Avingtrans Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

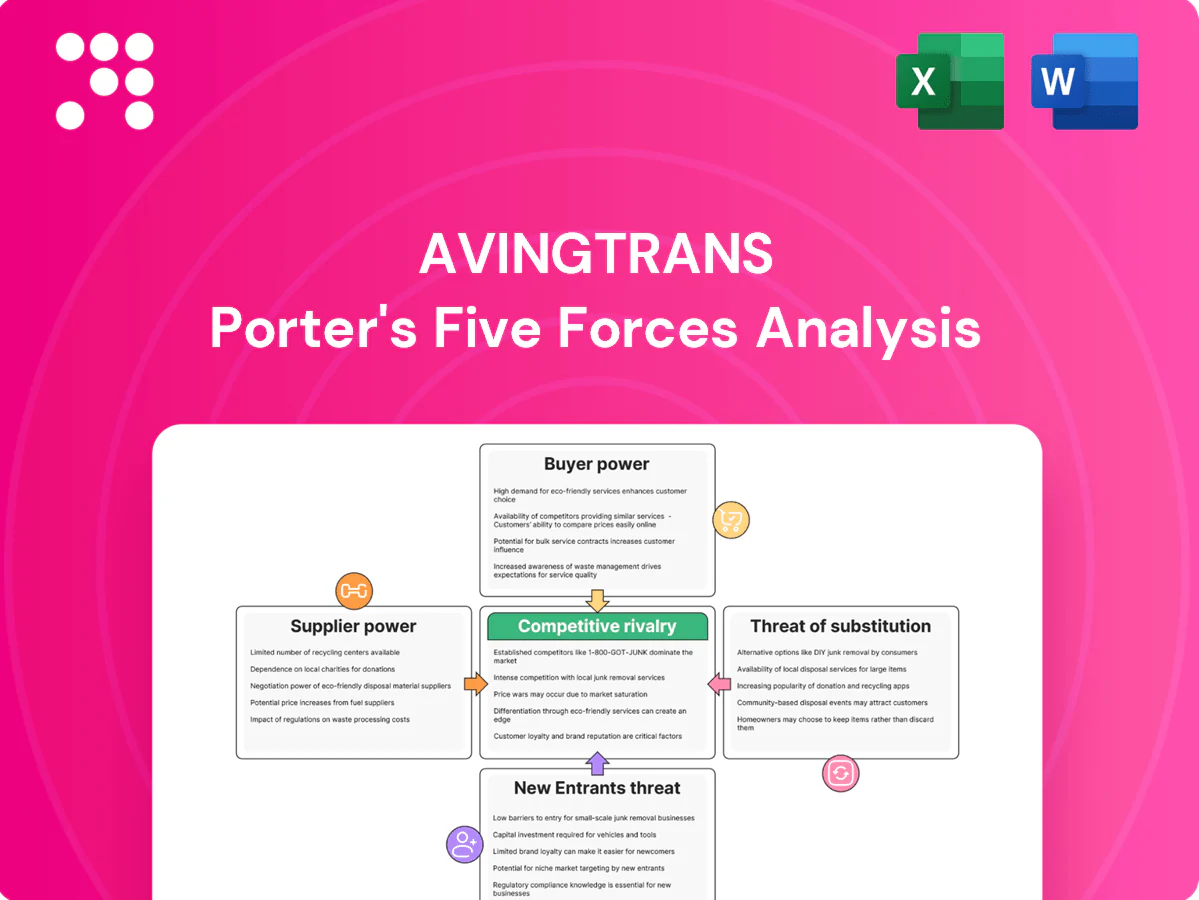

Avingtrans faces moderate supplier power, niche buyer leverage, and heightened rivalry from engineering peers, while barriers to entry and substitute threats vary by segment. Strategic partnerships and specialist IP are key defenses. This snapshot highlights immediate risks and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Avingtrans.

Suppliers Bargaining Power

Specialized, certified inputs

Many inputs for Avingtrans are niche—radiation‑tolerant materials, precision forgings and OEM‑approved sub‑assemblies—so certification regimes like nuclear and medical sharply constrain the pool of compliant suppliers. Limited alternatives raise supplier leverage and can pressure lead times and margins. Avingtrans mitigates this via extensive approved vendor lists and broad supplier qualification programs to secure continuity and cost control.

Long lead times, capacity constraints

Complex alloys, custom tooling and extended QA routinely push lead times to 12–24 weeks; in 2024 sector surveys reported average specialty component lead times near 18 weeks. When upstream capacity tightens, delivery risk and expediting premiums can rise 15–30%, strengthening suppliers in peak cycles. Forward scheduling and 8–12 weeks of safety stock are commonly used to buffer volatility.

Switching costs and requalification

Changing a supplier often triggers costly requalification and documentation, with validation cycles in regulated markets frequently taking 6–24 months and requalification costs reaching six figures. That regulatory stickiness elevates supplier bargaining power by increasing exit costs and lead-time risk. Multi-sourcing and early supplier involvement reduce lock-in and compress qualification timelines, lowering supplier leverage.

Input price volatility

Metals, energy and precision components show cyclical price swings that can pass through to Avingtrans quickly via supplier surcharges; Brent crude averaged about $86/barrel in 2024, amplifying energy-related input cost risk. Where contracts lack indexation, margin pressure shifts to Avingtrans, while hedging and pass-through clauses have been used to counteract spikes.

- Surcharge pass-through: weeks to implement

- Contract indexation: reduces margin leakage

- Hedging & pass-through: primary mitigation

Geopolitical and compliance risk

Geopolitical and compliance risks—expanded export controls, sanctions, and tightening ESG provenance rules—have narrowed supplier options for Avingtrans, with any disruption to critical geographies (China accounts for ~27% of global goods exports in 2024) able to choke component flows; this systemic risk indirectly raises supplier power while regional diversification and onshoring reduce exposure.

- Export controls/sanctions: shrink sourcing flexibility

- Concentration risk: China ~27% of goods exports (2024)

- Mitigation: regional diversification, onshoring

High supplier power: 12–24 week lead times, 6–24 month requalification, Brent $86/barrel

Supplier power is high due to niche, certified inputs and limited alternatives; lead times run 12–24 weeks (sector avg ~18 weeks in 2024), increasing leverage. Requalification in regulated markets takes 6–24 months with six‑figure costs, while energy (Brent ~$86/barrel in 2024) and China concentration (~27% of goods exports, 2024) raise pass‑through risk. Mitigations: multi‑sourcing, 8–12 weeks safety stock, contract indexation and hedging.

| Metric | Value (2024) |

|---|---|

| Avg specialty lead time | ~18 weeks |

| Requalification | 6–24 months; six‑figure cost |

| Safety stock | 8–12 weeks |

| Brent crude | $86/barrel |

| China share exports | ~27% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Avingtrans, uncovering competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers to assess pricing power, profitability risks, and strategic levers for growth.

Clear, one-sheet Porter's Five Forces for Avingtrans—instantly highlights competitive pressures and relief points so you can prioritize strategic moves and operational fixes with minimal effort.

Customers Bargaining Power

Concentrated, blue‑chip customers

Concentrated, blue‑chip buyers such as EDF, GE/GE‑Hitachi and med‑tech majors like Siemens Healthineers and Medtronic dominate demand; the global medical device market was roughly USD 520bn in 2024 and nuclear capacity stands near 390 GW, concentrating spend. Their scale and professional procurement raise bargaining leverage, enforcing price discipline and stringent SLAs. Long, multi‑year relationships with suppliers partially mitigate but do not eliminate margin pressure.

High qualification, low substitutability

Avingtrans, AIM-listed (ticker AVG), supplies customized safety‑critical parts that limit apples‑to‑apples comparisons; bespoke design‑in and regulatory traceability make vendor switching slow and costly. This embeds Avingtrans in in‑life programs and softens buyer power, with competitive tension concentrated at new tenders where specification changes reopen procurement.

Project‑based tendering

Large, episodic contracts (often >£1m) drive intense competitive bids and heightened price scrutiny, compressing margins at the bid stage. Buyers increasingly demand lifecycle cost transparency and include penalty clauses, shifting cost risk upstream. Margin volatility concentrates at tendering, so robust estimating and value engineering are critical to protect returns and win-repeat profitability.

Service and aftermarket leverage

Maintenance, spares and upgrades generate recurring revenue and aftersales margins for Avingtrans, with a large installed base and proprietary know‑how limiting buyer options after installation and shifting bargaining power toward the supplier across asset lifecycles. Performance‑based contracts can align incentives and share value fairly between Avingtrans and customers.

- Recurring revenue from maintenance and spares

- Installed base + know‑how reduces post‑install buyer switching

- Performance contracts enable fair value sharing

Compliance and delivery performance

Buyers enforce stringent quality and on-time metrics, with industry OTIF targets typically at or above 95% in 2024; failures can trigger chargebacks often cited at 1–3% of order value or supplier disqualification. Avingtrans’ strong QMS and schedule adherence reduce claims, while data-driven KPIs (delivery punctuality, defect rates, lead-time variance) underpin credibility and pricing power.

- OTIF ≥95% (2024 industry target)

- Chargebacks commonly 1–3% of order value

- KPIs: punctuality, defect rate, lead-time variance

Blue-chip buyers enforce strict price discipline, installed-base stickiness softens switches

Concentrated blue‑chip buyers (EDF, GE/GE‑Hitachi, Siemens Healthineers) wield strong price discipline; global med‑tech market ~USD 520bn (2024) and nuclear capacity ~390 GW concentrate spend. Avingtrans’ bespoke, safety‑critical parts and installed base soften switching but intense >£1m tenders and OTIF ≥95% targets keep margin pressure.

| Metric | 2024 |

|---|---|

| Med‑tech market | USD 520bn |

| Nuclear capacity | ~390 GW |

| OTIF target | ≥95% |

| Chargebacks | 1–3% order value |

Preview Before You Purchase

Avingtrans Porter's Five Forces Analysis

This Avingtrans Porter’s Five Forces analysis evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and industry profitability to inform strategic decisions. The preview is the exact, fully formatted document you’ll receive upon purchase—no placeholders or changes. You’ll have immediate access to this complete, ready-to-use file after payment.

Go Beyond the Preview—Access the Full Strategic Report

Avingtrans faces moderate supplier power, niche buyer leverage, and heightened rivalry from engineering peers, while barriers to entry and substitute threats vary by segment. Strategic partnerships and specialist IP are key defenses. This snapshot highlights immediate risks and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Avingtrans.

Suppliers Bargaining Power

Specialized, certified inputs

Many inputs for Avingtrans are niche—radiation‑tolerant materials, precision forgings and OEM‑approved sub‑assemblies—so certification regimes like nuclear and medical sharply constrain the pool of compliant suppliers. Limited alternatives raise supplier leverage and can pressure lead times and margins. Avingtrans mitigates this via extensive approved vendor lists and broad supplier qualification programs to secure continuity and cost control.

Long lead times, capacity constraints

Complex alloys, custom tooling and extended QA routinely push lead times to 12–24 weeks; in 2024 sector surveys reported average specialty component lead times near 18 weeks. When upstream capacity tightens, delivery risk and expediting premiums can rise 15–30%, strengthening suppliers in peak cycles. Forward scheduling and 8–12 weeks of safety stock are commonly used to buffer volatility.

Switching costs and requalification

Changing a supplier often triggers costly requalification and documentation, with validation cycles in regulated markets frequently taking 6–24 months and requalification costs reaching six figures. That regulatory stickiness elevates supplier bargaining power by increasing exit costs and lead-time risk. Multi-sourcing and early supplier involvement reduce lock-in and compress qualification timelines, lowering supplier leverage.

Input price volatility

Metals, energy and precision components show cyclical price swings that can pass through to Avingtrans quickly via supplier surcharges; Brent crude averaged about $86/barrel in 2024, amplifying energy-related input cost risk. Where contracts lack indexation, margin pressure shifts to Avingtrans, while hedging and pass-through clauses have been used to counteract spikes.

- Surcharge pass-through: weeks to implement

- Contract indexation: reduces margin leakage

- Hedging & pass-through: primary mitigation

Geopolitical and compliance risk

Geopolitical and compliance risks—expanded export controls, sanctions, and tightening ESG provenance rules—have narrowed supplier options for Avingtrans, with any disruption to critical geographies (China accounts for ~27% of global goods exports in 2024) able to choke component flows; this systemic risk indirectly raises supplier power while regional diversification and onshoring reduce exposure.

- Export controls/sanctions: shrink sourcing flexibility

- Concentration risk: China ~27% of goods exports (2024)

- Mitigation: regional diversification, onshoring

High supplier power: 12–24 week lead times, 6–24 month requalification, Brent $86/barrel

Supplier power is high due to niche, certified inputs and limited alternatives; lead times run 12–24 weeks (sector avg ~18 weeks in 2024), increasing leverage. Requalification in regulated markets takes 6–24 months with six‑figure costs, while energy (Brent ~$86/barrel in 2024) and China concentration (~27% of goods exports, 2024) raise pass‑through risk. Mitigations: multi‑sourcing, 8–12 weeks safety stock, contract indexation and hedging.

| Metric | Value (2024) |

|---|---|

| Avg specialty lead time | ~18 weeks |

| Requalification | 6–24 months; six‑figure cost |

| Safety stock | 8–12 weeks |

| Brent crude | $86/barrel |

| China share exports | ~27% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Avingtrans, uncovering competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers to assess pricing power, profitability risks, and strategic levers for growth.

Clear, one-sheet Porter's Five Forces for Avingtrans—instantly highlights competitive pressures and relief points so you can prioritize strategic moves and operational fixes with minimal effort.

Customers Bargaining Power

Concentrated, blue‑chip customers

Concentrated, blue‑chip buyers such as EDF, GE/GE‑Hitachi and med‑tech majors like Siemens Healthineers and Medtronic dominate demand; the global medical device market was roughly USD 520bn in 2024 and nuclear capacity stands near 390 GW, concentrating spend. Their scale and professional procurement raise bargaining leverage, enforcing price discipline and stringent SLAs. Long, multi‑year relationships with suppliers partially mitigate but do not eliminate margin pressure.

High qualification, low substitutability

Avingtrans, AIM-listed (ticker AVG), supplies customized safety‑critical parts that limit apples‑to‑apples comparisons; bespoke design‑in and regulatory traceability make vendor switching slow and costly. This embeds Avingtrans in in‑life programs and softens buyer power, with competitive tension concentrated at new tenders where specification changes reopen procurement.

Project‑based tendering

Large, episodic contracts (often >£1m) drive intense competitive bids and heightened price scrutiny, compressing margins at the bid stage. Buyers increasingly demand lifecycle cost transparency and include penalty clauses, shifting cost risk upstream. Margin volatility concentrates at tendering, so robust estimating and value engineering are critical to protect returns and win-repeat profitability.

Service and aftermarket leverage

Maintenance, spares and upgrades generate recurring revenue and aftersales margins for Avingtrans, with a large installed base and proprietary know‑how limiting buyer options after installation and shifting bargaining power toward the supplier across asset lifecycles. Performance‑based contracts can align incentives and share value fairly between Avingtrans and customers.

- Recurring revenue from maintenance and spares

- Installed base + know‑how reduces post‑install buyer switching

- Performance contracts enable fair value sharing

Compliance and delivery performance

Buyers enforce stringent quality and on-time metrics, with industry OTIF targets typically at or above 95% in 2024; failures can trigger chargebacks often cited at 1–3% of order value or supplier disqualification. Avingtrans’ strong QMS and schedule adherence reduce claims, while data-driven KPIs (delivery punctuality, defect rates, lead-time variance) underpin credibility and pricing power.

- OTIF ≥95% (2024 industry target)

- Chargebacks commonly 1–3% of order value

- KPIs: punctuality, defect rate, lead-time variance

Blue-chip buyers enforce strict price discipline, installed-base stickiness softens switches

Concentrated blue‑chip buyers (EDF, GE/GE‑Hitachi, Siemens Healthineers) wield strong price discipline; global med‑tech market ~USD 520bn (2024) and nuclear capacity ~390 GW concentrate spend. Avingtrans’ bespoke, safety‑critical parts and installed base soften switching but intense >£1m tenders and OTIF ≥95% targets keep margin pressure.

| Metric | 2024 |

|---|---|

| Med‑tech market | USD 520bn |

| Nuclear capacity | ~390 GW |

| OTIF target | ≥95% |

| Chargebacks | 1–3% order value |

Preview Before You Purchase

Avingtrans Porter's Five Forces Analysis

This Avingtrans Porter’s Five Forces analysis evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and industry profitability to inform strategic decisions. The preview is the exact, fully formatted document you’ll receive upon purchase—no placeholders or changes. You’ll have immediate access to this complete, ready-to-use file after payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Avingtrans faces moderate supplier power, niche buyer leverage, and heightened rivalry from engineering peers, while barriers to entry and substitute threats vary by segment. Strategic partnerships and specialist IP are key defenses. This snapshot highlights immediate risks and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Avingtrans.

Suppliers Bargaining Power

Specialized, certified inputs

Many inputs for Avingtrans are niche—radiation‑tolerant materials, precision forgings and OEM‑approved sub‑assemblies—so certification regimes like nuclear and medical sharply constrain the pool of compliant suppliers. Limited alternatives raise supplier leverage and can pressure lead times and margins. Avingtrans mitigates this via extensive approved vendor lists and broad supplier qualification programs to secure continuity and cost control.

Long lead times, capacity constraints

Complex alloys, custom tooling and extended QA routinely push lead times to 12–24 weeks; in 2024 sector surveys reported average specialty component lead times near 18 weeks. When upstream capacity tightens, delivery risk and expediting premiums can rise 15–30%, strengthening suppliers in peak cycles. Forward scheduling and 8–12 weeks of safety stock are commonly used to buffer volatility.

Switching costs and requalification

Changing a supplier often triggers costly requalification and documentation, with validation cycles in regulated markets frequently taking 6–24 months and requalification costs reaching six figures. That regulatory stickiness elevates supplier bargaining power by increasing exit costs and lead-time risk. Multi-sourcing and early supplier involvement reduce lock-in and compress qualification timelines, lowering supplier leverage.

Input price volatility

Metals, energy and precision components show cyclical price swings that can pass through to Avingtrans quickly via supplier surcharges; Brent crude averaged about $86/barrel in 2024, amplifying energy-related input cost risk. Where contracts lack indexation, margin pressure shifts to Avingtrans, while hedging and pass-through clauses have been used to counteract spikes.

- Surcharge pass-through: weeks to implement

- Contract indexation: reduces margin leakage

- Hedging & pass-through: primary mitigation

Geopolitical and compliance risk

Geopolitical and compliance risks—expanded export controls, sanctions, and tightening ESG provenance rules—have narrowed supplier options for Avingtrans, with any disruption to critical geographies (China accounts for ~27% of global goods exports in 2024) able to choke component flows; this systemic risk indirectly raises supplier power while regional diversification and onshoring reduce exposure.

- Export controls/sanctions: shrink sourcing flexibility

- Concentration risk: China ~27% of goods exports (2024)

- Mitigation: regional diversification, onshoring

High supplier power: 12–24 week lead times, 6–24 month requalification, Brent $86/barrel

Supplier power is high due to niche, certified inputs and limited alternatives; lead times run 12–24 weeks (sector avg ~18 weeks in 2024), increasing leverage. Requalification in regulated markets takes 6–24 months with six‑figure costs, while energy (Brent ~$86/barrel in 2024) and China concentration (~27% of goods exports, 2024) raise pass‑through risk. Mitigations: multi‑sourcing, 8–12 weeks safety stock, contract indexation and hedging.

| Metric | Value (2024) |

|---|---|

| Avg specialty lead time | ~18 weeks |

| Requalification | 6–24 months; six‑figure cost |

| Safety stock | 8–12 weeks |

| Brent crude | $86/barrel |

| China share exports | ~27% |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Avingtrans, uncovering competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers to assess pricing power, profitability risks, and strategic levers for growth.

Clear, one-sheet Porter's Five Forces for Avingtrans—instantly highlights competitive pressures and relief points so you can prioritize strategic moves and operational fixes with minimal effort.

Customers Bargaining Power

Concentrated, blue‑chip customers

Concentrated, blue‑chip buyers such as EDF, GE/GE‑Hitachi and med‑tech majors like Siemens Healthineers and Medtronic dominate demand; the global medical device market was roughly USD 520bn in 2024 and nuclear capacity stands near 390 GW, concentrating spend. Their scale and professional procurement raise bargaining leverage, enforcing price discipline and stringent SLAs. Long, multi‑year relationships with suppliers partially mitigate but do not eliminate margin pressure.

High qualification, low substitutability

Avingtrans, AIM-listed (ticker AVG), supplies customized safety‑critical parts that limit apples‑to‑apples comparisons; bespoke design‑in and regulatory traceability make vendor switching slow and costly. This embeds Avingtrans in in‑life programs and softens buyer power, with competitive tension concentrated at new tenders where specification changes reopen procurement.

Project‑based tendering

Large, episodic contracts (often >£1m) drive intense competitive bids and heightened price scrutiny, compressing margins at the bid stage. Buyers increasingly demand lifecycle cost transparency and include penalty clauses, shifting cost risk upstream. Margin volatility concentrates at tendering, so robust estimating and value engineering are critical to protect returns and win-repeat profitability.

Service and aftermarket leverage

Maintenance, spares and upgrades generate recurring revenue and aftersales margins for Avingtrans, with a large installed base and proprietary know‑how limiting buyer options after installation and shifting bargaining power toward the supplier across asset lifecycles. Performance‑based contracts can align incentives and share value fairly between Avingtrans and customers.

- Recurring revenue from maintenance and spares

- Installed base + know‑how reduces post‑install buyer switching

- Performance contracts enable fair value sharing

Compliance and delivery performance

Buyers enforce stringent quality and on-time metrics, with industry OTIF targets typically at or above 95% in 2024; failures can trigger chargebacks often cited at 1–3% of order value or supplier disqualification. Avingtrans’ strong QMS and schedule adherence reduce claims, while data-driven KPIs (delivery punctuality, defect rates, lead-time variance) underpin credibility and pricing power.

- OTIF ≥95% (2024 industry target)

- Chargebacks commonly 1–3% of order value

- KPIs: punctuality, defect rate, lead-time variance

Blue-chip buyers enforce strict price discipline, installed-base stickiness softens switches

Concentrated blue‑chip buyers (EDF, GE/GE‑Hitachi, Siemens Healthineers) wield strong price discipline; global med‑tech market ~USD 520bn (2024) and nuclear capacity ~390 GW concentrate spend. Avingtrans’ bespoke, safety‑critical parts and installed base soften switching but intense >£1m tenders and OTIF ≥95% targets keep margin pressure.

| Metric | 2024 |

|---|---|

| Med‑tech market | USD 520bn |

| Nuclear capacity | ~390 GW |

| OTIF target | ≥95% |

| Chargebacks | 1–3% order value |

Preview Before You Purchase

Avingtrans Porter's Five Forces Analysis

This Avingtrans Porter’s Five Forces analysis evaluates supplier and buyer power, competitive rivalry, threat of substitutes and new entrants, and industry profitability to inform strategic decisions. The preview is the exact, fully formatted document you’ll receive upon purchase—no placeholders or changes. You’ll have immediate access to this complete, ready-to-use file after payment.