Azbil Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

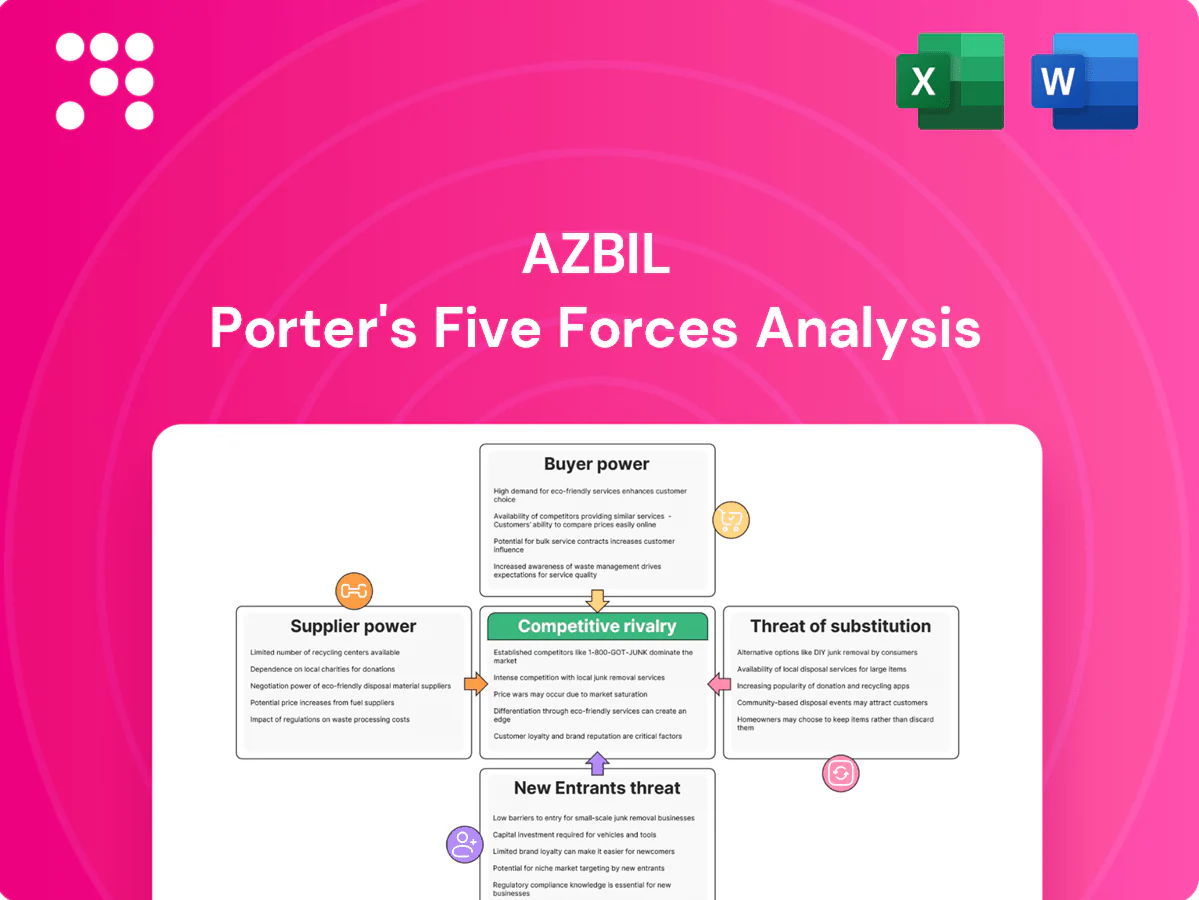

Azbil faces moderate supplier power due to specialized components, steady buyer leverage in industrial automation, and manageable threat from substitutes and new entrants amid high tech barriers; rivalry is intense among global automation firms. This brief snapshot highlights key pressures shaping Azbil’s strategy and valuation. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialized component concentration

Azbil depends on a relatively concentrated base for semiconductors, precision sensors, actuators and control ICs, making it vulnerable to supplier pricing power. Chip lead times spiked to 20+ weeks and industrial component costs rose roughly 10–20% during 2021–23, shifting negotiating leverage to suppliers. Dual-sourcing is feasible but qualification cycles often exceed 12 months, and design-in dependencies materially raise switching costs.

Proprietary software and firmware inputs

Licenses for embedded OS, cybersecurity stacks and middleware give niche vendors leverage over Azbil, especially as 2024 compliance regimes demand recurring, time-sensitive patches with typical SLAs of 30–90 days. Volume improves negotiation power, but deep integration limits viable alternatives. Long-term contracts (commonly 3–5 years) mitigate price volatility while reducing flexibility.

Materials and specialty machining

High-spec metals, advanced ceramics and precision machining for Azbil valves and sensors require certified suppliers (ISO 9001, AS9100, ISO 13485), which narrows the eligible pool and raises entry barriers. Certification and qualification typically take 6–12 months, concentrating risk in fewer vendors. Any disruption can ripple through production schedules, causing delays measured in weeks to months. Supplier development programs mitigate risk but often require multi-year investments.

Logistics and regional risk

- Shipping, geopolitical, FX risk: high

- Regional clustering: ~60% East Asia share (2024)

- Mitigation: inventory/nearshoring vs higher carrying costs

- Supplier behavior: surcharges passed through in tight markets

Standards and compliance inputs

Compliance with ISO/IEC and sector certifications ties Azbil to compliant components, raising switching costs; ISO reported over 1.1 million ISO 9001 certificates globally in 2024, underscoring supplier market depth. Approved vendor lists and audit/documentation demands amplify supplier bargaining power, while multi-year supplier agreements help stabilize the compliance pipeline and reduce sourcing risk.

- Approved-vendor constraints

- Audit/documentation increases power

- ISO 9001 >1.1M (2024)

- Long-term partnerships stabilize supply

Supply squeeze: 20+ weeks, 10-20% cost rise

Azbil faces high supplier power from concentrated semiconductor/sensor vendors; chip lead times hit 20+ weeks and component costs rose 10–20% (2021–23), raising switching costs. Certification and qualification (6–12 months) plus ISO/IEC compliance (ISO 9001 >1.1M certificates in 2024) narrow supplier pool. Long-term contracts (3–5 yrs) and nearshoring mitigate but raise carrying costs.

| Metric | 2024 value | Impact |

|---|---|---|

| Chip lead time | 20+ weeks | High |

| Component cost rise | 10–20% (2021–23) | Medium–High |

| East Asia share | ~60% | Concentration risk |

What is included in the product

Uncovers key drivers of competition and market entry risks tailored to Azbil, with detailed evaluation of supplier and buyer power and their impact on pricing and profitability. Identifies substitutes, disruptive threats, and incumbent protections to inform strategic decisions.

Condenses Azbil's competitive landscape into a single, easy-to-read Five Forces summary—ideal for fast strategic decisions—and lets you tweak pressure levels and notes to reflect real-time market shifts without technical hassle.

Customers Bargaining Power

Large enterprise and public-sector buyers

Large enterprise and public-sector buyers (building owners, industrial plants, governments) purchase via RFPs that intensify price pressure and drive competitive bidding, raising discount expectations. Volume and multi-year contracts typically span 3–5 years, giving buyers leverage on pricing and SLAs. Buyers frequently demand customization and strict service SLAs, forcing suppliers to absorb higher delivery and support costs.

High switching costs with integration

Azbil’s deep existing DCS/BAS footprints, decades of installed systems (company founded 1906; 118 years in 2024), plus operator training and historical data integrations create high switching costs that lock buyers in. Migration risks and potential days‑to‑weeks of downtime temper buyer leverage post‑install. Buyers counter with multi‑vendor sourcing to constrain pricing, while wider adoption of open protocols (eg BACnet/Modbus) slightly eases substitution.

Performance and ROI scrutiny

Energy savings (up to 30% per U.S. DOE estimates), uptime and safety metrics drive Azbil purchasing decisions, with buyers benchmarking vendors on total cost of ownership and payback timelines often targeted at 2–3 years. Demonstrable ROI allows Azbil to justify premium pricing, moderating buyer power, while weak or absent performance data strengthens buyer demands and price pressure.

System integrator influence

System integrators and EPCs aggregate client demand and steer product selection, forcing OEMs like Azbil to accept tighter pricing; complex projects increase integrator gatekeeping and raise switching costs. In 2024, the industrial automation market exceeded $200B, amplifying integrator leverage. Preferred-partner programs can partially restore OEM margins by aligning incentives.

- Integrator aggregation → margin pressure

- Complex projects → stronger gatekeeping

- 2024 market >$200B → higher integrator leverage

- Preferred-partner programs mitigate margin loss

Global alternatives and standardization

Widely adopted standards such as BACnet, Modbus and OPC UA, entrenched in building and industrial automation by 2024, enable multi-sourcing and seamless integration across vendors, letting buyers mix hardware and software from different suppliers and increasing comparability. This transparency intensifies price competition, so Azbil must shift differentiation toward advanced analytics, packaged services and proven reliability to protect margins. Service-level agreements and predictive-maintenance offerings become key value drivers.

- Standards: BACnet, Modbus, OPC UA widely supported in 2024

- Buyer power: easier vendor switching, higher price sensitivity

- Diff strategy: analytics, services, reliability

- Commercial focus: SLAs, predictive maintenance

118-yr DCS legacy limits post-install leverage despite strong buyer price pressure

Buyers exert strong price pressure via RFPs and integrator aggregation, but Azbil’s 118‑year DCS/BAS footprint (118 years in 2024) and high switching costs limit post‑install leverage. 3–5 year contracts and buyer focus on 2–3 year payback on energy savings (up to 30% per DOE) moderate bargaining power. Open standards increase comparability, raising price sensitivity.

| Metric | Value (2024) |

|---|---|

| Market size | >$200B |

| Azbil age/footprint | 118 yrs |

| Contract length | 3–5 yrs |

| Energy savings | up to 30% |

What You See Is What You Get

Azbil Porter's Five Forces Analysis

This preview shows the exact Azbil Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The file is professionally formatted, complete and ready for immediate download. Purchase grants instant access to this same, final document.

A Must-Have Tool for Decision-Makers

Azbil faces moderate supplier power due to specialized components, steady buyer leverage in industrial automation, and manageable threat from substitutes and new entrants amid high tech barriers; rivalry is intense among global automation firms. This brief snapshot highlights key pressures shaping Azbil’s strategy and valuation. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialized component concentration

Azbil depends on a relatively concentrated base for semiconductors, precision sensors, actuators and control ICs, making it vulnerable to supplier pricing power. Chip lead times spiked to 20+ weeks and industrial component costs rose roughly 10–20% during 2021–23, shifting negotiating leverage to suppliers. Dual-sourcing is feasible but qualification cycles often exceed 12 months, and design-in dependencies materially raise switching costs.

Proprietary software and firmware inputs

Licenses for embedded OS, cybersecurity stacks and middleware give niche vendors leverage over Azbil, especially as 2024 compliance regimes demand recurring, time-sensitive patches with typical SLAs of 30–90 days. Volume improves negotiation power, but deep integration limits viable alternatives. Long-term contracts (commonly 3–5 years) mitigate price volatility while reducing flexibility.

Materials and specialty machining

High-spec metals, advanced ceramics and precision machining for Azbil valves and sensors require certified suppliers (ISO 9001, AS9100, ISO 13485), which narrows the eligible pool and raises entry barriers. Certification and qualification typically take 6–12 months, concentrating risk in fewer vendors. Any disruption can ripple through production schedules, causing delays measured in weeks to months. Supplier development programs mitigate risk but often require multi-year investments.

Logistics and regional risk

- Shipping, geopolitical, FX risk: high

- Regional clustering: ~60% East Asia share (2024)

- Mitigation: inventory/nearshoring vs higher carrying costs

- Supplier behavior: surcharges passed through in tight markets

Standards and compliance inputs

Compliance with ISO/IEC and sector certifications ties Azbil to compliant components, raising switching costs; ISO reported over 1.1 million ISO 9001 certificates globally in 2024, underscoring supplier market depth. Approved vendor lists and audit/documentation demands amplify supplier bargaining power, while multi-year supplier agreements help stabilize the compliance pipeline and reduce sourcing risk.

- Approved-vendor constraints

- Audit/documentation increases power

- ISO 9001 >1.1M (2024)

- Long-term partnerships stabilize supply

Supply squeeze: 20+ weeks, 10-20% cost rise

Azbil faces high supplier power from concentrated semiconductor/sensor vendors; chip lead times hit 20+ weeks and component costs rose 10–20% (2021–23), raising switching costs. Certification and qualification (6–12 months) plus ISO/IEC compliance (ISO 9001 >1.1M certificates in 2024) narrow supplier pool. Long-term contracts (3–5 yrs) and nearshoring mitigate but raise carrying costs.

| Metric | 2024 value | Impact |

|---|---|---|

| Chip lead time | 20+ weeks | High |

| Component cost rise | 10–20% (2021–23) | Medium–High |

| East Asia share | ~60% | Concentration risk |

What is included in the product

Uncovers key drivers of competition and market entry risks tailored to Azbil, with detailed evaluation of supplier and buyer power and their impact on pricing and profitability. Identifies substitutes, disruptive threats, and incumbent protections to inform strategic decisions.

Condenses Azbil's competitive landscape into a single, easy-to-read Five Forces summary—ideal for fast strategic decisions—and lets you tweak pressure levels and notes to reflect real-time market shifts without technical hassle.

Customers Bargaining Power

Large enterprise and public-sector buyers

Large enterprise and public-sector buyers (building owners, industrial plants, governments) purchase via RFPs that intensify price pressure and drive competitive bidding, raising discount expectations. Volume and multi-year contracts typically span 3–5 years, giving buyers leverage on pricing and SLAs. Buyers frequently demand customization and strict service SLAs, forcing suppliers to absorb higher delivery and support costs.

High switching costs with integration

Azbil’s deep existing DCS/BAS footprints, decades of installed systems (company founded 1906; 118 years in 2024), plus operator training and historical data integrations create high switching costs that lock buyers in. Migration risks and potential days‑to‑weeks of downtime temper buyer leverage post‑install. Buyers counter with multi‑vendor sourcing to constrain pricing, while wider adoption of open protocols (eg BACnet/Modbus) slightly eases substitution.

Performance and ROI scrutiny

Energy savings (up to 30% per U.S. DOE estimates), uptime and safety metrics drive Azbil purchasing decisions, with buyers benchmarking vendors on total cost of ownership and payback timelines often targeted at 2–3 years. Demonstrable ROI allows Azbil to justify premium pricing, moderating buyer power, while weak or absent performance data strengthens buyer demands and price pressure.

System integrator influence

System integrators and EPCs aggregate client demand and steer product selection, forcing OEMs like Azbil to accept tighter pricing; complex projects increase integrator gatekeeping and raise switching costs. In 2024, the industrial automation market exceeded $200B, amplifying integrator leverage. Preferred-partner programs can partially restore OEM margins by aligning incentives.

- Integrator aggregation → margin pressure

- Complex projects → stronger gatekeeping

- 2024 market >$200B → higher integrator leverage

- Preferred-partner programs mitigate margin loss

Global alternatives and standardization

Widely adopted standards such as BACnet, Modbus and OPC UA, entrenched in building and industrial automation by 2024, enable multi-sourcing and seamless integration across vendors, letting buyers mix hardware and software from different suppliers and increasing comparability. This transparency intensifies price competition, so Azbil must shift differentiation toward advanced analytics, packaged services and proven reliability to protect margins. Service-level agreements and predictive-maintenance offerings become key value drivers.

- Standards: BACnet, Modbus, OPC UA widely supported in 2024

- Buyer power: easier vendor switching, higher price sensitivity

- Diff strategy: analytics, services, reliability

- Commercial focus: SLAs, predictive maintenance

118-yr DCS legacy limits post-install leverage despite strong buyer price pressure

Buyers exert strong price pressure via RFPs and integrator aggregation, but Azbil’s 118‑year DCS/BAS footprint (118 years in 2024) and high switching costs limit post‑install leverage. 3–5 year contracts and buyer focus on 2–3 year payback on energy savings (up to 30% per DOE) moderate bargaining power. Open standards increase comparability, raising price sensitivity.

| Metric | Value (2024) |

|---|---|

| Market size | >$200B |

| Azbil age/footprint | 118 yrs |

| Contract length | 3–5 yrs |

| Energy savings | up to 30% |

What You See Is What You Get

Azbil Porter's Five Forces Analysis

This preview shows the exact Azbil Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The file is professionally formatted, complete and ready for immediate download. Purchase grants instant access to this same, final document.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Azbil faces moderate supplier power due to specialized components, steady buyer leverage in industrial automation, and manageable threat from substitutes and new entrants amid high tech barriers; rivalry is intense among global automation firms. This brief snapshot highlights key pressures shaping Azbil’s strategy and valuation. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Specialized component concentration

Azbil depends on a relatively concentrated base for semiconductors, precision sensors, actuators and control ICs, making it vulnerable to supplier pricing power. Chip lead times spiked to 20+ weeks and industrial component costs rose roughly 10–20% during 2021–23, shifting negotiating leverage to suppliers. Dual-sourcing is feasible but qualification cycles often exceed 12 months, and design-in dependencies materially raise switching costs.

Proprietary software and firmware inputs

Licenses for embedded OS, cybersecurity stacks and middleware give niche vendors leverage over Azbil, especially as 2024 compliance regimes demand recurring, time-sensitive patches with typical SLAs of 30–90 days. Volume improves negotiation power, but deep integration limits viable alternatives. Long-term contracts (commonly 3–5 years) mitigate price volatility while reducing flexibility.

Materials and specialty machining

High-spec metals, advanced ceramics and precision machining for Azbil valves and sensors require certified suppliers (ISO 9001, AS9100, ISO 13485), which narrows the eligible pool and raises entry barriers. Certification and qualification typically take 6–12 months, concentrating risk in fewer vendors. Any disruption can ripple through production schedules, causing delays measured in weeks to months. Supplier development programs mitigate risk but often require multi-year investments.

Logistics and regional risk

- Shipping, geopolitical, FX risk: high

- Regional clustering: ~60% East Asia share (2024)

- Mitigation: inventory/nearshoring vs higher carrying costs

- Supplier behavior: surcharges passed through in tight markets

Standards and compliance inputs

Compliance with ISO/IEC and sector certifications ties Azbil to compliant components, raising switching costs; ISO reported over 1.1 million ISO 9001 certificates globally in 2024, underscoring supplier market depth. Approved vendor lists and audit/documentation demands amplify supplier bargaining power, while multi-year supplier agreements help stabilize the compliance pipeline and reduce sourcing risk.

- Approved-vendor constraints

- Audit/documentation increases power

- ISO 9001 >1.1M (2024)

- Long-term partnerships stabilize supply

Supply squeeze: 20+ weeks, 10-20% cost rise

Azbil faces high supplier power from concentrated semiconductor/sensor vendors; chip lead times hit 20+ weeks and component costs rose 10–20% (2021–23), raising switching costs. Certification and qualification (6–12 months) plus ISO/IEC compliance (ISO 9001 >1.1M certificates in 2024) narrow supplier pool. Long-term contracts (3–5 yrs) and nearshoring mitigate but raise carrying costs.

| Metric | 2024 value | Impact |

|---|---|---|

| Chip lead time | 20+ weeks | High |

| Component cost rise | 10–20% (2021–23) | Medium–High |

| East Asia share | ~60% | Concentration risk |

What is included in the product

Uncovers key drivers of competition and market entry risks tailored to Azbil, with detailed evaluation of supplier and buyer power and their impact on pricing and profitability. Identifies substitutes, disruptive threats, and incumbent protections to inform strategic decisions.

Condenses Azbil's competitive landscape into a single, easy-to-read Five Forces summary—ideal for fast strategic decisions—and lets you tweak pressure levels and notes to reflect real-time market shifts without technical hassle.

Customers Bargaining Power

Large enterprise and public-sector buyers

Large enterprise and public-sector buyers (building owners, industrial plants, governments) purchase via RFPs that intensify price pressure and drive competitive bidding, raising discount expectations. Volume and multi-year contracts typically span 3–5 years, giving buyers leverage on pricing and SLAs. Buyers frequently demand customization and strict service SLAs, forcing suppliers to absorb higher delivery and support costs.

High switching costs with integration

Azbil’s deep existing DCS/BAS footprints, decades of installed systems (company founded 1906; 118 years in 2024), plus operator training and historical data integrations create high switching costs that lock buyers in. Migration risks and potential days‑to‑weeks of downtime temper buyer leverage post‑install. Buyers counter with multi‑vendor sourcing to constrain pricing, while wider adoption of open protocols (eg BACnet/Modbus) slightly eases substitution.

Performance and ROI scrutiny

Energy savings (up to 30% per U.S. DOE estimates), uptime and safety metrics drive Azbil purchasing decisions, with buyers benchmarking vendors on total cost of ownership and payback timelines often targeted at 2–3 years. Demonstrable ROI allows Azbil to justify premium pricing, moderating buyer power, while weak or absent performance data strengthens buyer demands and price pressure.

System integrator influence

System integrators and EPCs aggregate client demand and steer product selection, forcing OEMs like Azbil to accept tighter pricing; complex projects increase integrator gatekeeping and raise switching costs. In 2024, the industrial automation market exceeded $200B, amplifying integrator leverage. Preferred-partner programs can partially restore OEM margins by aligning incentives.

- Integrator aggregation → margin pressure

- Complex projects → stronger gatekeeping

- 2024 market >$200B → higher integrator leverage

- Preferred-partner programs mitigate margin loss

Global alternatives and standardization

Widely adopted standards such as BACnet, Modbus and OPC UA, entrenched in building and industrial automation by 2024, enable multi-sourcing and seamless integration across vendors, letting buyers mix hardware and software from different suppliers and increasing comparability. This transparency intensifies price competition, so Azbil must shift differentiation toward advanced analytics, packaged services and proven reliability to protect margins. Service-level agreements and predictive-maintenance offerings become key value drivers.

- Standards: BACnet, Modbus, OPC UA widely supported in 2024

- Buyer power: easier vendor switching, higher price sensitivity

- Diff strategy: analytics, services, reliability

- Commercial focus: SLAs, predictive maintenance

118-yr DCS legacy limits post-install leverage despite strong buyer price pressure

Buyers exert strong price pressure via RFPs and integrator aggregation, but Azbil’s 118‑year DCS/BAS footprint (118 years in 2024) and high switching costs limit post‑install leverage. 3–5 year contracts and buyer focus on 2–3 year payback on energy savings (up to 30% per DOE) moderate bargaining power. Open standards increase comparability, raising price sensitivity.

| Metric | Value (2024) |

|---|---|

| Market size | >$200B |

| Azbil age/footprint | 118 yrs |

| Contract length | 3–5 yrs |

| Energy savings | up to 30% |

What You See Is What You Get

Azbil Porter's Five Forces Analysis

This preview shows the exact Azbil Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The file is professionally formatted, complete and ready for immediate download. Purchase grants instant access to this same, final document.