Aviat Networks Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

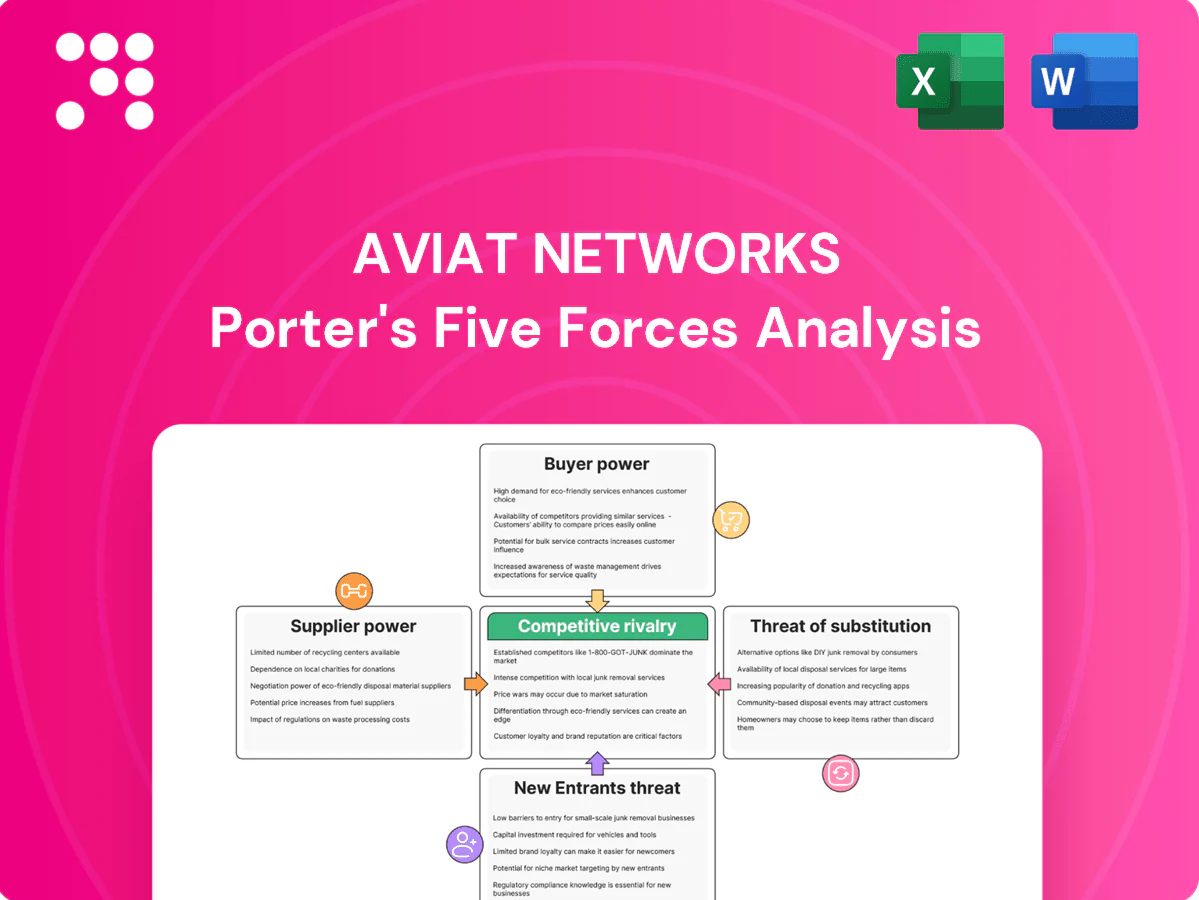

Aviat Networks faces intense competitive rivalry in wireless backhaul with moderate supplier influence and rising buyer price sensitivity; threats from new entrants are limited but technological substitutes and consolidation risks warrant attention. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated RF and semiconductor sources

Aviat depends on a narrow set of RF front-end, FPGA/SoC and high-frequency component suppliers, where 2024 semiconductor industry consolidation left the top 10 vendors controlling roughly 60% of revenue. Vendor consolidation and proprietary chipsets raise switching costs and extended lead times (often 12–20 weeks for RF/SoC parts in 2024). Any allocation or disruption can stall shipments and compress margins. Long-term contracts and dual-sourcing reduce but do not remove dependence.

Specialized materials and precision manufacturing

Specialized waveguides, antennas, E-band modules and high-reliability enclosures require precision fabrication, leaving a concentrated supplier base—by 2024 the top 5 qualified vendors still supply the majority of critical RF subcomponents—allowing pricing power and elevated MOQs. Strict quality, testing and certification regimes limit rapid supplier substitution, and contract manufacturers scale production but remain dependent on those critical sub-tier suppliers.

Firmware, software, and IP dependencies

Third-party software stacks, security libraries, and licensed algorithms embed supplier power over Aviat’s roadmap and IP exposure. Updates, security patches, and compatibility timelines often dictate release cadence and consume a meaningful share of development cycles. Royalty structures can erode roughly 3–8% of product gross margins; in-house software reduces dependency risk but cannot fully replace specialized external IP.

Logistics and compliance constraints

Export controls (ITAR/EAR) and country-specific approvals in 2024 constrain alternative sourcing paths, forcing Aviat to rely on suppliers with approved footprints and causing license-related lead times that can extend months and raise procurement costs. Geopolitical risks and tariffs have increased component complexity and price volatility for microwave and RF subsystems. Limited availability of specialized test and verification equipment further restricts throughput, giving compliant suppliers leverage in regulated markets.

- ITAR/EAR licensing delays: months

- Country approvals limit dual-source options

- Tariffs/geopolitics raise costs and complexity

- Specialized test equipment scarcity constrains throughput

- Compliant footprints = supplier leverage

Mitigation via design-for-multi-source

Engineering for pin-compatible FPGAs, RF chains, and modular designs increases leverage by enabling second-source swaps; E-band deployments operate in 71–76 GHz and 81–86 GHz bands, where RF performance constraints limit true alternatives, keeping supplier power moderate to high for leading-edge SKUs.

- Pin-compatible FPGAs enable vendor flexibility

- Modular RF chains reduce single-point failures

- Approved vendor lists + second-source tooling lower risk

- E-band physics narrows alternatives

Supplier power, long RF lead times and regulatory delays tighten E-band equipment supply

Aviat faces moderate–high supplier power: top 10 semiconductor vendors held ~60% revenue in 2024, RF/SoC lead times 12–20 weeks, royalties cutting 3–8% gross margin, and ITAR/EAR licensing adding months of delay; E-band (71–76/81–86 GHz) physics and specialized fabrication keep substitution hard despite pin-compatible design gains.

| Metric | 2024 |

|---|---|

| Top10 share | ~60% |

| Lead times | 12–20 weeks |

| Royalty drag | 3–8% GM |

| ITAR/EAR delays | Months |

What is included in the product

Tailored Porter’s Five Forces analysis for Aviat Networks uncovering competitive intensity, supplier and buyer bargaining power, threat of substitutes, and barriers to entry that shape pricing and profitability. It highlights disruptive wireless/backhaul technologies, emerging competitors, and strategic levers Aviat can use to protect market share and margins.

Clear, one-sheet Porter's Five Forces for Aviat Networks—instantly visualize competitive pressure with a customizable spider chart and swap in your own data to reflect shifts in regulation, suppliers, or new entrants; export-ready for decks and simple enough for non-finance users.

Customers Bargaining Power

Large carrier and government concentration

Mobile network operators and public agencies buy at scale and run formal RFPs, with global telecom operator capital expenditure around $300 billion in 2024, concentrating purchasing power. High deal sizes and multi-year frameworks (often >$10m) give buyers strong negotiating leverage. Customers demand price breaks, strict SLAs and customization. Lost tenders can materially dent Aviat's pipeline and revenue visibility.

Price sensitivity and TCO focus

Procurement in 2024 prioritizes capex per bit and opex efficiency, forcing vendors like Aviat to justify lifecycle costs rather than headline prices. Competing bids from multiple vendors amplify price pressure and push buyers to TCO comparisons that weigh energy use, spectrum efficiency and maintenance frequency. Discounting and financing terms frequently swing procurement decisions in favor of lower upfront or guaranteed-cost offers.

Switching costs tempered by standards

Installed base, network management software and trained staff create stickiness for Aviat Networks, supporting recurring service revenue after fiscal 2024 revenue of $242.3 million; however, global interoperability standards and multivendor backhaul strategies let buyers cherry-pick by link class, band or region. Switching costs are meaningful but not prohibitive as operators optimize cost-performance across vendors.

Service and lifecycle leverage

Customers push for extended warranties, spares, and professional services, tying payments to SLAs that often demand 99.99–99.999% availability (99.999% ≈ 5.26 minutes downtime/year), shifting risk and penalties onto vendors. Lifecycle roadmaps and refresh timing drive selection toward vendors that guarantee long-term support and predictable obsolescence. Service bundling is used to extract concessions on price and lead times.

- Warranty & spares leverage

- Availability clauses (99.99–99.999%)

- Lifecycle roadmaps influence refresh

- Bundling extracts concessions

Regulatory and security requirements

Government and critical-infrastructure buyers insist on certifications like FedRAMP, NIST SP 800-171 and the DoD's CMMC 2.0 (rolled out through 2023–24), which narrows the vendor pool but raises procurement scrutiny and technical due diligence.

- Compliance as leverage

- Data sovereignty demands

- Supply-chain attestations

- Qualification ≠ price relief

Buyers wield leverage: operator capex $300B vs vendor revenue $242.3M

Customers hold strong leverage: operator capex ~$300B (2024) vs Aviat FY2024 revenue $242.3M, with many RFPs >$10M and strict SLAs. Buyers push TCO, energy and maintenance metrics, use multivendor tendering and service bundling to extract price and financing concessions. Compliance (FedRAMP, CMMC 2.0) narrows vendors but raises procurement rigor.

| Metric | 2024 |

|---|---|

| Operator capex | $300B |

| Aviat revenue | $242.3M |

| Typical RFP | >$10M |

Same Document Delivered

Aviat Networks Porter's Five Forces Analysis

This preview shows the Aviat Networks Porter's Five Forces Analysis exactly as you'll receive it—no placeholders or mockups. The full, professionally formatted document is ready for download and immediate use the moment you complete your purchase. You're viewing the actual deliverable, with complete analysis and actionable insights included.

Go Beyond the Preview—Access the Full Strategic Report

Aviat Networks faces intense competitive rivalry in wireless backhaul with moderate supplier influence and rising buyer price sensitivity; threats from new entrants are limited but technological substitutes and consolidation risks warrant attention. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated RF and semiconductor sources

Aviat depends on a narrow set of RF front-end, FPGA/SoC and high-frequency component suppliers, where 2024 semiconductor industry consolidation left the top 10 vendors controlling roughly 60% of revenue. Vendor consolidation and proprietary chipsets raise switching costs and extended lead times (often 12–20 weeks for RF/SoC parts in 2024). Any allocation or disruption can stall shipments and compress margins. Long-term contracts and dual-sourcing reduce but do not remove dependence.

Specialized materials and precision manufacturing

Specialized waveguides, antennas, E-band modules and high-reliability enclosures require precision fabrication, leaving a concentrated supplier base—by 2024 the top 5 qualified vendors still supply the majority of critical RF subcomponents—allowing pricing power and elevated MOQs. Strict quality, testing and certification regimes limit rapid supplier substitution, and contract manufacturers scale production but remain dependent on those critical sub-tier suppliers.

Firmware, software, and IP dependencies

Third-party software stacks, security libraries, and licensed algorithms embed supplier power over Aviat’s roadmap and IP exposure. Updates, security patches, and compatibility timelines often dictate release cadence and consume a meaningful share of development cycles. Royalty structures can erode roughly 3–8% of product gross margins; in-house software reduces dependency risk but cannot fully replace specialized external IP.

Logistics and compliance constraints

Export controls (ITAR/EAR) and country-specific approvals in 2024 constrain alternative sourcing paths, forcing Aviat to rely on suppliers with approved footprints and causing license-related lead times that can extend months and raise procurement costs. Geopolitical risks and tariffs have increased component complexity and price volatility for microwave and RF subsystems. Limited availability of specialized test and verification equipment further restricts throughput, giving compliant suppliers leverage in regulated markets.

- ITAR/EAR licensing delays: months

- Country approvals limit dual-source options

- Tariffs/geopolitics raise costs and complexity

- Specialized test equipment scarcity constrains throughput

- Compliant footprints = supplier leverage

Mitigation via design-for-multi-source

Engineering for pin-compatible FPGAs, RF chains, and modular designs increases leverage by enabling second-source swaps; E-band deployments operate in 71–76 GHz and 81–86 GHz bands, where RF performance constraints limit true alternatives, keeping supplier power moderate to high for leading-edge SKUs.

- Pin-compatible FPGAs enable vendor flexibility

- Modular RF chains reduce single-point failures

- Approved vendor lists + second-source tooling lower risk

- E-band physics narrows alternatives

Supplier power, long RF lead times and regulatory delays tighten E-band equipment supply

Aviat faces moderate–high supplier power: top 10 semiconductor vendors held ~60% revenue in 2024, RF/SoC lead times 12–20 weeks, royalties cutting 3–8% gross margin, and ITAR/EAR licensing adding months of delay; E-band (71–76/81–86 GHz) physics and specialized fabrication keep substitution hard despite pin-compatible design gains.

| Metric | 2024 |

|---|---|

| Top10 share | ~60% |

| Lead times | 12–20 weeks |

| Royalty drag | 3–8% GM |

| ITAR/EAR delays | Months |

What is included in the product

Tailored Porter’s Five Forces analysis for Aviat Networks uncovering competitive intensity, supplier and buyer bargaining power, threat of substitutes, and barriers to entry that shape pricing and profitability. It highlights disruptive wireless/backhaul technologies, emerging competitors, and strategic levers Aviat can use to protect market share and margins.

Clear, one-sheet Porter's Five Forces for Aviat Networks—instantly visualize competitive pressure with a customizable spider chart and swap in your own data to reflect shifts in regulation, suppliers, or new entrants; export-ready for decks and simple enough for non-finance users.

Customers Bargaining Power

Large carrier and government concentration

Mobile network operators and public agencies buy at scale and run formal RFPs, with global telecom operator capital expenditure around $300 billion in 2024, concentrating purchasing power. High deal sizes and multi-year frameworks (often >$10m) give buyers strong negotiating leverage. Customers demand price breaks, strict SLAs and customization. Lost tenders can materially dent Aviat's pipeline and revenue visibility.

Price sensitivity and TCO focus

Procurement in 2024 prioritizes capex per bit and opex efficiency, forcing vendors like Aviat to justify lifecycle costs rather than headline prices. Competing bids from multiple vendors amplify price pressure and push buyers to TCO comparisons that weigh energy use, spectrum efficiency and maintenance frequency. Discounting and financing terms frequently swing procurement decisions in favor of lower upfront or guaranteed-cost offers.

Switching costs tempered by standards

Installed base, network management software and trained staff create stickiness for Aviat Networks, supporting recurring service revenue after fiscal 2024 revenue of $242.3 million; however, global interoperability standards and multivendor backhaul strategies let buyers cherry-pick by link class, band or region. Switching costs are meaningful but not prohibitive as operators optimize cost-performance across vendors.

Service and lifecycle leverage

Customers push for extended warranties, spares, and professional services, tying payments to SLAs that often demand 99.99–99.999% availability (99.999% ≈ 5.26 minutes downtime/year), shifting risk and penalties onto vendors. Lifecycle roadmaps and refresh timing drive selection toward vendors that guarantee long-term support and predictable obsolescence. Service bundling is used to extract concessions on price and lead times.

- Warranty & spares leverage

- Availability clauses (99.99–99.999%)

- Lifecycle roadmaps influence refresh

- Bundling extracts concessions

Regulatory and security requirements

Government and critical-infrastructure buyers insist on certifications like FedRAMP, NIST SP 800-171 and the DoD's CMMC 2.0 (rolled out through 2023–24), which narrows the vendor pool but raises procurement scrutiny and technical due diligence.

- Compliance as leverage

- Data sovereignty demands

- Supply-chain attestations

- Qualification ≠ price relief

Buyers wield leverage: operator capex $300B vs vendor revenue $242.3M

Customers hold strong leverage: operator capex ~$300B (2024) vs Aviat FY2024 revenue $242.3M, with many RFPs >$10M and strict SLAs. Buyers push TCO, energy and maintenance metrics, use multivendor tendering and service bundling to extract price and financing concessions. Compliance (FedRAMP, CMMC 2.0) narrows vendors but raises procurement rigor.

| Metric | 2024 |

|---|---|

| Operator capex | $300B |

| Aviat revenue | $242.3M |

| Typical RFP | >$10M |

Same Document Delivered

Aviat Networks Porter's Five Forces Analysis

This preview shows the Aviat Networks Porter's Five Forces Analysis exactly as you'll receive it—no placeholders or mockups. The full, professionally formatted document is ready for download and immediate use the moment you complete your purchase. You're viewing the actual deliverable, with complete analysis and actionable insights included.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Aviat Networks faces intense competitive rivalry in wireless backhaul with moderate supplier influence and rising buyer price sensitivity; threats from new entrants are limited but technological substitutes and consolidation risks warrant attention. This snapshot highlights key pressure points and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated RF and semiconductor sources

Aviat depends on a narrow set of RF front-end, FPGA/SoC and high-frequency component suppliers, where 2024 semiconductor industry consolidation left the top 10 vendors controlling roughly 60% of revenue. Vendor consolidation and proprietary chipsets raise switching costs and extended lead times (often 12–20 weeks for RF/SoC parts in 2024). Any allocation or disruption can stall shipments and compress margins. Long-term contracts and dual-sourcing reduce but do not remove dependence.

Specialized materials and precision manufacturing

Specialized waveguides, antennas, E-band modules and high-reliability enclosures require precision fabrication, leaving a concentrated supplier base—by 2024 the top 5 qualified vendors still supply the majority of critical RF subcomponents—allowing pricing power and elevated MOQs. Strict quality, testing and certification regimes limit rapid supplier substitution, and contract manufacturers scale production but remain dependent on those critical sub-tier suppliers.

Firmware, software, and IP dependencies

Third-party software stacks, security libraries, and licensed algorithms embed supplier power over Aviat’s roadmap and IP exposure. Updates, security patches, and compatibility timelines often dictate release cadence and consume a meaningful share of development cycles. Royalty structures can erode roughly 3–8% of product gross margins; in-house software reduces dependency risk but cannot fully replace specialized external IP.

Logistics and compliance constraints

Export controls (ITAR/EAR) and country-specific approvals in 2024 constrain alternative sourcing paths, forcing Aviat to rely on suppliers with approved footprints and causing license-related lead times that can extend months and raise procurement costs. Geopolitical risks and tariffs have increased component complexity and price volatility for microwave and RF subsystems. Limited availability of specialized test and verification equipment further restricts throughput, giving compliant suppliers leverage in regulated markets.

- ITAR/EAR licensing delays: months

- Country approvals limit dual-source options

- Tariffs/geopolitics raise costs and complexity

- Specialized test equipment scarcity constrains throughput

- Compliant footprints = supplier leverage

Mitigation via design-for-multi-source

Engineering for pin-compatible FPGAs, RF chains, and modular designs increases leverage by enabling second-source swaps; E-band deployments operate in 71–76 GHz and 81–86 GHz bands, where RF performance constraints limit true alternatives, keeping supplier power moderate to high for leading-edge SKUs.

- Pin-compatible FPGAs enable vendor flexibility

- Modular RF chains reduce single-point failures

- Approved vendor lists + second-source tooling lower risk

- E-band physics narrows alternatives

Supplier power, long RF lead times and regulatory delays tighten E-band equipment supply

Aviat faces moderate–high supplier power: top 10 semiconductor vendors held ~60% revenue in 2024, RF/SoC lead times 12–20 weeks, royalties cutting 3–8% gross margin, and ITAR/EAR licensing adding months of delay; E-band (71–76/81–86 GHz) physics and specialized fabrication keep substitution hard despite pin-compatible design gains.

| Metric | 2024 |

|---|---|

| Top10 share | ~60% |

| Lead times | 12–20 weeks |

| Royalty drag | 3–8% GM |

| ITAR/EAR delays | Months |

What is included in the product

Tailored Porter’s Five Forces analysis for Aviat Networks uncovering competitive intensity, supplier and buyer bargaining power, threat of substitutes, and barriers to entry that shape pricing and profitability. It highlights disruptive wireless/backhaul technologies, emerging competitors, and strategic levers Aviat can use to protect market share and margins.

Clear, one-sheet Porter's Five Forces for Aviat Networks—instantly visualize competitive pressure with a customizable spider chart and swap in your own data to reflect shifts in regulation, suppliers, or new entrants; export-ready for decks and simple enough for non-finance users.

Customers Bargaining Power

Large carrier and government concentration

Mobile network operators and public agencies buy at scale and run formal RFPs, with global telecom operator capital expenditure around $300 billion in 2024, concentrating purchasing power. High deal sizes and multi-year frameworks (often >$10m) give buyers strong negotiating leverage. Customers demand price breaks, strict SLAs and customization. Lost tenders can materially dent Aviat's pipeline and revenue visibility.

Price sensitivity and TCO focus

Procurement in 2024 prioritizes capex per bit and opex efficiency, forcing vendors like Aviat to justify lifecycle costs rather than headline prices. Competing bids from multiple vendors amplify price pressure and push buyers to TCO comparisons that weigh energy use, spectrum efficiency and maintenance frequency. Discounting and financing terms frequently swing procurement decisions in favor of lower upfront or guaranteed-cost offers.

Switching costs tempered by standards

Installed base, network management software and trained staff create stickiness for Aviat Networks, supporting recurring service revenue after fiscal 2024 revenue of $242.3 million; however, global interoperability standards and multivendor backhaul strategies let buyers cherry-pick by link class, band or region. Switching costs are meaningful but not prohibitive as operators optimize cost-performance across vendors.

Service and lifecycle leverage

Customers push for extended warranties, spares, and professional services, tying payments to SLAs that often demand 99.99–99.999% availability (99.999% ≈ 5.26 minutes downtime/year), shifting risk and penalties onto vendors. Lifecycle roadmaps and refresh timing drive selection toward vendors that guarantee long-term support and predictable obsolescence. Service bundling is used to extract concessions on price and lead times.

- Warranty & spares leverage

- Availability clauses (99.99–99.999%)

- Lifecycle roadmaps influence refresh

- Bundling extracts concessions

Regulatory and security requirements

Government and critical-infrastructure buyers insist on certifications like FedRAMP, NIST SP 800-171 and the DoD's CMMC 2.0 (rolled out through 2023–24), which narrows the vendor pool but raises procurement scrutiny and technical due diligence.

- Compliance as leverage

- Data sovereignty demands

- Supply-chain attestations

- Qualification ≠ price relief

Buyers wield leverage: operator capex $300B vs vendor revenue $242.3M

Customers hold strong leverage: operator capex ~$300B (2024) vs Aviat FY2024 revenue $242.3M, with many RFPs >$10M and strict SLAs. Buyers push TCO, energy and maintenance metrics, use multivendor tendering and service bundling to extract price and financing concessions. Compliance (FedRAMP, CMMC 2.0) narrows vendors but raises procurement rigor.

| Metric | 2024 |

|---|---|

| Operator capex | $300B |

| Aviat revenue | $242.3M |

| Typical RFP | >$10M |

Same Document Delivered

Aviat Networks Porter's Five Forces Analysis

This preview shows the Aviat Networks Porter's Five Forces Analysis exactly as you'll receive it—no placeholders or mockups. The full, professionally formatted document is ready for download and immediate use the moment you complete your purchase. You're viewing the actual deliverable, with complete analysis and actionable insights included.