Azkoyen Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Azkoyen faces nuanced competitive pressures across supplier bargaining, buyer power, substitute threats, industry rivalry and entry barriers, shaping margins and growth prospects. This snapshot highlights key tensions but stops short of force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get a consultant-grade, data-driven breakdown tailored to Azkoyen’s strategic decisions.

Suppliers Bargaining Power

Specialized components

Many inputs for payment systems and access control, such as RFID modules and secure chips, are specialized and sourced from a small number of suppliers, concentrating bargaining power and raising switching costs and lead times; qualification cycles are frequently lengthy, typically 12–18 months. Supplier consolidation can drive pricing power and volatility; dual-sourcing mitigates risk but increases qualification cost and inventory needs.

Electronics and semiconductors

Volatile semiconductor cycles drive board, sensor and display price swings and lead times often stretching 12–52 weeks; global semiconductor sales rose from about $556B in 2023 to roughly $588B in 2024 (WSTS), concentrating capacity. Priority allocations favor large OEMs, squeezing mid-cap manufacturers like Azkoyen and forcing 5–15% procurement premiums. Long component lifecycles in industrial gear limit redesign agility, so strategic inventory buffers mitigate shortages but tie up working capital and can raise inventory days by months.

Steel, plastics, and enclosures

Commodity steel and plastics, which comprise roughly 30% of vending-cabinet BOM, are widely available, limiting supplier power; however 2024 container spot rates averaged about $1,200/FEU and industrial energy volatility produced input cost swings often in the 10–25% range. Custom tooling and molds generate partial lock-in with typical lead times of 6–12 months, while regional suppliers can cut currency and freight risk by an estimated 10–20%.

Software and security IP

Licensing for encryption, payment kernels and OS stacks is concentrated among a few IP holders, giving them leverage as compliance updates like PCI and EMV force mandatory upgrades and patches that suppliers control.

Royalties and certification fees raise unit economics for device makers, though firms that invest in in-house software development gradually reduce supplier dependence and recurring costs.

- Concentration: few licensors control core IP

- Compliance leverage: PCI/EMV drive mandatory upgrades

- Cost impact: royalties and certification raise unit COGS

- Mitigation: in-house software lowers long-term dependence

Service and field parts

Aftermarket parts and maintenance kits for Azkoyen are typically sourced from approved suppliers to preserve warranty coverage, which restricts substitution and sustains supplier margins; multi-year service contracts further entrench these supplier relationships while standardizing parts across models can weaken that power.

- Approved suppliers limit substitution

- Service contracts embed relationships

- Standardized parts dilute power

Supply squeeze: chips lead times 12-52w, premiums 5-15%

Supplier power is high for secure chips/RFID and software IP, with qualification cycles of 12–18 months and semiconductor lead times 12–52 weeks; global semiconductor sales rose to about $588B in 2024 (WSTS). Procurement premiums of 5–15% hit mid-cap OEMs; container spot rates averaged ~$1,200/FEU in 2024, raising logistics cost exposure and working-capital needs.

| Factor | 2024 Data |

|---|---|

| Semiconductor market | $588B |

| Lead times | 12–52 weeks |

| Qualification | 12–18 months |

| Procurement premium | 5–15% |

| Container spot rate | $1,200/FEU |

What is included in the product

Tailored Porter's Five Forces for Azkoyen, assessing rival intensity, supplier and buyer power, substitute threats and entry barriers to reveal pricing pressure, profitability levers, and emerging disruptive risks.

A concise, one-sheet Porter's Five Forces for Azkoyen that distills competitive threats, supplier/customer bargaining, substitutes and entry barriers into board-ready insights—speeding strategic decisions and easing stakeholder communication.

Customers Bargaining Power

Consolidated enterprise buyers

Large operators in vending, coffee service, retail, and transit procure machines and consumables in high volumes, enabling aggressive bidding and strict total-cost-of-ownership requirements that compress supplier margins.

Demand for integration

Buyers now expect seamless payment, telemetry and access-control integration, driving demand for end-to-end vendors that lower switching costs by bundling hardware, software and services. The API management market reached about $5.2bn in 2024, enabling multi-sourcing and increasing buyer leverage. Closed ecosystems can retain clients but face growing pushback as buyers favor open standards.

Price sensitivity and ROI

Operators judge payback by uptime, cashless conversion and energy efficiency, typically targeting a sub-24‑month payback to justify deployments. High comparability across machines amplifies price pressure, while service SLAs and financing (often stretched to 30–36 months) are used as bargaining chips. Demonstrable TCO reductions of ~15–25% materially soften buyer power.

Customization requests

Customization requests for validators, readers and cabinets are common, raising switching costs through unique NRE but giving buyers leverage to negotiate NRE discounts; modular platforms can reduce NRE by about 25% while preserving feature flexibility. Delays in bespoke builds have been cited to jeopardize 15%–20% of deals in vending/hospitality bids in 2024.

- Sector-specific parts: validators/readers/cabinets

- Customization increases switching costs yet creates NRE negotiation points

- Modular platforms can cut NRE ~25%

- Bespoke build delays risk ~15%–20% of deals (2024)

Alternative channels

Some buyers consider refurbished or secondary-market vending units, which anchors lower price expectations; global refurbished electronics market surpassed $50 billion in 2024, reinforcing resale benchmarks. Warranty, regulatory compliance, and proprietary software support limit used-equipment appeal for Azkoyen’s cashless and telemetry-enabled machines. Trade-in programs can recapture up to mid-single-digit market share by converting replacement demand into company-controlled refurb inventory.

- Refurbished market size: >$50B (2024)

- Warranty/compliance restricts appeal

- Trade-ins recapture demand

Large buyers force sub-24-month paybacks; open APIs $5.2bn, refurbished $50bn+

Large-volume operators exert strong price and TCO-driven leverage, demanding sub-24-month paybacks; comparable machines and cashless/telemetry expectations increase supplier concessions. Buyers favor open APIs ($5.2bn API mgmt market in 2024) and refurbished benchmarks (> $50bn 2024), using SLAs, financing and NRE negotiations (modular NRE cuts ~25%) to enhance bargaining power.

| Metric | 2024 |

|---|---|

| API market | $5.2bn |

| Refurbished market | >$50bn |

| Modular NRE reduction | ~25% |

| TCO reduction wins | 15–25% |

Preview the Actual Deliverable

Azkoyen Porter's Five Forces Analysis

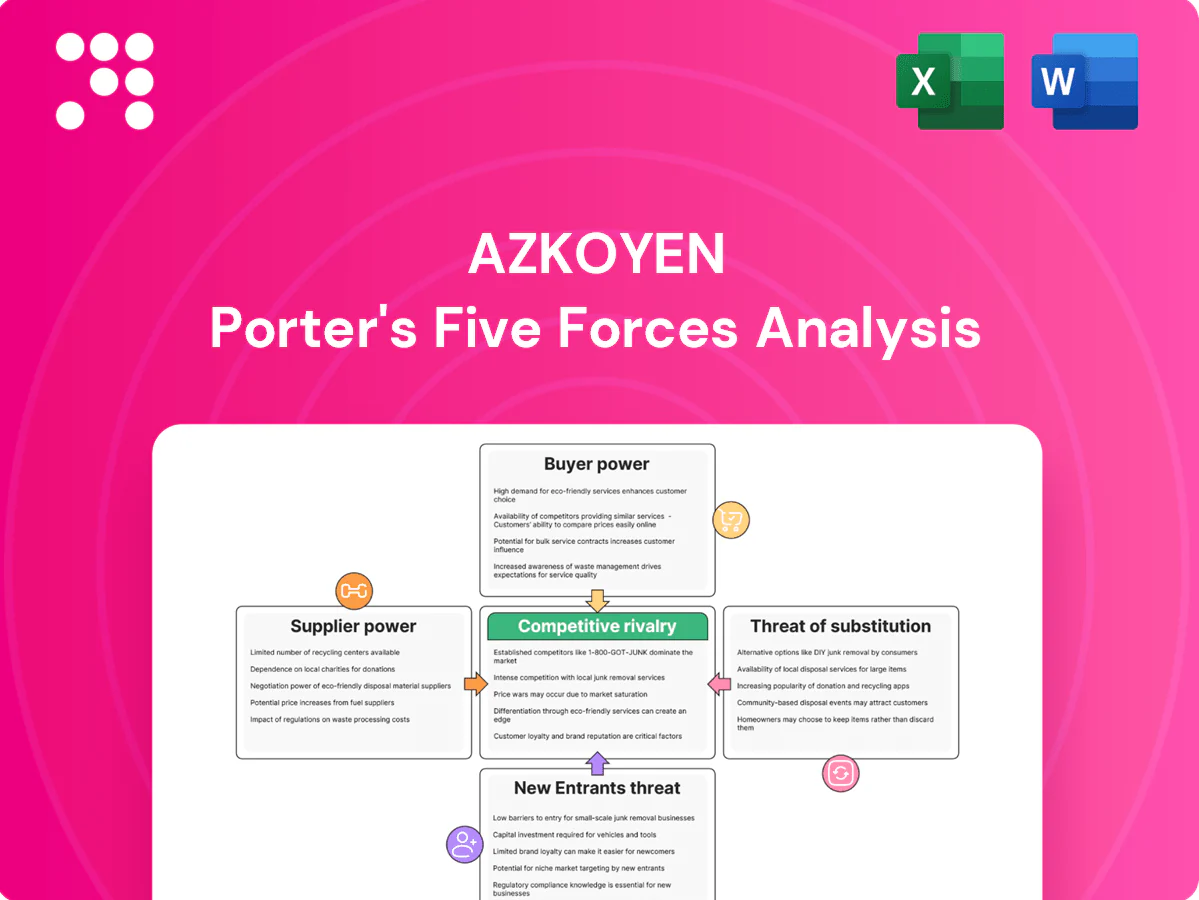

This preview shows the exact Azkoyen Porter's Five Forces Analysis you'll receive after purchase—fully detailed and professionally formatted. The file you see is the final deliverable, ready for immediate download and use. No placeholders, no mockups—what you preview is what you get.

Go Beyond the Preview—Access the Full Strategic Report

Azkoyen faces nuanced competitive pressures across supplier bargaining, buyer power, substitute threats, industry rivalry and entry barriers, shaping margins and growth prospects. This snapshot highlights key tensions but stops short of force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get a consultant-grade, data-driven breakdown tailored to Azkoyen’s strategic decisions.

Suppliers Bargaining Power

Specialized components

Many inputs for payment systems and access control, such as RFID modules and secure chips, are specialized and sourced from a small number of suppliers, concentrating bargaining power and raising switching costs and lead times; qualification cycles are frequently lengthy, typically 12–18 months. Supplier consolidation can drive pricing power and volatility; dual-sourcing mitigates risk but increases qualification cost and inventory needs.

Electronics and semiconductors

Volatile semiconductor cycles drive board, sensor and display price swings and lead times often stretching 12–52 weeks; global semiconductor sales rose from about $556B in 2023 to roughly $588B in 2024 (WSTS), concentrating capacity. Priority allocations favor large OEMs, squeezing mid-cap manufacturers like Azkoyen and forcing 5–15% procurement premiums. Long component lifecycles in industrial gear limit redesign agility, so strategic inventory buffers mitigate shortages but tie up working capital and can raise inventory days by months.

Steel, plastics, and enclosures

Commodity steel and plastics, which comprise roughly 30% of vending-cabinet BOM, are widely available, limiting supplier power; however 2024 container spot rates averaged about $1,200/FEU and industrial energy volatility produced input cost swings often in the 10–25% range. Custom tooling and molds generate partial lock-in with typical lead times of 6–12 months, while regional suppliers can cut currency and freight risk by an estimated 10–20%.

Software and security IP

Licensing for encryption, payment kernels and OS stacks is concentrated among a few IP holders, giving them leverage as compliance updates like PCI and EMV force mandatory upgrades and patches that suppliers control.

Royalties and certification fees raise unit economics for device makers, though firms that invest in in-house software development gradually reduce supplier dependence and recurring costs.

- Concentration: few licensors control core IP

- Compliance leverage: PCI/EMV drive mandatory upgrades

- Cost impact: royalties and certification raise unit COGS

- Mitigation: in-house software lowers long-term dependence

Service and field parts

Aftermarket parts and maintenance kits for Azkoyen are typically sourced from approved suppliers to preserve warranty coverage, which restricts substitution and sustains supplier margins; multi-year service contracts further entrench these supplier relationships while standardizing parts across models can weaken that power.

- Approved suppliers limit substitution

- Service contracts embed relationships

- Standardized parts dilute power

Supply squeeze: chips lead times 12-52w, premiums 5-15%

Supplier power is high for secure chips/RFID and software IP, with qualification cycles of 12–18 months and semiconductor lead times 12–52 weeks; global semiconductor sales rose to about $588B in 2024 (WSTS). Procurement premiums of 5–15% hit mid-cap OEMs; container spot rates averaged ~$1,200/FEU in 2024, raising logistics cost exposure and working-capital needs.

| Factor | 2024 Data |

|---|---|

| Semiconductor market | $588B |

| Lead times | 12–52 weeks |

| Qualification | 12–18 months |

| Procurement premium | 5–15% |

| Container spot rate | $1,200/FEU |

What is included in the product

Tailored Porter's Five Forces for Azkoyen, assessing rival intensity, supplier and buyer power, substitute threats and entry barriers to reveal pricing pressure, profitability levers, and emerging disruptive risks.

A concise, one-sheet Porter's Five Forces for Azkoyen that distills competitive threats, supplier/customer bargaining, substitutes and entry barriers into board-ready insights—speeding strategic decisions and easing stakeholder communication.

Customers Bargaining Power

Consolidated enterprise buyers

Large operators in vending, coffee service, retail, and transit procure machines and consumables in high volumes, enabling aggressive bidding and strict total-cost-of-ownership requirements that compress supplier margins.

Demand for integration

Buyers now expect seamless payment, telemetry and access-control integration, driving demand for end-to-end vendors that lower switching costs by bundling hardware, software and services. The API management market reached about $5.2bn in 2024, enabling multi-sourcing and increasing buyer leverage. Closed ecosystems can retain clients but face growing pushback as buyers favor open standards.

Price sensitivity and ROI

Operators judge payback by uptime, cashless conversion and energy efficiency, typically targeting a sub-24‑month payback to justify deployments. High comparability across machines amplifies price pressure, while service SLAs and financing (often stretched to 30–36 months) are used as bargaining chips. Demonstrable TCO reductions of ~15–25% materially soften buyer power.

Customization requests

Customization requests for validators, readers and cabinets are common, raising switching costs through unique NRE but giving buyers leverage to negotiate NRE discounts; modular platforms can reduce NRE by about 25% while preserving feature flexibility. Delays in bespoke builds have been cited to jeopardize 15%–20% of deals in vending/hospitality bids in 2024.

- Sector-specific parts: validators/readers/cabinets

- Customization increases switching costs yet creates NRE negotiation points

- Modular platforms can cut NRE ~25%

- Bespoke build delays risk ~15%–20% of deals (2024)

Alternative channels

Some buyers consider refurbished or secondary-market vending units, which anchors lower price expectations; global refurbished electronics market surpassed $50 billion in 2024, reinforcing resale benchmarks. Warranty, regulatory compliance, and proprietary software support limit used-equipment appeal for Azkoyen’s cashless and telemetry-enabled machines. Trade-in programs can recapture up to mid-single-digit market share by converting replacement demand into company-controlled refurb inventory.

- Refurbished market size: >$50B (2024)

- Warranty/compliance restricts appeal

- Trade-ins recapture demand

Large buyers force sub-24-month paybacks; open APIs $5.2bn, refurbished $50bn+

Large-volume operators exert strong price and TCO-driven leverage, demanding sub-24-month paybacks; comparable machines and cashless/telemetry expectations increase supplier concessions. Buyers favor open APIs ($5.2bn API mgmt market in 2024) and refurbished benchmarks (> $50bn 2024), using SLAs, financing and NRE negotiations (modular NRE cuts ~25%) to enhance bargaining power.

| Metric | 2024 |

|---|---|

| API market | $5.2bn |

| Refurbished market | >$50bn |

| Modular NRE reduction | ~25% |

| TCO reduction wins | 15–25% |

Preview the Actual Deliverable

Azkoyen Porter's Five Forces Analysis

This preview shows the exact Azkoyen Porter's Five Forces Analysis you'll receive after purchase—fully detailed and professionally formatted. The file you see is the final deliverable, ready for immediate download and use. No placeholders, no mockups—what you preview is what you get.

Description

Go Beyond the Preview—Access the Full Strategic Report

Azkoyen faces nuanced competitive pressures across supplier bargaining, buyer power, substitute threats, industry rivalry and entry barriers, shaping margins and growth prospects. This snapshot highlights key tensions but stops short of force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get a consultant-grade, data-driven breakdown tailored to Azkoyen’s strategic decisions.

Suppliers Bargaining Power

Specialized components

Many inputs for payment systems and access control, such as RFID modules and secure chips, are specialized and sourced from a small number of suppliers, concentrating bargaining power and raising switching costs and lead times; qualification cycles are frequently lengthy, typically 12–18 months. Supplier consolidation can drive pricing power and volatility; dual-sourcing mitigates risk but increases qualification cost and inventory needs.

Electronics and semiconductors

Volatile semiconductor cycles drive board, sensor and display price swings and lead times often stretching 12–52 weeks; global semiconductor sales rose from about $556B in 2023 to roughly $588B in 2024 (WSTS), concentrating capacity. Priority allocations favor large OEMs, squeezing mid-cap manufacturers like Azkoyen and forcing 5–15% procurement premiums. Long component lifecycles in industrial gear limit redesign agility, so strategic inventory buffers mitigate shortages but tie up working capital and can raise inventory days by months.

Steel, plastics, and enclosures

Commodity steel and plastics, which comprise roughly 30% of vending-cabinet BOM, are widely available, limiting supplier power; however 2024 container spot rates averaged about $1,200/FEU and industrial energy volatility produced input cost swings often in the 10–25% range. Custom tooling and molds generate partial lock-in with typical lead times of 6–12 months, while regional suppliers can cut currency and freight risk by an estimated 10–20%.

Software and security IP

Licensing for encryption, payment kernels and OS stacks is concentrated among a few IP holders, giving them leverage as compliance updates like PCI and EMV force mandatory upgrades and patches that suppliers control.

Royalties and certification fees raise unit economics for device makers, though firms that invest in in-house software development gradually reduce supplier dependence and recurring costs.

- Concentration: few licensors control core IP

- Compliance leverage: PCI/EMV drive mandatory upgrades

- Cost impact: royalties and certification raise unit COGS

- Mitigation: in-house software lowers long-term dependence

Service and field parts

Aftermarket parts and maintenance kits for Azkoyen are typically sourced from approved suppliers to preserve warranty coverage, which restricts substitution and sustains supplier margins; multi-year service contracts further entrench these supplier relationships while standardizing parts across models can weaken that power.

- Approved suppliers limit substitution

- Service contracts embed relationships

- Standardized parts dilute power

Supply squeeze: chips lead times 12-52w, premiums 5-15%

Supplier power is high for secure chips/RFID and software IP, with qualification cycles of 12–18 months and semiconductor lead times 12–52 weeks; global semiconductor sales rose to about $588B in 2024 (WSTS). Procurement premiums of 5–15% hit mid-cap OEMs; container spot rates averaged ~$1,200/FEU in 2024, raising logistics cost exposure and working-capital needs.

| Factor | 2024 Data |

|---|---|

| Semiconductor market | $588B |

| Lead times | 12–52 weeks |

| Qualification | 12–18 months |

| Procurement premium | 5–15% |

| Container spot rate | $1,200/FEU |

What is included in the product

Tailored Porter's Five Forces for Azkoyen, assessing rival intensity, supplier and buyer power, substitute threats and entry barriers to reveal pricing pressure, profitability levers, and emerging disruptive risks.

A concise, one-sheet Porter's Five Forces for Azkoyen that distills competitive threats, supplier/customer bargaining, substitutes and entry barriers into board-ready insights—speeding strategic decisions and easing stakeholder communication.

Customers Bargaining Power

Consolidated enterprise buyers

Large operators in vending, coffee service, retail, and transit procure machines and consumables in high volumes, enabling aggressive bidding and strict total-cost-of-ownership requirements that compress supplier margins.

Demand for integration

Buyers now expect seamless payment, telemetry and access-control integration, driving demand for end-to-end vendors that lower switching costs by bundling hardware, software and services. The API management market reached about $5.2bn in 2024, enabling multi-sourcing and increasing buyer leverage. Closed ecosystems can retain clients but face growing pushback as buyers favor open standards.

Price sensitivity and ROI

Operators judge payback by uptime, cashless conversion and energy efficiency, typically targeting a sub-24‑month payback to justify deployments. High comparability across machines amplifies price pressure, while service SLAs and financing (often stretched to 30–36 months) are used as bargaining chips. Demonstrable TCO reductions of ~15–25% materially soften buyer power.

Customization requests

Customization requests for validators, readers and cabinets are common, raising switching costs through unique NRE but giving buyers leverage to negotiate NRE discounts; modular platforms can reduce NRE by about 25% while preserving feature flexibility. Delays in bespoke builds have been cited to jeopardize 15%–20% of deals in vending/hospitality bids in 2024.

- Sector-specific parts: validators/readers/cabinets

- Customization increases switching costs yet creates NRE negotiation points

- Modular platforms can cut NRE ~25%

- Bespoke build delays risk ~15%–20% of deals (2024)

Alternative channels

Some buyers consider refurbished or secondary-market vending units, which anchors lower price expectations; global refurbished electronics market surpassed $50 billion in 2024, reinforcing resale benchmarks. Warranty, regulatory compliance, and proprietary software support limit used-equipment appeal for Azkoyen’s cashless and telemetry-enabled machines. Trade-in programs can recapture up to mid-single-digit market share by converting replacement demand into company-controlled refurb inventory.

- Refurbished market size: >$50B (2024)

- Warranty/compliance restricts appeal

- Trade-ins recapture demand

Large buyers force sub-24-month paybacks; open APIs $5.2bn, refurbished $50bn+

Large-volume operators exert strong price and TCO-driven leverage, demanding sub-24-month paybacks; comparable machines and cashless/telemetry expectations increase supplier concessions. Buyers favor open APIs ($5.2bn API mgmt market in 2024) and refurbished benchmarks (> $50bn 2024), using SLAs, financing and NRE negotiations (modular NRE cuts ~25%) to enhance bargaining power.

| Metric | 2024 |

|---|---|

| API market | $5.2bn |

| Refurbished market | >$50bn |

| Modular NRE reduction | ~25% |

| TCO reduction wins | 15–25% |

Preview the Actual Deliverable

Azkoyen Porter's Five Forces Analysis

This preview shows the exact Azkoyen Porter's Five Forces Analysis you'll receive after purchase—fully detailed and professionally formatted. The file you see is the final deliverable, ready for immediate download and use. No placeholders, no mockups—what you preview is what you get.