Autobio Diagnostics Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Autobio Diagnostics faces concentrated supplier power, evolving buyer demands, and rising substitute technologies that pressure margins and growth—this brief snapshot highlights key dynamics and risks. Ready for deeper clarity? Unlock the full Porter's Five Forces Analysis to view force-by-force ratings, visuals, and actionable strategy insights tailored to Autobio Diagnostics.

Suppliers Bargaining Power

Critical biologics concentration

High-quality antibodies, antigens and enzymes are concentrated among a few vetted bioreagent suppliers, so qualification and lot-to-lot validation raise switching costs for Autobio; scarcity in specialty biomarkers gives niche vendors pricing leverage. Long-term contracts and second-sourcing reduce but do not eliminate dependency, keeping supplier bargaining power elevated into 2024.

Instrument components and OEMs

Key subsystems (optics, pumps, robotics, sensors) are sourced from specialized OEMs, creating supplier concentration that firms report as causing 6–9 month lead times in 2024 procurement cycles. Performance specs and regulatory files lock designs to specific vendors, so redesigns to swap suppliers typically exceed $1M in engineering and validation costs and add months to approval. Volume commitments can temper pricing power, often delivering 10–20% price concessions on high-volume contracts.

Disposable plastics and consumables

Tips, cuvettes, cartridges and plates are largely commoditized with broad supplier pools, reducing individual bargaining power for Autobio, yet precision tolerances and cleanliness standards restrict viable vendors and raise qualification barriers. Tooling and molds create moderate switching friction due to upfront CAPEX and 4–12 week lead times. Strategic bulk contracts can lower unit costs by up to 20–25% while preserving quality.

Regulatory-grade quality systems

Suppliers must meet ISO 13485:2016, GMP and FDA QSR (21 CFR 820) expectations, concentrating the qualified pool and raising entry barriers. Any supplier change triggers re-validation, design history file updates and possible regulatory notifications, lengthening approval timelines and strengthening supplier bargaining. Strategic quality audits and dual qualification materially reduce disruption risk.

- Regulatory standards: ISO 13485:2016, GMP, 21 CFR 820

- Change impact: re-validation + regulatory notifications

- Mitigation: quality audits, dual qualification

Geopolitical and FX exposure

Imported reagents and components expose Autobio to currency swings and export controls, which can lengthen lead times and increase buffer-stock needs, boosting supplier leverage. Disruptions from trade restrictions have tightened delivery schedules and elevated working capital requirements. Localization programs and vendor diversification, together with FX hedging, reduce but do not eliminate this supplier power.

- Imported inputs increase supplier leverage

- Export controls raise lead times and buffers

- Localization dilutes dependence over time

- Hedging/diversification partially offset volatility

2024: Supplier power high - 6-9 month lead times, >$1M switching costs, 10-25% bulk savings

Supplier power is high in 2024: key bioreagents concentrated (few vetted suppliers) and OEM subsystems cause 6–9 month lead times; redesign/validation to switch suppliers often exceeds $1M. Commoditized consumables yield 10–25% bulk savings, but ISO 13485/21 CFR 820 compliance concentrates vendors. FX, export controls increase buffers and working capital.

| Metric | 2024 Value |

|---|---|

| Lead time | 6–9 months |

| Switching cost | >$1M |

| Bulk discount | 10–25% |

| Supplier concentration | High |

What is included in the product

Tailored for Autobio Diagnostics, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer leverage, and threats from substitutes and new entrants, with strategic commentary on pricing power and market entry barriers. Use in investor materials, strategy decks, or business plans to identify disruptive forces and protect market share.

A concise, one-sheet Porter's Five Forces for Autobio Diagnostics—instantly map supplier, buyer, competitor and regulatory pressures to relieve strategic uncertainty. Customize force intensities, swap in your data, and export a clean radar chart for decks or boardroom decisions.

Customers Bargaining Power

Hospital and reference lab scale

Large hospitals, GPOs and public procurement channels concentrate purchasing, with centralized tenders in China and other markets driving reagent price declines commonly in the 20–60% range in 2023–24. Buyers leverage aggregated volume for steep discounts and service upgrades, while multi-year reagent rental contracts further intensify negotiations and margin pressure on Autobio Diagnostics.

Reagent lock-in to installed base

Analyzer-specific reagents create strong lock-in post-installation, making reagent sales a steady revenue stream in the IVD reagents market, estimated at about $54 billion in 2024. Buyers balance analyzer menu breadth and uptime against price concessions, so suppliers with broader menus command premium pricing. Contract expiries prompt aggressive re-bids as labs seek cost savings, yet superior service quality and uptime often override lowest-price bids.

Outcome and reimbursement pressure

Payers demand demonstrable cost-effectiveness as diagnostics face outcome and reimbursement pressure, with the global in vitro diagnostics market valued at about $90 billion in 2023. Labs increasingly prioritize assays with clear clinical utility and guideline support, driving purchasing toward tests with demonstrated impact on care pathways. Pharmacoeconomic evidence now shapes formulary-like lab formularies, and rising value-based procurement programs are strengthening buyer leverage.

Quality, accreditation, and data integration

Accreditation bodies such as CAP, ISO 15189 and CLIA mandate consistent performance and LIS connectivity, so buyers demand vendor verification data, QC tools and middleware integration. Vendors therefore compete on analytical sensitivity, traceability and interoperability; robust clinical and validation evidence in 2024 reduces price pressure by shifting decisions toward value over cost.

- Accreditation: CAP/ISO 15189/CLIA required

- Buyer demands: verification data, QC, middleware

- Vendor edges: sensitivity, traceability, interoperability

- Evidence: stronger data lowers price sensitivity

Menu breadth and TAT expectations

Comprehensive assay menus and sub-60-minute TAT for STAT testing drive buyer choice; vendors offering immunoassay, microbiology, chemistry and molecular on unified workflows win pricing and adoption advantages. Where gaps exist, buyers keep multi-vendor setups to preserve leverage and negotiate better service-levels. 2024 diagnostic M&A activity lifted consolidation, temporarily shifting bargaining power toward large integrated suppliers.

- Unified-workflow preference: ~62% (2024 survey)

- STAT TAT expectation: <60 minutes

- Multi-vendor retention: preserves supplier leverage

- 2024 M&A: increased consolidation, rebalance power

Buyers force reagent cuts 20–60%; analyzer lock-in shields $54B

Buyers (hospitals, GPOs, public tenders) consolidated purchases, driving reagent price declines of 20–60% in 2023–24 and intense discounting. Analyzer lock-in sustains reagent revenue (IVD reagents ≈ $54B in 2024) but buyers push for value, evidence and interoperability as reimbursement ties to outcomes (IVD market ≈ $90B in 2023). Unified-workflow preference (~62% in 2024) and M&A consolidation shift leverage intermittently.

| Metric | Value |

|---|---|

| IVD market 2023 | $90B |

| Reagents 2024 | $54B |

| Price declines 2023–24 | 20–60% |

| Unified-workflow preference 2024 | ~62% |

Preview the Actual Deliverable

Autobio Diagnostics Porter's Five Forces Analysis

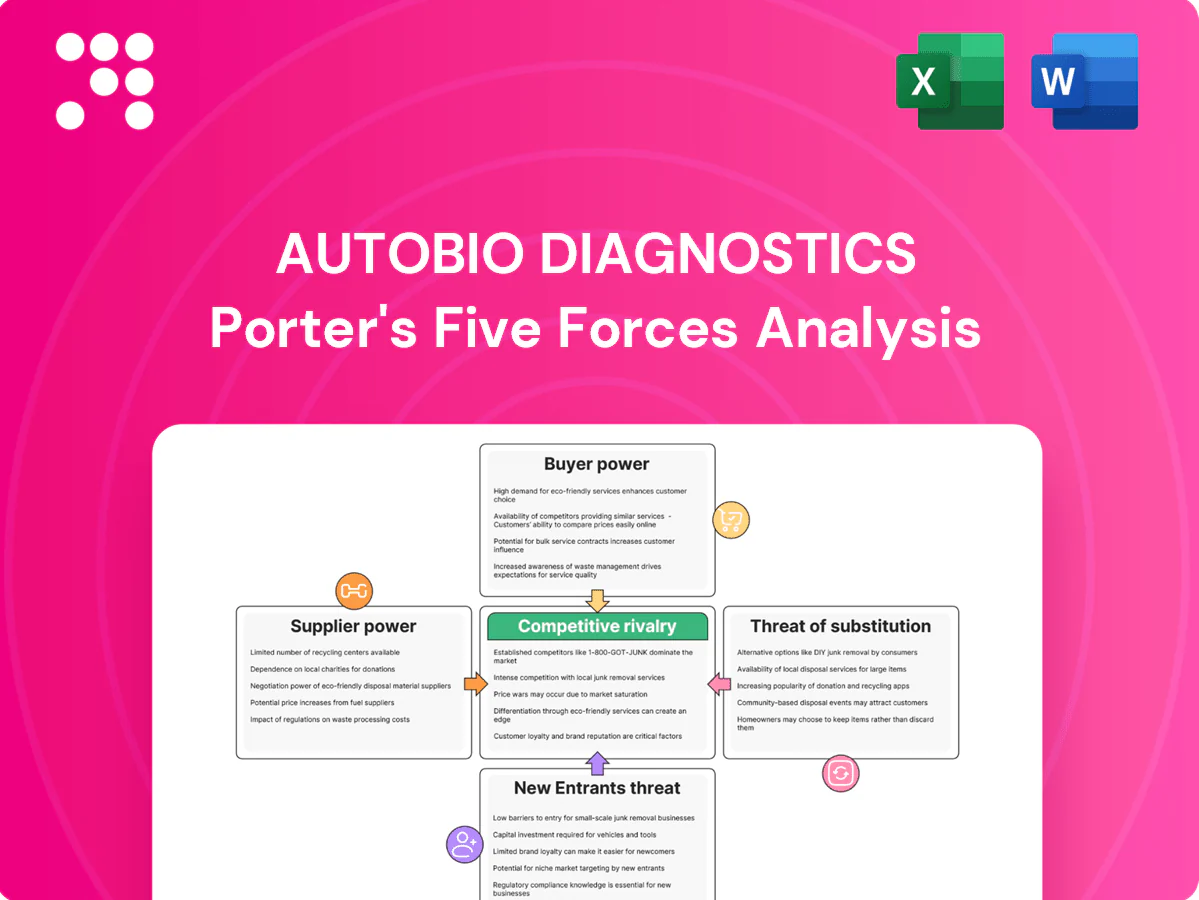

This preview shows the exact Porter's Five Forces analysis for Autobio Diagnostics you'll receive—no placeholders or samples—fully formatted and ready for use. It contains a thorough assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers tailored to Autobio's market position. Purchase grants instant access to this identical document for download and application.

A Must-Have Tool for Decision-Makers

Autobio Diagnostics faces concentrated supplier power, evolving buyer demands, and rising substitute technologies that pressure margins and growth—this brief snapshot highlights key dynamics and risks. Ready for deeper clarity? Unlock the full Porter's Five Forces Analysis to view force-by-force ratings, visuals, and actionable strategy insights tailored to Autobio Diagnostics.

Suppliers Bargaining Power

Critical biologics concentration

High-quality antibodies, antigens and enzymes are concentrated among a few vetted bioreagent suppliers, so qualification and lot-to-lot validation raise switching costs for Autobio; scarcity in specialty biomarkers gives niche vendors pricing leverage. Long-term contracts and second-sourcing reduce but do not eliminate dependency, keeping supplier bargaining power elevated into 2024.

Instrument components and OEMs

Key subsystems (optics, pumps, robotics, sensors) are sourced from specialized OEMs, creating supplier concentration that firms report as causing 6–9 month lead times in 2024 procurement cycles. Performance specs and regulatory files lock designs to specific vendors, so redesigns to swap suppliers typically exceed $1M in engineering and validation costs and add months to approval. Volume commitments can temper pricing power, often delivering 10–20% price concessions on high-volume contracts.

Disposable plastics and consumables

Tips, cuvettes, cartridges and plates are largely commoditized with broad supplier pools, reducing individual bargaining power for Autobio, yet precision tolerances and cleanliness standards restrict viable vendors and raise qualification barriers. Tooling and molds create moderate switching friction due to upfront CAPEX and 4–12 week lead times. Strategic bulk contracts can lower unit costs by up to 20–25% while preserving quality.

Regulatory-grade quality systems

Suppliers must meet ISO 13485:2016, GMP and FDA QSR (21 CFR 820) expectations, concentrating the qualified pool and raising entry barriers. Any supplier change triggers re-validation, design history file updates and possible regulatory notifications, lengthening approval timelines and strengthening supplier bargaining. Strategic quality audits and dual qualification materially reduce disruption risk.

- Regulatory standards: ISO 13485:2016, GMP, 21 CFR 820

- Change impact: re-validation + regulatory notifications

- Mitigation: quality audits, dual qualification

Geopolitical and FX exposure

Imported reagents and components expose Autobio to currency swings and export controls, which can lengthen lead times and increase buffer-stock needs, boosting supplier leverage. Disruptions from trade restrictions have tightened delivery schedules and elevated working capital requirements. Localization programs and vendor diversification, together with FX hedging, reduce but do not eliminate this supplier power.

- Imported inputs increase supplier leverage

- Export controls raise lead times and buffers

- Localization dilutes dependence over time

- Hedging/diversification partially offset volatility

2024: Supplier power high - 6-9 month lead times, >$1M switching costs, 10-25% bulk savings

Supplier power is high in 2024: key bioreagents concentrated (few vetted suppliers) and OEM subsystems cause 6–9 month lead times; redesign/validation to switch suppliers often exceeds $1M. Commoditized consumables yield 10–25% bulk savings, but ISO 13485/21 CFR 820 compliance concentrates vendors. FX, export controls increase buffers and working capital.

| Metric | 2024 Value |

|---|---|

| Lead time | 6–9 months |

| Switching cost | >$1M |

| Bulk discount | 10–25% |

| Supplier concentration | High |

What is included in the product

Tailored for Autobio Diagnostics, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer leverage, and threats from substitutes and new entrants, with strategic commentary on pricing power and market entry barriers. Use in investor materials, strategy decks, or business plans to identify disruptive forces and protect market share.

A concise, one-sheet Porter's Five Forces for Autobio Diagnostics—instantly map supplier, buyer, competitor and regulatory pressures to relieve strategic uncertainty. Customize force intensities, swap in your data, and export a clean radar chart for decks or boardroom decisions.

Customers Bargaining Power

Hospital and reference lab scale

Large hospitals, GPOs and public procurement channels concentrate purchasing, with centralized tenders in China and other markets driving reagent price declines commonly in the 20–60% range in 2023–24. Buyers leverage aggregated volume for steep discounts and service upgrades, while multi-year reagent rental contracts further intensify negotiations and margin pressure on Autobio Diagnostics.

Reagent lock-in to installed base

Analyzer-specific reagents create strong lock-in post-installation, making reagent sales a steady revenue stream in the IVD reagents market, estimated at about $54 billion in 2024. Buyers balance analyzer menu breadth and uptime against price concessions, so suppliers with broader menus command premium pricing. Contract expiries prompt aggressive re-bids as labs seek cost savings, yet superior service quality and uptime often override lowest-price bids.

Outcome and reimbursement pressure

Payers demand demonstrable cost-effectiveness as diagnostics face outcome and reimbursement pressure, with the global in vitro diagnostics market valued at about $90 billion in 2023. Labs increasingly prioritize assays with clear clinical utility and guideline support, driving purchasing toward tests with demonstrated impact on care pathways. Pharmacoeconomic evidence now shapes formulary-like lab formularies, and rising value-based procurement programs are strengthening buyer leverage.

Quality, accreditation, and data integration

Accreditation bodies such as CAP, ISO 15189 and CLIA mandate consistent performance and LIS connectivity, so buyers demand vendor verification data, QC tools and middleware integration. Vendors therefore compete on analytical sensitivity, traceability and interoperability; robust clinical and validation evidence in 2024 reduces price pressure by shifting decisions toward value over cost.

- Accreditation: CAP/ISO 15189/CLIA required

- Buyer demands: verification data, QC, middleware

- Vendor edges: sensitivity, traceability, interoperability

- Evidence: stronger data lowers price sensitivity

Menu breadth and TAT expectations

Comprehensive assay menus and sub-60-minute TAT for STAT testing drive buyer choice; vendors offering immunoassay, microbiology, chemistry and molecular on unified workflows win pricing and adoption advantages. Where gaps exist, buyers keep multi-vendor setups to preserve leverage and negotiate better service-levels. 2024 diagnostic M&A activity lifted consolidation, temporarily shifting bargaining power toward large integrated suppliers.

- Unified-workflow preference: ~62% (2024 survey)

- STAT TAT expectation: <60 minutes

- Multi-vendor retention: preserves supplier leverage

- 2024 M&A: increased consolidation, rebalance power

Buyers force reagent cuts 20–60%; analyzer lock-in shields $54B

Buyers (hospitals, GPOs, public tenders) consolidated purchases, driving reagent price declines of 20–60% in 2023–24 and intense discounting. Analyzer lock-in sustains reagent revenue (IVD reagents ≈ $54B in 2024) but buyers push for value, evidence and interoperability as reimbursement ties to outcomes (IVD market ≈ $90B in 2023). Unified-workflow preference (~62% in 2024) and M&A consolidation shift leverage intermittently.

| Metric | Value |

|---|---|

| IVD market 2023 | $90B |

| Reagents 2024 | $54B |

| Price declines 2023–24 | 20–60% |

| Unified-workflow preference 2024 | ~62% |

Preview the Actual Deliverable

Autobio Diagnostics Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Autobio Diagnostics you'll receive—no placeholders or samples—fully formatted and ready for use. It contains a thorough assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers tailored to Autobio's market position. Purchase grants instant access to this identical document for download and application.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Autobio Diagnostics faces concentrated supplier power, evolving buyer demands, and rising substitute technologies that pressure margins and growth—this brief snapshot highlights key dynamics and risks. Ready for deeper clarity? Unlock the full Porter's Five Forces Analysis to view force-by-force ratings, visuals, and actionable strategy insights tailored to Autobio Diagnostics.

Suppliers Bargaining Power

Critical biologics concentration

High-quality antibodies, antigens and enzymes are concentrated among a few vetted bioreagent suppliers, so qualification and lot-to-lot validation raise switching costs for Autobio; scarcity in specialty biomarkers gives niche vendors pricing leverage. Long-term contracts and second-sourcing reduce but do not eliminate dependency, keeping supplier bargaining power elevated into 2024.

Instrument components and OEMs

Key subsystems (optics, pumps, robotics, sensors) are sourced from specialized OEMs, creating supplier concentration that firms report as causing 6–9 month lead times in 2024 procurement cycles. Performance specs and regulatory files lock designs to specific vendors, so redesigns to swap suppliers typically exceed $1M in engineering and validation costs and add months to approval. Volume commitments can temper pricing power, often delivering 10–20% price concessions on high-volume contracts.

Disposable plastics and consumables

Tips, cuvettes, cartridges and plates are largely commoditized with broad supplier pools, reducing individual bargaining power for Autobio, yet precision tolerances and cleanliness standards restrict viable vendors and raise qualification barriers. Tooling and molds create moderate switching friction due to upfront CAPEX and 4–12 week lead times. Strategic bulk contracts can lower unit costs by up to 20–25% while preserving quality.

Regulatory-grade quality systems

Suppliers must meet ISO 13485:2016, GMP and FDA QSR (21 CFR 820) expectations, concentrating the qualified pool and raising entry barriers. Any supplier change triggers re-validation, design history file updates and possible regulatory notifications, lengthening approval timelines and strengthening supplier bargaining. Strategic quality audits and dual qualification materially reduce disruption risk.

- Regulatory standards: ISO 13485:2016, GMP, 21 CFR 820

- Change impact: re-validation + regulatory notifications

- Mitigation: quality audits, dual qualification

Geopolitical and FX exposure

Imported reagents and components expose Autobio to currency swings and export controls, which can lengthen lead times and increase buffer-stock needs, boosting supplier leverage. Disruptions from trade restrictions have tightened delivery schedules and elevated working capital requirements. Localization programs and vendor diversification, together with FX hedging, reduce but do not eliminate this supplier power.

- Imported inputs increase supplier leverage

- Export controls raise lead times and buffers

- Localization dilutes dependence over time

- Hedging/diversification partially offset volatility

2024: Supplier power high - 6-9 month lead times, >$1M switching costs, 10-25% bulk savings

Supplier power is high in 2024: key bioreagents concentrated (few vetted suppliers) and OEM subsystems cause 6–9 month lead times; redesign/validation to switch suppliers often exceeds $1M. Commoditized consumables yield 10–25% bulk savings, but ISO 13485/21 CFR 820 compliance concentrates vendors. FX, export controls increase buffers and working capital.

| Metric | 2024 Value |

|---|---|

| Lead time | 6–9 months |

| Switching cost | >$1M |

| Bulk discount | 10–25% |

| Supplier concentration | High |

What is included in the product

Tailored for Autobio Diagnostics, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer leverage, and threats from substitutes and new entrants, with strategic commentary on pricing power and market entry barriers. Use in investor materials, strategy decks, or business plans to identify disruptive forces and protect market share.

A concise, one-sheet Porter's Five Forces for Autobio Diagnostics—instantly map supplier, buyer, competitor and regulatory pressures to relieve strategic uncertainty. Customize force intensities, swap in your data, and export a clean radar chart for decks or boardroom decisions.

Customers Bargaining Power

Hospital and reference lab scale

Large hospitals, GPOs and public procurement channels concentrate purchasing, with centralized tenders in China and other markets driving reagent price declines commonly in the 20–60% range in 2023–24. Buyers leverage aggregated volume for steep discounts and service upgrades, while multi-year reagent rental contracts further intensify negotiations and margin pressure on Autobio Diagnostics.

Reagent lock-in to installed base

Analyzer-specific reagents create strong lock-in post-installation, making reagent sales a steady revenue stream in the IVD reagents market, estimated at about $54 billion in 2024. Buyers balance analyzer menu breadth and uptime against price concessions, so suppliers with broader menus command premium pricing. Contract expiries prompt aggressive re-bids as labs seek cost savings, yet superior service quality and uptime often override lowest-price bids.

Outcome and reimbursement pressure

Payers demand demonstrable cost-effectiveness as diagnostics face outcome and reimbursement pressure, with the global in vitro diagnostics market valued at about $90 billion in 2023. Labs increasingly prioritize assays with clear clinical utility and guideline support, driving purchasing toward tests with demonstrated impact on care pathways. Pharmacoeconomic evidence now shapes formulary-like lab formularies, and rising value-based procurement programs are strengthening buyer leverage.

Quality, accreditation, and data integration

Accreditation bodies such as CAP, ISO 15189 and CLIA mandate consistent performance and LIS connectivity, so buyers demand vendor verification data, QC tools and middleware integration. Vendors therefore compete on analytical sensitivity, traceability and interoperability; robust clinical and validation evidence in 2024 reduces price pressure by shifting decisions toward value over cost.

- Accreditation: CAP/ISO 15189/CLIA required

- Buyer demands: verification data, QC, middleware

- Vendor edges: sensitivity, traceability, interoperability

- Evidence: stronger data lowers price sensitivity

Menu breadth and TAT expectations

Comprehensive assay menus and sub-60-minute TAT for STAT testing drive buyer choice; vendors offering immunoassay, microbiology, chemistry and molecular on unified workflows win pricing and adoption advantages. Where gaps exist, buyers keep multi-vendor setups to preserve leverage and negotiate better service-levels. 2024 diagnostic M&A activity lifted consolidation, temporarily shifting bargaining power toward large integrated suppliers.

- Unified-workflow preference: ~62% (2024 survey)

- STAT TAT expectation: <60 minutes

- Multi-vendor retention: preserves supplier leverage

- 2024 M&A: increased consolidation, rebalance power

Buyers force reagent cuts 20–60%; analyzer lock-in shields $54B

Buyers (hospitals, GPOs, public tenders) consolidated purchases, driving reagent price declines of 20–60% in 2023–24 and intense discounting. Analyzer lock-in sustains reagent revenue (IVD reagents ≈ $54B in 2024) but buyers push for value, evidence and interoperability as reimbursement ties to outcomes (IVD market ≈ $90B in 2023). Unified-workflow preference (~62% in 2024) and M&A consolidation shift leverage intermittently.

| Metric | Value |

|---|---|

| IVD market 2023 | $90B |

| Reagents 2024 | $54B |

| Price declines 2023–24 | 20–60% |

| Unified-workflow preference 2024 | ~62% |

Preview the Actual Deliverable

Autobio Diagnostics Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Autobio Diagnostics you'll receive—no placeholders or samples—fully formatted and ready for use. It contains a thorough assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers tailored to Autobio's market position. Purchase grants instant access to this identical document for download and application.