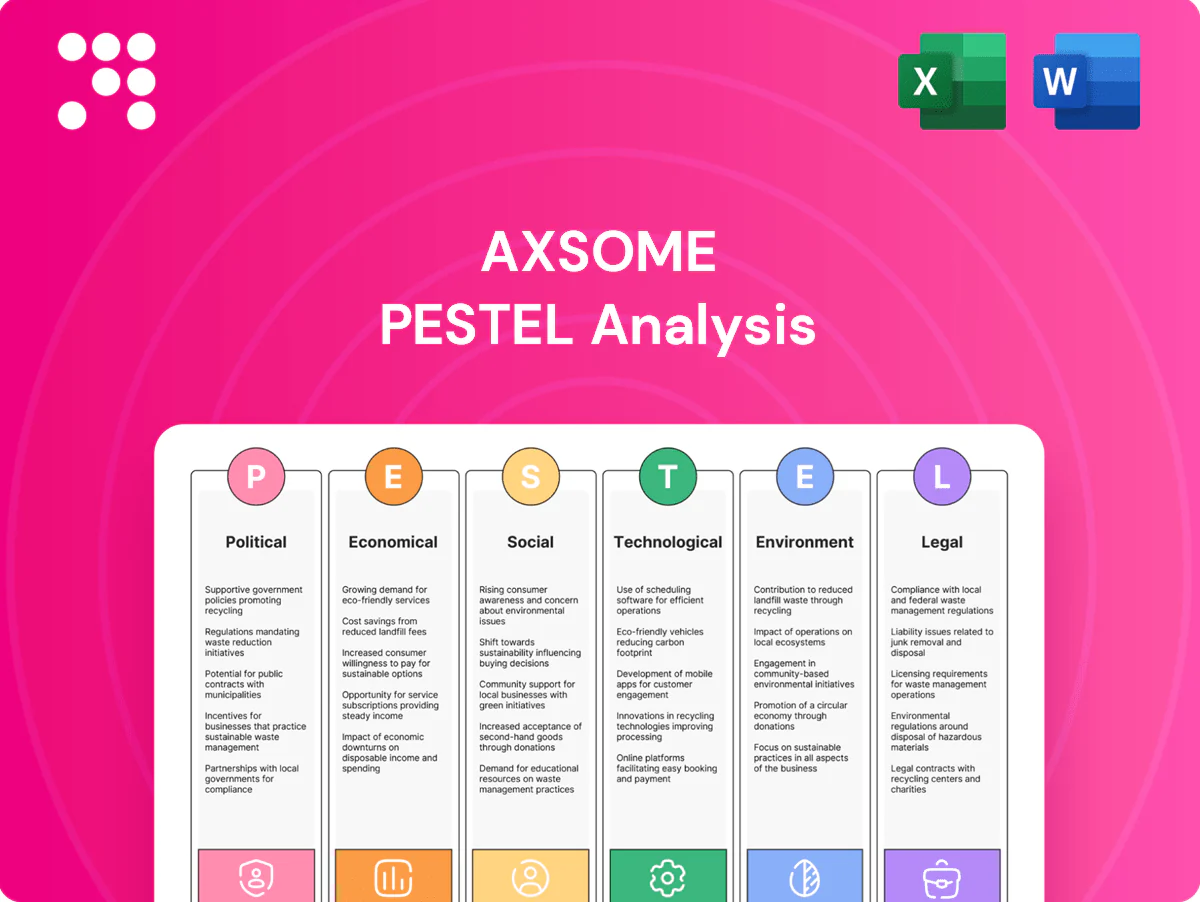

Axsome PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping Axsome’s trajectory in our concise PESTLE overview. This expert snapshot highlights risks and opportunity areas for investors and strategists. Buy the full, editable PESTLE analysis to get detailed, actionable insights and support confident decisions.

Political factors

US FDA policy stability

Regulatory predictability shapes Axsome’s clinical and approval timelines, illustrated by AXS-05 (approved Aug 4, 2022). Stable FDA guidance on CNS endpoints and trial designs reduces execution risk; PDUFA review goals remain 6 months for priority and 10 months standard. Shifts in leadership or advisory priorities can tighten evidentiary standards, while continued PFDD emphasis could streamline interactions.

Government drug pricing agendas

Political momentum for price controls—including Medicare drug price negotiation authorized under the Inflation Reduction Act starting in 2026—can compress Axsome’s launch and lifetime value. Ongoing debates on international reference pricing and cross-border benchmarking add pricing uncertainty. CNS therapies treating millions of patients are often targeted for savings. Robust value frameworks and health-economic data can mitigate reimbursement pressure.

Public R&D funding and incentives

NIH grants (>45B annually) plus orphan incentives (7-year exclusivity, 25% R&D tax credit) and R&D tax credits catalyze CNS innovation. Priority review (≈6-month target vs 10-month standard) and tradable PRVs (valued up to 200–350M) improve capital efficiency. Policy pullbacks could raise Axsome’s cost of capital by multiple hundred basis points. Maintaining unmet-need positioning preserves eligibility and financing optionality.

Trade and supply-chain geopolitics

Tariffs and export controls—such as recent US Commerce Department restrictions on select biotech equipment—raise costs and timing risks for APIs and specialized ingredients, pressuring Axsome’s margin and launch timelines.

Geopolitical tensions can abruptly disrupt CRO/CMO operations abroad, making clinical supply continuity and regulatory filing schedules vulnerable.

Diversified sourcing and strategic onshoring reduce political exposure; contracts must include force majeure, inventory buffers, and clauses for rapid requalification of suppliers.

- tariffs/export-controls: increase cost and lead-time risk

- CRO/CMO disruption: operational and regulatory delays

- sourcing strategy: diversification and onshoring mitigate exposure

- contract protections: force majeure and rapid requalification

Global health policy alignment

Different HTA bodies—NICE, IQWiG, CADTH, PBAC and others—drive pricing and access decisions globally; the EU HTA Regulation (adopted 2021) targets harmonization across 27 member states to streamline joint clinical assessments. Divergence in CNS treatment guidelines across jurisdictions continues to slow uptake of novel therapies. Early payer engagement is routinely used to tailor evidence packages to local HTA and reimbursement requirements.

- HTA influencers: NICE, IQWiG, CADTH, PBAC

- EU HTA Regulation: adopted 2021, 27 member states

- CNS guideline divergence reduces cross-market uptake

- Early payer engagement customizes evidence per market

Predictable regulation and PDUFA vs IRA price pressures compress drug lifetime value

Regulatory predictability (AXS-05 approved Aug 4, 2022) and PDUFA targets (6/10 months) lower execution risk; FDA/HTA shifts can raise evidentiary bar. Medicare negotiation from 2026 under the Inflation Reduction Act and global price-control debates compress lifetime value. NIH funding (~$45.5B FY2024), orphan incentives (7-year exclusivity) and tradable PRVs ($200–350M) support financing despite tariff/export-control risks.

| Factor | Key Data |

|---|---|

| PDUFA | 6/10 months |

| Medicare negotiation | Starts 2026 (IRA) |

| NIH funding | $45.5B FY2024 |

| PRV value | $200–350M |

What is included in the product

Explores how macro-environmental factors uniquely affect Axsome across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, consultants, and investors; delivered in clean, insert-ready format for plans, decks, and reports.

Axsome's PESTLE analysis delivers a clean, visually segmented summary that’s easily editable and shareable, enabling quick alignment across teams, concise insertion into presentations, and efficient risk and market-position discussions during planning sessions.

Economic factors

Capital market cycles

Biotech funding windows dictate trial pacing and runway, with companies often accelerating milestones to hit investor windows; rate hikes — Fed funds ~5.25–5.50% mid‑2025 — raise discount rates and compress valuations. Partnerships and royalty deals provide non‑dilutive cash and hedge equity volatility, while strong clinical data can decouple Axsome’s performance from broader capital‑market weakness.

Healthcare spending resilience

Defensive demand for CNS care supports Axsome revenue durability amid US national health expenditures of about $4.6 trillion in 2023; persistent unmet need in depression and CNS disorders cushions sales volatility. Budget pressures can delay formulary wins or impose step edits, while employer plans—facing average 2023 family premiums near $23,000—scrutinize cost-effectiveness for broad indications. Real-world outcomes can justify premium positioning.

Cost inflation in trials

Rising site fees, increased monitoring and tougher patient recruitment are driving trial cost inflation for Axsome, with per-patient budgets frequently exceeding $50,000 in later‑phase studies. Wage and input inflation compress margins and require protocol tradeoffs. Adaptive designs and decentralized trials can reduce on-site visits and operational overhead, lowering costs. Currency swings, especially a stronger US dollar, increase ex-US development expenses.

Payer mix and reimbursement

Axsome’s net pricing is shaped by commercial versus government mix, with Medicare covering about 64 million beneficiaries in 2024 (CMS) and manufacturer rebates averaging ~26% of list price in 2023 (IQVIA). Rebates, prior authorizations and outcomes-based contracts materially influence realized yield and gross-to-net erosion. Faster time-to-preferred formulary status accelerates uptake, while robust patient support programs reduce abandonment and improve persistence.

- Commercial vs government mix -> net pricing

- Rebates (~26% 2023), prior auth, outcomes contracts -> yield

- Faster preferred status -> faster uptake

- Patient support -> lower abandonment, better persistence

M&A and partnering landscape

Big pharma CNS appetite dictates licensing terms and milestone structures, with strategic partners setting commercial and clinical thresholds that shape Axsome’s deal economics. Competitive dealmaking validates Axsome assets and can provide non-dilutive funding to accelerate its pipeline while antitrust scrutiny in major jurisdictions can delay or reshape large combinations. Structured transactions with co-promotion or commercialization splits allow Axsome to expand reach efficiently without full exits.

- Deal terms set by big pharma

- Competitive deals validate assets

- Antitrust review may slow M&A

- Co-promotion expands reach

Predictable regulation and PDUFA vs IRA price pressures compress drug lifetime value

Biotech funding windows and Fed funds ~5.25–5.50% (mid‑2025) raise discount rates, compressing valuations; partnerships supply non‑dilutive cash while strong clinical data can decouple performance. US health spending ~$4.6T (2023) and Medicare ~64M (2024) shape net pricing; rebates ~26% (2023) and per‑patient late‑phase costs >$50k pressure margins.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| US health spend (2023) | $4.6T |

| Medicare (2024) | ~64M |

| Manufacturer rebates (2023) | ~26% |

| Late‑phase per‑patient cost | >$50k |

What You See Is What You Get

Axsome PESTLE Analysis

The Axsome PESTLE Analysis delivers concise political, economic, social, technological, legal and environmental insights tailored for investors and strategists. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers—this is the finished, downloadable file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping Axsome’s trajectory in our concise PESTLE overview. This expert snapshot highlights risks and opportunity areas for investors and strategists. Buy the full, editable PESTLE analysis to get detailed, actionable insights and support confident decisions.

Political factors

US FDA policy stability

Regulatory predictability shapes Axsome’s clinical and approval timelines, illustrated by AXS-05 (approved Aug 4, 2022). Stable FDA guidance on CNS endpoints and trial designs reduces execution risk; PDUFA review goals remain 6 months for priority and 10 months standard. Shifts in leadership or advisory priorities can tighten evidentiary standards, while continued PFDD emphasis could streamline interactions.

Government drug pricing agendas

Political momentum for price controls—including Medicare drug price negotiation authorized under the Inflation Reduction Act starting in 2026—can compress Axsome’s launch and lifetime value. Ongoing debates on international reference pricing and cross-border benchmarking add pricing uncertainty. CNS therapies treating millions of patients are often targeted for savings. Robust value frameworks and health-economic data can mitigate reimbursement pressure.

Public R&D funding and incentives

NIH grants (>45B annually) plus orphan incentives (7-year exclusivity, 25% R&D tax credit) and R&D tax credits catalyze CNS innovation. Priority review (≈6-month target vs 10-month standard) and tradable PRVs (valued up to 200–350M) improve capital efficiency. Policy pullbacks could raise Axsome’s cost of capital by multiple hundred basis points. Maintaining unmet-need positioning preserves eligibility and financing optionality.

Trade and supply-chain geopolitics

Tariffs and export controls—such as recent US Commerce Department restrictions on select biotech equipment—raise costs and timing risks for APIs and specialized ingredients, pressuring Axsome’s margin and launch timelines.

Geopolitical tensions can abruptly disrupt CRO/CMO operations abroad, making clinical supply continuity and regulatory filing schedules vulnerable.

Diversified sourcing and strategic onshoring reduce political exposure; contracts must include force majeure, inventory buffers, and clauses for rapid requalification of suppliers.

- tariffs/export-controls: increase cost and lead-time risk

- CRO/CMO disruption: operational and regulatory delays

- sourcing strategy: diversification and onshoring mitigate exposure

- contract protections: force majeure and rapid requalification

Global health policy alignment

Different HTA bodies—NICE, IQWiG, CADTH, PBAC and others—drive pricing and access decisions globally; the EU HTA Regulation (adopted 2021) targets harmonization across 27 member states to streamline joint clinical assessments. Divergence in CNS treatment guidelines across jurisdictions continues to slow uptake of novel therapies. Early payer engagement is routinely used to tailor evidence packages to local HTA and reimbursement requirements.

- HTA influencers: NICE, IQWiG, CADTH, PBAC

- EU HTA Regulation: adopted 2021, 27 member states

- CNS guideline divergence reduces cross-market uptake

- Early payer engagement customizes evidence per market

Predictable regulation and PDUFA vs IRA price pressures compress drug lifetime value

Regulatory predictability (AXS-05 approved Aug 4, 2022) and PDUFA targets (6/10 months) lower execution risk; FDA/HTA shifts can raise evidentiary bar. Medicare negotiation from 2026 under the Inflation Reduction Act and global price-control debates compress lifetime value. NIH funding (~$45.5B FY2024), orphan incentives (7-year exclusivity) and tradable PRVs ($200–350M) support financing despite tariff/export-control risks.

| Factor | Key Data |

|---|---|

| PDUFA | 6/10 months |

| Medicare negotiation | Starts 2026 (IRA) |

| NIH funding | $45.5B FY2024 |

| PRV value | $200–350M |

What is included in the product

Explores how macro-environmental factors uniquely affect Axsome across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, consultants, and investors; delivered in clean, insert-ready format for plans, decks, and reports.

Axsome's PESTLE analysis delivers a clean, visually segmented summary that’s easily editable and shareable, enabling quick alignment across teams, concise insertion into presentations, and efficient risk and market-position discussions during planning sessions.

Economic factors

Capital market cycles

Biotech funding windows dictate trial pacing and runway, with companies often accelerating milestones to hit investor windows; rate hikes — Fed funds ~5.25–5.50% mid‑2025 — raise discount rates and compress valuations. Partnerships and royalty deals provide non‑dilutive cash and hedge equity volatility, while strong clinical data can decouple Axsome’s performance from broader capital‑market weakness.

Healthcare spending resilience

Defensive demand for CNS care supports Axsome revenue durability amid US national health expenditures of about $4.6 trillion in 2023; persistent unmet need in depression and CNS disorders cushions sales volatility. Budget pressures can delay formulary wins or impose step edits, while employer plans—facing average 2023 family premiums near $23,000—scrutinize cost-effectiveness for broad indications. Real-world outcomes can justify premium positioning.

Cost inflation in trials

Rising site fees, increased monitoring and tougher patient recruitment are driving trial cost inflation for Axsome, with per-patient budgets frequently exceeding $50,000 in later‑phase studies. Wage and input inflation compress margins and require protocol tradeoffs. Adaptive designs and decentralized trials can reduce on-site visits and operational overhead, lowering costs. Currency swings, especially a stronger US dollar, increase ex-US development expenses.

Payer mix and reimbursement

Axsome’s net pricing is shaped by commercial versus government mix, with Medicare covering about 64 million beneficiaries in 2024 (CMS) and manufacturer rebates averaging ~26% of list price in 2023 (IQVIA). Rebates, prior authorizations and outcomes-based contracts materially influence realized yield and gross-to-net erosion. Faster time-to-preferred formulary status accelerates uptake, while robust patient support programs reduce abandonment and improve persistence.

- Commercial vs government mix -> net pricing

- Rebates (~26% 2023), prior auth, outcomes contracts -> yield

- Faster preferred status -> faster uptake

- Patient support -> lower abandonment, better persistence

M&A and partnering landscape

Big pharma CNS appetite dictates licensing terms and milestone structures, with strategic partners setting commercial and clinical thresholds that shape Axsome’s deal economics. Competitive dealmaking validates Axsome assets and can provide non-dilutive funding to accelerate its pipeline while antitrust scrutiny in major jurisdictions can delay or reshape large combinations. Structured transactions with co-promotion or commercialization splits allow Axsome to expand reach efficiently without full exits.

- Deal terms set by big pharma

- Competitive deals validate assets

- Antitrust review may slow M&A

- Co-promotion expands reach

Predictable regulation and PDUFA vs IRA price pressures compress drug lifetime value

Biotech funding windows and Fed funds ~5.25–5.50% (mid‑2025) raise discount rates, compressing valuations; partnerships supply non‑dilutive cash while strong clinical data can decouple performance. US health spending ~$4.6T (2023) and Medicare ~64M (2024) shape net pricing; rebates ~26% (2023) and per‑patient late‑phase costs >$50k pressure margins.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| US health spend (2023) | $4.6T |

| Medicare (2024) | ~64M |

| Manufacturer rebates (2023) | ~26% |

| Late‑phase per‑patient cost | >$50k |

What You See Is What You Get

Axsome PESTLE Analysis

The Axsome PESTLE Analysis delivers concise political, economic, social, technological, legal and environmental insights tailored for investors and strategists. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers—this is the finished, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping Axsome’s trajectory in our concise PESTLE overview. This expert snapshot highlights risks and opportunity areas for investors and strategists. Buy the full, editable PESTLE analysis to get detailed, actionable insights and support confident decisions.

Political factors

US FDA policy stability

Regulatory predictability shapes Axsome’s clinical and approval timelines, illustrated by AXS-05 (approved Aug 4, 2022). Stable FDA guidance on CNS endpoints and trial designs reduces execution risk; PDUFA review goals remain 6 months for priority and 10 months standard. Shifts in leadership or advisory priorities can tighten evidentiary standards, while continued PFDD emphasis could streamline interactions.

Government drug pricing agendas

Political momentum for price controls—including Medicare drug price negotiation authorized under the Inflation Reduction Act starting in 2026—can compress Axsome’s launch and lifetime value. Ongoing debates on international reference pricing and cross-border benchmarking add pricing uncertainty. CNS therapies treating millions of patients are often targeted for savings. Robust value frameworks and health-economic data can mitigate reimbursement pressure.

Public R&D funding and incentives

NIH grants (>45B annually) plus orphan incentives (7-year exclusivity, 25% R&D tax credit) and R&D tax credits catalyze CNS innovation. Priority review (≈6-month target vs 10-month standard) and tradable PRVs (valued up to 200–350M) improve capital efficiency. Policy pullbacks could raise Axsome’s cost of capital by multiple hundred basis points. Maintaining unmet-need positioning preserves eligibility and financing optionality.

Trade and supply-chain geopolitics

Tariffs and export controls—such as recent US Commerce Department restrictions on select biotech equipment—raise costs and timing risks for APIs and specialized ingredients, pressuring Axsome’s margin and launch timelines.

Geopolitical tensions can abruptly disrupt CRO/CMO operations abroad, making clinical supply continuity and regulatory filing schedules vulnerable.

Diversified sourcing and strategic onshoring reduce political exposure; contracts must include force majeure, inventory buffers, and clauses for rapid requalification of suppliers.

- tariffs/export-controls: increase cost and lead-time risk

- CRO/CMO disruption: operational and regulatory delays

- sourcing strategy: diversification and onshoring mitigate exposure

- contract protections: force majeure and rapid requalification

Global health policy alignment

Different HTA bodies—NICE, IQWiG, CADTH, PBAC and others—drive pricing and access decisions globally; the EU HTA Regulation (adopted 2021) targets harmonization across 27 member states to streamline joint clinical assessments. Divergence in CNS treatment guidelines across jurisdictions continues to slow uptake of novel therapies. Early payer engagement is routinely used to tailor evidence packages to local HTA and reimbursement requirements.

- HTA influencers: NICE, IQWiG, CADTH, PBAC

- EU HTA Regulation: adopted 2021, 27 member states

- CNS guideline divergence reduces cross-market uptake

- Early payer engagement customizes evidence per market

Predictable regulation and PDUFA vs IRA price pressures compress drug lifetime value

Regulatory predictability (AXS-05 approved Aug 4, 2022) and PDUFA targets (6/10 months) lower execution risk; FDA/HTA shifts can raise evidentiary bar. Medicare negotiation from 2026 under the Inflation Reduction Act and global price-control debates compress lifetime value. NIH funding (~$45.5B FY2024), orphan incentives (7-year exclusivity) and tradable PRVs ($200–350M) support financing despite tariff/export-control risks.

| Factor | Key Data |

|---|---|

| PDUFA | 6/10 months |

| Medicare negotiation | Starts 2026 (IRA) |

| NIH funding | $45.5B FY2024 |

| PRV value | $200–350M |

What is included in the product

Explores how macro-environmental factors uniquely affect Axsome across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, consultants, and investors; delivered in clean, insert-ready format for plans, decks, and reports.

Axsome's PESTLE analysis delivers a clean, visually segmented summary that’s easily editable and shareable, enabling quick alignment across teams, concise insertion into presentations, and efficient risk and market-position discussions during planning sessions.

Economic factors

Capital market cycles

Biotech funding windows dictate trial pacing and runway, with companies often accelerating milestones to hit investor windows; rate hikes — Fed funds ~5.25–5.50% mid‑2025 — raise discount rates and compress valuations. Partnerships and royalty deals provide non‑dilutive cash and hedge equity volatility, while strong clinical data can decouple Axsome’s performance from broader capital‑market weakness.

Healthcare spending resilience

Defensive demand for CNS care supports Axsome revenue durability amid US national health expenditures of about $4.6 trillion in 2023; persistent unmet need in depression and CNS disorders cushions sales volatility. Budget pressures can delay formulary wins or impose step edits, while employer plans—facing average 2023 family premiums near $23,000—scrutinize cost-effectiveness for broad indications. Real-world outcomes can justify premium positioning.

Cost inflation in trials

Rising site fees, increased monitoring and tougher patient recruitment are driving trial cost inflation for Axsome, with per-patient budgets frequently exceeding $50,000 in later‑phase studies. Wage and input inflation compress margins and require protocol tradeoffs. Adaptive designs and decentralized trials can reduce on-site visits and operational overhead, lowering costs. Currency swings, especially a stronger US dollar, increase ex-US development expenses.

Payer mix and reimbursement

Axsome’s net pricing is shaped by commercial versus government mix, with Medicare covering about 64 million beneficiaries in 2024 (CMS) and manufacturer rebates averaging ~26% of list price in 2023 (IQVIA). Rebates, prior authorizations and outcomes-based contracts materially influence realized yield and gross-to-net erosion. Faster time-to-preferred formulary status accelerates uptake, while robust patient support programs reduce abandonment and improve persistence.

- Commercial vs government mix -> net pricing

- Rebates (~26% 2023), prior auth, outcomes contracts -> yield

- Faster preferred status -> faster uptake

- Patient support -> lower abandonment, better persistence

M&A and partnering landscape

Big pharma CNS appetite dictates licensing terms and milestone structures, with strategic partners setting commercial and clinical thresholds that shape Axsome’s deal economics. Competitive dealmaking validates Axsome assets and can provide non-dilutive funding to accelerate its pipeline while antitrust scrutiny in major jurisdictions can delay or reshape large combinations. Structured transactions with co-promotion or commercialization splits allow Axsome to expand reach efficiently without full exits.

- Deal terms set by big pharma

- Competitive deals validate assets

- Antitrust review may slow M&A

- Co-promotion expands reach

Predictable regulation and PDUFA vs IRA price pressures compress drug lifetime value

Biotech funding windows and Fed funds ~5.25–5.50% (mid‑2025) raise discount rates, compressing valuations; partnerships supply non‑dilutive cash while strong clinical data can decouple performance. US health spending ~$4.6T (2023) and Medicare ~64M (2024) shape net pricing; rebates ~26% (2023) and per‑patient late‑phase costs >$50k pressure margins.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| US health spend (2023) | $4.6T |

| Medicare (2024) | ~64M |

| Manufacturer rebates (2023) | ~26% |

| Late‑phase per‑patient cost | >$50k |

What You See Is What You Get

Axsome PESTLE Analysis

The Axsome PESTLE Analysis delivers concise political, economic, social, technological, legal and environmental insights tailored for investors and strategists. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers—this is the finished, downloadable file.