Ayr Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Ayr’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute risk, and barriers to entry shaping its market position. This brief exposes key pressures but only hints at strategic implications and quantified force ratings. Unlock the full Porter's Five Forces Analysis for Ayr to get force-by-force ratings, visuals, and actionable recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Vertical integration dampens leverage

AYR’s vertical integration—spanning cultivation, processing and retail—reduces reliance on external biomass suppliers and limits their ability to dictate terms; as of 2024 AYR operated over 160 retail locations, supporting internal offtake. Gaps in capacity or new market entries can still force purchases from third‑party wholesalers. In those scenarios bargaining power shifts to licensed cultivators holding scarce surplus, who can command premium pricing.

Commoditized inputs, niche specialties

Most inputs—fertilizers, lighting, HVAC, packaging—are commoditized and widely available, keeping supplier power low; fertilizer prices fell from 2022 peaks and remained volatile into 2024. Niche suppliers of proprietary genetics, IP licenses, or premium packaging can exert greater leverage through limited supply. Switching costs for commodities are modest, but proprietary strains carry higher technical and contractual switching costs. Tight contract terms and long lead times can magnify bottlenecks.

Regulatory constraints narrow options

State-by-state rules narrow supplier pools: 38 states had medical cannabis programs and 23 allowed adult-use by 2024, with many jurisdictions restricting who may supply product and inputs. Approved-vendor lists and varying testing standards limit substitutions and raise supplier leverage. Extensive compliance paperwork and provenance documentation increase switching costs. The effect is intensified in tightly regulated medical markets.

Scale buying moderates pricing

AYR’s multi-state scale enables bulk purchasing and negotiated discounts, shifting pricing leverage away from suppliers; volume commitments and multi-year contracts further constrain supplier bargaining power, though new markets with limited store counts weaken this effect until scale accumulates.

- scale: multi-state presence

- contracts: volume & multi-year

- procurement: consolidated, standardized

- limitation: smaller/new markets dilute advantage

Logistics and lead-time risk

Long lead times for equipment, child-resistant packaging, and lab capacity (often exceeding 24 weeks in 2024) temporarily raise supplier power; product-launch demand spikes can double short-term dependency and backlogs. Nearshoring or dual-sourcing reduces single-supplier leverage, while inventory buffers mitigate stockouts but can increase working capital by roughly 15%.

- Lead times: >24 weeks

- Launch spikes: demand ×2

- Mitigation: nearshoring/dual-sourcing

- Cost: inventory +≈15% WC

Integration and 160+ stores lower supplier sway; biomass shortages increase risk

AYR’s vertical integration and >160 retail locations (2024) lower supplier leverage, but third‑party biomass suppliers gain power in capacity gaps. Commoditized inputs keep power low; proprietary genetics/IP and approved‑vendor rules in 38 medical/23 adult‑use states raise supplier leverage. Long lead times (>24 weeks) and launch spikes double dependency; inventory buffers add ≈15% working capital.

| Metric | 2024 |

|---|---|

| Retail locations | 160+ |

| States (medical/adult) | 38 / 23 |

| Lead times | >24 weeks |

| WC impact | +≈15% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored exclusively for Ayr, analyzing its position within the competitive landscape and identifying disruptive threats and substitutes. Fully editable Word format—use in investor materials, strategy decks, or academic projects.

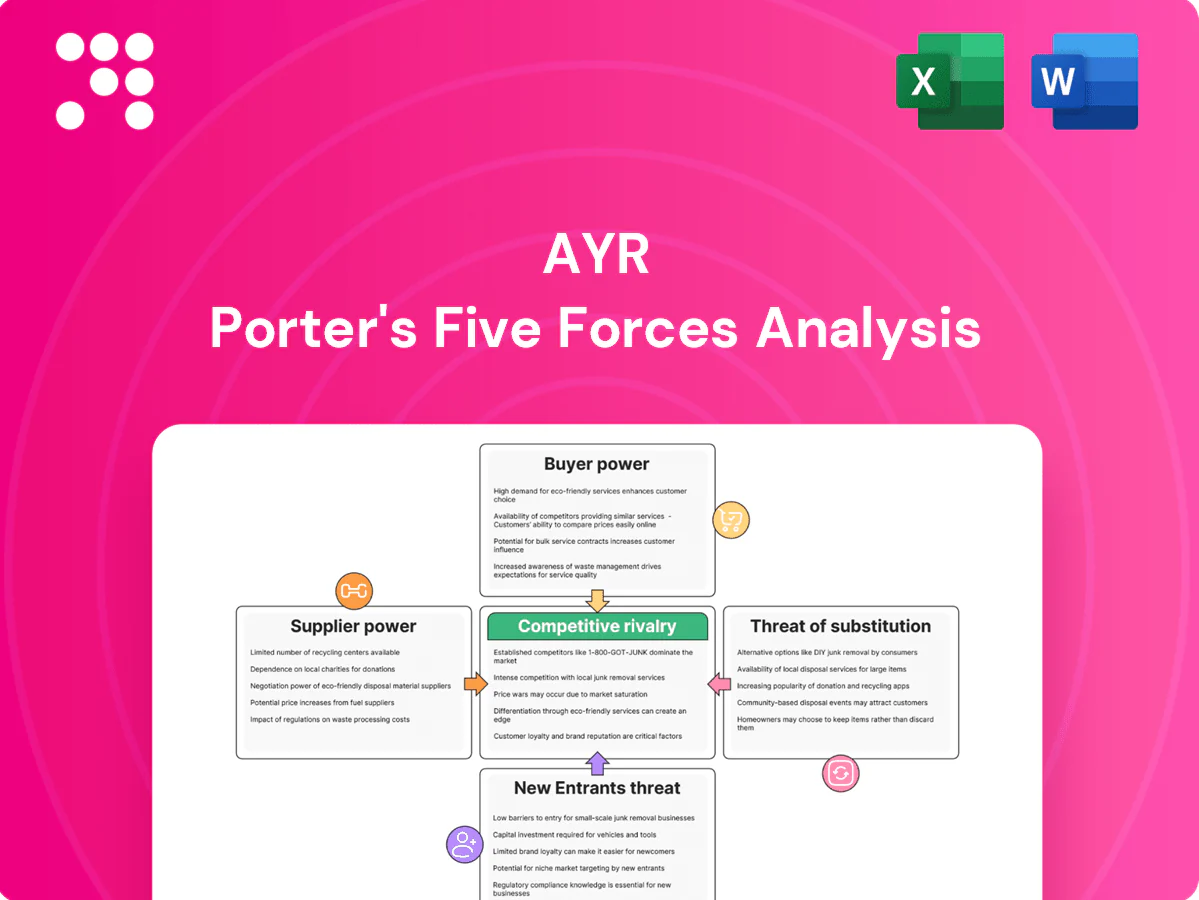

Ayr Porter's Five Forces delivers a clean, one-sheet summary with customizable pressure levels and an instant spider chart, so teams can quickly diagnose competitive stress and slot insights straight into pitch decks or dashboards without complex code.

Customers Bargaining Power

Fragmented but price-sensitive consumers

Retail consumers are numerous and fragmented, so individual bargaining power remains low; U.S. legal cannabis sales topped roughly $30B in 2023 (BDSA), highlighting broad demand. Rising price compression and 2024 CPI inflation around 3.4% (BLS) have increased price sensitivity. Switching costs are minimal across nearby dispensaries, making promotions and loyalty programs essential to retain traffic and preserve margins.

Illicit and hemp-THC alternatives

Unlicensed markets and hemp-derived THC alternatives erode pricing power as illicit/Shelf delta-8 products often retail 20–30% below regulated adult-use prices, forcing customers to shop outside legal channels. Buyers' ability to choose cheaper options strengthens their indirect negotiating leverage, compelling legal operators to compete on proven safety, testing transparency and loyalty programs. Regulatory enforcement varies by state; as of 2024 more than 20 states have restricted hemp-derived THC, which directly shapes the scale of this downward pressure.

Wholesale buyers in limited-license states

In limited-license states where AYR wholesales, licensed retailers wield significant leverage when supply outstrips demand, negotiating deeper discounts and consignment arrangements to protect margins.

Brand loyalty and experience offset

Strong brands, consistent quality and differentiated in-store experience materially reduce buyer power; membership and delivery programs boost stickiness, with 2024 McKinsey data showing personalization can raise revenues 10–15%. Premium formats and proprietary strains create perceived switching costs and support higher margins; data-driven local assortments increase basket relevance and repeat purchases.

- Brand strength: lowers price sensitivity

- Membership/delivery: increases retention

- Proprietary products: raise switching costs

- Data-led assortments: tailor value to local demand

Information transparency

Information transparency—menu pricing, reviews and third-party analytics—gives buyers clearer SKU comparisons; BDSA data shows US legal cannabis sales topped about 26 billion USD in 2023, amplifying price sensitivity. Transparent potency and terpene metrics standardize quality, compressing margins on undifferentiated products, so AYR must innovate and segment to preserve pricing.

- Menu pricing: increased visibility

- Potency/terpenes: easier SKU comparison

- Margin pressure: commoditization

- Strategy: innovate, segment, premiumize

Price-Sensitive Buyers and Cheap Hemp Supply Squeeze Margins; Brands Win with Loyalty

Buyers are numerous and price-sensitive; US legal cannabis sales ≈30B USD in 2023 with 2024 CPI ~3.4% (BLS). Low switching costs and nearby dispensaries raise promotional pressure. Hemp-derived/illicit options 20–30% cheaper and >20 states limited hemp THC in 2024, compressing margins. Strong brands, memberships and proprietary SKUs offset buyer power.

| Metric | Value |

|---|---|

| US legal sales (2023) | ~30B USD |

| CPI (2024) | ~3.4% |

| Illicit/HEMP price delta | 20–30% lower |

| States restricting hemp-THC (2024) | >20 |

What You See Is What You Get

Ayr Porter's Five Forces Analysis

This preview shows the exact Ayr Porter’s Five Forces Analysis document you’ll receive—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use upon purchase. What you see here is precisely the deliverable you’ll get instantly after payment.

A Must-Have Tool for Decision-Makers

Ayr’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute risk, and barriers to entry shaping its market position. This brief exposes key pressures but only hints at strategic implications and quantified force ratings. Unlock the full Porter's Five Forces Analysis for Ayr to get force-by-force ratings, visuals, and actionable recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Vertical integration dampens leverage

AYR’s vertical integration—spanning cultivation, processing and retail—reduces reliance on external biomass suppliers and limits their ability to dictate terms; as of 2024 AYR operated over 160 retail locations, supporting internal offtake. Gaps in capacity or new market entries can still force purchases from third‑party wholesalers. In those scenarios bargaining power shifts to licensed cultivators holding scarce surplus, who can command premium pricing.

Commoditized inputs, niche specialties

Most inputs—fertilizers, lighting, HVAC, packaging—are commoditized and widely available, keeping supplier power low; fertilizer prices fell from 2022 peaks and remained volatile into 2024. Niche suppliers of proprietary genetics, IP licenses, or premium packaging can exert greater leverage through limited supply. Switching costs for commodities are modest, but proprietary strains carry higher technical and contractual switching costs. Tight contract terms and long lead times can magnify bottlenecks.

Regulatory constraints narrow options

State-by-state rules narrow supplier pools: 38 states had medical cannabis programs and 23 allowed adult-use by 2024, with many jurisdictions restricting who may supply product and inputs. Approved-vendor lists and varying testing standards limit substitutions and raise supplier leverage. Extensive compliance paperwork and provenance documentation increase switching costs. The effect is intensified in tightly regulated medical markets.

Scale buying moderates pricing

AYR’s multi-state scale enables bulk purchasing and negotiated discounts, shifting pricing leverage away from suppliers; volume commitments and multi-year contracts further constrain supplier bargaining power, though new markets with limited store counts weaken this effect until scale accumulates.

- scale: multi-state presence

- contracts: volume & multi-year

- procurement: consolidated, standardized

- limitation: smaller/new markets dilute advantage

Logistics and lead-time risk

Long lead times for equipment, child-resistant packaging, and lab capacity (often exceeding 24 weeks in 2024) temporarily raise supplier power; product-launch demand spikes can double short-term dependency and backlogs. Nearshoring or dual-sourcing reduces single-supplier leverage, while inventory buffers mitigate stockouts but can increase working capital by roughly 15%.

- Lead times: >24 weeks

- Launch spikes: demand ×2

- Mitigation: nearshoring/dual-sourcing

- Cost: inventory +≈15% WC

Integration and 160+ stores lower supplier sway; biomass shortages increase risk

AYR’s vertical integration and >160 retail locations (2024) lower supplier leverage, but third‑party biomass suppliers gain power in capacity gaps. Commoditized inputs keep power low; proprietary genetics/IP and approved‑vendor rules in 38 medical/23 adult‑use states raise supplier leverage. Long lead times (>24 weeks) and launch spikes double dependency; inventory buffers add ≈15% working capital.

| Metric | 2024 |

|---|---|

| Retail locations | 160+ |

| States (medical/adult) | 38 / 23 |

| Lead times | >24 weeks |

| WC impact | +≈15% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored exclusively for Ayr, analyzing its position within the competitive landscape and identifying disruptive threats and substitutes. Fully editable Word format—use in investor materials, strategy decks, or academic projects.

Ayr Porter's Five Forces delivers a clean, one-sheet summary with customizable pressure levels and an instant spider chart, so teams can quickly diagnose competitive stress and slot insights straight into pitch decks or dashboards without complex code.

Customers Bargaining Power

Fragmented but price-sensitive consumers

Retail consumers are numerous and fragmented, so individual bargaining power remains low; U.S. legal cannabis sales topped roughly $30B in 2023 (BDSA), highlighting broad demand. Rising price compression and 2024 CPI inflation around 3.4% (BLS) have increased price sensitivity. Switching costs are minimal across nearby dispensaries, making promotions and loyalty programs essential to retain traffic and preserve margins.

Illicit and hemp-THC alternatives

Unlicensed markets and hemp-derived THC alternatives erode pricing power as illicit/Shelf delta-8 products often retail 20–30% below regulated adult-use prices, forcing customers to shop outside legal channels. Buyers' ability to choose cheaper options strengthens their indirect negotiating leverage, compelling legal operators to compete on proven safety, testing transparency and loyalty programs. Regulatory enforcement varies by state; as of 2024 more than 20 states have restricted hemp-derived THC, which directly shapes the scale of this downward pressure.

Wholesale buyers in limited-license states

In limited-license states where AYR wholesales, licensed retailers wield significant leverage when supply outstrips demand, negotiating deeper discounts and consignment arrangements to protect margins.

Brand loyalty and experience offset

Strong brands, consistent quality and differentiated in-store experience materially reduce buyer power; membership and delivery programs boost stickiness, with 2024 McKinsey data showing personalization can raise revenues 10–15%. Premium formats and proprietary strains create perceived switching costs and support higher margins; data-driven local assortments increase basket relevance and repeat purchases.

- Brand strength: lowers price sensitivity

- Membership/delivery: increases retention

- Proprietary products: raise switching costs

- Data-led assortments: tailor value to local demand

Information transparency

Information transparency—menu pricing, reviews and third-party analytics—gives buyers clearer SKU comparisons; BDSA data shows US legal cannabis sales topped about 26 billion USD in 2023, amplifying price sensitivity. Transparent potency and terpene metrics standardize quality, compressing margins on undifferentiated products, so AYR must innovate and segment to preserve pricing.

- Menu pricing: increased visibility

- Potency/terpenes: easier SKU comparison

- Margin pressure: commoditization

- Strategy: innovate, segment, premiumize

Price-Sensitive Buyers and Cheap Hemp Supply Squeeze Margins; Brands Win with Loyalty

Buyers are numerous and price-sensitive; US legal cannabis sales ≈30B USD in 2023 with 2024 CPI ~3.4% (BLS). Low switching costs and nearby dispensaries raise promotional pressure. Hemp-derived/illicit options 20–30% cheaper and >20 states limited hemp THC in 2024, compressing margins. Strong brands, memberships and proprietary SKUs offset buyer power.

| Metric | Value |

|---|---|

| US legal sales (2023) | ~30B USD |

| CPI (2024) | ~3.4% |

| Illicit/HEMP price delta | 20–30% lower |

| States restricting hemp-THC (2024) | >20 |

What You See Is What You Get

Ayr Porter's Five Forces Analysis

This preview shows the exact Ayr Porter’s Five Forces Analysis document you’ll receive—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use upon purchase. What you see here is precisely the deliverable you’ll get instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Ayr’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute risk, and barriers to entry shaping its market position. This brief exposes key pressures but only hints at strategic implications and quantified force ratings. Unlock the full Porter's Five Forces Analysis for Ayr to get force-by-force ratings, visuals, and actionable recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Vertical integration dampens leverage

AYR’s vertical integration—spanning cultivation, processing and retail—reduces reliance on external biomass suppliers and limits their ability to dictate terms; as of 2024 AYR operated over 160 retail locations, supporting internal offtake. Gaps in capacity or new market entries can still force purchases from third‑party wholesalers. In those scenarios bargaining power shifts to licensed cultivators holding scarce surplus, who can command premium pricing.

Commoditized inputs, niche specialties

Most inputs—fertilizers, lighting, HVAC, packaging—are commoditized and widely available, keeping supplier power low; fertilizer prices fell from 2022 peaks and remained volatile into 2024. Niche suppliers of proprietary genetics, IP licenses, or premium packaging can exert greater leverage through limited supply. Switching costs for commodities are modest, but proprietary strains carry higher technical and contractual switching costs. Tight contract terms and long lead times can magnify bottlenecks.

Regulatory constraints narrow options

State-by-state rules narrow supplier pools: 38 states had medical cannabis programs and 23 allowed adult-use by 2024, with many jurisdictions restricting who may supply product and inputs. Approved-vendor lists and varying testing standards limit substitutions and raise supplier leverage. Extensive compliance paperwork and provenance documentation increase switching costs. The effect is intensified in tightly regulated medical markets.

Scale buying moderates pricing

AYR’s multi-state scale enables bulk purchasing and negotiated discounts, shifting pricing leverage away from suppliers; volume commitments and multi-year contracts further constrain supplier bargaining power, though new markets with limited store counts weaken this effect until scale accumulates.

- scale: multi-state presence

- contracts: volume & multi-year

- procurement: consolidated, standardized

- limitation: smaller/new markets dilute advantage

Logistics and lead-time risk

Long lead times for equipment, child-resistant packaging, and lab capacity (often exceeding 24 weeks in 2024) temporarily raise supplier power; product-launch demand spikes can double short-term dependency and backlogs. Nearshoring or dual-sourcing reduces single-supplier leverage, while inventory buffers mitigate stockouts but can increase working capital by roughly 15%.

- Lead times: >24 weeks

- Launch spikes: demand ×2

- Mitigation: nearshoring/dual-sourcing

- Cost: inventory +≈15% WC

Integration and 160+ stores lower supplier sway; biomass shortages increase risk

AYR’s vertical integration and >160 retail locations (2024) lower supplier leverage, but third‑party biomass suppliers gain power in capacity gaps. Commoditized inputs keep power low; proprietary genetics/IP and approved‑vendor rules in 38 medical/23 adult‑use states raise supplier leverage. Long lead times (>24 weeks) and launch spikes double dependency; inventory buffers add ≈15% working capital.

| Metric | 2024 |

|---|---|

| Retail locations | 160+ |

| States (medical/adult) | 38 / 23 |

| Lead times | >24 weeks |

| WC impact | +≈15% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored exclusively for Ayr, analyzing its position within the competitive landscape and identifying disruptive threats and substitutes. Fully editable Word format—use in investor materials, strategy decks, or academic projects.

Ayr Porter's Five Forces delivers a clean, one-sheet summary with customizable pressure levels and an instant spider chart, so teams can quickly diagnose competitive stress and slot insights straight into pitch decks or dashboards without complex code.

Customers Bargaining Power

Fragmented but price-sensitive consumers

Retail consumers are numerous and fragmented, so individual bargaining power remains low; U.S. legal cannabis sales topped roughly $30B in 2023 (BDSA), highlighting broad demand. Rising price compression and 2024 CPI inflation around 3.4% (BLS) have increased price sensitivity. Switching costs are minimal across nearby dispensaries, making promotions and loyalty programs essential to retain traffic and preserve margins.

Illicit and hemp-THC alternatives

Unlicensed markets and hemp-derived THC alternatives erode pricing power as illicit/Shelf delta-8 products often retail 20–30% below regulated adult-use prices, forcing customers to shop outside legal channels. Buyers' ability to choose cheaper options strengthens their indirect negotiating leverage, compelling legal operators to compete on proven safety, testing transparency and loyalty programs. Regulatory enforcement varies by state; as of 2024 more than 20 states have restricted hemp-derived THC, which directly shapes the scale of this downward pressure.

Wholesale buyers in limited-license states

In limited-license states where AYR wholesales, licensed retailers wield significant leverage when supply outstrips demand, negotiating deeper discounts and consignment arrangements to protect margins.

Brand loyalty and experience offset

Strong brands, consistent quality and differentiated in-store experience materially reduce buyer power; membership and delivery programs boost stickiness, with 2024 McKinsey data showing personalization can raise revenues 10–15%. Premium formats and proprietary strains create perceived switching costs and support higher margins; data-driven local assortments increase basket relevance and repeat purchases.

- Brand strength: lowers price sensitivity

- Membership/delivery: increases retention

- Proprietary products: raise switching costs

- Data-led assortments: tailor value to local demand

Information transparency

Information transparency—menu pricing, reviews and third-party analytics—gives buyers clearer SKU comparisons; BDSA data shows US legal cannabis sales topped about 26 billion USD in 2023, amplifying price sensitivity. Transparent potency and terpene metrics standardize quality, compressing margins on undifferentiated products, so AYR must innovate and segment to preserve pricing.

- Menu pricing: increased visibility

- Potency/terpenes: easier SKU comparison

- Margin pressure: commoditization

- Strategy: innovate, segment, premiumize

Price-Sensitive Buyers and Cheap Hemp Supply Squeeze Margins; Brands Win with Loyalty

Buyers are numerous and price-sensitive; US legal cannabis sales ≈30B USD in 2023 with 2024 CPI ~3.4% (BLS). Low switching costs and nearby dispensaries raise promotional pressure. Hemp-derived/illicit options 20–30% cheaper and >20 states limited hemp THC in 2024, compressing margins. Strong brands, memberships and proprietary SKUs offset buyer power.

| Metric | Value |

|---|---|

| US legal sales (2023) | ~30B USD |

| CPI (2024) | ~3.4% |

| Illicit/HEMP price delta | 20–30% lower |

| States restricting hemp-THC (2024) | >20 |

What You See Is What You Get

Ayr Porter's Five Forces Analysis

This preview shows the exact Ayr Porter’s Five Forces Analysis document you’ll receive—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use upon purchase. What you see here is precisely the deliverable you’ll get instantly after payment.