Axsome Business Model Canvas

Unlock the strategic playbook: Complete Business Model Canvas for investors and founders

Unlock Axsome’s strategic playbook with our full Business Model Canvas—clarifying value propositions, revenue levers, partnerships and growth risks in one ready-to-use file. Ideal for investors, advisors, and founders wanting actionable insights; download the complete Canvas to benchmark and build winning strategies.

Partnerships

CROs and CDMOs

CROs and CDMOs let Axsome scale R&D and GMP production without heavy fixed investment; the global CRO market topped $60B in 2024 and the CDMO sector surpassed $160B in 2024, reflecting broad outsourcing adoption. They enable rapid trial startup, wider geographic reach, and GMP-scale manufacturing to accelerate timelines. Strategic vendor selection manages quality and cost, while multi-vendor redundancy cuts supply risk.

Academic and KOL Networks

Universities and KOLs collaborate on target validation, trial design and peer-reviewed publication, reinforcing Axsome assets such as AXS-05 and AXS-07 whose pivotal trials led to FDA approvals in 2022–2023 and underpin ongoing 2024 evidence generation. These partnerships drive credibility in CNS disorders and accelerate data accrual. Active KOL advocacy supports guideline consideration and formulary decisions, while joint research may reveal novel indications.

Patient Advocacy and Registries

Patient advocacy groups improve recruitment, retention and real-world insights; ClinicalTrials.gov lists over 420,000 studies, highlighting registry value in matching patients to trials. Collaboration with advocates refines endpoints toward meaningful outcomes and patient-reported measures. Orphanet tracks >6,000 rare disease registries, whose natural history data inform trial design and strengthen market-access dossiers. Advocacy networks also boost disease awareness and adherence support.

Payers and PBMs

Payers and PBMs drive access through value-based and outcomes-sharing frameworks that tie reimbursement to real-world results, shaping coverage and step-edit policies via early engagement. HEOR collaborations establish cost-effectiveness narratives (commonly using $100,000–$150,000 per QALY thresholds) to support formulary placement. Data-sharing agreements improve utilization management and patient persistence, lowering total cost of care; US prescription drug spend was roughly $577B in 2023.

Commercial and Distribution Partners

Commercial partners such as specialty pharmacies, wholesalers, and ex-US licensees extend Axsome’s reach into specialty channels and international markets, while co-promotion alliances accelerate uptake in targeted specialties; specialty medicines accounted for about 55% of US drug spending in 2023 (IQVIA). Third-party logistics providers and HUB services streamline cold-chain logistics, reimbursement support, and patient onboarding to reduce time-to-therapy.

- Specialty pharmacies: channel access and adherence

- Wholesalers: national distribution scale

- Co-promotion: faster specialist adoption

- 3PLs/HUBs: logistics, REMS, patient support

- International licensees: local regs and payers

CROs/CDMOs scale R&D/GMP; specialty meds drive US $577B market, 55% spend

CROs/CDMOs scale R&D and GMP production—global CRO market $60B and CDMO $160B in 2024—reducing capex and accelerating timelines. KOLs/universities validate targets and drive publications for AXS-05/07 (FDA approvals 2022–2023). Payers, PBMs, specialty pharmacies and 3PLs enable access; specialty medicines =55% of US drug spend (2023), US drug spend $577B (2023).

| Partner | Role | 2023/24 metric |

|---|---|---|

| CRO/CDMO | Scale R&D/GMP | $60B/$160B (2024) |

| KOLs/Univ | Evidence & advocacy | FDA approvals 2022–23 |

| Payers/PBMs | Access & VBAs | $577B drug spend (2023) |

| Commercial | Distribution & HUBs | 55% specialty spend (2023) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Axsome that maps all nine BMC blocks with detailed customer segments, channels, value propositions and monetization, plus competitive advantages and SWOT-linked insights for presentations and investor discussions.

Editable one-page Business Model Canvas for Axsome that condenses strategy into a clean, shareable layout—saving hours of formatting, enabling fast executive summaries, supporting team collaboration, and ideal for boardroom reviews or side-by-side comparisons.

Activities

R&D and Clinical Development

Axsome advances discovery, formulation and phase 1–3 clinical trials to de-risk CNS assets; AXS-05 (Auvelity) received FDA approval in August 2022. Biomarker strategy and endpoint selection are tailored to CNS heterogeneity to improve signal detection. Portfolio prioritization weighs risk, time-to-market and unmet need. Continuous interim data monitoring drives go/no-go decisions.

Regulatory Strategy and Submissions

End-to-end engagement with FDA and EMA drives designations and approvals, following PDUFA review timelines (standard 10 months, priority 6 months) and 2024 EMA procedures for MAA interactions. Preparation of INDs, NDAs and MAAs plus structured post-marketing commitments and Phase IV studies are routine. Label negotiation targets optimized positioning and claims to support uptake. Pharmacovigilance planning, including REMS and safety signal monitoring, is integrated into regulatory pathways.

Manufacturing and Quality Management

Scale-up of API and finished-dose manufacturing is managed under stringent QA/QC with formal tech transfer and process validation protocols to transition from pilot to commercial batches. Robust supply-chain risk control, including supplier qualification and dual sourcing, supports on-time supply. Serialization, cold-chain where required, and tight inventory management ensure traceability and product integrity. Continuous process verification monitors stability and manufacturing reliability.

Market Access and Medical Affairs

Axsome drives market access through HEOR and budget‑impact modeling to support pricing and payer negotiations; in 2024 specialty drugs represented ~50% of US drug spend, making robust value dossiers essential. MSL engagement, peer‑reviewed publications and congress presence build the evidence base and KOL advocacy. Treatment‑pathway integration and KAM work with IDNs plus patient services (patient support programs can cut abandonment ~35%) reduce access friction.

- HEOR / BIM for pricing & payers

- MSL, publications, congress presence

- KAM & IDN pathway integration

- Patient services to lower abandonment ~35%

Commercialization and Lifecycle Management

Commercialization and lifecycle management focus on launch planning, targeted field force deployment and omnichannel campaigns initiated in 2024 to drive uptake, supported by indication expansion, label updates and selective reformulations. Real-world evidence programs collect persistence and outcomes data while competitive intelligence shapes differentiation.

- Launch planning: 2024 omnichannel rollouts

- Field force: targeted HCP coverage

- RWE: persistence/outcomes collection

- Lifecycle: label/indication updates

- CI: informs differentiation

CNS pipeline; PDUFA 6–10m, services cut abandonment 35%

Axsome advances CNS discovery to phase 1–3, AXS-05 approved Aug 2022, portfolio prioritization balances risk/time-to-market. Regulatory engagement targets PDUFA 6–10 months and 2024 EMA MAA pathways; IND/NDA/MAA prep plus REMS and PV are routine. Manufacturing scales via tech transfer, dual sourcing and process validation; HEOR, KOLs and patient services (reduce abandonment ~35%) drive access; specialty drugs ~50% of US spend in 2024.

| Metric | 2024 Figure |

|---|---|

| Specialty share of US drug spend | ~50% |

| Patient abandonment reduction (services) | ~35% |

| PDUFA timelines | Priority 6m / Standard 10m |

Delivered as Displayed

Business Model Canvas

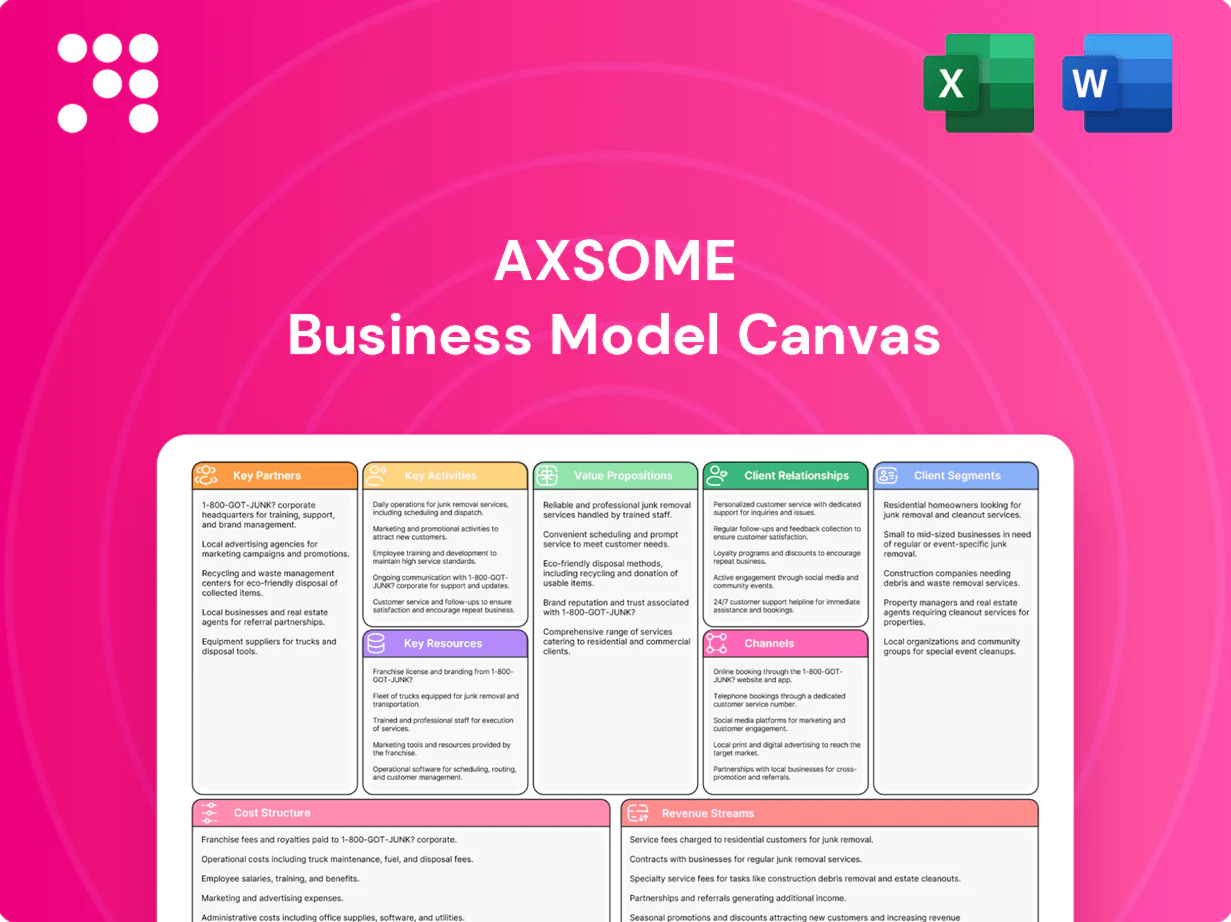

The preview you see is the actual Axsome Business Model Canvas, not a mockup—it's a direct snapshot of the final deliverable. When you purchase, you’ll receive this exact, fully editable file (Word and Excel) with all content and pages included, ready to present or customize. No surprises, just the document you previewed.

Unlock the strategic playbook: Complete Business Model Canvas for investors and founders

Unlock Axsome’s strategic playbook with our full Business Model Canvas—clarifying value propositions, revenue levers, partnerships and growth risks in one ready-to-use file. Ideal for investors, advisors, and founders wanting actionable insights; download the complete Canvas to benchmark and build winning strategies.

Partnerships

CROs and CDMOs

CROs and CDMOs let Axsome scale R&D and GMP production without heavy fixed investment; the global CRO market topped $60B in 2024 and the CDMO sector surpassed $160B in 2024, reflecting broad outsourcing adoption. They enable rapid trial startup, wider geographic reach, and GMP-scale manufacturing to accelerate timelines. Strategic vendor selection manages quality and cost, while multi-vendor redundancy cuts supply risk.

Academic and KOL Networks

Universities and KOLs collaborate on target validation, trial design and peer-reviewed publication, reinforcing Axsome assets such as AXS-05 and AXS-07 whose pivotal trials led to FDA approvals in 2022–2023 and underpin ongoing 2024 evidence generation. These partnerships drive credibility in CNS disorders and accelerate data accrual. Active KOL advocacy supports guideline consideration and formulary decisions, while joint research may reveal novel indications.

Patient Advocacy and Registries

Patient advocacy groups improve recruitment, retention and real-world insights; ClinicalTrials.gov lists over 420,000 studies, highlighting registry value in matching patients to trials. Collaboration with advocates refines endpoints toward meaningful outcomes and patient-reported measures. Orphanet tracks >6,000 rare disease registries, whose natural history data inform trial design and strengthen market-access dossiers. Advocacy networks also boost disease awareness and adherence support.

Payers and PBMs

Payers and PBMs drive access through value-based and outcomes-sharing frameworks that tie reimbursement to real-world results, shaping coverage and step-edit policies via early engagement. HEOR collaborations establish cost-effectiveness narratives (commonly using $100,000–$150,000 per QALY thresholds) to support formulary placement. Data-sharing agreements improve utilization management and patient persistence, lowering total cost of care; US prescription drug spend was roughly $577B in 2023.

Commercial and Distribution Partners

Commercial partners such as specialty pharmacies, wholesalers, and ex-US licensees extend Axsome’s reach into specialty channels and international markets, while co-promotion alliances accelerate uptake in targeted specialties; specialty medicines accounted for about 55% of US drug spending in 2023 (IQVIA). Third-party logistics providers and HUB services streamline cold-chain logistics, reimbursement support, and patient onboarding to reduce time-to-therapy.

- Specialty pharmacies: channel access and adherence

- Wholesalers: national distribution scale

- Co-promotion: faster specialist adoption

- 3PLs/HUBs: logistics, REMS, patient support

- International licensees: local regs and payers

CROs/CDMOs scale R&D/GMP; specialty meds drive US $577B market, 55% spend

CROs/CDMOs scale R&D and GMP production—global CRO market $60B and CDMO $160B in 2024—reducing capex and accelerating timelines. KOLs/universities validate targets and drive publications for AXS-05/07 (FDA approvals 2022–2023). Payers, PBMs, specialty pharmacies and 3PLs enable access; specialty medicines =55% of US drug spend (2023), US drug spend $577B (2023).

| Partner | Role | 2023/24 metric |

|---|---|---|

| CRO/CDMO | Scale R&D/GMP | $60B/$160B (2024) |

| KOLs/Univ | Evidence & advocacy | FDA approvals 2022–23 |

| Payers/PBMs | Access & VBAs | $577B drug spend (2023) |

| Commercial | Distribution & HUBs | 55% specialty spend (2023) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Axsome that maps all nine BMC blocks with detailed customer segments, channels, value propositions and monetization, plus competitive advantages and SWOT-linked insights for presentations and investor discussions.

Editable one-page Business Model Canvas for Axsome that condenses strategy into a clean, shareable layout—saving hours of formatting, enabling fast executive summaries, supporting team collaboration, and ideal for boardroom reviews or side-by-side comparisons.

Activities

R&D and Clinical Development

Axsome advances discovery, formulation and phase 1–3 clinical trials to de-risk CNS assets; AXS-05 (Auvelity) received FDA approval in August 2022. Biomarker strategy and endpoint selection are tailored to CNS heterogeneity to improve signal detection. Portfolio prioritization weighs risk, time-to-market and unmet need. Continuous interim data monitoring drives go/no-go decisions.

Regulatory Strategy and Submissions

End-to-end engagement with FDA and EMA drives designations and approvals, following PDUFA review timelines (standard 10 months, priority 6 months) and 2024 EMA procedures for MAA interactions. Preparation of INDs, NDAs and MAAs plus structured post-marketing commitments and Phase IV studies are routine. Label negotiation targets optimized positioning and claims to support uptake. Pharmacovigilance planning, including REMS and safety signal monitoring, is integrated into regulatory pathways.

Manufacturing and Quality Management

Scale-up of API and finished-dose manufacturing is managed under stringent QA/QC with formal tech transfer and process validation protocols to transition from pilot to commercial batches. Robust supply-chain risk control, including supplier qualification and dual sourcing, supports on-time supply. Serialization, cold-chain where required, and tight inventory management ensure traceability and product integrity. Continuous process verification monitors stability and manufacturing reliability.

Market Access and Medical Affairs

Axsome drives market access through HEOR and budget‑impact modeling to support pricing and payer negotiations; in 2024 specialty drugs represented ~50% of US drug spend, making robust value dossiers essential. MSL engagement, peer‑reviewed publications and congress presence build the evidence base and KOL advocacy. Treatment‑pathway integration and KAM work with IDNs plus patient services (patient support programs can cut abandonment ~35%) reduce access friction.

- HEOR / BIM for pricing & payers

- MSL, publications, congress presence

- KAM & IDN pathway integration

- Patient services to lower abandonment ~35%

Commercialization and Lifecycle Management

Commercialization and lifecycle management focus on launch planning, targeted field force deployment and omnichannel campaigns initiated in 2024 to drive uptake, supported by indication expansion, label updates and selective reformulations. Real-world evidence programs collect persistence and outcomes data while competitive intelligence shapes differentiation.

- Launch planning: 2024 omnichannel rollouts

- Field force: targeted HCP coverage

- RWE: persistence/outcomes collection

- Lifecycle: label/indication updates

- CI: informs differentiation

CNS pipeline; PDUFA 6–10m, services cut abandonment 35%

Axsome advances CNS discovery to phase 1–3, AXS-05 approved Aug 2022, portfolio prioritization balances risk/time-to-market. Regulatory engagement targets PDUFA 6–10 months and 2024 EMA MAA pathways; IND/NDA/MAA prep plus REMS and PV are routine. Manufacturing scales via tech transfer, dual sourcing and process validation; HEOR, KOLs and patient services (reduce abandonment ~35%) drive access; specialty drugs ~50% of US spend in 2024.

| Metric | 2024 Figure |

|---|---|

| Specialty share of US drug spend | ~50% |

| Patient abandonment reduction (services) | ~35% |

| PDUFA timelines | Priority 6m / Standard 10m |

Delivered as Displayed

Business Model Canvas

The preview you see is the actual Axsome Business Model Canvas, not a mockup—it's a direct snapshot of the final deliverable. When you purchase, you’ll receive this exact, fully editable file (Word and Excel) with all content and pages included, ready to present or customize. No surprises, just the document you previewed.

Description

Unlock the strategic playbook: Complete Business Model Canvas for investors and founders

Unlock Axsome’s strategic playbook with our full Business Model Canvas—clarifying value propositions, revenue levers, partnerships and growth risks in one ready-to-use file. Ideal for investors, advisors, and founders wanting actionable insights; download the complete Canvas to benchmark and build winning strategies.

Partnerships

CROs and CDMOs

CROs and CDMOs let Axsome scale R&D and GMP production without heavy fixed investment; the global CRO market topped $60B in 2024 and the CDMO sector surpassed $160B in 2024, reflecting broad outsourcing adoption. They enable rapid trial startup, wider geographic reach, and GMP-scale manufacturing to accelerate timelines. Strategic vendor selection manages quality and cost, while multi-vendor redundancy cuts supply risk.

Academic and KOL Networks

Universities and KOLs collaborate on target validation, trial design and peer-reviewed publication, reinforcing Axsome assets such as AXS-05 and AXS-07 whose pivotal trials led to FDA approvals in 2022–2023 and underpin ongoing 2024 evidence generation. These partnerships drive credibility in CNS disorders and accelerate data accrual. Active KOL advocacy supports guideline consideration and formulary decisions, while joint research may reveal novel indications.

Patient Advocacy and Registries

Patient advocacy groups improve recruitment, retention and real-world insights; ClinicalTrials.gov lists over 420,000 studies, highlighting registry value in matching patients to trials. Collaboration with advocates refines endpoints toward meaningful outcomes and patient-reported measures. Orphanet tracks >6,000 rare disease registries, whose natural history data inform trial design and strengthen market-access dossiers. Advocacy networks also boost disease awareness and adherence support.

Payers and PBMs

Payers and PBMs drive access through value-based and outcomes-sharing frameworks that tie reimbursement to real-world results, shaping coverage and step-edit policies via early engagement. HEOR collaborations establish cost-effectiveness narratives (commonly using $100,000–$150,000 per QALY thresholds) to support formulary placement. Data-sharing agreements improve utilization management and patient persistence, lowering total cost of care; US prescription drug spend was roughly $577B in 2023.

Commercial and Distribution Partners

Commercial partners such as specialty pharmacies, wholesalers, and ex-US licensees extend Axsome’s reach into specialty channels and international markets, while co-promotion alliances accelerate uptake in targeted specialties; specialty medicines accounted for about 55% of US drug spending in 2023 (IQVIA). Third-party logistics providers and HUB services streamline cold-chain logistics, reimbursement support, and patient onboarding to reduce time-to-therapy.

- Specialty pharmacies: channel access and adherence

- Wholesalers: national distribution scale

- Co-promotion: faster specialist adoption

- 3PLs/HUBs: logistics, REMS, patient support

- International licensees: local regs and payers

CROs/CDMOs scale R&D/GMP; specialty meds drive US $577B market, 55% spend

CROs/CDMOs scale R&D and GMP production—global CRO market $60B and CDMO $160B in 2024—reducing capex and accelerating timelines. KOLs/universities validate targets and drive publications for AXS-05/07 (FDA approvals 2022–2023). Payers, PBMs, specialty pharmacies and 3PLs enable access; specialty medicines =55% of US drug spend (2023), US drug spend $577B (2023).

| Partner | Role | 2023/24 metric |

|---|---|---|

| CRO/CDMO | Scale R&D/GMP | $60B/$160B (2024) |

| KOLs/Univ | Evidence & advocacy | FDA approvals 2022–23 |

| Payers/PBMs | Access & VBAs | $577B drug spend (2023) |

| Commercial | Distribution & HUBs | 55% specialty spend (2023) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Axsome that maps all nine BMC blocks with detailed customer segments, channels, value propositions and monetization, plus competitive advantages and SWOT-linked insights for presentations and investor discussions.

Editable one-page Business Model Canvas for Axsome that condenses strategy into a clean, shareable layout—saving hours of formatting, enabling fast executive summaries, supporting team collaboration, and ideal for boardroom reviews or side-by-side comparisons.

Activities

R&D and Clinical Development

Axsome advances discovery, formulation and phase 1–3 clinical trials to de-risk CNS assets; AXS-05 (Auvelity) received FDA approval in August 2022. Biomarker strategy and endpoint selection are tailored to CNS heterogeneity to improve signal detection. Portfolio prioritization weighs risk, time-to-market and unmet need. Continuous interim data monitoring drives go/no-go decisions.

Regulatory Strategy and Submissions

End-to-end engagement with FDA and EMA drives designations and approvals, following PDUFA review timelines (standard 10 months, priority 6 months) and 2024 EMA procedures for MAA interactions. Preparation of INDs, NDAs and MAAs plus structured post-marketing commitments and Phase IV studies are routine. Label negotiation targets optimized positioning and claims to support uptake. Pharmacovigilance planning, including REMS and safety signal monitoring, is integrated into regulatory pathways.

Manufacturing and Quality Management

Scale-up of API and finished-dose manufacturing is managed under stringent QA/QC with formal tech transfer and process validation protocols to transition from pilot to commercial batches. Robust supply-chain risk control, including supplier qualification and dual sourcing, supports on-time supply. Serialization, cold-chain where required, and tight inventory management ensure traceability and product integrity. Continuous process verification monitors stability and manufacturing reliability.

Market Access and Medical Affairs

Axsome drives market access through HEOR and budget‑impact modeling to support pricing and payer negotiations; in 2024 specialty drugs represented ~50% of US drug spend, making robust value dossiers essential. MSL engagement, peer‑reviewed publications and congress presence build the evidence base and KOL advocacy. Treatment‑pathway integration and KAM work with IDNs plus patient services (patient support programs can cut abandonment ~35%) reduce access friction.

- HEOR / BIM for pricing & payers

- MSL, publications, congress presence

- KAM & IDN pathway integration

- Patient services to lower abandonment ~35%

Commercialization and Lifecycle Management

Commercialization and lifecycle management focus on launch planning, targeted field force deployment and omnichannel campaigns initiated in 2024 to drive uptake, supported by indication expansion, label updates and selective reformulations. Real-world evidence programs collect persistence and outcomes data while competitive intelligence shapes differentiation.

- Launch planning: 2024 omnichannel rollouts

- Field force: targeted HCP coverage

- RWE: persistence/outcomes collection

- Lifecycle: label/indication updates

- CI: informs differentiation

CNS pipeline; PDUFA 6–10m, services cut abandonment 35%

Axsome advances CNS discovery to phase 1–3, AXS-05 approved Aug 2022, portfolio prioritization balances risk/time-to-market. Regulatory engagement targets PDUFA 6–10 months and 2024 EMA MAA pathways; IND/NDA/MAA prep plus REMS and PV are routine. Manufacturing scales via tech transfer, dual sourcing and process validation; HEOR, KOLs and patient services (reduce abandonment ~35%) drive access; specialty drugs ~50% of US spend in 2024.

| Metric | 2024 Figure |

|---|---|

| Specialty share of US drug spend | ~50% |

| Patient abandonment reduction (services) | ~35% |

| PDUFA timelines | Priority 6m / Standard 10m |

Delivered as Displayed

Business Model Canvas

The preview you see is the actual Axsome Business Model Canvas, not a mockup—it's a direct snapshot of the final deliverable. When you purchase, you’ll receive this exact, fully editable file (Word and Excel) with all content and pages included, ready to present or customize. No surprises, just the document you previewed.