AtriCure Porter's Five Forces Analysis

From Overview to Strategy Blueprint

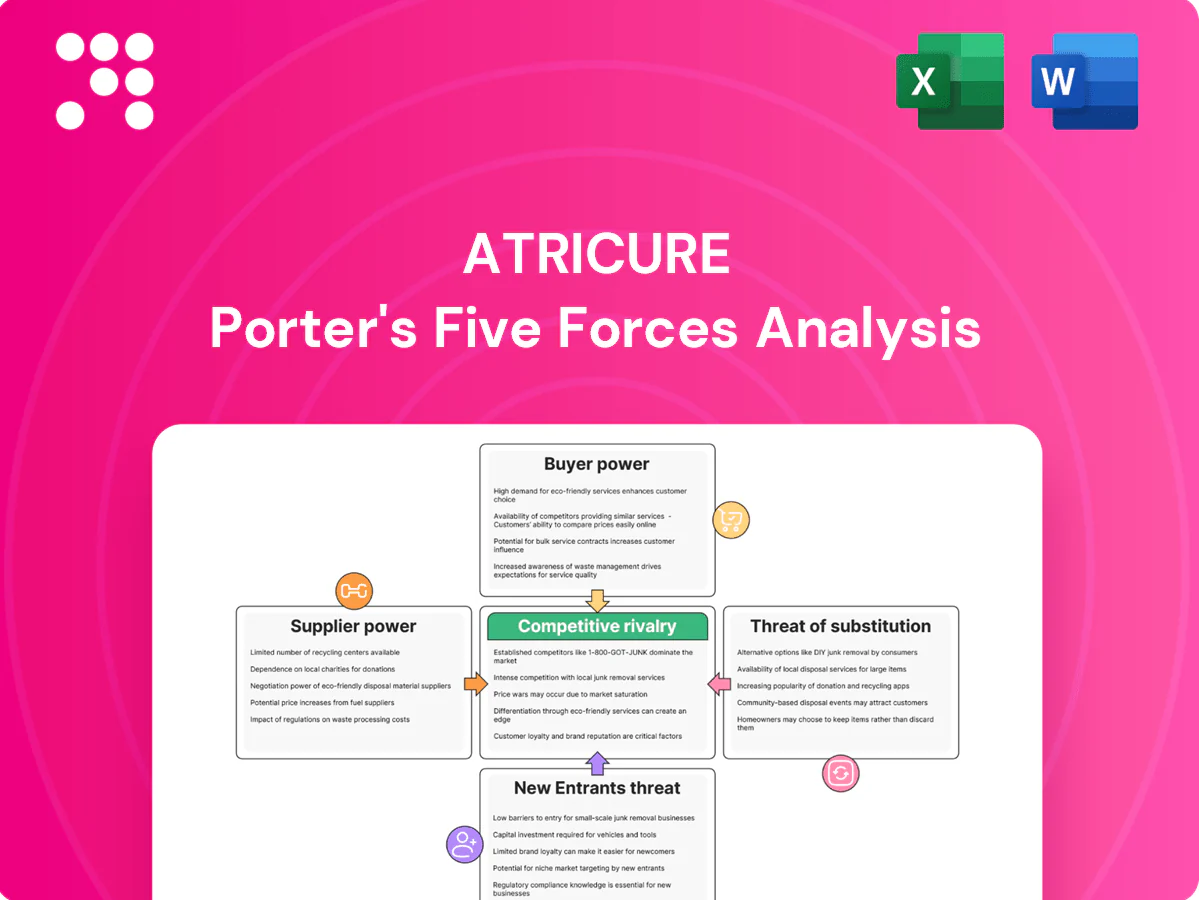

AtriCure’s Porter’s Five Forces snapshot highlights strong buyer scrutiny, significant supplier specialization, moderate threat from substitutes, high regulatory barriers, and intense rivalry among cardiac device makers. This brief overview surfaces key competitive pressures and strategic vulnerabilities. This preview is just the beginning—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialized biocompatible materials

Devices require high-spec polymers, nitinol, and biocompatible metals that must meet ISO 10993 biocompatibility and FDA device standards, raising material quality thresholds. Limited qualified suppliers for nitinol and cardiac-grade alloys concentrate leverage, increasing pricing and supply risk. Certification and validation per ISO 13485 and regulatory testing drive lengthy, costly supplier switches. Long lead times for specialty components can disrupt inventory and production planning.

Precision electronics and semiconductors

AtriCure's ablation and energy platforms depend on chips, sensors and power components with tight tolerances, making supplier precision critical. Semiconductor cyclicality and allocation can constrain availability and raise costs for medical OEMs. Redesigns to qualify alternate suppliers trigger costly regulatory workstreams—about 90% of devices use FDA 510(k) pathways—so supplier changes are burdensome. Strategic long-term agreements partially mitigate volatility.

Sterile disposables and contract manufacturing

Single-use ablation tools and accessories require validated sterile processes and Class III cardiac-quality systems, limiting the pool of qualified contract manufacturers and increasing supplier bargaining power.

Few CMOs possess the necessary ISO 13485 and FDA QSR maturity, so nonconformance can trigger recalls and production line stoppages that directly hit revenue and market supply.

Multi-sourcing and dual qualification mitigate exposure but do not eliminate dependency or the risk of simultaneous disruptions.

Regulatory and testing services

Accredited labs perform biocompatibility, reliability, and sterilization testing, and limited capacity or adverse findings can add roughly 3–6 months to regulatory timelines, delaying filings and launches. CROs controlling patient enrollment and site activation exert timing leverage; the global CRO market reached about $61 billion in 2024. Early engagement with vendors and selective in-house testing reduces AtriCure’s exposure.

- Dependency: accredited labs for biocompatibility/reliability

- Risk: capacity/findings → ~3–6 month delays

- CRO leverage: $61B CRO market (2024)

- Mitigation: early engagement + in‑house testing

Proprietary components and IP constraints

Custom tips, cables and coatings for Atricure devices are often single-sourced due to IP and tooling, giving suppliers leverage; tooling transfers and revalidations commonly add 6–12 months and FDA 510(k) median review was about 5 months in 2024, extending timelines. Suppliers can negotiate volume and pricing, impacting COGS, while contractual protections and VAVE programs help rebalance power.

- Single-sourcing: IP/tooling constraints

- Timelines: tooling transfers +6–12 months; FDA 510(k) ~5 months (2024)

- Mitigation: contracts, VAVE, supplier diversification

Supply risk: concentrated nitinol; certification adds 3–12m, CRO $61B

Supplier power is high due to concentrated nitinol/alloy sources, certified CMOs and labs; shortages and single‑sourcing raise COGS and disruption risk. Certification and design requalification add ~3–12 months; CRO market $61B (2024) and FDA 510(k) median review ~5 months (2024). Mitigants: long‑term contracts, multi‑sourcing, selective in‑house testing.

| Factor | Metric |

|---|---|

| Lab delays | 3–6 months |

| Tooling transfers | 6–12 months |

| CRO market | $61B (2024) |

| 510(k) median | ~5 months (2024) |

What is included in the product

Detailed Porter’s Five Forces analysis for AtriCure assessing competitive rivalry, buyer and supplier power, and threats from substitutes and new entrants; highlights disruptive technologies, pricing pressures, and entry barriers shaping the company’s profitability and strategic positioning.

AtriCure Porter’s Five Forces delivers a concise, one-sheet pain-point reliever—quickly highlighting competitive pressures, supplier/payer risks, and entrant threats for strategic decisions. Clean layout and customizable pressure levels make it easy to drop into decks or adapt for regulatory or market shifts.

Customers Bargaining Power

Hospital systems and IDNs

Hospital systems and IDNs centralize purchasing and enforce device formularies, with over 60% of U.S. hospital beds in systems by 2024, increasing leverage. Volume-based contracts and standardization drive double-digit price concessions; GPOs cover ~90–95% of hospitals, adding negotiation layers. Payers and IDNs demand total-cost-of-care evidence to justify price premiums, pressuring AtriCure to demonstrate reductions in readmissions and LOS.

Surgeon and EP preference

Clinician preference drives adoption in the OR and EP lab, with studies showing clinicians influence roughly 70% of device selection decisions in cardiac procedures in 2024. Training, ease-of-use and outcomes data—including lesion durability and complication rates—sway choices even within contracted lists. KOL advocacy can increase hospital adoption rates by 2–3x, helping offset purchasing scrutiny. Switching costs rise materially as procedure workflows, disposables and installed capital create integration and training expenses often equal to 20–25% of first-year procedural spend.

Reimbursement sensitivity

Hospitals prioritize predictable reimbursement and DRG margins under Medicare/Medicaid and commercial payers, so coverage shifts or coding/prior authorization changes directly depress elective demand. Technologies that demonstrably cut length of stay—US average inpatient LOS ~4.6 days—and reduce complications gain negotiating leverage. Economic value analyses and cost-offset data are now pivotal in payer and hospital contract negotiations.

Capital-plus-disposable economics

Razor-razorblade platform ties for AtriCure lock buyers into capital-plus-disposable economics, with bundled pricing and service agreements limiting buyer flexibility but increasing lifetime revenue predictability. Multi-vendor OR environments still allow competitive bids, keeping price pressure on disposables. Demonstrable utilization and outcomes data strengthen AtriCure’s negotiating power and justify premium pricing.

- Bundled lock-in

- Service constraints

- Multi-vendor competition

- Utilization = leverage

Outcome and data expectations

Customers demand RCT-level Afib endpoints and registry/RWE; atrial fibrillation affects ~33 million people worldwide and catheter ablation achieves ~60–70% 1-year freedom from AF, so payers/providers benchmark AtriCure against these outcomes and drug comparators; coverage hinges on comparative effectiveness and growing real-world evidence; post-market support and training influence retention and utilization.

- Outcomes focus: RCT/RWE vs catheter ablation (60–70% 1‑yr freedom)

- Coverage gatekeepers: comparative evidence vs drugs/ablation

- Registry/RWE: essential for reimbursement and adoption

- Post-market training: drives retention and repeat purchases

Buyers leverage: >60% beds, 90–95% GPO coverage; AF ablation 60–70% 1‑yr

Hospital consolidation gives buyers strong leverage—>60% US beds in systems (2024) and GPO coverage ~90–95%, driving double-digit price concessions. Clinician preference, KOLs and training mitigate leverage; switching costs ~20–25% of first‑year procedural spend. Payers demand TCO/RWE—AF affects ~33M globally; catheter ablation 60–70% 1‑yr freedom—so coverage hinges on comparative outcomes.

| Metric | Value (2024) |

|---|---|

| System bed share | >60% |

| GPO coverage | 90–95% |

| AF prevalence | ~33M |

| Ablation 1‑yr freedom | 60–70% |

Preview Before You Purchase

AtriCure Porter's Five Forces Analysis

This preview shows the exact AtriCure Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You’re looking at the actual file; instant access is granted upon payment.

From Overview to Strategy Blueprint

AtriCure’s Porter’s Five Forces snapshot highlights strong buyer scrutiny, significant supplier specialization, moderate threat from substitutes, high regulatory barriers, and intense rivalry among cardiac device makers. This brief overview surfaces key competitive pressures and strategic vulnerabilities. This preview is just the beginning—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialized biocompatible materials

Devices require high-spec polymers, nitinol, and biocompatible metals that must meet ISO 10993 biocompatibility and FDA device standards, raising material quality thresholds. Limited qualified suppliers for nitinol and cardiac-grade alloys concentrate leverage, increasing pricing and supply risk. Certification and validation per ISO 13485 and regulatory testing drive lengthy, costly supplier switches. Long lead times for specialty components can disrupt inventory and production planning.

Precision electronics and semiconductors

AtriCure's ablation and energy platforms depend on chips, sensors and power components with tight tolerances, making supplier precision critical. Semiconductor cyclicality and allocation can constrain availability and raise costs for medical OEMs. Redesigns to qualify alternate suppliers trigger costly regulatory workstreams—about 90% of devices use FDA 510(k) pathways—so supplier changes are burdensome. Strategic long-term agreements partially mitigate volatility.

Sterile disposables and contract manufacturing

Single-use ablation tools and accessories require validated sterile processes and Class III cardiac-quality systems, limiting the pool of qualified contract manufacturers and increasing supplier bargaining power.

Few CMOs possess the necessary ISO 13485 and FDA QSR maturity, so nonconformance can trigger recalls and production line stoppages that directly hit revenue and market supply.

Multi-sourcing and dual qualification mitigate exposure but do not eliminate dependency or the risk of simultaneous disruptions.

Regulatory and testing services

Accredited labs perform biocompatibility, reliability, and sterilization testing, and limited capacity or adverse findings can add roughly 3–6 months to regulatory timelines, delaying filings and launches. CROs controlling patient enrollment and site activation exert timing leverage; the global CRO market reached about $61 billion in 2024. Early engagement with vendors and selective in-house testing reduces AtriCure’s exposure.

- Dependency: accredited labs for biocompatibility/reliability

- Risk: capacity/findings → ~3–6 month delays

- CRO leverage: $61B CRO market (2024)

- Mitigation: early engagement + in‑house testing

Proprietary components and IP constraints

Custom tips, cables and coatings for Atricure devices are often single-sourced due to IP and tooling, giving suppliers leverage; tooling transfers and revalidations commonly add 6–12 months and FDA 510(k) median review was about 5 months in 2024, extending timelines. Suppliers can negotiate volume and pricing, impacting COGS, while contractual protections and VAVE programs help rebalance power.

- Single-sourcing: IP/tooling constraints

- Timelines: tooling transfers +6–12 months; FDA 510(k) ~5 months (2024)

- Mitigation: contracts, VAVE, supplier diversification

Supply risk: concentrated nitinol; certification adds 3–12m, CRO $61B

Supplier power is high due to concentrated nitinol/alloy sources, certified CMOs and labs; shortages and single‑sourcing raise COGS and disruption risk. Certification and design requalification add ~3–12 months; CRO market $61B (2024) and FDA 510(k) median review ~5 months (2024). Mitigants: long‑term contracts, multi‑sourcing, selective in‑house testing.

| Factor | Metric |

|---|---|

| Lab delays | 3–6 months |

| Tooling transfers | 6–12 months |

| CRO market | $61B (2024) |

| 510(k) median | ~5 months (2024) |

What is included in the product

Detailed Porter’s Five Forces analysis for AtriCure assessing competitive rivalry, buyer and supplier power, and threats from substitutes and new entrants; highlights disruptive technologies, pricing pressures, and entry barriers shaping the company’s profitability and strategic positioning.

AtriCure Porter’s Five Forces delivers a concise, one-sheet pain-point reliever—quickly highlighting competitive pressures, supplier/payer risks, and entrant threats for strategic decisions. Clean layout and customizable pressure levels make it easy to drop into decks or adapt for regulatory or market shifts.

Customers Bargaining Power

Hospital systems and IDNs

Hospital systems and IDNs centralize purchasing and enforce device formularies, with over 60% of U.S. hospital beds in systems by 2024, increasing leverage. Volume-based contracts and standardization drive double-digit price concessions; GPOs cover ~90–95% of hospitals, adding negotiation layers. Payers and IDNs demand total-cost-of-care evidence to justify price premiums, pressuring AtriCure to demonstrate reductions in readmissions and LOS.

Surgeon and EP preference

Clinician preference drives adoption in the OR and EP lab, with studies showing clinicians influence roughly 70% of device selection decisions in cardiac procedures in 2024. Training, ease-of-use and outcomes data—including lesion durability and complication rates—sway choices even within contracted lists. KOL advocacy can increase hospital adoption rates by 2–3x, helping offset purchasing scrutiny. Switching costs rise materially as procedure workflows, disposables and installed capital create integration and training expenses often equal to 20–25% of first-year procedural spend.

Reimbursement sensitivity

Hospitals prioritize predictable reimbursement and DRG margins under Medicare/Medicaid and commercial payers, so coverage shifts or coding/prior authorization changes directly depress elective demand. Technologies that demonstrably cut length of stay—US average inpatient LOS ~4.6 days—and reduce complications gain negotiating leverage. Economic value analyses and cost-offset data are now pivotal in payer and hospital contract negotiations.

Capital-plus-disposable economics

Razor-razorblade platform ties for AtriCure lock buyers into capital-plus-disposable economics, with bundled pricing and service agreements limiting buyer flexibility but increasing lifetime revenue predictability. Multi-vendor OR environments still allow competitive bids, keeping price pressure on disposables. Demonstrable utilization and outcomes data strengthen AtriCure’s negotiating power and justify premium pricing.

- Bundled lock-in

- Service constraints

- Multi-vendor competition

- Utilization = leverage

Outcome and data expectations

Customers demand RCT-level Afib endpoints and registry/RWE; atrial fibrillation affects ~33 million people worldwide and catheter ablation achieves ~60–70% 1-year freedom from AF, so payers/providers benchmark AtriCure against these outcomes and drug comparators; coverage hinges on comparative effectiveness and growing real-world evidence; post-market support and training influence retention and utilization.

- Outcomes focus: RCT/RWE vs catheter ablation (60–70% 1‑yr freedom)

- Coverage gatekeepers: comparative evidence vs drugs/ablation

- Registry/RWE: essential for reimbursement and adoption

- Post-market training: drives retention and repeat purchases

Buyers leverage: >60% beds, 90–95% GPO coverage; AF ablation 60–70% 1‑yr

Hospital consolidation gives buyers strong leverage—>60% US beds in systems (2024) and GPO coverage ~90–95%, driving double-digit price concessions. Clinician preference, KOLs and training mitigate leverage; switching costs ~20–25% of first‑year procedural spend. Payers demand TCO/RWE—AF affects ~33M globally; catheter ablation 60–70% 1‑yr freedom—so coverage hinges on comparative outcomes.

| Metric | Value (2024) |

|---|---|

| System bed share | >60% |

| GPO coverage | 90–95% |

| AF prevalence | ~33M |

| Ablation 1‑yr freedom | 60–70% |

Preview Before You Purchase

AtriCure Porter's Five Forces Analysis

This preview shows the exact AtriCure Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You’re looking at the actual file; instant access is granted upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

AtriCure’s Porter’s Five Forces snapshot highlights strong buyer scrutiny, significant supplier specialization, moderate threat from substitutes, high regulatory barriers, and intense rivalry among cardiac device makers. This brief overview surfaces key competitive pressures and strategic vulnerabilities. This preview is just the beginning—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialized biocompatible materials

Devices require high-spec polymers, nitinol, and biocompatible metals that must meet ISO 10993 biocompatibility and FDA device standards, raising material quality thresholds. Limited qualified suppliers for nitinol and cardiac-grade alloys concentrate leverage, increasing pricing and supply risk. Certification and validation per ISO 13485 and regulatory testing drive lengthy, costly supplier switches. Long lead times for specialty components can disrupt inventory and production planning.

Precision electronics and semiconductors

AtriCure's ablation and energy platforms depend on chips, sensors and power components with tight tolerances, making supplier precision critical. Semiconductor cyclicality and allocation can constrain availability and raise costs for medical OEMs. Redesigns to qualify alternate suppliers trigger costly regulatory workstreams—about 90% of devices use FDA 510(k) pathways—so supplier changes are burdensome. Strategic long-term agreements partially mitigate volatility.

Sterile disposables and contract manufacturing

Single-use ablation tools and accessories require validated sterile processes and Class III cardiac-quality systems, limiting the pool of qualified contract manufacturers and increasing supplier bargaining power.

Few CMOs possess the necessary ISO 13485 and FDA QSR maturity, so nonconformance can trigger recalls and production line stoppages that directly hit revenue and market supply.

Multi-sourcing and dual qualification mitigate exposure but do not eliminate dependency or the risk of simultaneous disruptions.

Regulatory and testing services

Accredited labs perform biocompatibility, reliability, and sterilization testing, and limited capacity or adverse findings can add roughly 3–6 months to regulatory timelines, delaying filings and launches. CROs controlling patient enrollment and site activation exert timing leverage; the global CRO market reached about $61 billion in 2024. Early engagement with vendors and selective in-house testing reduces AtriCure’s exposure.

- Dependency: accredited labs for biocompatibility/reliability

- Risk: capacity/findings → ~3–6 month delays

- CRO leverage: $61B CRO market (2024)

- Mitigation: early engagement + in‑house testing

Proprietary components and IP constraints

Custom tips, cables and coatings for Atricure devices are often single-sourced due to IP and tooling, giving suppliers leverage; tooling transfers and revalidations commonly add 6–12 months and FDA 510(k) median review was about 5 months in 2024, extending timelines. Suppliers can negotiate volume and pricing, impacting COGS, while contractual protections and VAVE programs help rebalance power.

- Single-sourcing: IP/tooling constraints

- Timelines: tooling transfers +6–12 months; FDA 510(k) ~5 months (2024)

- Mitigation: contracts, VAVE, supplier diversification

Supply risk: concentrated nitinol; certification adds 3–12m, CRO $61B

Supplier power is high due to concentrated nitinol/alloy sources, certified CMOs and labs; shortages and single‑sourcing raise COGS and disruption risk. Certification and design requalification add ~3–12 months; CRO market $61B (2024) and FDA 510(k) median review ~5 months (2024). Mitigants: long‑term contracts, multi‑sourcing, selective in‑house testing.

| Factor | Metric |

|---|---|

| Lab delays | 3–6 months |

| Tooling transfers | 6–12 months |

| CRO market | $61B (2024) |

| 510(k) median | ~5 months (2024) |

What is included in the product

Detailed Porter’s Five Forces analysis for AtriCure assessing competitive rivalry, buyer and supplier power, and threats from substitutes and new entrants; highlights disruptive technologies, pricing pressures, and entry barriers shaping the company’s profitability and strategic positioning.

AtriCure Porter’s Five Forces delivers a concise, one-sheet pain-point reliever—quickly highlighting competitive pressures, supplier/payer risks, and entrant threats for strategic decisions. Clean layout and customizable pressure levels make it easy to drop into decks or adapt for regulatory or market shifts.

Customers Bargaining Power

Hospital systems and IDNs

Hospital systems and IDNs centralize purchasing and enforce device formularies, with over 60% of U.S. hospital beds in systems by 2024, increasing leverage. Volume-based contracts and standardization drive double-digit price concessions; GPOs cover ~90–95% of hospitals, adding negotiation layers. Payers and IDNs demand total-cost-of-care evidence to justify price premiums, pressuring AtriCure to demonstrate reductions in readmissions and LOS.

Surgeon and EP preference

Clinician preference drives adoption in the OR and EP lab, with studies showing clinicians influence roughly 70% of device selection decisions in cardiac procedures in 2024. Training, ease-of-use and outcomes data—including lesion durability and complication rates—sway choices even within contracted lists. KOL advocacy can increase hospital adoption rates by 2–3x, helping offset purchasing scrutiny. Switching costs rise materially as procedure workflows, disposables and installed capital create integration and training expenses often equal to 20–25% of first-year procedural spend.

Reimbursement sensitivity

Hospitals prioritize predictable reimbursement and DRG margins under Medicare/Medicaid and commercial payers, so coverage shifts or coding/prior authorization changes directly depress elective demand. Technologies that demonstrably cut length of stay—US average inpatient LOS ~4.6 days—and reduce complications gain negotiating leverage. Economic value analyses and cost-offset data are now pivotal in payer and hospital contract negotiations.

Capital-plus-disposable economics

Razor-razorblade platform ties for AtriCure lock buyers into capital-plus-disposable economics, with bundled pricing and service agreements limiting buyer flexibility but increasing lifetime revenue predictability. Multi-vendor OR environments still allow competitive bids, keeping price pressure on disposables. Demonstrable utilization and outcomes data strengthen AtriCure’s negotiating power and justify premium pricing.

- Bundled lock-in

- Service constraints

- Multi-vendor competition

- Utilization = leverage

Outcome and data expectations

Customers demand RCT-level Afib endpoints and registry/RWE; atrial fibrillation affects ~33 million people worldwide and catheter ablation achieves ~60–70% 1-year freedom from AF, so payers/providers benchmark AtriCure against these outcomes and drug comparators; coverage hinges on comparative effectiveness and growing real-world evidence; post-market support and training influence retention and utilization.

- Outcomes focus: RCT/RWE vs catheter ablation (60–70% 1‑yr freedom)

- Coverage gatekeepers: comparative evidence vs drugs/ablation

- Registry/RWE: essential for reimbursement and adoption

- Post-market training: drives retention and repeat purchases

Buyers leverage: >60% beds, 90–95% GPO coverage; AF ablation 60–70% 1‑yr

Hospital consolidation gives buyers strong leverage—>60% US beds in systems (2024) and GPO coverage ~90–95%, driving double-digit price concessions. Clinician preference, KOLs and training mitigate leverage; switching costs ~20–25% of first‑year procedural spend. Payers demand TCO/RWE—AF affects ~33M globally; catheter ablation 60–70% 1‑yr freedom—so coverage hinges on comparative outcomes.

| Metric | Value (2024) |

|---|---|

| System bed share | >60% |

| GPO coverage | 90–95% |

| AF prevalence | ~33M |

| Ablation 1‑yr freedom | 60–70% |

Preview Before You Purchase

AtriCure Porter's Five Forces Analysis

This preview shows the exact AtriCure Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy. You’re looking at the actual file; instant access is granted upon payment.