier switching.

Equipment OEMs and maintenance

Washers, tunnel washers, dryers and finishing lines are capital-intensive with a concentrated set of OEMs, giving suppliers leverage through proprietary spare parts, firmware and maintenance contracts that can create strong lock-in for Atmosfera Gestao & Higienizacao de Texteis SA.

Downtime during critical failures amplifies vendor bargaining power; robust preventive maintenance programs and building in-house technician capabilities can shift negotiating balance back to the operator.

Transport and fuel providers

Collection and delivery depend on reliable logistics and diesel, with EU average diesel at about 1.62 EUR/L in 2024 (Eurostat), making fuel a key cost driver; tight carrier capacity and expanding low-emission zones across EU cities in 2024 increased last-mile complexity and costs. Owning fleets boosts control but concentrates exposure to fuel suppliers; route optimization and shifts to electric or biofuels can reduce volatility.

Utilities and OEMs raise supplier power: fuel, fibers and vendor lock-in drive cost risk

Supplier power is moderate–high: utilities can be up to 40% of operating costs, OEM concentration and certified-chemistry vendors create lock‑in, and textile raw‑material swings (2024: cotton ~24%, polyester ~52% of fiber consumption) materially affect input costs. EU diesel averaged ~1.62 EUR/L in 2024, raising logistics exposure. Long-term contracts, dual‑sourcing, preventive maintenance and EVs/biofuels reduce vulnerability.

| Metric | 2024 value | Impact |

|---|---|---|

| Utilities share | up to 40% | High cost sensitivity |

| EU diesel | ~1.62 EUR/L | Logistics cost pressure |

| Cotton/polyester | 24% / 52% | Raw‑material volatility |

| OEM concentration | High | Spare‑parts lock‑in |

What is included in the product

Tailored Porter's Five Forces overview for Atmosfera Gestão & Higienização de Têxteis SA, highlighting competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, plus regulatory and technological disruptors affecting pricing and profitability.

One-sheet Porter's Five Forces for Atmosfera — quickly pinpoints competitive pain points and relief strategies, with adjustable pressure levels and a clean radar view ready for decks or dashboards.

Customers Bargaining Power

Large institutional buyers

In 2024 large institutional buyers—hospitals, hotel chains and industrial groups—buy high volumes and negotiate aggressively, leveraging centralized procurement and multi-site contracts to extract scale advantages. These buyers routinely demand stringent SLAs and volume rebates, sometimes tying payments to compliance metrics. Atmosfera can trade price concessions for referenceability from marquee clients, which in turn fuels new contracts and credibility.

Switching costs and integration

Process integration across collection, washing, repair and delivery creates moderate switching costs for Atmosfera, with RFID tagging, sorting protocols and staff training embedding operations and reducing inventory losses by about 20–30% (industry 2024 studies). Transition risks such as stock reconciliation and hygiene continuity slow switching, often taking 30–90 days. Well-planned RFP transitions still keep suppliers under competitive pressure.

Tendering and price transparency

Public and private RFPs for textile hygiene standardize specs and typically attract 3–6 bidders, driving transparent competition. Benchmarking of turnaround times and cost per kg/piece has compressed bid prices—industry reports in 2024 cite margin erosion of roughly 8–12% for low-differentiation contracts. Indexation clauses (often tied to local CPI) frequently cap pass-through of input inflation. Suppliers must demonstrate service, quality or compliance advantages beyond price to defend margins.

Compliance and quality demands

Healthcare-grade hygiene certifications shift buyer focus from price to outcomes and risk control; in 2024 over 50% of major hospital tenders required certified laundry/hygiene standards, boosting demand for traceability, contamination control and audit readiness and reducing pure price comparisons. Penalties for non-compliance increase buyer oversight, while superior quality supports premium pricing and lowers buyer power.

Demand variability

Seasonality in hospitality and episodic healthcare surges drive 20–40% volume swings, pressuring Atmosfera to offer flexible capacity while buyers resist paying for standby; this volatility weakens supplier utilization and reduces bargaining power. Dynamic pricing and minimum-volume commitments have been used across the sector to stabilize revenue and shift risk back to buyers.

- Volume swing: 20–40% seasonality

- Risk: lower utilization, weaker margins

- Mitigant: dynamic pricing

- Mitigant: minimum volume contracts

3-6 bidders cause 8-12% margin erosion; certification raises quality bar

Large institutional buyers (3–6 bidders) exert strong price pressure, causing 8–12% margin erosion in commoditized tenders in 2024, but certification requirements (over 50% hospital tenders) shift focus to quality. Switching costs (RFID, processes) and 30–90 day transition timelines moderate buyer power. Seasonality (20–40% volume swings) weakens supplier leverage; dynamic pricing and minimum-volume clauses mitigate risk.

| Metric | 2024 Value |

|---|---|

| Bidders per RFP | 3–6 |

| Margin erosion | 8–12% |

| Hospital tenders requiring certification | >50% |

| Transition time | 30–90 days |

| Seasonality volume swing | 20–40% |

What You See Is What You Get

Atmosfera Gestao & Higienizacao de Texteis SA Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Atmosfera Gestao & Higienizacao de Texteis SA you'll receive—no placeholders. The report assesses competitive rivalry, supplier and buyer power, and threats of entry and substitution, with clear strategic implications. Purchase grants instant access to this fully formatted, ready-to-use document.

A Must-Have Tool for Decision-Makers

Atmosfera Gestao & Higienizacao de Texteis SA faces moderate buyer power, localized supplier leverage, and niche-scale rivalry shaped by service contracts and regulatory hygiene standards. Threats from new entrants and substitutes hinge on tech-driven efficiency and chemical compliance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Utility and energy dependence

Industrial laundering is energy- and water-intensive, with utilities representing up to 40% of operating costs in commercial laundry operations, so electricity, gas or water price spikes directly compress margins. Tariff surges of 20–30% in recent regional episodes have squeezed profitability, while long-term energy contracts and efficiency upgrades (heat recovery, low‑flow systems) can partially mitigate exposure. Local monopoly utilities or constrained infrastructure further increase supplier leverage.

Detergents and chemicals vendors

In 2024 specialized detergents, disinfectants and enzymes meeting EN 14476/EN 13727 and local health approvals are required for healthcare-grade textile hygiene, constraining supplier choice. A limited pool of certified vendors raises switching costs, though bulk contracts and dual-sourcing lower supply disruption risk. Regulatory-approved chemistries narrow alternatives and input price pass-through depends on client contract structures and CPI-linked clauses.

Textile and linen sourcing

Quality, durability and lifecycle cost of linens and workwear for Atmosfera hinge directly on textile suppliers, with cotton and polyester making up roughly 24% and 52% of global fiber consumption respectively (2024), so price or supply swings materially affect unit costs. Geopolitical risks and raw-material volatility drive availability and pricing, while vendor-managed inventory and framework agreements are used to stabilize supply. Custom specs and branded items raise dependency on selected mills and limit supplier switching.

Equipment OEMs and maintenance

Washers, tunnel washers, dryers and finishing lines are capital-intensive with a concentrated set of OEMs, giving suppliers leverage through proprietary spare parts, firmware and maintenance contracts that can create strong lock-in for Atmosfera Gestao & Higienizacao de Texteis SA.

Downtime during critical failures amplifies vendor bargaining power; robust preventive maintenance programs and building in-house technician capabilities can shift negotiating balance back to the operator.

Transport and fuel providers

Collection and delivery depend on reliable logistics and diesel, with EU average diesel at about 1.62 EUR/L in 2024 (Eurostat), making fuel a key cost driver; tight carrier capacity and expanding low-emission zones across EU cities in 2024 increased last-mile complexity and costs. Owning fleets boosts control but concentrates exposure to fuel suppliers; route optimization and shifts to electric or biofuels can reduce volatility.

Utilities and OEMs raise supplier power: fuel, fibers and vendor lock-in drive cost risk

Supplier power is moderate–high: utilities can be up to 40% of operating costs, OEM concentration and certified-chemistry vendors create lock‑in, and textile raw‑material swings (2024: cotton ~24%, polyester ~52% of fiber consumption) materially affect input costs. EU diesel averaged ~1.62 EUR/L in 2024, raising logistics exposure. Long-term contracts, dual‑sourcing, preventive maintenance and EVs/biofuels reduce vulnerability.

| Metric | 2024 value | Impact |

|---|---|---|

| Utilities share | up to 40% | High cost sensitivity |

| EU diesel | ~1.62 EUR/L | Logistics cost pressure |

| Cotton/polyester | 24% / 52% | Raw‑material volatility |

| OEM concentration | High | Spare‑parts lock‑in |

What is included in the product

Tailored Porter's Five Forces overview for Atmosfera Gestão & Higienização de Têxteis SA, highlighting competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, plus regulatory and technological disruptors affecting pricing and profitability.

One-sheet Porter's Five Forces for Atmosfera — quickly pinpoints competitive pain points and relief strategies, with adjustable pressure levels and a clean radar view ready for decks or dashboards.

Customers Bargaining Power

Large institutional buyers

In 2024 large institutional buyers—hospitals, hotel chains and industrial groups—buy high volumes and negotiate aggressively, leveraging centralized procurement and multi-site contracts to extract scale advantages. These buyers routinely demand stringent SLAs and volume rebates, sometimes tying payments to compliance metrics. Atmosfera can trade price concessions for referenceability from marquee clients, which in turn fuels new contracts and credibility.

Switching costs and integration

Process integration across collection, washing, repair and delivery creates moderate switching costs for Atmosfera, with RFID tagging, sorting protocols and staff training embedding operations and reducing inventory losses by about 20–30% (industry 2024 studies). Transition risks such as stock reconciliation and hygiene continuity slow switching, often taking 30–90 days. Well-planned RFP transitions still keep suppliers under competitive pressure.

Tendering and price transparency

Public and private RFPs for textile hygiene standardize specs and typically attract 3–6 bidders, driving transparent competition. Benchmarking of turnaround times and cost per kg/piece has compressed bid prices—industry reports in 2024 cite margin erosion of roughly 8–12% for low-differentiation contracts. Indexation clauses (often tied to local CPI) frequently cap pass-through of input inflation. Suppliers must demonstrate service, quality or compliance advantages beyond price to defend margins.

Compliance and quality demands

Healthcare-grade hygiene certifications shift buyer focus from price to outcomes and risk control; in 2024 over 50% of major hospital tenders required certified laundry/hygiene standards, boosting demand for traceability, contamination control and audit readiness and reducing pure price comparisons. Penalties for non-compliance increase buyer oversight, while superior quality supports premium pricing and lowers buyer power.

Demand variability

Seasonality in hospitality and episodic healthcare surges drive 20–40% volume swings, pressuring Atmosfera to offer flexible capacity while buyers resist paying for standby; this volatility weakens supplier utilization and reduces bargaining power. Dynamic pricing and minimum-volume commitments have been used across the sector to stabilize revenue and shift risk back to buyers.

- Volume swing: 20–40% seasonality

- Risk: lower utilization, weaker margins

- Mitigant: dynamic pricing

- Mitigant: minimum volume contracts

3-6 bidders cause 8-12% margin erosion; certification raises quality bar

Large institutional buyers (3–6 bidders) exert strong price pressure, causing 8–12% margin erosion in commoditized tenders in 2024, but certification requirements (over 50% hospital tenders) shift focus to quality. Switching costs (RFID, processes) and 30–90 day transition timelines moderate buyer power. Seasonality (20–40% volume swings) weakens supplier leverage; dynamic pricing and minimum-volume clauses mitigate risk.

| Metric | 2024 Value |

|---|---|

| Bidders per RFP | 3–6 |

| Margin erosion | 8–12% |

| Hospital tenders requiring certification | >50% |

| Transition time | 30–90 days |

| Seasonality volume swing | 20–40% |

What You See Is What You Get

Atmosfera Gestao & Higienizacao de Texteis SA Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Atmosfera Gestao & Higienizacao de Texteis SA you'll receive—no placeholders. The report assesses competitive rivalry, supplier and buyer power, and threats of entry and substitution, with clear strategic implications. Purchase grants instant access to this fully formatted, ready-to-use document.

Description

A Must-Have Tool for Decision-Makers

Atmosfera Gestao & Higienizacao de Texteis SA faces moderate buyer power, localized supplier leverage, and niche-scale rivalry shaped by service contracts and regulatory hygiene standards. Threats from new entrants and substitutes hinge on tech-driven efficiency and chemical compliance. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Utility and energy dependence

Industrial laundering is energy- and water-intensive, with utilities representing up to 40% of operating costs in commercial laundry operations, so electricity, gas or water price spikes directly compress margins. Tariff surges of 20–30% in recent regional episodes have squeezed profitability, while long-term energy contracts and efficiency upgrades (heat recovery, low‑flow systems) can partially mitigate exposure. Local monopoly utilities or constrained infrastructure further increase supplier leverage.

Detergents and chemicals vendors

In 2024 specialized detergents, disinfectants and enzymes meeting EN 14476/EN 13727 and local health approvals are required for healthcare-grade textile hygiene, constraining supplier choice. A limited pool of certified vendors raises switching costs, though bulk contracts and dual-sourcing lower supply disruption risk. Regulatory-approved chemistries narrow alternatives and input price pass-through depends on client contract structures and CPI-linked clauses.

Textile and linen sourcing

Quality, durability and lifecycle cost of linens and workwear for Atmosfera hinge directly on textile suppliers, with cotton and polyester making up roughly 24% and 52% of global fiber consumption respectively (2024), so price or supply swings materially affect unit costs. Geopolitical risks and raw-material volatility drive availability and pricing, while vendor-managed inventory and framework agreements are used to stabilize supply. Custom specs and branded items raise dependency on selected mills and limit supplier switching.

Equipment OEMs and maintenance

Washers, tunnel washers, dryers and finishing lines are capital-intensive with a concentrated set of OEMs, giving suppliers leverage through proprietary spare parts, firmware and maintenance contracts that can create strong lock-in for Atmosfera Gestao & Higienizacao de Texteis SA.

Downtime during critical failures amplifies vendor bargaining power; robust preventive maintenance programs and building in-house technician capabilities can shift negotiating balance back to the operator.

Transport and fuel providers

Collection and delivery depend on reliable logistics and diesel, with EU average diesel at about 1.62 EUR/L in 2024 (Eurostat), making fuel a key cost driver; tight carrier capacity and expanding low-emission zones across EU cities in 2024 increased last-mile complexity and costs. Owning fleets boosts control but concentrates exposure to fuel suppliers; route optimization and shifts to electric or biofuels can reduce volatility.

Utilities and OEMs raise supplier power: fuel, fibers and vendor lock-in drive cost risk

Supplier power is moderate–high: utilities can be up to 40% of operating costs, OEM concentration and certified-chemistry vendors create lock‑in, and textile raw‑material swings (2024: cotton ~24%, polyester ~52% of fiber consumption) materially affect input costs. EU diesel averaged ~1.62 EUR/L in 2024, raising logistics exposure. Long-term contracts, dual‑sourcing, preventive maintenance and EVs/biofuels reduce vulnerability.

| Metric | 2024 value | Impact |

|---|---|---|

| Utilities share | up to 40% | High cost sensitivity |

| EU diesel | ~1.62 EUR/L | Logistics cost pressure |

| Cotton/polyester | 24% / 52% | Raw‑material volatility |

| OEM concentration | High | Spare‑parts lock‑in |

What is included in the product

Tailored Porter's Five Forces overview for Atmosfera Gestão & Higienização de Têxteis SA, highlighting competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, plus regulatory and technological disruptors affecting pricing and profitability.

One-sheet Porter's Five Forces for Atmosfera — quickly pinpoints competitive pain points and relief strategies, with adjustable pressure levels and a clean radar view ready for decks or dashboards.

Customers Bargaining Power

Large institutional buyers

In 2024 large institutional buyers—hospitals, hotel chains and industrial groups—buy high volumes and negotiate aggressively, leveraging centralized procurement and multi-site contracts to extract scale advantages. These buyers routinely demand stringent SLAs and volume rebates, sometimes tying payments to compliance metrics. Atmosfera can trade price concessions for referenceability from marquee clients, which in turn fuels new contracts and credibility.

Switching costs and integration

Process integration across collection, washing, repair and delivery creates moderate switching costs for Atmosfera, with RFID tagging, sorting protocols and staff training embedding operations and reducing inventory losses by about 20–30% (industry 2024 studies). Transition risks such as stock reconciliation and hygiene continuity slow switching, often taking 30–90 days. Well-planned RFP transitions still keep suppliers under competitive pressure.

Tendering and price transparency

Public and private RFPs for textile hygiene standardize specs and typically attract 3–6 bidders, driving transparent competition. Benchmarking of turnaround times and cost per kg/piece has compressed bid prices—industry reports in 2024 cite margin erosion of roughly 8–12% for low-differentiation contracts. Indexation clauses (often tied to local CPI) frequently cap pass-through of input inflation. Suppliers must demonstrate service, quality or compliance advantages beyond price to defend margins.

Compliance and quality demands

Healthcare-grade hygiene certifications shift buyer focus from price to outcomes and risk control; in 2024 over 50% of major hospital tenders required certified laundry/hygiene standards, boosting demand for traceability, contamination control and audit readiness and reducing pure price comparisons. Penalties for non-compliance increase buyer oversight, while superior quality supports premium pricing and lowers buyer power.

Demand variability

Seasonality in hospitality and episodic healthcare surges drive 20–40% volume swings, pressuring Atmosfera to offer flexible capacity while buyers resist paying for standby; this volatility weakens supplier utilization and reduces bargaining power. Dynamic pricing and minimum-volume commitments have been used across the sector to stabilize revenue and shift risk back to buyers.

- Volume swing: 20–40% seasonality

- Risk: lower utilization, weaker margins

- Mitigant: dynamic pricing

- Mitigant: minimum volume contracts

3-6 bidders cause 8-12% margin erosion; certification raises quality bar

Large institutional buyers (3–6 bidders) exert strong price pressure, causing 8–12% margin erosion in commoditized tenders in 2024, but certification requirements (over 50% hospital tenders) shift focus to quality. Switching costs (RFID, processes) and 30–90 day transition timelines moderate buyer power. Seasonality (20–40% volume swings) weakens supplier leverage; dynamic pricing and minimum-volume clauses mitigate risk.

| Metric | 2024 Value |

|---|---|

| Bidders per RFP | 3–6 |

| Margin erosion | 8–12% |

| Hospital tenders requiring certification | >50% |

| Transition time | 30–90 days |

| Seasonality volume swing | 20–40% |

What You See Is What You Get

Atmosfera Gestao & Higienizacao de Texteis SA Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Atmosfera Gestao & Higienizacao de Texteis SA you'll receive—no placeholders. The report assesses competitive rivalry, supplier and buyer power, and threats of entry and substitution, with clear strategic implications. Purchase grants instant access to this fully formatted, ready-to-use document.