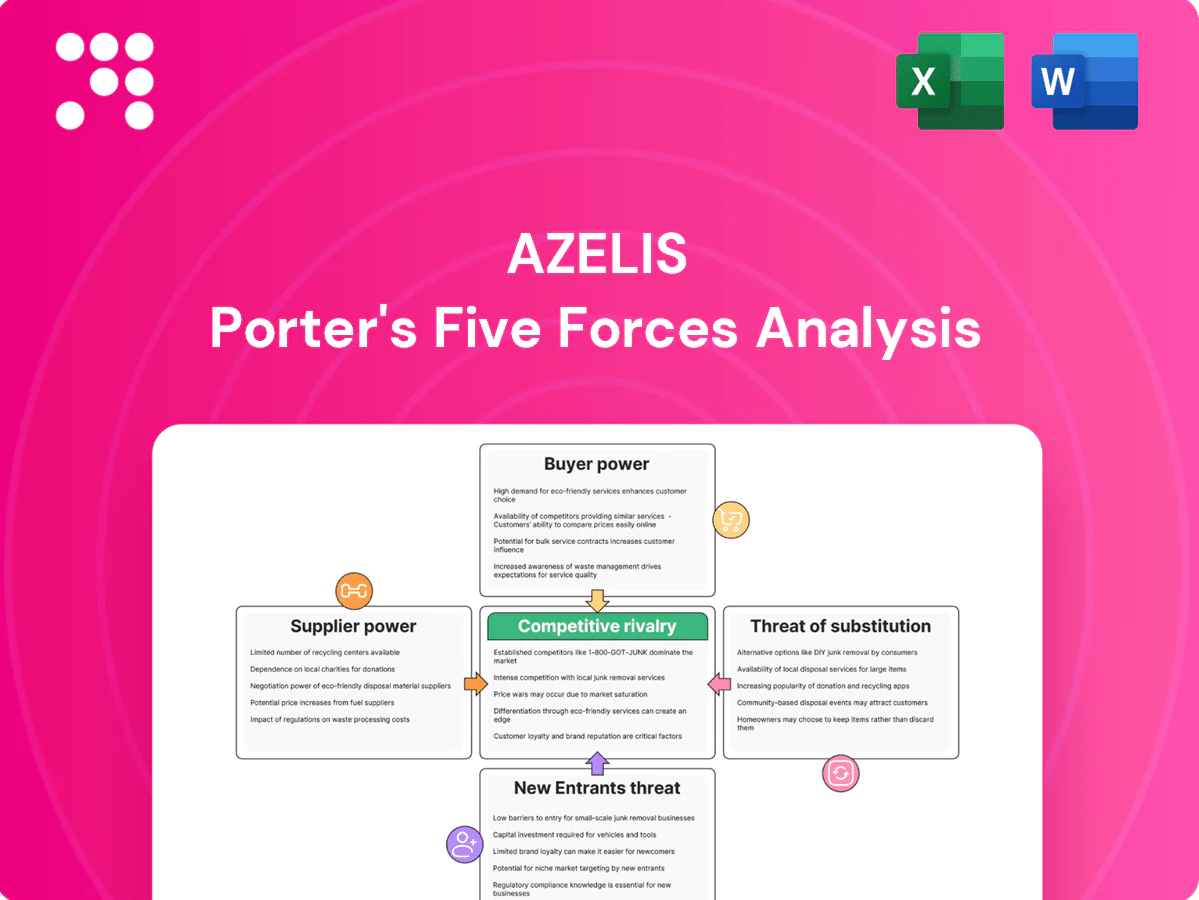

Azelis Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Azelis faces moderate supplier power, fragmented buyer segments, and steady rivalry as specialty chemicals distribution grows; substitutes and new entrants pose selective threats across regions. This snapshot highlights strategic pressures shaping margins and growth potential. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable insights to inform investment and strategy.

Suppliers Bargaining Power

Consolidated specialty principals

Consolidated specialty principals in personal care, CASE, food and pharma exert strong leverage over contract terms and territory assignments, reflecting a 2024 global specialty chemicals market estimated at USD 839 billion. Their brand equity and innovation pipelines make like-for-like substitution difficult. Concentration often forces stricter margin structures and inventory obligations on distributors, while Azelis’ >5,000-principal portfolio and multi-principal balance in 2024 mitigate supplier power.

Exclusive territories and line cards

Suppliers often grant exclusivity by country or segment, which boosts Azelis volume commitments but can concentrate risk in specific niches. As of 2024 Azelis operates in 60+ countries, so exclusivity can both expand market reach and increase dependence on a few principals. Principals may renegotiate or reallocate lines based on sales performance, margins or strategic shifts. Superior technical service and demonstrated market access are key to retaining and renewing lines.

Innovation and technical dependence

Principals control access to novel chemistries and application data, giving suppliers strong bargaining power; distributors that accelerate adoption via formulation expertise often secure preferential terms while those lacking lab capabilities face commoditization. Azelis’ global application labs and formulation support reduce this asymmetry by providing principals with demonstrated market traction and customers with tailored solutions. Joint development projects further increase supplier stickiness and long-term exclusivity.

Capacity, ESG, and regulatory constraints

- Capacity tightness → supplier leverage

- REACH/FDA compliance → allocation preference

- ESG reporting → preferred supplier status

- Forecasting/compliance → pricing & service stability

Disintermediation risk

Larger principals can contemplate going direct to key accounts or using digital portals, increasing margin pressure on Azelis; by 2024 digital B2B buying reached majority adoption, amplifying this risk. The fragmented long tail of customers and high technical selling effort still sustain distributor value. Azelis mitigates risks by bundling multi-principal solutions and value-added services and using performance-based agreements to align incentives.

- Disintermediation risk: higher with digital adoption (2024)

- Defensive strength: long-tail fragmentation, technical selling

- Mitigation: multi-principal bundles, value-added services

- Alignment: performance-based contracts

Supplier power and exclusivity squeeze specialty chemicals margins as digital B2B rises

Suppliers hold strong leverage via brand, novel chemistries and exclusivities, driving margin pressure and allocations; 2024 specialty chemicals market ~USD 839bn. Azelis' >5,000 principals across 60+ countries, global labs and ESG reporting partly mitigate power and disintermediation risks as digital B2B adoption reached majority in 2024.

| Metric | Value (2024) |

|---|---|

| Specialty market | USD 839bn |

| Azelis principals | >5,000 |

| Countries | 60+ |

| REACH substances | 22,000+ |

What is included in the product

Tailored Porter's Five Forces analysis for Azelis that uncovers competition drivers, supplier and buyer power, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, risk mitigation and growth decisions.

Azelis Porter's Five Forces delivers a one-sheet, editable radar summary that instantly visualizes competitive pressure, customizable for decks, scenarios, and non‑finance users.

Customers Bargaining Power

Fragmented but with large anchor accounts

Customer base mixes many SMEs with multinational formulators that run centralized tenders and command service SLAs, rebates and volume discounts; large accounts thus wield strong negotiating leverage. The fragmented long tail of SMEs dilutes aggregate buyer power, while Azelis’ scale—present in 57 countries with roughly 6,000 employees—lets it serve both efficiently and absorb pricing pressure.

Switching costs via qualification

Regulatory and performance qualifications in pharma, food and CASE typically require 6–12 months of testing and documentation, with annual audits and revalidation often costing tens of thousands of euros, making distributor switches slow and costly. Reformulation risk and audit-led revalidation protect margins, while Azelis’ extensive documentation and traceability deepen customer embeddedness. Still, buyers commonly dual-source non-critical SKUs to manage supply risk.

Price sensitivity in cyclical end-markets

In downturns customers push for price concessions and extended payment terms, often driving discounts of 5–15% and payment extensions by 30–60 days; inventory destocking (often 10–20% lower turnover) amplifies downward price pressure on distributors. Azelis defends value via total cost of ownership arguments and client efficiency programs that protect margins. Dynamic pricing algorithms and commodity hedging reduce margin volatility and pass-through risk.

Demand for technical service

Buyers increasingly prioritize formulation support, rapid sampling and troubleshooting, so price is less central; Azelis reported €3.0bn sales in 2024 and leverages this scale to embed technical services into deals. On-site lab trials and co-development programs raise switching costs, and Azelis application centers shift transactions from product sales to solution-based contracts, reducing buyer leverage.

- Technical support: rapid sampling & troubleshooting

- Switching barriers: on-site trials & co-development

- Business model: application centers → solutions selling

- Impact 2024: service intensity weakens buyer bargaining power

Digital transparency and tendering

- Spec comparability: boosts buyer leverage

- Reverse auctions/RFQs: common for commodities

- Azelis differentiation: curated portfolios + compliance

- Bundling: offsets price-only comparisons

Scale shields global distributor from discounts, longer payments and regulatory churn

Customers mix large centralized tenders (high leverage) and fragmented SMEs (low leverage); Azelis’ scale—€3.0bn sales in 2024, 57 countries, ~6,000 employees—helps absorb pressure. Regulatory revalidation (6–12 months, audits costing tens of thousands €) and co-development raise switching costs, though buyers often seek 5–15% discounts and 30–60 day payment extensions.

| Metric | 2024 / Impact |

|---|---|

| Sales | €3.0bn |

| Countries / Staff | 57 / ~6,000 |

| Typical discounts | 5–15% |

| Payment terms | +30–60 days |

| Regulatory lead time | 6–12 months |

What You See Is What You Get

Azelis Porter's Five Forces Analysis

This preview shows the exact Azelis Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the complete deliverable, so there are no surprises: the document shown is precisely what will be available to you after payment.

Don't Miss the Bigger Picture

Azelis faces moderate supplier power, fragmented buyer segments, and steady rivalry as specialty chemicals distribution grows; substitutes and new entrants pose selective threats across regions. This snapshot highlights strategic pressures shaping margins and growth potential. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable insights to inform investment and strategy.

Suppliers Bargaining Power

Consolidated specialty principals

Consolidated specialty principals in personal care, CASE, food and pharma exert strong leverage over contract terms and territory assignments, reflecting a 2024 global specialty chemicals market estimated at USD 839 billion. Their brand equity and innovation pipelines make like-for-like substitution difficult. Concentration often forces stricter margin structures and inventory obligations on distributors, while Azelis’ >5,000-principal portfolio and multi-principal balance in 2024 mitigate supplier power.

Exclusive territories and line cards

Suppliers often grant exclusivity by country or segment, which boosts Azelis volume commitments but can concentrate risk in specific niches. As of 2024 Azelis operates in 60+ countries, so exclusivity can both expand market reach and increase dependence on a few principals. Principals may renegotiate or reallocate lines based on sales performance, margins or strategic shifts. Superior technical service and demonstrated market access are key to retaining and renewing lines.

Innovation and technical dependence

Principals control access to novel chemistries and application data, giving suppliers strong bargaining power; distributors that accelerate adoption via formulation expertise often secure preferential terms while those lacking lab capabilities face commoditization. Azelis’ global application labs and formulation support reduce this asymmetry by providing principals with demonstrated market traction and customers with tailored solutions. Joint development projects further increase supplier stickiness and long-term exclusivity.

Capacity, ESG, and regulatory constraints

- Capacity tightness → supplier leverage

- REACH/FDA compliance → allocation preference

- ESG reporting → preferred supplier status

- Forecasting/compliance → pricing & service stability

Disintermediation risk

Larger principals can contemplate going direct to key accounts or using digital portals, increasing margin pressure on Azelis; by 2024 digital B2B buying reached majority adoption, amplifying this risk. The fragmented long tail of customers and high technical selling effort still sustain distributor value. Azelis mitigates risks by bundling multi-principal solutions and value-added services and using performance-based agreements to align incentives.

- Disintermediation risk: higher with digital adoption (2024)

- Defensive strength: long-tail fragmentation, technical selling

- Mitigation: multi-principal bundles, value-added services

- Alignment: performance-based contracts

Supplier power and exclusivity squeeze specialty chemicals margins as digital B2B rises

Suppliers hold strong leverage via brand, novel chemistries and exclusivities, driving margin pressure and allocations; 2024 specialty chemicals market ~USD 839bn. Azelis' >5,000 principals across 60+ countries, global labs and ESG reporting partly mitigate power and disintermediation risks as digital B2B adoption reached majority in 2024.

| Metric | Value (2024) |

|---|---|

| Specialty market | USD 839bn |

| Azelis principals | >5,000 |

| Countries | 60+ |

| REACH substances | 22,000+ |

What is included in the product

Tailored Porter's Five Forces analysis for Azelis that uncovers competition drivers, supplier and buyer power, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, risk mitigation and growth decisions.

Azelis Porter's Five Forces delivers a one-sheet, editable radar summary that instantly visualizes competitive pressure, customizable for decks, scenarios, and non‑finance users.

Customers Bargaining Power

Fragmented but with large anchor accounts

Customer base mixes many SMEs with multinational formulators that run centralized tenders and command service SLAs, rebates and volume discounts; large accounts thus wield strong negotiating leverage. The fragmented long tail of SMEs dilutes aggregate buyer power, while Azelis’ scale—present in 57 countries with roughly 6,000 employees—lets it serve both efficiently and absorb pricing pressure.

Switching costs via qualification

Regulatory and performance qualifications in pharma, food and CASE typically require 6–12 months of testing and documentation, with annual audits and revalidation often costing tens of thousands of euros, making distributor switches slow and costly. Reformulation risk and audit-led revalidation protect margins, while Azelis’ extensive documentation and traceability deepen customer embeddedness. Still, buyers commonly dual-source non-critical SKUs to manage supply risk.

Price sensitivity in cyclical end-markets

In downturns customers push for price concessions and extended payment terms, often driving discounts of 5–15% and payment extensions by 30–60 days; inventory destocking (often 10–20% lower turnover) amplifies downward price pressure on distributors. Azelis defends value via total cost of ownership arguments and client efficiency programs that protect margins. Dynamic pricing algorithms and commodity hedging reduce margin volatility and pass-through risk.

Demand for technical service

Buyers increasingly prioritize formulation support, rapid sampling and troubleshooting, so price is less central; Azelis reported €3.0bn sales in 2024 and leverages this scale to embed technical services into deals. On-site lab trials and co-development programs raise switching costs, and Azelis application centers shift transactions from product sales to solution-based contracts, reducing buyer leverage.

- Technical support: rapid sampling & troubleshooting

- Switching barriers: on-site trials & co-development

- Business model: application centers → solutions selling

- Impact 2024: service intensity weakens buyer bargaining power

Digital transparency and tendering

- Spec comparability: boosts buyer leverage

- Reverse auctions/RFQs: common for commodities

- Azelis differentiation: curated portfolios + compliance

- Bundling: offsets price-only comparisons

Scale shields global distributor from discounts, longer payments and regulatory churn

Customers mix large centralized tenders (high leverage) and fragmented SMEs (low leverage); Azelis’ scale—€3.0bn sales in 2024, 57 countries, ~6,000 employees—helps absorb pressure. Regulatory revalidation (6–12 months, audits costing tens of thousands €) and co-development raise switching costs, though buyers often seek 5–15% discounts and 30–60 day payment extensions.

| Metric | 2024 / Impact |

|---|---|

| Sales | €3.0bn |

| Countries / Staff | 57 / ~6,000 |

| Typical discounts | 5–15% |

| Payment terms | +30–60 days |

| Regulatory lead time | 6–12 months |

What You See Is What You Get

Azelis Porter's Five Forces Analysis

This preview shows the exact Azelis Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the complete deliverable, so there are no surprises: the document shown is precisely what will be available to you after payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Azelis faces moderate supplier power, fragmented buyer segments, and steady rivalry as specialty chemicals distribution grows; substitutes and new entrants pose selective threats across regions. This snapshot highlights strategic pressures shaping margins and growth potential. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable insights to inform investment and strategy.

Suppliers Bargaining Power

Consolidated specialty principals

Consolidated specialty principals in personal care, CASE, food and pharma exert strong leverage over contract terms and territory assignments, reflecting a 2024 global specialty chemicals market estimated at USD 839 billion. Their brand equity and innovation pipelines make like-for-like substitution difficult. Concentration often forces stricter margin structures and inventory obligations on distributors, while Azelis’ >5,000-principal portfolio and multi-principal balance in 2024 mitigate supplier power.

Exclusive territories and line cards

Suppliers often grant exclusivity by country or segment, which boosts Azelis volume commitments but can concentrate risk in specific niches. As of 2024 Azelis operates in 60+ countries, so exclusivity can both expand market reach and increase dependence on a few principals. Principals may renegotiate or reallocate lines based on sales performance, margins or strategic shifts. Superior technical service and demonstrated market access are key to retaining and renewing lines.

Innovation and technical dependence

Principals control access to novel chemistries and application data, giving suppliers strong bargaining power; distributors that accelerate adoption via formulation expertise often secure preferential terms while those lacking lab capabilities face commoditization. Azelis’ global application labs and formulation support reduce this asymmetry by providing principals with demonstrated market traction and customers with tailored solutions. Joint development projects further increase supplier stickiness and long-term exclusivity.

Capacity, ESG, and regulatory constraints

- Capacity tightness → supplier leverage

- REACH/FDA compliance → allocation preference

- ESG reporting → preferred supplier status

- Forecasting/compliance → pricing & service stability

Disintermediation risk

Larger principals can contemplate going direct to key accounts or using digital portals, increasing margin pressure on Azelis; by 2024 digital B2B buying reached majority adoption, amplifying this risk. The fragmented long tail of customers and high technical selling effort still sustain distributor value. Azelis mitigates risks by bundling multi-principal solutions and value-added services and using performance-based agreements to align incentives.

- Disintermediation risk: higher with digital adoption (2024)

- Defensive strength: long-tail fragmentation, technical selling

- Mitigation: multi-principal bundles, value-added services

- Alignment: performance-based contracts

Supplier power and exclusivity squeeze specialty chemicals margins as digital B2B rises

Suppliers hold strong leverage via brand, novel chemistries and exclusivities, driving margin pressure and allocations; 2024 specialty chemicals market ~USD 839bn. Azelis' >5,000 principals across 60+ countries, global labs and ESG reporting partly mitigate power and disintermediation risks as digital B2B adoption reached majority in 2024.

| Metric | Value (2024) |

|---|---|

| Specialty market | USD 839bn |

| Azelis principals | >5,000 |

| Countries | 60+ |

| REACH substances | 22,000+ |

What is included in the product

Tailored Porter's Five Forces analysis for Azelis that uncovers competition drivers, supplier and buyer power, entry barriers, substitutes and emerging threats, with strategic commentary to inform pricing, risk mitigation and growth decisions.

Azelis Porter's Five Forces delivers a one-sheet, editable radar summary that instantly visualizes competitive pressure, customizable for decks, scenarios, and non‑finance users.

Customers Bargaining Power

Fragmented but with large anchor accounts

Customer base mixes many SMEs with multinational formulators that run centralized tenders and command service SLAs, rebates and volume discounts; large accounts thus wield strong negotiating leverage. The fragmented long tail of SMEs dilutes aggregate buyer power, while Azelis’ scale—present in 57 countries with roughly 6,000 employees—lets it serve both efficiently and absorb pricing pressure.

Switching costs via qualification

Regulatory and performance qualifications in pharma, food and CASE typically require 6–12 months of testing and documentation, with annual audits and revalidation often costing tens of thousands of euros, making distributor switches slow and costly. Reformulation risk and audit-led revalidation protect margins, while Azelis’ extensive documentation and traceability deepen customer embeddedness. Still, buyers commonly dual-source non-critical SKUs to manage supply risk.

Price sensitivity in cyclical end-markets

In downturns customers push for price concessions and extended payment terms, often driving discounts of 5–15% and payment extensions by 30–60 days; inventory destocking (often 10–20% lower turnover) amplifies downward price pressure on distributors. Azelis defends value via total cost of ownership arguments and client efficiency programs that protect margins. Dynamic pricing algorithms and commodity hedging reduce margin volatility and pass-through risk.

Demand for technical service

Buyers increasingly prioritize formulation support, rapid sampling and troubleshooting, so price is less central; Azelis reported €3.0bn sales in 2024 and leverages this scale to embed technical services into deals. On-site lab trials and co-development programs raise switching costs, and Azelis application centers shift transactions from product sales to solution-based contracts, reducing buyer leverage.

- Technical support: rapid sampling & troubleshooting

- Switching barriers: on-site trials & co-development

- Business model: application centers → solutions selling

- Impact 2024: service intensity weakens buyer bargaining power

Digital transparency and tendering

- Spec comparability: boosts buyer leverage

- Reverse auctions/RFQs: common for commodities

- Azelis differentiation: curated portfolios + compliance

- Bundling: offsets price-only comparisons

Scale shields global distributor from discounts, longer payments and regulatory churn

Customers mix large centralized tenders (high leverage) and fragmented SMEs (low leverage); Azelis’ scale—€3.0bn sales in 2024, 57 countries, ~6,000 employees—helps absorb pressure. Regulatory revalidation (6–12 months, audits costing tens of thousands €) and co-development raise switching costs, though buyers often seek 5–15% discounts and 30–60 day payment extensions.

| Metric | 2024 / Impact |

|---|---|

| Sales | €3.0bn |

| Countries / Staff | 57 / ~6,000 |

| Typical discounts | 5–15% |

| Payment terms | +30–60 days |

| Regulatory lead time | 6–12 months |

What You See Is What You Get

Azelis Porter's Five Forces Analysis

This preview shows the exact Azelis Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the complete deliverable, so there are no surprises: the document shown is precisely what will be available to you after payment.