Avanos Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

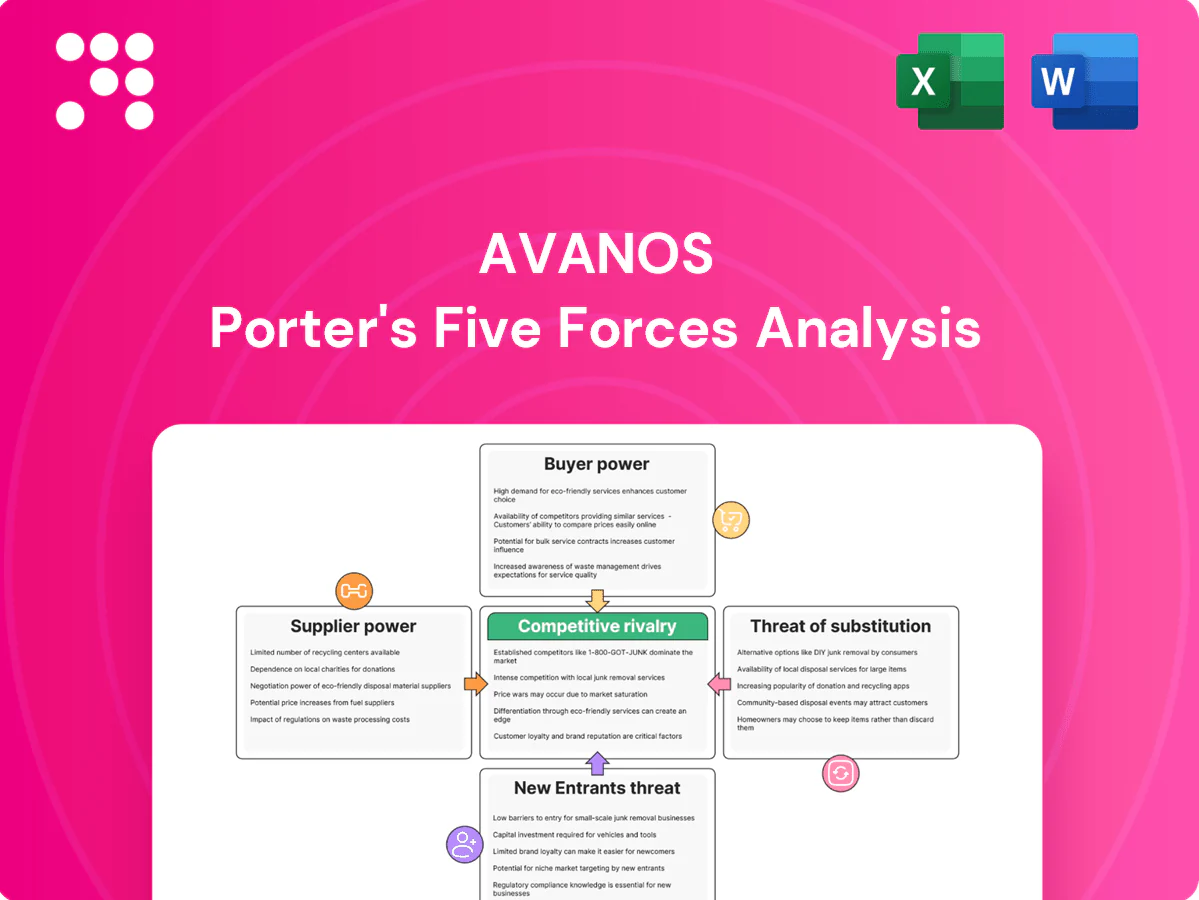

Avanos faces moderate buyer power, concentrated suppliers for clinical products, steady rivalry among medtech peers, manageable new-entrant barriers, and evolving substitute threats from alternative therapies. This snapshot highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Avanos.

Suppliers Bargaining Power

Concentrated critical materials

Avanos depends on specialized polymers, biocompatible resins and precision electronics available from few qualified suppliers, concentrating supplier power. Sterilization services such as EtO and gamma remain capacity-constrained, amplifying leverage and time-to-market risk. Disruptions can materially lengthen lead times and increase input costs. Dual-sourcing mitigates risk but supplier qualification cycles are lengthy and costly.

Regulatory-grade specifications

Suppliers for Avanos must meet ISO 13485 and FDA GMP/QSR (21 CFR Part 820) requirements, which narrows the qualified vendor pool and raises entry barriers. Qualification, validation, and change-control processes typically take 6–12 months, increasing supplier stickiness and switching costs, thereby shifting negotiating leverage upstream. Long-term supply contracts (commonly 3–5 years) reduce price volatility but lock in terms.

Proprietary components and tooling

Custom molds, catheters and RF parts for Avanos frequently rely on supplier-owned tooling—often $100k–$500k per tool—with minimum order quantities of 5k–50k units; engineering change orders can take 6–18 months and add significant cost, enabling niche suppliers to extract 5–15% price or delivery premiums and exert meaningful bargaining leverage.

Logistics and sterilization bottlenecks

Global freight and EtO sterilization queue volatility in 2024 strained availability—container and air spot rates swung over 25% while EtO capacity tightened (estimated ~20% reduction in 2023–24 amid regulatory scrutiny), limiting supplier bargaining flexibility; suppliers can and do prioritize larger-volume or higher-margin customers, forcing Avanos (FY2024 revenue ~1.1B) to buffer with inventory and diversify lanes.

- Freight volatility: spot swings >25% (2024)

- EtO capacity: ~20% reduction (2023–24)

- Supplier prioritization: favors large/higher-margin clients

- Avanos response: inventory buffers + diversified lanes

Countervailing scale and planning

Countervailing scale and planning lower supplier leverage for Avanos: 2024 global medical device market size (~624B) and visible demand allow volume discounts and centralized procurement, while vendor-managed inventory and long-range planning raise supplier utilization and reduce per-unit costs. Strategic partnerships and co-development trade margin for supply stability, partially offsetting inherent supplier power and concentration risks.

- Volume discounts from global scale

- VMI improves utilization

- Long-range planning reduces stockouts

- Co-development trades margin for stability

Concentrated suppliers; EtO ≈-20%, freight >25%

Avanos faces concentrated supplier power for specialty polymers, biocompatible resins, precision electronics and EtO sterilization, with 2024 freight spot swings >25% and EtO capacity down ~20% (2023–24). Supplier qualification (6–12 months) and tooling costs ($100k–$500k) raise switching costs; FY2024 revenue ~1.1B gives some countervailing scale.

| Metric | Value |

|---|---|

| Freight volatility (2024) | >25% |

| EtO capacity change (2023–24) | ≈-20% |

| Tooling cost | $100k–$500k |

| Supplier qual. time | 6–12 months |

| Avanos FY2024 rev | ~$1.1B |

What is included in the product

Tailored Porter's Five Forces analysis for Avanos uncovering competitive intensity, buyer/supplier leverage, threat of substitutes and new entrants, and highlighting disruptive trends and regulatory pressures that influence pricing and profitability.

A one-sheet Avanos Porter's Five Forces summary that turns complex competitive dynamics into a clean spider chart—customize pressure levels, swap in your data, and drop straight into pitch decks or executive reports.

Customers Bargaining Power

GPO and IDN consolidation

US hospitals buy predominantly through GPOs and consolidated IDNs that wield strong negotiating clout; roughly 90% of hospitals source via GPOs and the top five GPOs control about 70–80% of hospital purchasing spend.

Large tenders and formulary access hinge on contracting terms and rebates, with rebate pools commonly ranging 5–15% across device categories.

Buyers demand price concessions for multi-category awards and cross-category bundling; losing a single major IDN or system can reduce volumes for a medtech supplier by an estimated 3–10%.

Clinical outcomes and switching costs

Devices embedded in care pathways create training and protocol costs that raise switching costs for hospitals, often requiring weeks of staff training and protocol revision. Proven reductions in complications or length of stay can justify premium pricing, and value‑based purchasing remained a strong driver in 2024. If outcomes are comparable, buyers will switch on price, while robust education and KOL support reduce churn risk.

Reimbursement and budget pressure

Flat DRGs and static procedure budgets in 2024 continue to push hospitals to prioritize lower total cost, forcing procurement to demand price concessions. Value analysis committees—present in over 80% of health systems—rigorously test incremental benefit claims against clinical and economic evidence. Suppliers are routinely required to offer discounts, bundled pricing and enhanced service support; robust cost-effectiveness data is pivotal to sustain premium pricing.

Distributor leverage internationally

Outside the US distributors gatekeep market access and in 2024 Avanos derived roughly 40% of revenue from international markets, allowing partners to extract margin, exclusivity fees and co-op marketing funds. Tender-driven markets amplify price pressure and can cut supplier prices by double digits; performance clauses are increasingly used to align incentives and protect net margins.

- Distributor gatekeeping

- ~40% revenue international (2024)

- Tender-driven price pressure

- Use performance clauses

Data and transparency

Benchmark pricing databases and real-time market data have raised buyer awareness of fair rates, empowering large health systems to demand lower prices; competitive quoting and reverse auctions further compress supplier margins and shorten negotiation cycles. Buyers increasingly require inventory guarantees and consignment terms to reduce working capital, while robust post-sale clinical and service support shifts some procurement decisions away from lowest-price bids.

- Benchmarking boosts buyer leverage

- Reverse auctions compress margins

- Inventory guarantees expected

- Post-sale support reduces price-only focus

GPOs drive hospital buying: ~90% sourced; top5 70-80%

US hospitals source ~90% via GPOs; top five GPOs control ~70–80% of spend, giving buyers strong leverage. Rebates commonly 5–15% and losing a major IDN can cut supplier volumes 3–10%; value analysis committees exist in >80% of systems. Avanos had ~40% revenue from international markets (2024), where distributors and tenders drive double‑digit price cuts.

| Metric | 2024 |

|---|---|

| Hospitals via GPOs | ~90% |

| Top5 GPO spend | 70–80% |

| Rebate pools | 5–15% |

| Avanos int'l revenue | ~40% |

What You See Is What You Get

Avanos Porter's Five Forces Analysis

This preview shows the exact Avanos Porter's Five Forces analysis you'll receive—complete, professionally formatted, and ready for immediate use. No placeholders or mockups; the file available after purchase is identical to what you see here. Buy and download instantly with full confidence.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Avanos faces moderate buyer power, concentrated suppliers for clinical products, steady rivalry among medtech peers, manageable new-entrant barriers, and evolving substitute threats from alternative therapies. This snapshot highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Avanos.

Suppliers Bargaining Power

Concentrated critical materials

Avanos depends on specialized polymers, biocompatible resins and precision electronics available from few qualified suppliers, concentrating supplier power. Sterilization services such as EtO and gamma remain capacity-constrained, amplifying leverage and time-to-market risk. Disruptions can materially lengthen lead times and increase input costs. Dual-sourcing mitigates risk but supplier qualification cycles are lengthy and costly.

Regulatory-grade specifications

Suppliers for Avanos must meet ISO 13485 and FDA GMP/QSR (21 CFR Part 820) requirements, which narrows the qualified vendor pool and raises entry barriers. Qualification, validation, and change-control processes typically take 6–12 months, increasing supplier stickiness and switching costs, thereby shifting negotiating leverage upstream. Long-term supply contracts (commonly 3–5 years) reduce price volatility but lock in terms.

Proprietary components and tooling

Custom molds, catheters and RF parts for Avanos frequently rely on supplier-owned tooling—often $100k–$500k per tool—with minimum order quantities of 5k–50k units; engineering change orders can take 6–18 months and add significant cost, enabling niche suppliers to extract 5–15% price or delivery premiums and exert meaningful bargaining leverage.

Logistics and sterilization bottlenecks

Global freight and EtO sterilization queue volatility in 2024 strained availability—container and air spot rates swung over 25% while EtO capacity tightened (estimated ~20% reduction in 2023–24 amid regulatory scrutiny), limiting supplier bargaining flexibility; suppliers can and do prioritize larger-volume or higher-margin customers, forcing Avanos (FY2024 revenue ~1.1B) to buffer with inventory and diversify lanes.

- Freight volatility: spot swings >25% (2024)

- EtO capacity: ~20% reduction (2023–24)

- Supplier prioritization: favors large/higher-margin clients

- Avanos response: inventory buffers + diversified lanes

Countervailing scale and planning

Countervailing scale and planning lower supplier leverage for Avanos: 2024 global medical device market size (~624B) and visible demand allow volume discounts and centralized procurement, while vendor-managed inventory and long-range planning raise supplier utilization and reduce per-unit costs. Strategic partnerships and co-development trade margin for supply stability, partially offsetting inherent supplier power and concentration risks.

- Volume discounts from global scale

- VMI improves utilization

- Long-range planning reduces stockouts

- Co-development trades margin for stability

Concentrated suppliers; EtO ≈-20%, freight >25%

Avanos faces concentrated supplier power for specialty polymers, biocompatible resins, precision electronics and EtO sterilization, with 2024 freight spot swings >25% and EtO capacity down ~20% (2023–24). Supplier qualification (6–12 months) and tooling costs ($100k–$500k) raise switching costs; FY2024 revenue ~1.1B gives some countervailing scale.

| Metric | Value |

|---|---|

| Freight volatility (2024) | >25% |

| EtO capacity change (2023–24) | ≈-20% |

| Tooling cost | $100k–$500k |

| Supplier qual. time | 6–12 months |

| Avanos FY2024 rev | ~$1.1B |

What is included in the product

Tailored Porter's Five Forces analysis for Avanos uncovering competitive intensity, buyer/supplier leverage, threat of substitutes and new entrants, and highlighting disruptive trends and regulatory pressures that influence pricing and profitability.

A one-sheet Avanos Porter's Five Forces summary that turns complex competitive dynamics into a clean spider chart—customize pressure levels, swap in your data, and drop straight into pitch decks or executive reports.

Customers Bargaining Power

GPO and IDN consolidation

US hospitals buy predominantly through GPOs and consolidated IDNs that wield strong negotiating clout; roughly 90% of hospitals source via GPOs and the top five GPOs control about 70–80% of hospital purchasing spend.

Large tenders and formulary access hinge on contracting terms and rebates, with rebate pools commonly ranging 5–15% across device categories.

Buyers demand price concessions for multi-category awards and cross-category bundling; losing a single major IDN or system can reduce volumes for a medtech supplier by an estimated 3–10%.

Clinical outcomes and switching costs

Devices embedded in care pathways create training and protocol costs that raise switching costs for hospitals, often requiring weeks of staff training and protocol revision. Proven reductions in complications or length of stay can justify premium pricing, and value‑based purchasing remained a strong driver in 2024. If outcomes are comparable, buyers will switch on price, while robust education and KOL support reduce churn risk.

Reimbursement and budget pressure

Flat DRGs and static procedure budgets in 2024 continue to push hospitals to prioritize lower total cost, forcing procurement to demand price concessions. Value analysis committees—present in over 80% of health systems—rigorously test incremental benefit claims against clinical and economic evidence. Suppliers are routinely required to offer discounts, bundled pricing and enhanced service support; robust cost-effectiveness data is pivotal to sustain premium pricing.

Distributor leverage internationally

Outside the US distributors gatekeep market access and in 2024 Avanos derived roughly 40% of revenue from international markets, allowing partners to extract margin, exclusivity fees and co-op marketing funds. Tender-driven markets amplify price pressure and can cut supplier prices by double digits; performance clauses are increasingly used to align incentives and protect net margins.

- Distributor gatekeeping

- ~40% revenue international (2024)

- Tender-driven price pressure

- Use performance clauses

Data and transparency

Benchmark pricing databases and real-time market data have raised buyer awareness of fair rates, empowering large health systems to demand lower prices; competitive quoting and reverse auctions further compress supplier margins and shorten negotiation cycles. Buyers increasingly require inventory guarantees and consignment terms to reduce working capital, while robust post-sale clinical and service support shifts some procurement decisions away from lowest-price bids.

- Benchmarking boosts buyer leverage

- Reverse auctions compress margins

- Inventory guarantees expected

- Post-sale support reduces price-only focus

GPOs drive hospital buying: ~90% sourced; top5 70-80%

US hospitals source ~90% via GPOs; top five GPOs control ~70–80% of spend, giving buyers strong leverage. Rebates commonly 5–15% and losing a major IDN can cut supplier volumes 3–10%; value analysis committees exist in >80% of systems. Avanos had ~40% revenue from international markets (2024), where distributors and tenders drive double‑digit price cuts.

| Metric | 2024 |

|---|---|

| Hospitals via GPOs | ~90% |

| Top5 GPO spend | 70–80% |

| Rebate pools | 5–15% |

| Avanos int'l revenue | ~40% |

What You See Is What You Get

Avanos Porter's Five Forces Analysis

This preview shows the exact Avanos Porter's Five Forces analysis you'll receive—complete, professionally formatted, and ready for immediate use. No placeholders or mockups; the file available after purchase is identical to what you see here. Buy and download instantly with full confidence.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Avanos faces moderate buyer power, concentrated suppliers for clinical products, steady rivalry among medtech peers, manageable new-entrant barriers, and evolving substitute threats from alternative therapies. This snapshot highlights key tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Avanos.

Suppliers Bargaining Power

Concentrated critical materials

Avanos depends on specialized polymers, biocompatible resins and precision electronics available from few qualified suppliers, concentrating supplier power. Sterilization services such as EtO and gamma remain capacity-constrained, amplifying leverage and time-to-market risk. Disruptions can materially lengthen lead times and increase input costs. Dual-sourcing mitigates risk but supplier qualification cycles are lengthy and costly.

Regulatory-grade specifications

Suppliers for Avanos must meet ISO 13485 and FDA GMP/QSR (21 CFR Part 820) requirements, which narrows the qualified vendor pool and raises entry barriers. Qualification, validation, and change-control processes typically take 6–12 months, increasing supplier stickiness and switching costs, thereby shifting negotiating leverage upstream. Long-term supply contracts (commonly 3–5 years) reduce price volatility but lock in terms.

Proprietary components and tooling

Custom molds, catheters and RF parts for Avanos frequently rely on supplier-owned tooling—often $100k–$500k per tool—with minimum order quantities of 5k–50k units; engineering change orders can take 6–18 months and add significant cost, enabling niche suppliers to extract 5–15% price or delivery premiums and exert meaningful bargaining leverage.

Logistics and sterilization bottlenecks

Global freight and EtO sterilization queue volatility in 2024 strained availability—container and air spot rates swung over 25% while EtO capacity tightened (estimated ~20% reduction in 2023–24 amid regulatory scrutiny), limiting supplier bargaining flexibility; suppliers can and do prioritize larger-volume or higher-margin customers, forcing Avanos (FY2024 revenue ~1.1B) to buffer with inventory and diversify lanes.

- Freight volatility: spot swings >25% (2024)

- EtO capacity: ~20% reduction (2023–24)

- Supplier prioritization: favors large/higher-margin clients

- Avanos response: inventory buffers + diversified lanes

Countervailing scale and planning

Countervailing scale and planning lower supplier leverage for Avanos: 2024 global medical device market size (~624B) and visible demand allow volume discounts and centralized procurement, while vendor-managed inventory and long-range planning raise supplier utilization and reduce per-unit costs. Strategic partnerships and co-development trade margin for supply stability, partially offsetting inherent supplier power and concentration risks.

- Volume discounts from global scale

- VMI improves utilization

- Long-range planning reduces stockouts

- Co-development trades margin for stability

Concentrated suppliers; EtO ≈-20%, freight >25%

Avanos faces concentrated supplier power for specialty polymers, biocompatible resins, precision electronics and EtO sterilization, with 2024 freight spot swings >25% and EtO capacity down ~20% (2023–24). Supplier qualification (6–12 months) and tooling costs ($100k–$500k) raise switching costs; FY2024 revenue ~1.1B gives some countervailing scale.

| Metric | Value |

|---|---|

| Freight volatility (2024) | >25% |

| EtO capacity change (2023–24) | ≈-20% |

| Tooling cost | $100k–$500k |

| Supplier qual. time | 6–12 months |

| Avanos FY2024 rev | ~$1.1B |

What is included in the product

Tailored Porter's Five Forces analysis for Avanos uncovering competitive intensity, buyer/supplier leverage, threat of substitutes and new entrants, and highlighting disruptive trends and regulatory pressures that influence pricing and profitability.

A one-sheet Avanos Porter's Five Forces summary that turns complex competitive dynamics into a clean spider chart—customize pressure levels, swap in your data, and drop straight into pitch decks or executive reports.

Customers Bargaining Power

GPO and IDN consolidation

US hospitals buy predominantly through GPOs and consolidated IDNs that wield strong negotiating clout; roughly 90% of hospitals source via GPOs and the top five GPOs control about 70–80% of hospital purchasing spend.

Large tenders and formulary access hinge on contracting terms and rebates, with rebate pools commonly ranging 5–15% across device categories.

Buyers demand price concessions for multi-category awards and cross-category bundling; losing a single major IDN or system can reduce volumes for a medtech supplier by an estimated 3–10%.

Clinical outcomes and switching costs

Devices embedded in care pathways create training and protocol costs that raise switching costs for hospitals, often requiring weeks of staff training and protocol revision. Proven reductions in complications or length of stay can justify premium pricing, and value‑based purchasing remained a strong driver in 2024. If outcomes are comparable, buyers will switch on price, while robust education and KOL support reduce churn risk.

Reimbursement and budget pressure

Flat DRGs and static procedure budgets in 2024 continue to push hospitals to prioritize lower total cost, forcing procurement to demand price concessions. Value analysis committees—present in over 80% of health systems—rigorously test incremental benefit claims against clinical and economic evidence. Suppliers are routinely required to offer discounts, bundled pricing and enhanced service support; robust cost-effectiveness data is pivotal to sustain premium pricing.

Distributor leverage internationally

Outside the US distributors gatekeep market access and in 2024 Avanos derived roughly 40% of revenue from international markets, allowing partners to extract margin, exclusivity fees and co-op marketing funds. Tender-driven markets amplify price pressure and can cut supplier prices by double digits; performance clauses are increasingly used to align incentives and protect net margins.

- Distributor gatekeeping

- ~40% revenue international (2024)

- Tender-driven price pressure

- Use performance clauses

Data and transparency

Benchmark pricing databases and real-time market data have raised buyer awareness of fair rates, empowering large health systems to demand lower prices; competitive quoting and reverse auctions further compress supplier margins and shorten negotiation cycles. Buyers increasingly require inventory guarantees and consignment terms to reduce working capital, while robust post-sale clinical and service support shifts some procurement decisions away from lowest-price bids.

- Benchmarking boosts buyer leverage

- Reverse auctions compress margins

- Inventory guarantees expected

- Post-sale support reduces price-only focus

GPOs drive hospital buying: ~90% sourced; top5 70-80%

US hospitals source ~90% via GPOs; top five GPOs control ~70–80% of spend, giving buyers strong leverage. Rebates commonly 5–15% and losing a major IDN can cut supplier volumes 3–10%; value analysis committees exist in >80% of systems. Avanos had ~40% revenue from international markets (2024), where distributors and tenders drive double‑digit price cuts.

| Metric | 2024 |

|---|---|

| Hospitals via GPOs | ~90% |

| Top5 GPO spend | 70–80% |

| Rebate pools | 5–15% |

| Avanos int'l revenue | ~40% |

What You See Is What You Get

Avanos Porter's Five Forces Analysis

This preview shows the exact Avanos Porter's Five Forces analysis you'll receive—complete, professionally formatted, and ready for immediate use. No placeholders or mockups; the file available after purchase is identical to what you see here. Buy and download instantly with full confidence.