Avient Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Avient’s Porter's Five Forces snapshot highlights strong supplier relationships, moderate buyer power, niche substitute threats, and high industry rivalry driven by specialty polymer innovation. This brief view flags key strategic risks and growth levers. Unlock the full Porter's Five Forces Analysis to explore Avient’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Avient reported $3.9 billion revenue in 2023, yet relies on a limited set of upstream petrochemical producers for key resins and monomers, creating material exposure to supplier concentration. Few global crackers and resin majors can tighten supply during disruptions, amplifying price pass-through pressure on Avient. Hedging and diversified sourcing mitigate but only partially offset volatility.

Specialty additives and pigments

High-performance additives, colorants and functional pigments are often supplied by niche firms, and the global pigments/additives market was roughly $30–40 billion in 2024, underscoring concentrated value pools. Differentiated chemistries and tight qualifying specs give suppliers leverage and limited substitutability raises switching costs. Avient reduces supplier power through co-development, multi-vendor sourcing and long-term agreements.

Recycled and bio-based inputs scarcity

Premium recyclate and bio-feedstocks remain supply constrained and quality variable, with suppliers of certified circular materials commanding premiums often in the 15–30% range versus virgin resins in 2023–24.

Tight availability, with high-grade recyclate volumes limited to low single-digit millions of tonnes globally, amplifies supplier power in sustainability-led segments.

Long-term offtakes and certification partnerships are used to secure volume and price stability for Avient.

Qualification and switching costs

Material requalification in regulated end-markets (healthcare, food-contact) is costly and time-consuming, often requiring 6–12 months and extensive documentation and testing. This creates bilateral dependence with critical suppliers while simultaneously raising Avient’s switching barriers. Implementing dual-qualification programs reduces single-supplier risk and preserves supply continuity.

- 6–12 months requalification

- Bilateral supplier dependence

- Dual-qualification mitigates single-supplier risk

Logistics and energy cost pass-through

Energy prices (Brent averaged about $86/bbl in 2024) and volatile global freight raise upstream costs that suppliers can pass downstream; regional suppliers or vertically integrated producers exert pricing power during tight supply periods, while Avient’s global footprint and sourcing flexibility provide some cost arbitrage; acute spikes, however, still bolster supplier leverage.

- 2024 Brent ≈ $86/bbl

- Drewry WCI normalized vs 2021 peaks, increasing supplier pass-through risk in short shocks

- Regional/integrated suppliers = stronger terms

- Avient global footprint = partial mitigation

Concentrated resin/additive supply raises pass-through risk; recyclate premium 15–30%

Avient (revenue $3.9B in 2023) faces supplier concentration for key resins and niche additives, amplifying price pass-through and switching costs. Pigments/additives market ~$30–40B (2024); high-grade recyclate premiums ~15–30% vs virgin (2023–24). Requalification in regulated markets takes 6–12 months; Brent ~$86/bbl (2024) raises upstream pass-through risk.

| Metric | Value |

|---|---|

| Avient revenue (2023) | $3.9B |

| Pigments/additives (2024) | $30–40B |

| Recyclate premium | 15–30% |

| Requalification | 6–12 months |

| Brent (2024) | $86/bbl |

What is included in the product

Tailored Porter's Five Forces analysis for Avient that uncovers key competitive drivers—supplier and buyer power, threat of substitutes, new entrants, and rivalry—highlighting disruptive threats, pricing influence, and barriers protecting incumbents, delivered in fully editable format for strategic and investor use.

A concise Porter's Five Forces snapshot for Avient—clarifies supplier, buyer, rivalry, and threat pressures at a glance to speed strategic decisions and prioritize mitigation actions.

Customers Bargaining Power

Large OEM and CPG purchasing scale

Large OEMs and CPGs in packaging, healthcare and transportation buy pigments, compounds and colorants at scale and negotiate aggressively, concentrating volume to push down prices and raise service expectations.

Performance-driven differentiation

Where formulations are mission-critical, buyers face high switching and failure risks, so Avient’s performance-led products weaken pure price pressure; Avient reported roughly $3.0 billion revenue in 2024, underscoring scale in critical markets. Superior material properties and application support shift buyer focus from cost to reliability, reducing bargaining power in safety- or compliance-sensitive uses. Documented performance data and regulatory compliance (FDA, REACH) are decisive levers.

Multi-sourcing and commoditized grades

In standard masterbatch and commodity formulations buyers can multi-source easily; comparable offerings intensify price competition, with masterbatch pressure contributing to margin strain—Avient reported roughly $3.1 billion revenue in 2024, highlighting exposure to commoditized segments. This strengthens buyer bargaining power. Avient counters by selling customized formulations and bundled services to protect margins.

Sustainability and compliance demands

Design and technical service stickiness

Design co-development, color-matching and on-site processing support embed Avient into customer workflows, raising practical switching costs and making pure price-based moves unattractive; Avient reported approximately $3.08 billion revenue in FY2024, underscoring scale of services tied to product sales.

- Co-development embeds know-how

- Color-matching raises asset-specific switching costs

- Processing support reduces price elasticity

- Service-level agreements anchor relationships

Scale, services and circularity defend margins as OEM consolidation squeezes commodity prices

Large OEMs and CPGs consolidate volume to press prices, raising buyer bargaining power in commoditized masterbatch and pigment segments.

Where formulations are mission-critical Avient’s performance products, regulatory compliance and SLA-backed services reduce pure price pressure and switching risk.

Sustainability mandates and LCA requirements shift qualification costs to suppliers but Avient’s circularity services and co-development restore pricing leverage; 2024 revenue ~$3.08B.

| Metric | 2024 | Impact |

|---|---|---|

| Revenue | $3.08B | Scale in critical markets, supports service-led margin defense |

What You See Is What You Get

Avient Porter's Five Forces Analysis

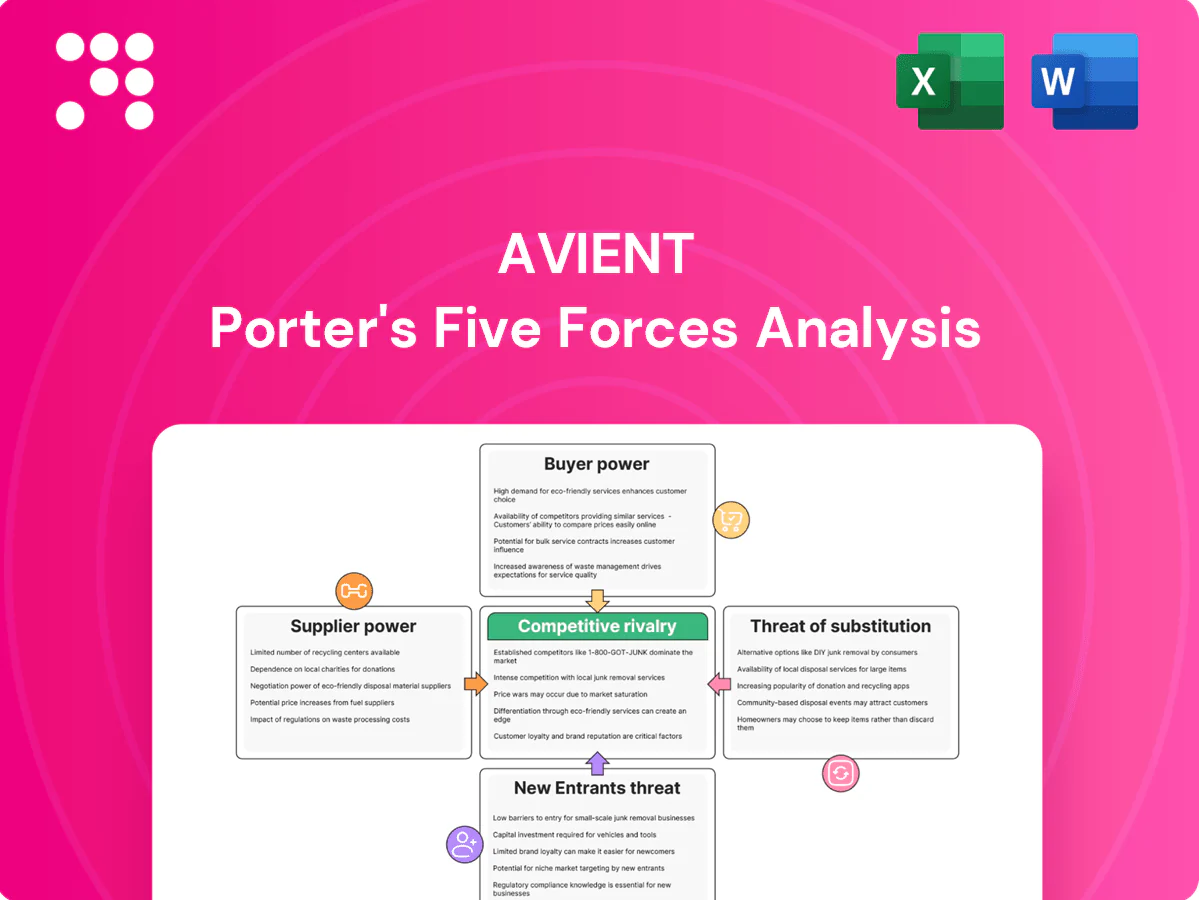

This preview shows the exact Avient Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the actual deliverable; upon payment you'll get instant access to this same document.

Go Beyond the Preview—Access the Full Strategic Report

Avient’s Porter's Five Forces snapshot highlights strong supplier relationships, moderate buyer power, niche substitute threats, and high industry rivalry driven by specialty polymer innovation. This brief view flags key strategic risks and growth levers. Unlock the full Porter's Five Forces Analysis to explore Avient’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Avient reported $3.9 billion revenue in 2023, yet relies on a limited set of upstream petrochemical producers for key resins and monomers, creating material exposure to supplier concentration. Few global crackers and resin majors can tighten supply during disruptions, amplifying price pass-through pressure on Avient. Hedging and diversified sourcing mitigate but only partially offset volatility.

Specialty additives and pigments

High-performance additives, colorants and functional pigments are often supplied by niche firms, and the global pigments/additives market was roughly $30–40 billion in 2024, underscoring concentrated value pools. Differentiated chemistries and tight qualifying specs give suppliers leverage and limited substitutability raises switching costs. Avient reduces supplier power through co-development, multi-vendor sourcing and long-term agreements.

Recycled and bio-based inputs scarcity

Premium recyclate and bio-feedstocks remain supply constrained and quality variable, with suppliers of certified circular materials commanding premiums often in the 15–30% range versus virgin resins in 2023–24.

Tight availability, with high-grade recyclate volumes limited to low single-digit millions of tonnes globally, amplifies supplier power in sustainability-led segments.

Long-term offtakes and certification partnerships are used to secure volume and price stability for Avient.

Qualification and switching costs

Material requalification in regulated end-markets (healthcare, food-contact) is costly and time-consuming, often requiring 6–12 months and extensive documentation and testing. This creates bilateral dependence with critical suppliers while simultaneously raising Avient’s switching barriers. Implementing dual-qualification programs reduces single-supplier risk and preserves supply continuity.

- 6–12 months requalification

- Bilateral supplier dependence

- Dual-qualification mitigates single-supplier risk

Logistics and energy cost pass-through

Energy prices (Brent averaged about $86/bbl in 2024) and volatile global freight raise upstream costs that suppliers can pass downstream; regional suppliers or vertically integrated producers exert pricing power during tight supply periods, while Avient’s global footprint and sourcing flexibility provide some cost arbitrage; acute spikes, however, still bolster supplier leverage.

- 2024 Brent ≈ $86/bbl

- Drewry WCI normalized vs 2021 peaks, increasing supplier pass-through risk in short shocks

- Regional/integrated suppliers = stronger terms

- Avient global footprint = partial mitigation

Concentrated resin/additive supply raises pass-through risk; recyclate premium 15–30%

Avient (revenue $3.9B in 2023) faces supplier concentration for key resins and niche additives, amplifying price pass-through and switching costs. Pigments/additives market ~$30–40B (2024); high-grade recyclate premiums ~15–30% vs virgin (2023–24). Requalification in regulated markets takes 6–12 months; Brent ~$86/bbl (2024) raises upstream pass-through risk.

| Metric | Value |

|---|---|

| Avient revenue (2023) | $3.9B |

| Pigments/additives (2024) | $30–40B |

| Recyclate premium | 15–30% |

| Requalification | 6–12 months |

| Brent (2024) | $86/bbl |

What is included in the product

Tailored Porter's Five Forces analysis for Avient that uncovers key competitive drivers—supplier and buyer power, threat of substitutes, new entrants, and rivalry—highlighting disruptive threats, pricing influence, and barriers protecting incumbents, delivered in fully editable format for strategic and investor use.

A concise Porter's Five Forces snapshot for Avient—clarifies supplier, buyer, rivalry, and threat pressures at a glance to speed strategic decisions and prioritize mitigation actions.

Customers Bargaining Power

Large OEM and CPG purchasing scale

Large OEMs and CPGs in packaging, healthcare and transportation buy pigments, compounds and colorants at scale and negotiate aggressively, concentrating volume to push down prices and raise service expectations.

Performance-driven differentiation

Where formulations are mission-critical, buyers face high switching and failure risks, so Avient’s performance-led products weaken pure price pressure; Avient reported roughly $3.0 billion revenue in 2024, underscoring scale in critical markets. Superior material properties and application support shift buyer focus from cost to reliability, reducing bargaining power in safety- or compliance-sensitive uses. Documented performance data and regulatory compliance (FDA, REACH) are decisive levers.

Multi-sourcing and commoditized grades

In standard masterbatch and commodity formulations buyers can multi-source easily; comparable offerings intensify price competition, with masterbatch pressure contributing to margin strain—Avient reported roughly $3.1 billion revenue in 2024, highlighting exposure to commoditized segments. This strengthens buyer bargaining power. Avient counters by selling customized formulations and bundled services to protect margins.

Sustainability and compliance demands

Design and technical service stickiness

Design co-development, color-matching and on-site processing support embed Avient into customer workflows, raising practical switching costs and making pure price-based moves unattractive; Avient reported approximately $3.08 billion revenue in FY2024, underscoring scale of services tied to product sales.

- Co-development embeds know-how

- Color-matching raises asset-specific switching costs

- Processing support reduces price elasticity

- Service-level agreements anchor relationships

Scale, services and circularity defend margins as OEM consolidation squeezes commodity prices

Large OEMs and CPGs consolidate volume to press prices, raising buyer bargaining power in commoditized masterbatch and pigment segments.

Where formulations are mission-critical Avient’s performance products, regulatory compliance and SLA-backed services reduce pure price pressure and switching risk.

Sustainability mandates and LCA requirements shift qualification costs to suppliers but Avient’s circularity services and co-development restore pricing leverage; 2024 revenue ~$3.08B.

| Metric | 2024 | Impact |

|---|---|---|

| Revenue | $3.08B | Scale in critical markets, supports service-led margin defense |

What You See Is What You Get

Avient Porter's Five Forces Analysis

This preview shows the exact Avient Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the actual deliverable; upon payment you'll get instant access to this same document.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Avient’s Porter's Five Forces snapshot highlights strong supplier relationships, moderate buyer power, niche substitute threats, and high industry rivalry driven by specialty polymer innovation. This brief view flags key strategic risks and growth levers. Unlock the full Porter's Five Forces Analysis to explore Avient’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Petrochemical feedstock concentration

Avient reported $3.9 billion revenue in 2023, yet relies on a limited set of upstream petrochemical producers for key resins and monomers, creating material exposure to supplier concentration. Few global crackers and resin majors can tighten supply during disruptions, amplifying price pass-through pressure on Avient. Hedging and diversified sourcing mitigate but only partially offset volatility.

Specialty additives and pigments

High-performance additives, colorants and functional pigments are often supplied by niche firms, and the global pigments/additives market was roughly $30–40 billion in 2024, underscoring concentrated value pools. Differentiated chemistries and tight qualifying specs give suppliers leverage and limited substitutability raises switching costs. Avient reduces supplier power through co-development, multi-vendor sourcing and long-term agreements.

Recycled and bio-based inputs scarcity

Premium recyclate and bio-feedstocks remain supply constrained and quality variable, with suppliers of certified circular materials commanding premiums often in the 15–30% range versus virgin resins in 2023–24.

Tight availability, with high-grade recyclate volumes limited to low single-digit millions of tonnes globally, amplifies supplier power in sustainability-led segments.

Long-term offtakes and certification partnerships are used to secure volume and price stability for Avient.

Qualification and switching costs

Material requalification in regulated end-markets (healthcare, food-contact) is costly and time-consuming, often requiring 6–12 months and extensive documentation and testing. This creates bilateral dependence with critical suppliers while simultaneously raising Avient’s switching barriers. Implementing dual-qualification programs reduces single-supplier risk and preserves supply continuity.

- 6–12 months requalification

- Bilateral supplier dependence

- Dual-qualification mitigates single-supplier risk

Logistics and energy cost pass-through

Energy prices (Brent averaged about $86/bbl in 2024) and volatile global freight raise upstream costs that suppliers can pass downstream; regional suppliers or vertically integrated producers exert pricing power during tight supply periods, while Avient’s global footprint and sourcing flexibility provide some cost arbitrage; acute spikes, however, still bolster supplier leverage.

- 2024 Brent ≈ $86/bbl

- Drewry WCI normalized vs 2021 peaks, increasing supplier pass-through risk in short shocks

- Regional/integrated suppliers = stronger terms

- Avient global footprint = partial mitigation

Concentrated resin/additive supply raises pass-through risk; recyclate premium 15–30%

Avient (revenue $3.9B in 2023) faces supplier concentration for key resins and niche additives, amplifying price pass-through and switching costs. Pigments/additives market ~$30–40B (2024); high-grade recyclate premiums ~15–30% vs virgin (2023–24). Requalification in regulated markets takes 6–12 months; Brent ~$86/bbl (2024) raises upstream pass-through risk.

| Metric | Value |

|---|---|

| Avient revenue (2023) | $3.9B |

| Pigments/additives (2024) | $30–40B |

| Recyclate premium | 15–30% |

| Requalification | 6–12 months |

| Brent (2024) | $86/bbl |

What is included in the product

Tailored Porter's Five Forces analysis for Avient that uncovers key competitive drivers—supplier and buyer power, threat of substitutes, new entrants, and rivalry—highlighting disruptive threats, pricing influence, and barriers protecting incumbents, delivered in fully editable format for strategic and investor use.

A concise Porter's Five Forces snapshot for Avient—clarifies supplier, buyer, rivalry, and threat pressures at a glance to speed strategic decisions and prioritize mitigation actions.

Customers Bargaining Power

Large OEM and CPG purchasing scale

Large OEMs and CPGs in packaging, healthcare and transportation buy pigments, compounds and colorants at scale and negotiate aggressively, concentrating volume to push down prices and raise service expectations.

Performance-driven differentiation

Where formulations are mission-critical, buyers face high switching and failure risks, so Avient’s performance-led products weaken pure price pressure; Avient reported roughly $3.0 billion revenue in 2024, underscoring scale in critical markets. Superior material properties and application support shift buyer focus from cost to reliability, reducing bargaining power in safety- or compliance-sensitive uses. Documented performance data and regulatory compliance (FDA, REACH) are decisive levers.

Multi-sourcing and commoditized grades

In standard masterbatch and commodity formulations buyers can multi-source easily; comparable offerings intensify price competition, with masterbatch pressure contributing to margin strain—Avient reported roughly $3.1 billion revenue in 2024, highlighting exposure to commoditized segments. This strengthens buyer bargaining power. Avient counters by selling customized formulations and bundled services to protect margins.

Sustainability and compliance demands

Design and technical service stickiness

Design co-development, color-matching and on-site processing support embed Avient into customer workflows, raising practical switching costs and making pure price-based moves unattractive; Avient reported approximately $3.08 billion revenue in FY2024, underscoring scale of services tied to product sales.

- Co-development embeds know-how

- Color-matching raises asset-specific switching costs

- Processing support reduces price elasticity

- Service-level agreements anchor relationships

Scale, services and circularity defend margins as OEM consolidation squeezes commodity prices

Large OEMs and CPGs consolidate volume to press prices, raising buyer bargaining power in commoditized masterbatch and pigment segments.

Where formulations are mission-critical Avient’s performance products, regulatory compliance and SLA-backed services reduce pure price pressure and switching risk.

Sustainability mandates and LCA requirements shift qualification costs to suppliers but Avient’s circularity services and co-development restore pricing leverage; 2024 revenue ~$3.08B.

| Metric | 2024 | Impact |

|---|---|---|

| Revenue | $3.08B | Scale in critical markets, supports service-led margin defense |

What You See Is What You Get

Avient Porter's Five Forces Analysis

This preview shows the exact Avient Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the actual deliverable; upon payment you'll get instant access to this same document.