Aurobindo Pharma Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Aurobindo Pharma faces intense industry rivalry driven by global generics competition and price pressure; buyer power is high among large purchasers while supplier power is moderate due to diversified API sources. Regulatory barriers limit new entrants but substitute therapies and margin compression remain tangible threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Aurobindo Pharma’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse API sources dilute leverage

Aurobindo sources APIs and key starting materials from multiple regions — India, China and Europe — diluting dependence on any single vendor as of 2024. This geographic diversification curbs supplier pricing power and reduces risk of wide-scale supply disruptions. Concentration remains for certain specialized intermediates and solvents, raising niche-input vulnerability. Strategic dual-sourcing and selective backward integration further buffer supplier influence.

Backward integration into APIs

By 2024 Aurobindo's backward integration into APIs reduces reliance on external suppliers for key molecules, strengthening cost control, quality oversight and supply assurance and thus shrinking supplier bargaining power. Capital intensity and regulatory compliance keep full integration impractical across all products, maintaining selective external sourcing. The current mix of internal and external APIs balances operational flexibility with resilience.

Regulatory-grade inputs constrain alternatives

Pharma-grade materials must meet stringent regulatory standards, narrowing the pool of qualified suppliers and increasing supplier leverage for critical APIs and excipients. Fewer compliant vendors can command better terms for select inputs, while approved-supplier lists and validation cycles—typically 6–18 months in 2024—raise switching costs for Aurobindo. Long-term quality agreements with volume commitments partially offset pricing pressure through predictable off-take and negotiated rebates.

Logistics and geopolitical exposure

Global supply chains for solvents, intermediates and packaging face freight volatility and geopolitical risks; container spot rates jumped about 30% after Red Sea disruptions in H1 2024, shifting leverage to suppliers with assured capacity. Aurobindo mitigates via regional stocking, multi-LOC approvals and selective nearshoring, while indexed supplier contracts pass volatility into higher input costs.

- Freight spike ~30% H1 2024

- Regional stocking reduces stockouts

- Multi-LOC approvals increase sourcing flexibility

- Indexed contracts share, but raise, input costs

Commoditized packaging vs specialized equipment

For Aurobindo Pharma, 2024 industry data shows over 75% of common packaging materials are commoditized, keeping supplier power low and price competition high. Conversely, specialized equipment, filters and single-use systems are concentrated: the top 4 OEMs account for roughly 65% of market share, creating supplier leverage. Lead times of 6–12 months plus lengthy validation increase switching costs, while lifecycle service agreements commonly embed an 8–12% premium.

Geographic diversification and API integration cut supplier power; freight +30% hikes switching costs

Aurobindo's geographic diversification and backward integration in APIs (2024) limit supplier leverage for commoditized inputs, though niche intermediates and validated suppliers retain pricing power. Supply shocks (container rates +30% H1 2024) and long validation/lead times (6–18 months; 6–12 months) raise switching costs. Packaging largely commoditized (>75%), while top-4 OEMs hold ~65%.

| Metric | Value (2024) |

|---|---|

| Packaging commoditized | >75% |

| Top-4 OEM share | ≈65% |

| Freight spike H1 | ~30% |

| Validation/lead times | 6–18 / 6–12 months |

What is included in the product

Tailored Porter's Five Forces for Aurobindo Pharma assessing rivalry, buyer/supplier power, threats from generics and biosimilars, substitute medicines, and entry barriers shaping its pricing, margins, and strategic risks.

Clear, one-sheet Porter's Five Forces for Aurobindo Pharma—instantly spot supplier, buyer, and regulatory pressures to guide strategic responses and ease executive decision-making.

Customers Bargaining Power

Large institutional buyers negotiate hard

Large institutional buyers — government tenders, GPOs and the three US wholesalers (McKesson, AmerisourceBergen, Cardinal) that together handle about 85% of US pharmaceutical distribution — aggregate demand and exert strong price and service-level pressure. Aurobindo must compete on price, reliability and product breadth, compressing margins in mature molecules. Preferential contracts raise volume visibility while increasing rebate and service commitments.

Product commoditization heightens price sensitivity

Generic drugs are largely interchangeable once deemed bioequivalent by regulators, and with generics accounting for about 90% of U.S. prescriptions by volume (FDA), buyers prioritize lowest total cost, boosting switching and negotiation power versus suppliers like Aurobindo.

Differentiation through superior dossier quality, fill rates and regulatory compliance can modestly defend share.

During supply shortages, temporary reliability premiums can reverse customer leverage.

Regulatory and quality performance as a lever

Buyers of Aurobindo prioritize consistent cGMP compliance and on-time delivery to avoid stockouts and contract penalties; strong audit histories with regulators raise trust and reduce pressure for price concessions. Any compliance lapse or inspection finding would immediately strengthen buyer bargaining power and could trigger delisting risk. Transparent quality metrics, public audit outcomes and manufacturing redundancy visibly lower perceived buyer risk and preserve negotiating leverage.

Portfolio breadth and bundling

Aurobindo’s portfolio of over 1,500 products across 150+ countries enables bundling across molecules and markets; bundles let it trade price for share gains and greater customer stickiness, tempering buyer power. Sophisticated buyers (large chains, governments) can decouple lines to maximize savings, pressuring margins. Cross-supply agreements and multi-year framework contracts help stabilize pricing and volume.

- Portfolio: 1,500+ products; 150+ markets

- Bargaining: bundles reduce churn but large buyers decouple

- Contracts: cross-supply & framework deals stabilize terms

International market mix

- US/EU pressure: high; ~60% revenue exposure

- FY2024 revenue: ~INR 36,000 crore

- Emerging markets: fragmented, higher pricing power

- Mitigants: currency diversification, local partnerships

Buyers squeeze margins; 1,500+ SKUs, bundling partly offsets, FY24 revenue ~INR 36,000cr

Large institutional buyers (US wholesalers, GPOs, governments) exert strong price/service pressure, compressing margins; generics' interchangeability (≈90% US Rx) increases switching power. Aurobindo's 1,500+ product portfolio and bundling plus cross-supply contracts partially mitigate leverage; compliance and on‑time delivery critically reduce buyer bargaining. FY2024 revenue ~INR 36,000 crore with ~60% from US/EU.

| Metric | Value |

|---|---|

| FY2024 revenue | ~INR 36,000 crore |

| US/EU share | ~60% |

| Products/Markets | 1,500+ / 150+ |

| US generic Rx | ~90% |

| Three US wholesalers | ~85% distribution |

What You See Is What You Get

Aurobindo Pharma Porter's Five Forces Analysis

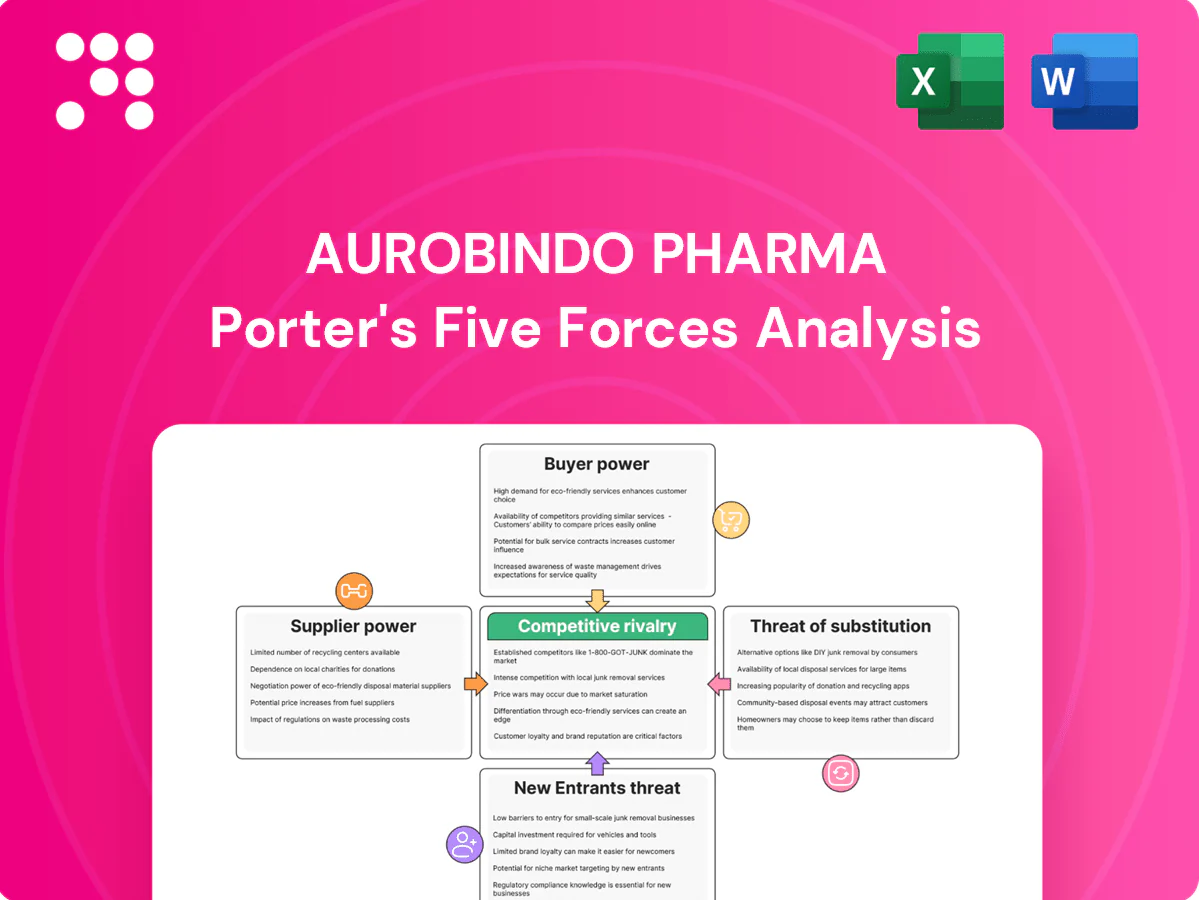

This preview shows the exact Aurobindo Pharma Porter's Five Forces analysis you'll receive—no placeholders. It covers industry rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with concise, data-driven insights. The full document is fully formatted and available instantly after purchase.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Aurobindo Pharma faces intense industry rivalry driven by global generics competition and price pressure; buyer power is high among large purchasers while supplier power is moderate due to diversified API sources. Regulatory barriers limit new entrants but substitute therapies and margin compression remain tangible threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Aurobindo Pharma’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse API sources dilute leverage

Aurobindo sources APIs and key starting materials from multiple regions — India, China and Europe — diluting dependence on any single vendor as of 2024. This geographic diversification curbs supplier pricing power and reduces risk of wide-scale supply disruptions. Concentration remains for certain specialized intermediates and solvents, raising niche-input vulnerability. Strategic dual-sourcing and selective backward integration further buffer supplier influence.

Backward integration into APIs

By 2024 Aurobindo's backward integration into APIs reduces reliance on external suppliers for key molecules, strengthening cost control, quality oversight and supply assurance and thus shrinking supplier bargaining power. Capital intensity and regulatory compliance keep full integration impractical across all products, maintaining selective external sourcing. The current mix of internal and external APIs balances operational flexibility with resilience.

Regulatory-grade inputs constrain alternatives

Pharma-grade materials must meet stringent regulatory standards, narrowing the pool of qualified suppliers and increasing supplier leverage for critical APIs and excipients. Fewer compliant vendors can command better terms for select inputs, while approved-supplier lists and validation cycles—typically 6–18 months in 2024—raise switching costs for Aurobindo. Long-term quality agreements with volume commitments partially offset pricing pressure through predictable off-take and negotiated rebates.

Logistics and geopolitical exposure

Global supply chains for solvents, intermediates and packaging face freight volatility and geopolitical risks; container spot rates jumped about 30% after Red Sea disruptions in H1 2024, shifting leverage to suppliers with assured capacity. Aurobindo mitigates via regional stocking, multi-LOC approvals and selective nearshoring, while indexed supplier contracts pass volatility into higher input costs.

- Freight spike ~30% H1 2024

- Regional stocking reduces stockouts

- Multi-LOC approvals increase sourcing flexibility

- Indexed contracts share, but raise, input costs

Commoditized packaging vs specialized equipment

For Aurobindo Pharma, 2024 industry data shows over 75% of common packaging materials are commoditized, keeping supplier power low and price competition high. Conversely, specialized equipment, filters and single-use systems are concentrated: the top 4 OEMs account for roughly 65% of market share, creating supplier leverage. Lead times of 6–12 months plus lengthy validation increase switching costs, while lifecycle service agreements commonly embed an 8–12% premium.

Geographic diversification and API integration cut supplier power; freight +30% hikes switching costs

Aurobindo's geographic diversification and backward integration in APIs (2024) limit supplier leverage for commoditized inputs, though niche intermediates and validated suppliers retain pricing power. Supply shocks (container rates +30% H1 2024) and long validation/lead times (6–18 months; 6–12 months) raise switching costs. Packaging largely commoditized (>75%), while top-4 OEMs hold ~65%.

| Metric | Value (2024) |

|---|---|

| Packaging commoditized | >75% |

| Top-4 OEM share | ≈65% |

| Freight spike H1 | ~30% |

| Validation/lead times | 6–18 / 6–12 months |

What is included in the product

Tailored Porter's Five Forces for Aurobindo Pharma assessing rivalry, buyer/supplier power, threats from generics and biosimilars, substitute medicines, and entry barriers shaping its pricing, margins, and strategic risks.

Clear, one-sheet Porter's Five Forces for Aurobindo Pharma—instantly spot supplier, buyer, and regulatory pressures to guide strategic responses and ease executive decision-making.

Customers Bargaining Power

Large institutional buyers negotiate hard

Large institutional buyers — government tenders, GPOs and the three US wholesalers (McKesson, AmerisourceBergen, Cardinal) that together handle about 85% of US pharmaceutical distribution — aggregate demand and exert strong price and service-level pressure. Aurobindo must compete on price, reliability and product breadth, compressing margins in mature molecules. Preferential contracts raise volume visibility while increasing rebate and service commitments.

Product commoditization heightens price sensitivity

Generic drugs are largely interchangeable once deemed bioequivalent by regulators, and with generics accounting for about 90% of U.S. prescriptions by volume (FDA), buyers prioritize lowest total cost, boosting switching and negotiation power versus suppliers like Aurobindo.

Differentiation through superior dossier quality, fill rates and regulatory compliance can modestly defend share.

During supply shortages, temporary reliability premiums can reverse customer leverage.

Regulatory and quality performance as a lever

Buyers of Aurobindo prioritize consistent cGMP compliance and on-time delivery to avoid stockouts and contract penalties; strong audit histories with regulators raise trust and reduce pressure for price concessions. Any compliance lapse or inspection finding would immediately strengthen buyer bargaining power and could trigger delisting risk. Transparent quality metrics, public audit outcomes and manufacturing redundancy visibly lower perceived buyer risk and preserve negotiating leverage.

Portfolio breadth and bundling

Aurobindo’s portfolio of over 1,500 products across 150+ countries enables bundling across molecules and markets; bundles let it trade price for share gains and greater customer stickiness, tempering buyer power. Sophisticated buyers (large chains, governments) can decouple lines to maximize savings, pressuring margins. Cross-supply agreements and multi-year framework contracts help stabilize pricing and volume.

- Portfolio: 1,500+ products; 150+ markets

- Bargaining: bundles reduce churn but large buyers decouple

- Contracts: cross-supply & framework deals stabilize terms

International market mix

- US/EU pressure: high; ~60% revenue exposure

- FY2024 revenue: ~INR 36,000 crore

- Emerging markets: fragmented, higher pricing power

- Mitigants: currency diversification, local partnerships

Buyers squeeze margins; 1,500+ SKUs, bundling partly offsets, FY24 revenue ~INR 36,000cr

Large institutional buyers (US wholesalers, GPOs, governments) exert strong price/service pressure, compressing margins; generics' interchangeability (≈90% US Rx) increases switching power. Aurobindo's 1,500+ product portfolio and bundling plus cross-supply contracts partially mitigate leverage; compliance and on‑time delivery critically reduce buyer bargaining. FY2024 revenue ~INR 36,000 crore with ~60% from US/EU.

| Metric | Value |

|---|---|

| FY2024 revenue | ~INR 36,000 crore |

| US/EU share | ~60% |

| Products/Markets | 1,500+ / 150+ |

| US generic Rx | ~90% |

| Three US wholesalers | ~85% distribution |

What You See Is What You Get

Aurobindo Pharma Porter's Five Forces Analysis

This preview shows the exact Aurobindo Pharma Porter's Five Forces analysis you'll receive—no placeholders. It covers industry rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with concise, data-driven insights. The full document is fully formatted and available instantly after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Aurobindo Pharma faces intense industry rivalry driven by global generics competition and price pressure; buyer power is high among large purchasers while supplier power is moderate due to diversified API sources. Regulatory barriers limit new entrants but substitute therapies and margin compression remain tangible threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Aurobindo Pharma’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse API sources dilute leverage

Aurobindo sources APIs and key starting materials from multiple regions — India, China and Europe — diluting dependence on any single vendor as of 2024. This geographic diversification curbs supplier pricing power and reduces risk of wide-scale supply disruptions. Concentration remains for certain specialized intermediates and solvents, raising niche-input vulnerability. Strategic dual-sourcing and selective backward integration further buffer supplier influence.

Backward integration into APIs

By 2024 Aurobindo's backward integration into APIs reduces reliance on external suppliers for key molecules, strengthening cost control, quality oversight and supply assurance and thus shrinking supplier bargaining power. Capital intensity and regulatory compliance keep full integration impractical across all products, maintaining selective external sourcing. The current mix of internal and external APIs balances operational flexibility with resilience.

Regulatory-grade inputs constrain alternatives

Pharma-grade materials must meet stringent regulatory standards, narrowing the pool of qualified suppliers and increasing supplier leverage for critical APIs and excipients. Fewer compliant vendors can command better terms for select inputs, while approved-supplier lists and validation cycles—typically 6–18 months in 2024—raise switching costs for Aurobindo. Long-term quality agreements with volume commitments partially offset pricing pressure through predictable off-take and negotiated rebates.

Logistics and geopolitical exposure

Global supply chains for solvents, intermediates and packaging face freight volatility and geopolitical risks; container spot rates jumped about 30% after Red Sea disruptions in H1 2024, shifting leverage to suppliers with assured capacity. Aurobindo mitigates via regional stocking, multi-LOC approvals and selective nearshoring, while indexed supplier contracts pass volatility into higher input costs.

- Freight spike ~30% H1 2024

- Regional stocking reduces stockouts

- Multi-LOC approvals increase sourcing flexibility

- Indexed contracts share, but raise, input costs

Commoditized packaging vs specialized equipment

For Aurobindo Pharma, 2024 industry data shows over 75% of common packaging materials are commoditized, keeping supplier power low and price competition high. Conversely, specialized equipment, filters and single-use systems are concentrated: the top 4 OEMs account for roughly 65% of market share, creating supplier leverage. Lead times of 6–12 months plus lengthy validation increase switching costs, while lifecycle service agreements commonly embed an 8–12% premium.

Geographic diversification and API integration cut supplier power; freight +30% hikes switching costs

Aurobindo's geographic diversification and backward integration in APIs (2024) limit supplier leverage for commoditized inputs, though niche intermediates and validated suppliers retain pricing power. Supply shocks (container rates +30% H1 2024) and long validation/lead times (6–18 months; 6–12 months) raise switching costs. Packaging largely commoditized (>75%), while top-4 OEMs hold ~65%.

| Metric | Value (2024) |

|---|---|

| Packaging commoditized | >75% |

| Top-4 OEM share | ≈65% |

| Freight spike H1 | ~30% |

| Validation/lead times | 6–18 / 6–12 months |

What is included in the product

Tailored Porter's Five Forces for Aurobindo Pharma assessing rivalry, buyer/supplier power, threats from generics and biosimilars, substitute medicines, and entry barriers shaping its pricing, margins, and strategic risks.

Clear, one-sheet Porter's Five Forces for Aurobindo Pharma—instantly spot supplier, buyer, and regulatory pressures to guide strategic responses and ease executive decision-making.

Customers Bargaining Power

Large institutional buyers negotiate hard

Large institutional buyers — government tenders, GPOs and the three US wholesalers (McKesson, AmerisourceBergen, Cardinal) that together handle about 85% of US pharmaceutical distribution — aggregate demand and exert strong price and service-level pressure. Aurobindo must compete on price, reliability and product breadth, compressing margins in mature molecules. Preferential contracts raise volume visibility while increasing rebate and service commitments.

Product commoditization heightens price sensitivity

Generic drugs are largely interchangeable once deemed bioequivalent by regulators, and with generics accounting for about 90% of U.S. prescriptions by volume (FDA), buyers prioritize lowest total cost, boosting switching and negotiation power versus suppliers like Aurobindo.

Differentiation through superior dossier quality, fill rates and regulatory compliance can modestly defend share.

During supply shortages, temporary reliability premiums can reverse customer leverage.

Regulatory and quality performance as a lever

Buyers of Aurobindo prioritize consistent cGMP compliance and on-time delivery to avoid stockouts and contract penalties; strong audit histories with regulators raise trust and reduce pressure for price concessions. Any compliance lapse or inspection finding would immediately strengthen buyer bargaining power and could trigger delisting risk. Transparent quality metrics, public audit outcomes and manufacturing redundancy visibly lower perceived buyer risk and preserve negotiating leverage.

Portfolio breadth and bundling

Aurobindo’s portfolio of over 1,500 products across 150+ countries enables bundling across molecules and markets; bundles let it trade price for share gains and greater customer stickiness, tempering buyer power. Sophisticated buyers (large chains, governments) can decouple lines to maximize savings, pressuring margins. Cross-supply agreements and multi-year framework contracts help stabilize pricing and volume.

- Portfolio: 1,500+ products; 150+ markets

- Bargaining: bundles reduce churn but large buyers decouple

- Contracts: cross-supply & framework deals stabilize terms

International market mix

- US/EU pressure: high; ~60% revenue exposure

- FY2024 revenue: ~INR 36,000 crore

- Emerging markets: fragmented, higher pricing power

- Mitigants: currency diversification, local partnerships

Buyers squeeze margins; 1,500+ SKUs, bundling partly offsets, FY24 revenue ~INR 36,000cr

Large institutional buyers (US wholesalers, GPOs, governments) exert strong price/service pressure, compressing margins; generics' interchangeability (≈90% US Rx) increases switching power. Aurobindo's 1,500+ product portfolio and bundling plus cross-supply contracts partially mitigate leverage; compliance and on‑time delivery critically reduce buyer bargaining. FY2024 revenue ~INR 36,000 crore with ~60% from US/EU.

| Metric | Value |

|---|---|

| FY2024 revenue | ~INR 36,000 crore |

| US/EU share | ~60% |

| Products/Markets | 1,500+ / 150+ |

| US generic Rx | ~90% |

| Three US wholesalers | ~85% distribution |

What You See Is What You Get

Aurobindo Pharma Porter's Five Forces Analysis

This preview shows the exact Aurobindo Pharma Porter's Five Forces analysis you'll receive—no placeholders. It covers industry rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with concise, data-driven insights. The full document is fully formatted and available instantly after purchase.