Autlan Porter's Five Forces Analysis

From Overview to Strategy Blueprint

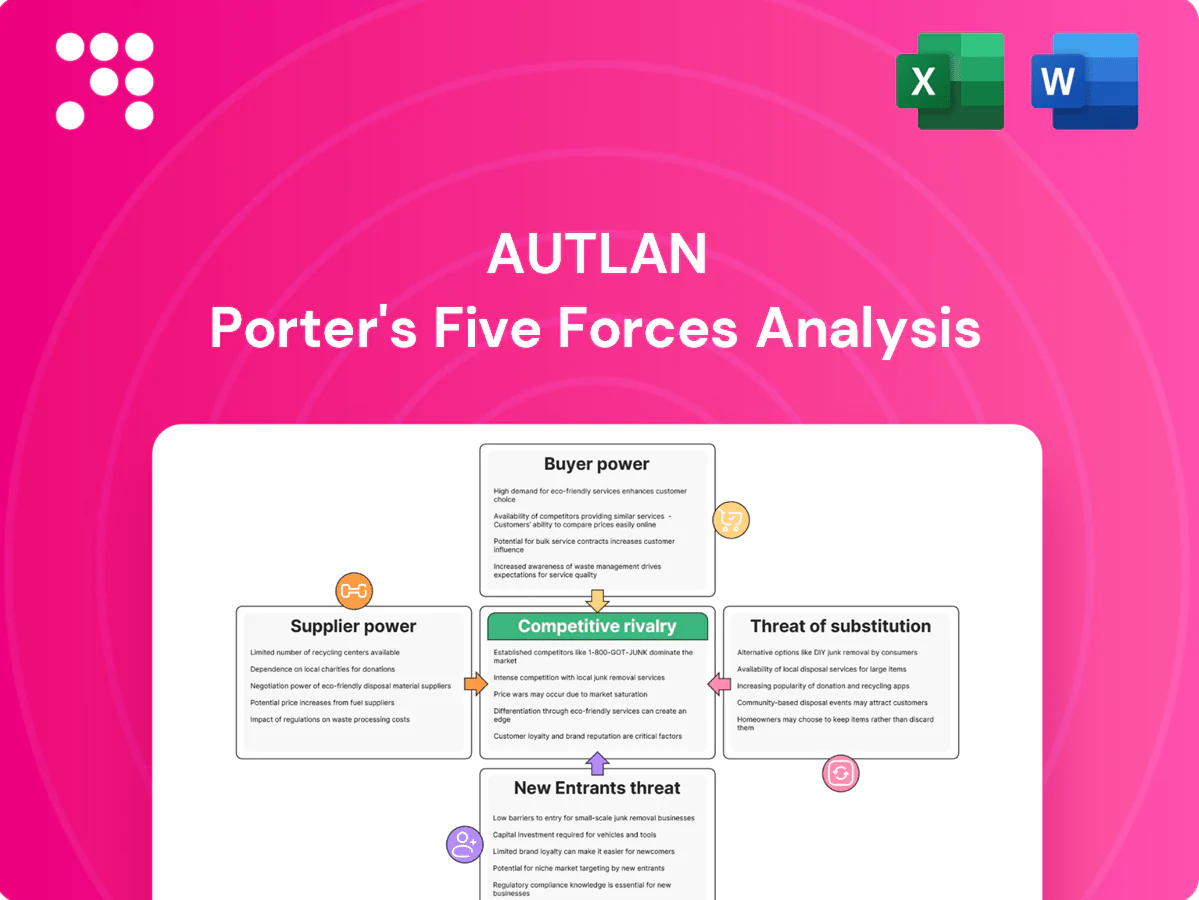

Autlan faces concentrated supplier power and cyclical demand that compress margins, while moderate buyer leverage and substitution risks shape pricing flexibility. Competitive rivalry is intense due to capacity expansion and commodity pressure. This snapshot highlights key strategic tensions—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated mining inputs and OEM dependence

Autlán depends on a narrow set of global OEMs for specialized mining equipment, explosives and reagents, giving suppliers leverage over pricing and delivery. Proprietary parts and long lead times raise switching costs and increase downtime risk for operations. Autlán’s scale and multi-year procurement contracts provide negotiating power to secure better pricing. Localization and dual-sourcing strategies can further reduce supplier concentration risk.

Energy self-sufficiency via hydro reduces exposure

Autlán's ownership of hydroelectric assets lowers dependence on external providers, stabilizing energy costs and weakening utility suppliers' bargaining power; Mexico's hydro supplied about 12% of electricity in 2024, providing a tangible domestic hedge. This vertical integration cushions the company from grid price spikes and enhances operational continuity during volatility. Any hydro seasonality is managed through grid interconnection and supplemental contracts to ensure steady supply.

Logistics and transport bottlenecks

Bulk ores and ferroalloys depend on reliable trucking, rail, and port services, and limited capacity—notably concentrated rail operations by two major carriers in Mexico—can elevate carrier bargaining power. Take-or-pay rail contracts and scarce port slots increase logistics costs for Autlan. Long-term logistics contracts and route diversification mitigate concentration risk. Proximity to Mexican steel customers reduces reliance on international shippers and their leverage.

Contractor and skilled labor constraints

Mining relies heavily on specialized contractors and scarce skilled labor, concentrating supplier power where regional pools are tight and mobilization costs are high.

Wage inflation and stricter safety compliance have heightened contractor leverage, increasing operating cost volatility for miners like Autlan.

Investing in training pipelines and community engagement expands the talent pool and reduces reliance on external suppliers, while multi-year contractor frameworks help cap rate volatility.

- Contractor concentration

- Wage and compliance pressure

- Training expands supply

- Multi-year contracts reduce volatility

Regulatory and permitting services

Regulatory and permitting vendors (environmental consulting, permitting, remediation) hold notable leverage over Autlán because 2024 global environmental consulting market size reached about $36 billion, and compliance is critical to avoid fines and shutdowns; project timelines often hinge on their technical approvals, increasing supplier dependence. Building in-house environmental teams can materially reduce this reliance and mitigate schedule risk.

- Early engagement with vendors

- Competitive tenders to control fees

- Develop internal environmental capacity

Supplier concentration raises costs; hydropower ≈12% reduces risk

Autlán faces concentrated supplier leverage for specialized equipment, explosives and reagents, with long lead times raising switching costs. Hydropower ownership (≈12% of Mexico's 2024 mix) reduces energy supplier power. Logistics tied to two major rail carriers and port capacity elevate transport bargaining power. Investing in dual-sourcing, training and multi-year contracts mitigates supplier risk.

| Metric | Value |

|---|---|

| Hydro share (2024) | ≈12% |

| Env consulting market (2024) | $36bn |

| Major rail carriers | 2 |

| Typical procurement contracts | 3–5 yrs |

What is included in the product

Uncovers the five competitive forces shaping Autlán’s ferroalloy market position—analyzing supplier power, buyer influence, entry barriers, substitute threats, and industry rivalry to reveal pricing, profitability, and disruption risks tailored to Autlán.

A clear, one-sheet summary of Autlán's Porter's Five Forces for quick decision-making; customizable pressure levels and an instant spider chart make strategic pressure easy to update, visualize, and drop into pitch decks or reports.

Customers Bargaining Power

Concentrated steelmaker customer base

Ferroalloys are sold to a concentrated set of steelmakers, giving large mills outsized leverage; China accounted for about 54% of global crude steel production in 2024 (World Steel Association), concentrating buying power. Major mill groups routinely negotiate aggressive pricing and strict quality clauses, while long-term offtake deals trade volume certainty for price concessions. Regional dependence heightens single-customer risk if Autlan lacks diversification.

Commodity pricing and index linkage

In 2024 Autlán’s customer leverage is heightened because contract prices largely track global manganese ore and alloy indices, constraining its pricing discretion. Buyers increasingly demand index-linked formulas with monthly or quarterly resets and tighter payment terms. Quality, supply reliability and delivery windows drive premium realizations. Strategic hedging and higher-value grades help preserve margins amidst index volatility.

Specification and qualification hurdles

Steelmakers demand stringent chemistry and batch-to-batch consistency, with supplier qualification cycles typically taking 3–12 months, which raises switching costs once Autlán is approved and reduces buyer willingness to change solely for price. Maintaining high on-time, in-spec performance (critical as global crude steel output reached about 1.86 billion tonnes in 2024) strengthens Autlán’s bargaining position. Deep technical support and co-development of alloys further lock in customers and increase stickiness.

Alternative sourcing and imports

- Sources: Africa/Asia/SA exporters maintain global presence in 2024

- Constraints: freight, tariffs, lead times limit immediate switching

- Advantage: Autlán proximity improves responsiveness and lowers inland logistics

- Risk: currency moves in 2024 can alter landed-cost competitiveness

Energy sales diversify revenue

Energy sales diversify revenue beyond steel, expanding Autlan's customer base and diluting ferroalloy buyers' bargaining power across the company; long-term power purchase agreements provide predictable cash flows and reduce price sensitivity in negotiations. Grid sales act as a hedge against cyclical steel downturns, smoothing revenue volatility and strengthening Autlan's negotiating position.

- Diversification reduces single-industry dependency

- Long-term PPAs stabilize cash flows

- Grid sales hedge steel cyclicality

China-led steel demand gives ferroalloy buyers strong pricing leverage

Ferroalloy buyers (concentrated steelmakers; China ~54% of crude steel in 2024; global output ~1.86bn t) wield strong price leverage via index-linked contracts and tight terms. Supplier qualification and technical support raise switching costs, but seaborne supply, freight and FX shifts sustain buyer negotiating power.

| Metric | 2024 | Implication |

|---|---|---|

| China share | 54% | High buyer concentration |

| Global steel | 1.86bn t | Large demand base |

Same Document Delivered

Autlan Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Autlan you'll receive after purchase—fully formatted and ready to use. It evaluates supplier and buyer power, threat of new entrants, substitutes, and competitive rivalry, and includes actionable insights and supporting data. No placeholders or mockups—this is the final deliverable available instantly after payment.

From Overview to Strategy Blueprint

Autlan faces concentrated supplier power and cyclical demand that compress margins, while moderate buyer leverage and substitution risks shape pricing flexibility. Competitive rivalry is intense due to capacity expansion and commodity pressure. This snapshot highlights key strategic tensions—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated mining inputs and OEM dependence

Autlán depends on a narrow set of global OEMs for specialized mining equipment, explosives and reagents, giving suppliers leverage over pricing and delivery. Proprietary parts and long lead times raise switching costs and increase downtime risk for operations. Autlán’s scale and multi-year procurement contracts provide negotiating power to secure better pricing. Localization and dual-sourcing strategies can further reduce supplier concentration risk.

Energy self-sufficiency via hydro reduces exposure

Autlán's ownership of hydroelectric assets lowers dependence on external providers, stabilizing energy costs and weakening utility suppliers' bargaining power; Mexico's hydro supplied about 12% of electricity in 2024, providing a tangible domestic hedge. This vertical integration cushions the company from grid price spikes and enhances operational continuity during volatility. Any hydro seasonality is managed through grid interconnection and supplemental contracts to ensure steady supply.

Logistics and transport bottlenecks

Bulk ores and ferroalloys depend on reliable trucking, rail, and port services, and limited capacity—notably concentrated rail operations by two major carriers in Mexico—can elevate carrier bargaining power. Take-or-pay rail contracts and scarce port slots increase logistics costs for Autlan. Long-term logistics contracts and route diversification mitigate concentration risk. Proximity to Mexican steel customers reduces reliance on international shippers and their leverage.

Contractor and skilled labor constraints

Mining relies heavily on specialized contractors and scarce skilled labor, concentrating supplier power where regional pools are tight and mobilization costs are high.

Wage inflation and stricter safety compliance have heightened contractor leverage, increasing operating cost volatility for miners like Autlan.

Investing in training pipelines and community engagement expands the talent pool and reduces reliance on external suppliers, while multi-year contractor frameworks help cap rate volatility.

- Contractor concentration

- Wage and compliance pressure

- Training expands supply

- Multi-year contracts reduce volatility

Regulatory and permitting services

Regulatory and permitting vendors (environmental consulting, permitting, remediation) hold notable leverage over Autlán because 2024 global environmental consulting market size reached about $36 billion, and compliance is critical to avoid fines and shutdowns; project timelines often hinge on their technical approvals, increasing supplier dependence. Building in-house environmental teams can materially reduce this reliance and mitigate schedule risk.

- Early engagement with vendors

- Competitive tenders to control fees

- Develop internal environmental capacity

Supplier concentration raises costs; hydropower ≈12% reduces risk

Autlán faces concentrated supplier leverage for specialized equipment, explosives and reagents, with long lead times raising switching costs. Hydropower ownership (≈12% of Mexico's 2024 mix) reduces energy supplier power. Logistics tied to two major rail carriers and port capacity elevate transport bargaining power. Investing in dual-sourcing, training and multi-year contracts mitigates supplier risk.

| Metric | Value |

|---|---|

| Hydro share (2024) | ≈12% |

| Env consulting market (2024) | $36bn |

| Major rail carriers | 2 |

| Typical procurement contracts | 3–5 yrs |

What is included in the product

Uncovers the five competitive forces shaping Autlán’s ferroalloy market position—analyzing supplier power, buyer influence, entry barriers, substitute threats, and industry rivalry to reveal pricing, profitability, and disruption risks tailored to Autlán.

A clear, one-sheet summary of Autlán's Porter's Five Forces for quick decision-making; customizable pressure levels and an instant spider chart make strategic pressure easy to update, visualize, and drop into pitch decks or reports.

Customers Bargaining Power

Concentrated steelmaker customer base

Ferroalloys are sold to a concentrated set of steelmakers, giving large mills outsized leverage; China accounted for about 54% of global crude steel production in 2024 (World Steel Association), concentrating buying power. Major mill groups routinely negotiate aggressive pricing and strict quality clauses, while long-term offtake deals trade volume certainty for price concessions. Regional dependence heightens single-customer risk if Autlan lacks diversification.

Commodity pricing and index linkage

In 2024 Autlán’s customer leverage is heightened because contract prices largely track global manganese ore and alloy indices, constraining its pricing discretion. Buyers increasingly demand index-linked formulas with monthly or quarterly resets and tighter payment terms. Quality, supply reliability and delivery windows drive premium realizations. Strategic hedging and higher-value grades help preserve margins amidst index volatility.

Specification and qualification hurdles

Steelmakers demand stringent chemistry and batch-to-batch consistency, with supplier qualification cycles typically taking 3–12 months, which raises switching costs once Autlán is approved and reduces buyer willingness to change solely for price. Maintaining high on-time, in-spec performance (critical as global crude steel output reached about 1.86 billion tonnes in 2024) strengthens Autlán’s bargaining position. Deep technical support and co-development of alloys further lock in customers and increase stickiness.

Alternative sourcing and imports

- Sources: Africa/Asia/SA exporters maintain global presence in 2024

- Constraints: freight, tariffs, lead times limit immediate switching

- Advantage: Autlán proximity improves responsiveness and lowers inland logistics

- Risk: currency moves in 2024 can alter landed-cost competitiveness

Energy sales diversify revenue

Energy sales diversify revenue beyond steel, expanding Autlan's customer base and diluting ferroalloy buyers' bargaining power across the company; long-term power purchase agreements provide predictable cash flows and reduce price sensitivity in negotiations. Grid sales act as a hedge against cyclical steel downturns, smoothing revenue volatility and strengthening Autlan's negotiating position.

- Diversification reduces single-industry dependency

- Long-term PPAs stabilize cash flows

- Grid sales hedge steel cyclicality

China-led steel demand gives ferroalloy buyers strong pricing leverage

Ferroalloy buyers (concentrated steelmakers; China ~54% of crude steel in 2024; global output ~1.86bn t) wield strong price leverage via index-linked contracts and tight terms. Supplier qualification and technical support raise switching costs, but seaborne supply, freight and FX shifts sustain buyer negotiating power.

| Metric | 2024 | Implication |

|---|---|---|

| China share | 54% | High buyer concentration |

| Global steel | 1.86bn t | Large demand base |

Same Document Delivered

Autlan Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Autlan you'll receive after purchase—fully formatted and ready to use. It evaluates supplier and buyer power, threat of new entrants, substitutes, and competitive rivalry, and includes actionable insights and supporting data. No placeholders or mockups—this is the final deliverable available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Autlan faces concentrated supplier power and cyclical demand that compress margins, while moderate buyer leverage and substitution risks shape pricing flexibility. Competitive rivalry is intense due to capacity expansion and commodity pressure. This snapshot highlights key strategic tensions—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated mining inputs and OEM dependence

Autlán depends on a narrow set of global OEMs for specialized mining equipment, explosives and reagents, giving suppliers leverage over pricing and delivery. Proprietary parts and long lead times raise switching costs and increase downtime risk for operations. Autlán’s scale and multi-year procurement contracts provide negotiating power to secure better pricing. Localization and dual-sourcing strategies can further reduce supplier concentration risk.

Energy self-sufficiency via hydro reduces exposure

Autlán's ownership of hydroelectric assets lowers dependence on external providers, stabilizing energy costs and weakening utility suppliers' bargaining power; Mexico's hydro supplied about 12% of electricity in 2024, providing a tangible domestic hedge. This vertical integration cushions the company from grid price spikes and enhances operational continuity during volatility. Any hydro seasonality is managed through grid interconnection and supplemental contracts to ensure steady supply.

Logistics and transport bottlenecks

Bulk ores and ferroalloys depend on reliable trucking, rail, and port services, and limited capacity—notably concentrated rail operations by two major carriers in Mexico—can elevate carrier bargaining power. Take-or-pay rail contracts and scarce port slots increase logistics costs for Autlan. Long-term logistics contracts and route diversification mitigate concentration risk. Proximity to Mexican steel customers reduces reliance on international shippers and their leverage.

Contractor and skilled labor constraints

Mining relies heavily on specialized contractors and scarce skilled labor, concentrating supplier power where regional pools are tight and mobilization costs are high.

Wage inflation and stricter safety compliance have heightened contractor leverage, increasing operating cost volatility for miners like Autlan.

Investing in training pipelines and community engagement expands the talent pool and reduces reliance on external suppliers, while multi-year contractor frameworks help cap rate volatility.

- Contractor concentration

- Wage and compliance pressure

- Training expands supply

- Multi-year contracts reduce volatility

Regulatory and permitting services

Regulatory and permitting vendors (environmental consulting, permitting, remediation) hold notable leverage over Autlán because 2024 global environmental consulting market size reached about $36 billion, and compliance is critical to avoid fines and shutdowns; project timelines often hinge on their technical approvals, increasing supplier dependence. Building in-house environmental teams can materially reduce this reliance and mitigate schedule risk.

- Early engagement with vendors

- Competitive tenders to control fees

- Develop internal environmental capacity

Supplier concentration raises costs; hydropower ≈12% reduces risk

Autlán faces concentrated supplier leverage for specialized equipment, explosives and reagents, with long lead times raising switching costs. Hydropower ownership (≈12% of Mexico's 2024 mix) reduces energy supplier power. Logistics tied to two major rail carriers and port capacity elevate transport bargaining power. Investing in dual-sourcing, training and multi-year contracts mitigates supplier risk.

| Metric | Value |

|---|---|

| Hydro share (2024) | ≈12% |

| Env consulting market (2024) | $36bn |

| Major rail carriers | 2 |

| Typical procurement contracts | 3–5 yrs |

What is included in the product

Uncovers the five competitive forces shaping Autlán’s ferroalloy market position—analyzing supplier power, buyer influence, entry barriers, substitute threats, and industry rivalry to reveal pricing, profitability, and disruption risks tailored to Autlán.

A clear, one-sheet summary of Autlán's Porter's Five Forces for quick decision-making; customizable pressure levels and an instant spider chart make strategic pressure easy to update, visualize, and drop into pitch decks or reports.

Customers Bargaining Power

Concentrated steelmaker customer base

Ferroalloys are sold to a concentrated set of steelmakers, giving large mills outsized leverage; China accounted for about 54% of global crude steel production in 2024 (World Steel Association), concentrating buying power. Major mill groups routinely negotiate aggressive pricing and strict quality clauses, while long-term offtake deals trade volume certainty for price concessions. Regional dependence heightens single-customer risk if Autlan lacks diversification.

Commodity pricing and index linkage

In 2024 Autlán’s customer leverage is heightened because contract prices largely track global manganese ore and alloy indices, constraining its pricing discretion. Buyers increasingly demand index-linked formulas with monthly or quarterly resets and tighter payment terms. Quality, supply reliability and delivery windows drive premium realizations. Strategic hedging and higher-value grades help preserve margins amidst index volatility.

Specification and qualification hurdles

Steelmakers demand stringent chemistry and batch-to-batch consistency, with supplier qualification cycles typically taking 3–12 months, which raises switching costs once Autlán is approved and reduces buyer willingness to change solely for price. Maintaining high on-time, in-spec performance (critical as global crude steel output reached about 1.86 billion tonnes in 2024) strengthens Autlán’s bargaining position. Deep technical support and co-development of alloys further lock in customers and increase stickiness.

Alternative sourcing and imports

- Sources: Africa/Asia/SA exporters maintain global presence in 2024

- Constraints: freight, tariffs, lead times limit immediate switching

- Advantage: Autlán proximity improves responsiveness and lowers inland logistics

- Risk: currency moves in 2024 can alter landed-cost competitiveness

Energy sales diversify revenue

Energy sales diversify revenue beyond steel, expanding Autlan's customer base and diluting ferroalloy buyers' bargaining power across the company; long-term power purchase agreements provide predictable cash flows and reduce price sensitivity in negotiations. Grid sales act as a hedge against cyclical steel downturns, smoothing revenue volatility and strengthening Autlan's negotiating position.

- Diversification reduces single-industry dependency

- Long-term PPAs stabilize cash flows

- Grid sales hedge steel cyclicality

China-led steel demand gives ferroalloy buyers strong pricing leverage

Ferroalloy buyers (concentrated steelmakers; China ~54% of crude steel in 2024; global output ~1.86bn t) wield strong price leverage via index-linked contracts and tight terms. Supplier qualification and technical support raise switching costs, but seaborne supply, freight and FX shifts sustain buyer negotiating power.

| Metric | 2024 | Implication |

|---|---|---|

| China share | 54% | High buyer concentration |

| Global steel | 1.86bn t | Large demand base |

Same Document Delivered

Autlan Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Autlan you'll receive after purchase—fully formatted and ready to use. It evaluates supplier and buyer power, threat of new entrants, substitutes, and competitive rivalry, and includes actionable insights and supporting data. No placeholders or mockups—this is the final deliverable available instantly after payment.