Aurionpro Solutions Porter's Five Forces Analysis

Don't Miss the Bigger Picture

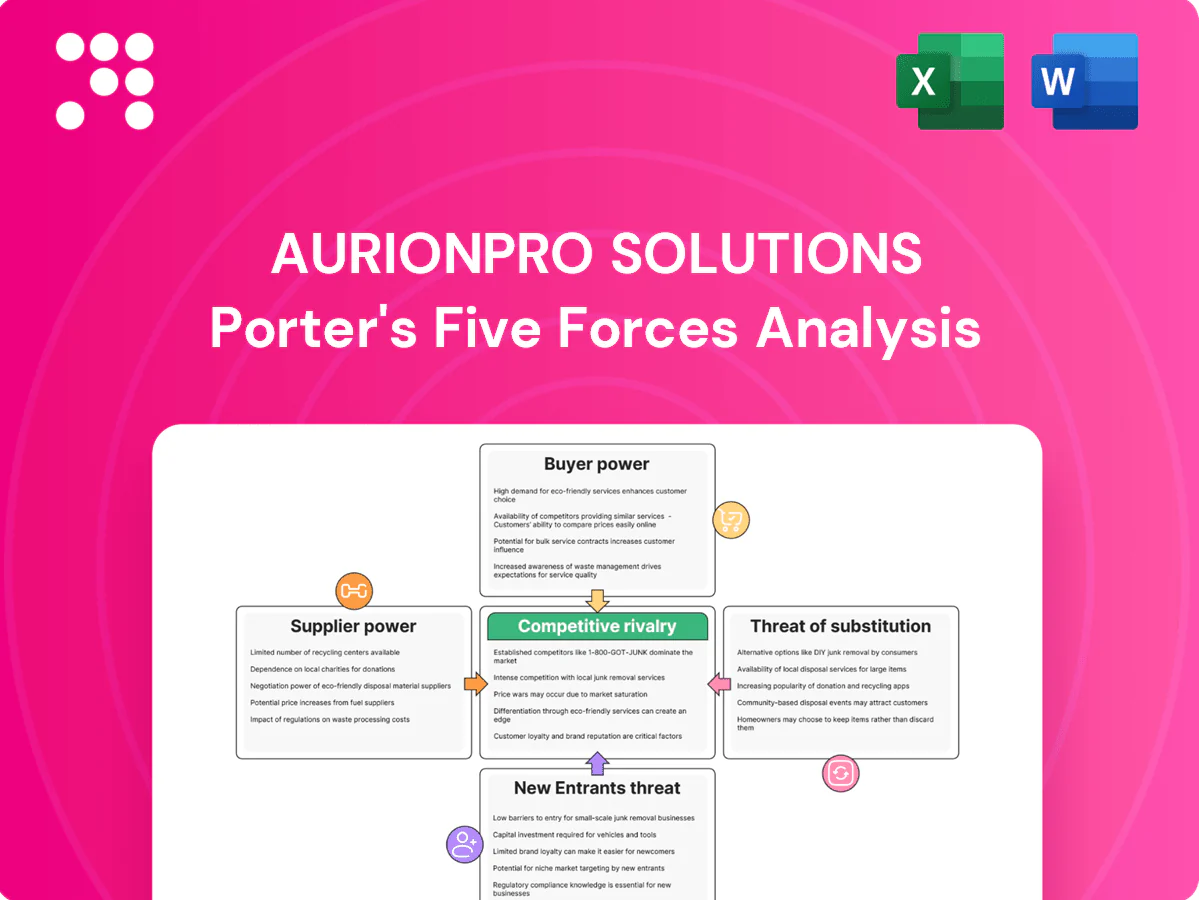

Aurionpro Solutions faces moderate buyer power, niche supplier relationships, rising digital substitutes, and cautious entrant risk due to regulatory and scale barriers. Competitive rivalry is intense among fintech-focused integrators, but strong IP and client relationships are defensive advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aurionpro Solutions’s competitive dynamics in detail.

Suppliers Bargaining Power

Hyperscale cloud dependence

Aurionpro depends on AWS (~32% share), Azure (~23%) and GCP (~11%) in 2024, exposing it to pricing shifts and technical limits from suppliers; multi-cloud reduces lock-in but typically raises costs 10–25% and complexity. Volume commitments and partner tiers improve leverage, yet premium security and AI offerings remain price-led, while outages and compliance needs further boost supplier bargaining power.

Specialized talent scarcity

Deep skills in banking, payments, cybersecurity and mobility are scarce, with the 2024 ISC2 gap for cybersecurity at about 3.4 million, giving niche contractors and recruiters strong leverage. Wage inflation (roughly 8–12% in tech roles in 2023–24) and 15–20% attrition elevate delivery costs and schedule risk. Building captive pipelines can cut exposure but typically requires 12–24 months. Certifications and security clearances can add 30–60 days to hiring timelines.

Core software and tool vendors

Dependencies on databases, security suites, DevSecOps tools and payment gateways create high switching costs and lock-in for Aurionpro; vendors increasingly bundle features and push maintenance fees, commonly around 20% of license value annually. Enterprise agreements and growing open-source use (≈65% of enterprises in 2024) temper supplier power but often fail strict compliance needs. Integration certifications tie Aurionpro to vendor roadmaps, constraining flexibility and capex planning.

Hardware and edge device suppliers

Hardware and edge device suppliers for mobility and security solutions remain concentrated, and in 2024 regulatory requirements (PCI DSS, FIPS 140-3) kept certified HSMs and secure IoT modules in a narrow supplier pool, raising supplier bargaining power.

Component volatility and lead-time variability continued in 2024, delaying deployments; bulk buying and dual-sourcing mitigate risk but are often constrained by certification and cost.

- Limited certified vendors increase supplier leverage

- Lead-time variability delays rollouts

- Bulk purchase/dual-source reduce risk but raise costs

- Regulatory-grade hardware narrows options

Data and compliance services

Access to KYC/AML datasets, identity verification and fraud intelligence for Aurionpro depend on specialized providers, with the global identity verification market ~4.0 billion USD in 2024, concentrating supplier power. Usage-based pricing creates variable OPEX exposure and can swing project costs by double-digit percentages. SLAs, indemnities and required vendor audits/certifications limit buyer leverage and add recurring overhead.

- High dependency: 60–80% of critical datasets from 3rd parties

- Cost volatility: usage fees can alter OPEX by 10–30%

- Compliance burden: annual audit/cert costs add fixed overhead

Supplier power hits margins: cloud 32%/23%/11%, identity $4.0bn

Aurionpro faces strong supplier power in cloud (AWS 32%, Azure 23%, GCP 11% in 2024), niche security/hardware vendors and identity data providers (~$4.0bn market) driving pricing and lead-time risk; multi-cloud and bulk buys reduce lock-in but raise costs 10–25% and complexity.

| Area | 2024 Metric | Impact |

|---|---|---|

| Cloud share | AWS 32%/Azure 23%/GCP 11% | Pricing exposure |

| Identity market | $4.0bn | Concentrated suppliers |

| Tech attrition | 15–20% | Hiring cost |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Aurionpro Solutions, while identifying disruptive substitutes and emerging threats to market share. Evaluates supplier and buyer power and market dynamics that deter new entrants, presented in an editable format for investor materials and strategy decks.

Aurionpro Solutions Porter's Five Forces Analysis condenses competitive pressures into a single, actionable view for faster strategic decisions, with editable force levels and a ready-to-share radar chart for boardroom clarity.

Customers Bargaining Power

Large enterprise buyers

Banks, payment networks and transit authorities command big-ticket deals often exceeding $1M and run competitive RFPs that demand volume discounts and outcome-based pricing. Long sales cycles, typically 12–18 months, and stringent compliance requirements shift bargaining power toward these buyers. Strong referenceability and demonstrable RoI are essential for Aurionpro to defend pricing and win renewals.

High switching costs

Deep integration with Aurionpro platforms creates strong lock-in, yet phased rebids commonly shave 10–15% off renewal pricing. Open APIs and interoperability standards erode captivity over 2–4 years. Data migration and regulatory testing typically make switching a 6–12 month, $0.5–2M process, so managed-service transitions are leveraged to extract concessions.

Price-performance scrutiny

Buyers benchmark Aurionpro against global SIs and SaaS vendors to press rates and demand 99.9–99.99% uptime SLAs; in 2024 enterprise procurement emphasized measurable KPIs on uptime, fraud reduction and time-to-market improvements measured in weeks. Gainshare and penalty clauses increasingly shift contract risk to vendors, often tying 10–30% of fees to outcomes. Transparent TCO models are required to protect margins.

Customization demands

Regulated clients force Aurionpro to deliver tailored features, driving scope creep risk and requiring stricter change-control to protect margins. Customization raises switching costs but compresses timelines and budgets, increasing delivery and compliance scrutiny in 2024. Buyers now expect reusable accelerators to limit bespoke expense, shifting negotiation leverage toward clear governance.

- Scope creep risk

- Higher switching costs

- Pressure on timelines/budgets

- Demand for reusable accelerators

- Need for change-control governance

Consolidation and vendor rationalization

Consolidation and vendor rationalization have pushed enterprises to cut supplier counts, intensifying competition among vendors for strategic slots and forcing Aurionpro to defend margins as framework agreements increasingly cap rates across portfolios. Cross-sell opportunities rise with larger accounts, but concession pressure grows as buyers leverage bundled pricing and standardized SLAs. Strong account management and integrated service offerings can partially offset buyer leverage by demonstrating differentiated value and reducing switching risk.

- Vendor cuts concentrate spend with fewer partners

- Framework agreements cap portfolio rates

- Cross-sell up; margin concession pressure up

- Account management mitigates but does not eliminate buyer power

Power play: 12–18mo, 10–30% fees

Banks, payment networks and transit authorities wield strong negotiating leverage via competitive RFPs, long 12–18 month sales cycles and outcome-based clauses (10–30% fees tied to KPIs). Renewals often see 10–15% price erosion; switching costs run $0.5–2M and 6–12 months. 99.9–99.99% SLAs and reusable accelerators shape concessions and governance.

| Metric | 2024 Value |

|---|---|

| Sales cycle | 12–18 months |

| Renewal price cut | 10–15% |

| Switch cost | $0.5–2M / 6–12 months |

| Outcome fees | 10–30% |

| Uptime SLA | 99.9–99.99% |

Full Version Awaits

Aurionpro Solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Aurionpro Solutions you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants with data-backed insights. It's fully formatted and ready for immediate download and use.

Don't Miss the Bigger Picture

Aurionpro Solutions faces moderate buyer power, niche supplier relationships, rising digital substitutes, and cautious entrant risk due to regulatory and scale barriers. Competitive rivalry is intense among fintech-focused integrators, but strong IP and client relationships are defensive advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aurionpro Solutions’s competitive dynamics in detail.

Suppliers Bargaining Power

Hyperscale cloud dependence

Aurionpro depends on AWS (~32% share), Azure (~23%) and GCP (~11%) in 2024, exposing it to pricing shifts and technical limits from suppliers; multi-cloud reduces lock-in but typically raises costs 10–25% and complexity. Volume commitments and partner tiers improve leverage, yet premium security and AI offerings remain price-led, while outages and compliance needs further boost supplier bargaining power.

Specialized talent scarcity

Deep skills in banking, payments, cybersecurity and mobility are scarce, with the 2024 ISC2 gap for cybersecurity at about 3.4 million, giving niche contractors and recruiters strong leverage. Wage inflation (roughly 8–12% in tech roles in 2023–24) and 15–20% attrition elevate delivery costs and schedule risk. Building captive pipelines can cut exposure but typically requires 12–24 months. Certifications and security clearances can add 30–60 days to hiring timelines.

Core software and tool vendors

Dependencies on databases, security suites, DevSecOps tools and payment gateways create high switching costs and lock-in for Aurionpro; vendors increasingly bundle features and push maintenance fees, commonly around 20% of license value annually. Enterprise agreements and growing open-source use (≈65% of enterprises in 2024) temper supplier power but often fail strict compliance needs. Integration certifications tie Aurionpro to vendor roadmaps, constraining flexibility and capex planning.

Hardware and edge device suppliers

Hardware and edge device suppliers for mobility and security solutions remain concentrated, and in 2024 regulatory requirements (PCI DSS, FIPS 140-3) kept certified HSMs and secure IoT modules in a narrow supplier pool, raising supplier bargaining power.

Component volatility and lead-time variability continued in 2024, delaying deployments; bulk buying and dual-sourcing mitigate risk but are often constrained by certification and cost.

- Limited certified vendors increase supplier leverage

- Lead-time variability delays rollouts

- Bulk purchase/dual-source reduce risk but raise costs

- Regulatory-grade hardware narrows options

Data and compliance services

Access to KYC/AML datasets, identity verification and fraud intelligence for Aurionpro depend on specialized providers, with the global identity verification market ~4.0 billion USD in 2024, concentrating supplier power. Usage-based pricing creates variable OPEX exposure and can swing project costs by double-digit percentages. SLAs, indemnities and required vendor audits/certifications limit buyer leverage and add recurring overhead.

- High dependency: 60–80% of critical datasets from 3rd parties

- Cost volatility: usage fees can alter OPEX by 10–30%

- Compliance burden: annual audit/cert costs add fixed overhead

Supplier power hits margins: cloud 32%/23%/11%, identity $4.0bn

Aurionpro faces strong supplier power in cloud (AWS 32%, Azure 23%, GCP 11% in 2024), niche security/hardware vendors and identity data providers (~$4.0bn market) driving pricing and lead-time risk; multi-cloud and bulk buys reduce lock-in but raise costs 10–25% and complexity.

| Area | 2024 Metric | Impact |

|---|---|---|

| Cloud share | AWS 32%/Azure 23%/GCP 11% | Pricing exposure |

| Identity market | $4.0bn | Concentrated suppliers |

| Tech attrition | 15–20% | Hiring cost |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Aurionpro Solutions, while identifying disruptive substitutes and emerging threats to market share. Evaluates supplier and buyer power and market dynamics that deter new entrants, presented in an editable format for investor materials and strategy decks.

Aurionpro Solutions Porter's Five Forces Analysis condenses competitive pressures into a single, actionable view for faster strategic decisions, with editable force levels and a ready-to-share radar chart for boardroom clarity.

Customers Bargaining Power

Large enterprise buyers

Banks, payment networks and transit authorities command big-ticket deals often exceeding $1M and run competitive RFPs that demand volume discounts and outcome-based pricing. Long sales cycles, typically 12–18 months, and stringent compliance requirements shift bargaining power toward these buyers. Strong referenceability and demonstrable RoI are essential for Aurionpro to defend pricing and win renewals.

High switching costs

Deep integration with Aurionpro platforms creates strong lock-in, yet phased rebids commonly shave 10–15% off renewal pricing. Open APIs and interoperability standards erode captivity over 2–4 years. Data migration and regulatory testing typically make switching a 6–12 month, $0.5–2M process, so managed-service transitions are leveraged to extract concessions.

Price-performance scrutiny

Buyers benchmark Aurionpro against global SIs and SaaS vendors to press rates and demand 99.9–99.99% uptime SLAs; in 2024 enterprise procurement emphasized measurable KPIs on uptime, fraud reduction and time-to-market improvements measured in weeks. Gainshare and penalty clauses increasingly shift contract risk to vendors, often tying 10–30% of fees to outcomes. Transparent TCO models are required to protect margins.

Customization demands

Regulated clients force Aurionpro to deliver tailored features, driving scope creep risk and requiring stricter change-control to protect margins. Customization raises switching costs but compresses timelines and budgets, increasing delivery and compliance scrutiny in 2024. Buyers now expect reusable accelerators to limit bespoke expense, shifting negotiation leverage toward clear governance.

- Scope creep risk

- Higher switching costs

- Pressure on timelines/budgets

- Demand for reusable accelerators

- Need for change-control governance

Consolidation and vendor rationalization

Consolidation and vendor rationalization have pushed enterprises to cut supplier counts, intensifying competition among vendors for strategic slots and forcing Aurionpro to defend margins as framework agreements increasingly cap rates across portfolios. Cross-sell opportunities rise with larger accounts, but concession pressure grows as buyers leverage bundled pricing and standardized SLAs. Strong account management and integrated service offerings can partially offset buyer leverage by demonstrating differentiated value and reducing switching risk.

- Vendor cuts concentrate spend with fewer partners

- Framework agreements cap portfolio rates

- Cross-sell up; margin concession pressure up

- Account management mitigates but does not eliminate buyer power

Power play: 12–18mo, 10–30% fees

Banks, payment networks and transit authorities wield strong negotiating leverage via competitive RFPs, long 12–18 month sales cycles and outcome-based clauses (10–30% fees tied to KPIs). Renewals often see 10–15% price erosion; switching costs run $0.5–2M and 6–12 months. 99.9–99.99% SLAs and reusable accelerators shape concessions and governance.

| Metric | 2024 Value |

|---|---|

| Sales cycle | 12–18 months |

| Renewal price cut | 10–15% |

| Switch cost | $0.5–2M / 6–12 months |

| Outcome fees | 10–30% |

| Uptime SLA | 99.9–99.99% |

Full Version Awaits

Aurionpro Solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Aurionpro Solutions you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants with data-backed insights. It's fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Aurionpro Solutions faces moderate buyer power, niche supplier relationships, rising digital substitutes, and cautious entrant risk due to regulatory and scale barriers. Competitive rivalry is intense among fintech-focused integrators, but strong IP and client relationships are defensive advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aurionpro Solutions’s competitive dynamics in detail.

Suppliers Bargaining Power

Hyperscale cloud dependence

Aurionpro depends on AWS (~32% share), Azure (~23%) and GCP (~11%) in 2024, exposing it to pricing shifts and technical limits from suppliers; multi-cloud reduces lock-in but typically raises costs 10–25% and complexity. Volume commitments and partner tiers improve leverage, yet premium security and AI offerings remain price-led, while outages and compliance needs further boost supplier bargaining power.

Specialized talent scarcity

Deep skills in banking, payments, cybersecurity and mobility are scarce, with the 2024 ISC2 gap for cybersecurity at about 3.4 million, giving niche contractors and recruiters strong leverage. Wage inflation (roughly 8–12% in tech roles in 2023–24) and 15–20% attrition elevate delivery costs and schedule risk. Building captive pipelines can cut exposure but typically requires 12–24 months. Certifications and security clearances can add 30–60 days to hiring timelines.

Core software and tool vendors

Dependencies on databases, security suites, DevSecOps tools and payment gateways create high switching costs and lock-in for Aurionpro; vendors increasingly bundle features and push maintenance fees, commonly around 20% of license value annually. Enterprise agreements and growing open-source use (≈65% of enterprises in 2024) temper supplier power but often fail strict compliance needs. Integration certifications tie Aurionpro to vendor roadmaps, constraining flexibility and capex planning.

Hardware and edge device suppliers

Hardware and edge device suppliers for mobility and security solutions remain concentrated, and in 2024 regulatory requirements (PCI DSS, FIPS 140-3) kept certified HSMs and secure IoT modules in a narrow supplier pool, raising supplier bargaining power.

Component volatility and lead-time variability continued in 2024, delaying deployments; bulk buying and dual-sourcing mitigate risk but are often constrained by certification and cost.

- Limited certified vendors increase supplier leverage

- Lead-time variability delays rollouts

- Bulk purchase/dual-source reduce risk but raise costs

- Regulatory-grade hardware narrows options

Data and compliance services

Access to KYC/AML datasets, identity verification and fraud intelligence for Aurionpro depend on specialized providers, with the global identity verification market ~4.0 billion USD in 2024, concentrating supplier power. Usage-based pricing creates variable OPEX exposure and can swing project costs by double-digit percentages. SLAs, indemnities and required vendor audits/certifications limit buyer leverage and add recurring overhead.

- High dependency: 60–80% of critical datasets from 3rd parties

- Cost volatility: usage fees can alter OPEX by 10–30%

- Compliance burden: annual audit/cert costs add fixed overhead

Supplier power hits margins: cloud 32%/23%/11%, identity $4.0bn

Aurionpro faces strong supplier power in cloud (AWS 32%, Azure 23%, GCP 11% in 2024), niche security/hardware vendors and identity data providers (~$4.0bn market) driving pricing and lead-time risk; multi-cloud and bulk buys reduce lock-in but raise costs 10–25% and complexity.

| Area | 2024 Metric | Impact |

|---|---|---|

| Cloud share | AWS 32%/Azure 23%/GCP 11% | Pricing exposure |

| Identity market | $4.0bn | Concentrated suppliers |

| Tech attrition | 15–20% | Hiring cost |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Aurionpro Solutions, while identifying disruptive substitutes and emerging threats to market share. Evaluates supplier and buyer power and market dynamics that deter new entrants, presented in an editable format for investor materials and strategy decks.

Aurionpro Solutions Porter's Five Forces Analysis condenses competitive pressures into a single, actionable view for faster strategic decisions, with editable force levels and a ready-to-share radar chart for boardroom clarity.

Customers Bargaining Power

Large enterprise buyers

Banks, payment networks and transit authorities command big-ticket deals often exceeding $1M and run competitive RFPs that demand volume discounts and outcome-based pricing. Long sales cycles, typically 12–18 months, and stringent compliance requirements shift bargaining power toward these buyers. Strong referenceability and demonstrable RoI are essential for Aurionpro to defend pricing and win renewals.

High switching costs

Deep integration with Aurionpro platforms creates strong lock-in, yet phased rebids commonly shave 10–15% off renewal pricing. Open APIs and interoperability standards erode captivity over 2–4 years. Data migration and regulatory testing typically make switching a 6–12 month, $0.5–2M process, so managed-service transitions are leveraged to extract concessions.

Price-performance scrutiny

Buyers benchmark Aurionpro against global SIs and SaaS vendors to press rates and demand 99.9–99.99% uptime SLAs; in 2024 enterprise procurement emphasized measurable KPIs on uptime, fraud reduction and time-to-market improvements measured in weeks. Gainshare and penalty clauses increasingly shift contract risk to vendors, often tying 10–30% of fees to outcomes. Transparent TCO models are required to protect margins.

Customization demands

Regulated clients force Aurionpro to deliver tailored features, driving scope creep risk and requiring stricter change-control to protect margins. Customization raises switching costs but compresses timelines and budgets, increasing delivery and compliance scrutiny in 2024. Buyers now expect reusable accelerators to limit bespoke expense, shifting negotiation leverage toward clear governance.

- Scope creep risk

- Higher switching costs

- Pressure on timelines/budgets

- Demand for reusable accelerators

- Need for change-control governance

Consolidation and vendor rationalization

Consolidation and vendor rationalization have pushed enterprises to cut supplier counts, intensifying competition among vendors for strategic slots and forcing Aurionpro to defend margins as framework agreements increasingly cap rates across portfolios. Cross-sell opportunities rise with larger accounts, but concession pressure grows as buyers leverage bundled pricing and standardized SLAs. Strong account management and integrated service offerings can partially offset buyer leverage by demonstrating differentiated value and reducing switching risk.

- Vendor cuts concentrate spend with fewer partners

- Framework agreements cap portfolio rates

- Cross-sell up; margin concession pressure up

- Account management mitigates but does not eliminate buyer power

Power play: 12–18mo, 10–30% fees

Banks, payment networks and transit authorities wield strong negotiating leverage via competitive RFPs, long 12–18 month sales cycles and outcome-based clauses (10–30% fees tied to KPIs). Renewals often see 10–15% price erosion; switching costs run $0.5–2M and 6–12 months. 99.9–99.99% SLAs and reusable accelerators shape concessions and governance.

| Metric | 2024 Value |

|---|---|

| Sales cycle | 12–18 months |

| Renewal price cut | 10–15% |

| Switch cost | $0.5–2M / 6–12 months |

| Outcome fees | 10–30% |

| Uptime SLA | 99.9–99.99% |

Full Version Awaits

Aurionpro Solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Aurionpro Solutions you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants with data-backed insights. It's fully formatted and ready for immediate download and use.