B2Gold Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

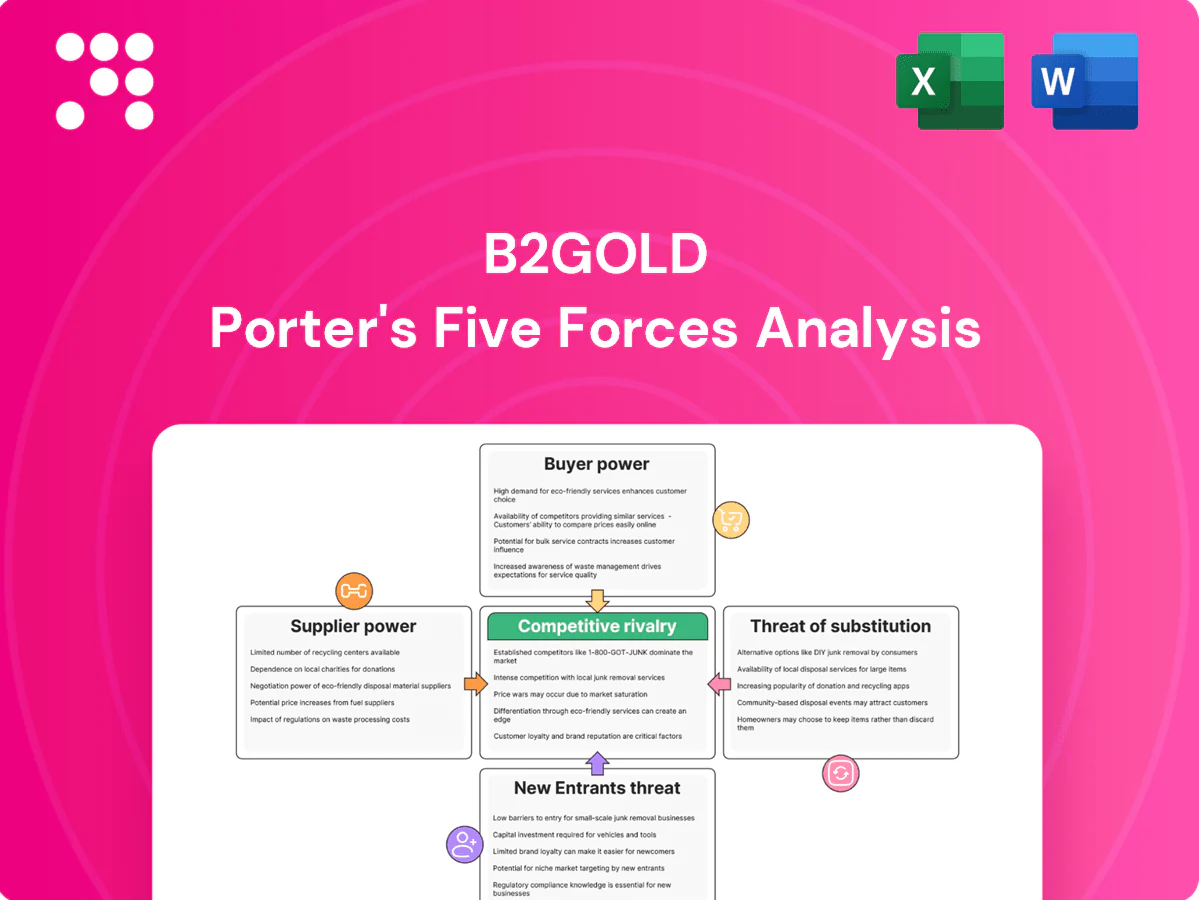

B2Gold's Porter's Five Forces snapshot shows moderate supplier power, commoditized buyer dynamics, intense rivalry among miners, limited substitutes, and barriers that restrain new entrants. These forces critically influence margins, project economics, and capital allocation across its assets. This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated critical inputs

Mining relies on a handful of global suppliers for explosives, cyanide, grinding media and OEM equipment, concentrating supplier leverage; limited substitutes and strict specs make switching costly and risky. Disruption at key vendors can halt throughput and force stockpile drawdowns. B2Gold mitigates risk through multi-sourcing and inventory buffers, but supplier depth remains thin in its remote operating regions.

Energy and fuel exposure

Diesel and power represent a material portion of B2Gold’s cash costs, with Brent averaging about 86 USD/bbl in 2024, driving volatile fuel-linked input prices. In Mali and Namibia heavy on-site diesel generation and constrained grids increase dependence on fuel suppliers and logistics. Fixed contracts can cap spikes but cannot eliminate pass-through risk to operating costs. Local currency moves (e.g., ZAR volatility for Namibia) can amplify domestic energy expense.

Logistics and remoteness

In 2024 B2Gold operations at Fekola (Mali), Otjikoto (Namibia) and Masbate (Philippines) face long supply chains and limited transport options, amplifying supplier bargaining power. Port congestion, seasonal weather and regional security constraints further restrict alternatives and raise costs. Maintaining inventory buffers mitigates disruption but ties up working capital. Freight providers and customs brokers gain leverage where logistics alternatives are scarce.

Skilled labor and contractors

Regulatory-linked inputs

Chemicals, explosives and environmental services for B2Gold are subject to strict regulatory regimes that sharply narrow the pool of qualified suppliers, constraining sourcing flexibility. Permit and compliance conditions often specify approved vendors or standards, making rapid supplier switching impractical and costly. This regulatory tie-in institutionalizes supplier leverage over prices and project timelines.

- Tightly regulated inputs reduce supplier pool

- Compliance limits rapid switching

- Permits can mandate specific vendors/standards

- Supplier control raises pricing and timing risk

Concentrated vendors and fuel volatility force higher cash costs and capital lock

Supplier power is high: concentrated global vendors for explosives, cyanide and OEMs, limited substitutes and strict specs raise switching costs. 2024 Brent ~86 USD/bbl and tight regional labor pushed input cost volatility and contractor premiums. Remote sites (Mali, Namibia, Philippines) and regulatory vendor lists amplify leverage; inventories and multi-sourcing mitigate but lock capital.

| Input | 2024 metric | Impact |

|---|---|---|

| Fuel | Brent ~86 USD/bbl | Higher cash costs, logistics risk |

| Labor/Contractors | Tighter 2024 market | Premium rates |

| Specialist supplies | Few approved vendors | Switching costly |

What is included in the product

Provides a tailored Porter's Five Forces overview for B2Gold, uncovering competitive pressures from rivals, substitutes, suppliers, buyers, and potential entrants. Highlights disruptive threats, pricing leverage, entry barriers and strategic implications for investors, advisors, and internal strategy use.

A one-sheet Porter's Five Forces for B2Gold—rapidly highlights competitive pressures, supplier/buyer leverage, substitution threats and entry risks so you can spot strategic pain points and act decisively.

Customers Bargaining Power

Commodity pricing limits leverage

Gold is sold into a deep, liquid market where the LBMA price, set via twice-daily USD auctions, benchmarks realization; individual buyers such as refiners and bullion banks therefore have limited leverage over spot pricing. Assay and quality terms affect payability but rarely displace LBMA-linked settlement. B2Gold’s dore is marketed under standardized contract structures aligned to LBMA settlement conventions.

Diversified buyer base

B2Gold sells to multiple refiners and traders across geographies, giving the company optionality that reduces dependence on any single customer. Switching among accredited counterparties is relatively straightforward due to industry-standard contracts and common accreditation. Credit risk is mitigated through established reputable offtakers and the use of trade finance facilities. This diversified buyer base weakens customer bargaining power.

Specification and assay terms

Buyers can dictate penalties and premiums through impurity specs and settlement clauses, with assay disputes known to delay cash receipts by days to weeks and effectively nudging realized prices; in 2024 the average London gold fix was about $2,150/oz, amplifying the dollar impact of small discounts. Strong metallurgical control at B2Gold narrows discounts, while long relationships standardize terms and speed settlements.

ESG and chain-of-custody demands

- LBMA and OECD standards required

- Non-compliance: exclusion/penalties

- High-risk jurisdictions: increased audits

- Strong ESG: protects market breadth

Hedging and sales flexibility

B2Gold relies mainly on spot sales with a minimal hedge book entering 2024, and occasional streaming or royalty structures that shift price risk and buyer influence; structured contracts can trade price certainty for greater counterparty say. Flexibility across offtakers and the gold market liquidity (global spot market >$300bn/day) limits sustained buyer power.

- 2024 production guidance ~880,000 oz

- Minimal hedging increases spot exposure

- Streaming/royalty can reduce upfront risk

- High market liquidity enables rapid re-marketing

LBMA liquidity limits buyer power - 2024 London fix ~2,150 USD/oz

Buyers have limited pricing power due to deep LBMA-linked liquidity (2024 London fix ~2,150 USD/oz) and global spot turnover >300bn USD/day. B2Gold’s diversified offtakers, minimal hedge book and 2024 guidance ~880,000 oz reduce single-buyer dependence. ESG/OECD compliance is required to avoid exclusions and pricing penalties.

| Metric | 2024 |

|---|---|

| London fix | ~2,150 USD/oz |

| Spot market turnover | >300 bn USD/day |

| Production guidance | ~880,000 oz |

Preview the Actual Deliverable

B2Gold Porter's Five Forces Analysis

This preview presents the B2Gold Porter's Five Forces Analysis exactly as delivered—comprehensive, professionally formatted and ready for immediate download after purchase. You’re viewing the final document, with no placeholders or sample content, and it’s the same file you’ll receive upon payment.

Go Beyond the Preview—Access the Full Strategic Report

B2Gold's Porter's Five Forces snapshot shows moderate supplier power, commoditized buyer dynamics, intense rivalry among miners, limited substitutes, and barriers that restrain new entrants. These forces critically influence margins, project economics, and capital allocation across its assets. This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated critical inputs

Mining relies on a handful of global suppliers for explosives, cyanide, grinding media and OEM equipment, concentrating supplier leverage; limited substitutes and strict specs make switching costly and risky. Disruption at key vendors can halt throughput and force stockpile drawdowns. B2Gold mitigates risk through multi-sourcing and inventory buffers, but supplier depth remains thin in its remote operating regions.

Energy and fuel exposure

Diesel and power represent a material portion of B2Gold’s cash costs, with Brent averaging about 86 USD/bbl in 2024, driving volatile fuel-linked input prices. In Mali and Namibia heavy on-site diesel generation and constrained grids increase dependence on fuel suppliers and logistics. Fixed contracts can cap spikes but cannot eliminate pass-through risk to operating costs. Local currency moves (e.g., ZAR volatility for Namibia) can amplify domestic energy expense.

Logistics and remoteness

In 2024 B2Gold operations at Fekola (Mali), Otjikoto (Namibia) and Masbate (Philippines) face long supply chains and limited transport options, amplifying supplier bargaining power. Port congestion, seasonal weather and regional security constraints further restrict alternatives and raise costs. Maintaining inventory buffers mitigates disruption but ties up working capital. Freight providers and customs brokers gain leverage where logistics alternatives are scarce.

Skilled labor and contractors

Regulatory-linked inputs

Chemicals, explosives and environmental services for B2Gold are subject to strict regulatory regimes that sharply narrow the pool of qualified suppliers, constraining sourcing flexibility. Permit and compliance conditions often specify approved vendors or standards, making rapid supplier switching impractical and costly. This regulatory tie-in institutionalizes supplier leverage over prices and project timelines.

- Tightly regulated inputs reduce supplier pool

- Compliance limits rapid switching

- Permits can mandate specific vendors/standards

- Supplier control raises pricing and timing risk

Concentrated vendors and fuel volatility force higher cash costs and capital lock

Supplier power is high: concentrated global vendors for explosives, cyanide and OEMs, limited substitutes and strict specs raise switching costs. 2024 Brent ~86 USD/bbl and tight regional labor pushed input cost volatility and contractor premiums. Remote sites (Mali, Namibia, Philippines) and regulatory vendor lists amplify leverage; inventories and multi-sourcing mitigate but lock capital.

| Input | 2024 metric | Impact |

|---|---|---|

| Fuel | Brent ~86 USD/bbl | Higher cash costs, logistics risk |

| Labor/Contractors | Tighter 2024 market | Premium rates |

| Specialist supplies | Few approved vendors | Switching costly |

What is included in the product

Provides a tailored Porter's Five Forces overview for B2Gold, uncovering competitive pressures from rivals, substitutes, suppliers, buyers, and potential entrants. Highlights disruptive threats, pricing leverage, entry barriers and strategic implications for investors, advisors, and internal strategy use.

A one-sheet Porter's Five Forces for B2Gold—rapidly highlights competitive pressures, supplier/buyer leverage, substitution threats and entry risks so you can spot strategic pain points and act decisively.

Customers Bargaining Power

Commodity pricing limits leverage

Gold is sold into a deep, liquid market where the LBMA price, set via twice-daily USD auctions, benchmarks realization; individual buyers such as refiners and bullion banks therefore have limited leverage over spot pricing. Assay and quality terms affect payability but rarely displace LBMA-linked settlement. B2Gold’s dore is marketed under standardized contract structures aligned to LBMA settlement conventions.

Diversified buyer base

B2Gold sells to multiple refiners and traders across geographies, giving the company optionality that reduces dependence on any single customer. Switching among accredited counterparties is relatively straightforward due to industry-standard contracts and common accreditation. Credit risk is mitigated through established reputable offtakers and the use of trade finance facilities. This diversified buyer base weakens customer bargaining power.

Specification and assay terms

Buyers can dictate penalties and premiums through impurity specs and settlement clauses, with assay disputes known to delay cash receipts by days to weeks and effectively nudging realized prices; in 2024 the average London gold fix was about $2,150/oz, amplifying the dollar impact of small discounts. Strong metallurgical control at B2Gold narrows discounts, while long relationships standardize terms and speed settlements.

ESG and chain-of-custody demands

- LBMA and OECD standards required

- Non-compliance: exclusion/penalties

- High-risk jurisdictions: increased audits

- Strong ESG: protects market breadth

Hedging and sales flexibility

B2Gold relies mainly on spot sales with a minimal hedge book entering 2024, and occasional streaming or royalty structures that shift price risk and buyer influence; structured contracts can trade price certainty for greater counterparty say. Flexibility across offtakers and the gold market liquidity (global spot market >$300bn/day) limits sustained buyer power.

- 2024 production guidance ~880,000 oz

- Minimal hedging increases spot exposure

- Streaming/royalty can reduce upfront risk

- High market liquidity enables rapid re-marketing

LBMA liquidity limits buyer power - 2024 London fix ~2,150 USD/oz

Buyers have limited pricing power due to deep LBMA-linked liquidity (2024 London fix ~2,150 USD/oz) and global spot turnover >300bn USD/day. B2Gold’s diversified offtakers, minimal hedge book and 2024 guidance ~880,000 oz reduce single-buyer dependence. ESG/OECD compliance is required to avoid exclusions and pricing penalties.

| Metric | 2024 |

|---|---|

| London fix | ~2,150 USD/oz |

| Spot market turnover | >300 bn USD/day |

| Production guidance | ~880,000 oz |

Preview the Actual Deliverable

B2Gold Porter's Five Forces Analysis

This preview presents the B2Gold Porter's Five Forces Analysis exactly as delivered—comprehensive, professionally formatted and ready for immediate download after purchase. You’re viewing the final document, with no placeholders or sample content, and it’s the same file you’ll receive upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

B2Gold's Porter's Five Forces snapshot shows moderate supplier power, commoditized buyer dynamics, intense rivalry among miners, limited substitutes, and barriers that restrain new entrants. These forces critically influence margins, project economics, and capital allocation across its assets. This brief preview only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Concentrated critical inputs

Mining relies on a handful of global suppliers for explosives, cyanide, grinding media and OEM equipment, concentrating supplier leverage; limited substitutes and strict specs make switching costly and risky. Disruption at key vendors can halt throughput and force stockpile drawdowns. B2Gold mitigates risk through multi-sourcing and inventory buffers, but supplier depth remains thin in its remote operating regions.

Energy and fuel exposure

Diesel and power represent a material portion of B2Gold’s cash costs, with Brent averaging about 86 USD/bbl in 2024, driving volatile fuel-linked input prices. In Mali and Namibia heavy on-site diesel generation and constrained grids increase dependence on fuel suppliers and logistics. Fixed contracts can cap spikes but cannot eliminate pass-through risk to operating costs. Local currency moves (e.g., ZAR volatility for Namibia) can amplify domestic energy expense.

Logistics and remoteness

In 2024 B2Gold operations at Fekola (Mali), Otjikoto (Namibia) and Masbate (Philippines) face long supply chains and limited transport options, amplifying supplier bargaining power. Port congestion, seasonal weather and regional security constraints further restrict alternatives and raise costs. Maintaining inventory buffers mitigates disruption but ties up working capital. Freight providers and customs brokers gain leverage where logistics alternatives are scarce.

Skilled labor and contractors

Regulatory-linked inputs

Chemicals, explosives and environmental services for B2Gold are subject to strict regulatory regimes that sharply narrow the pool of qualified suppliers, constraining sourcing flexibility. Permit and compliance conditions often specify approved vendors or standards, making rapid supplier switching impractical and costly. This regulatory tie-in institutionalizes supplier leverage over prices and project timelines.

- Tightly regulated inputs reduce supplier pool

- Compliance limits rapid switching

- Permits can mandate specific vendors/standards

- Supplier control raises pricing and timing risk

Concentrated vendors and fuel volatility force higher cash costs and capital lock

Supplier power is high: concentrated global vendors for explosives, cyanide and OEMs, limited substitutes and strict specs raise switching costs. 2024 Brent ~86 USD/bbl and tight regional labor pushed input cost volatility and contractor premiums. Remote sites (Mali, Namibia, Philippines) and regulatory vendor lists amplify leverage; inventories and multi-sourcing mitigate but lock capital.

| Input | 2024 metric | Impact |

|---|---|---|

| Fuel | Brent ~86 USD/bbl | Higher cash costs, logistics risk |

| Labor/Contractors | Tighter 2024 market | Premium rates |

| Specialist supplies | Few approved vendors | Switching costly |

What is included in the product

Provides a tailored Porter's Five Forces overview for B2Gold, uncovering competitive pressures from rivals, substitutes, suppliers, buyers, and potential entrants. Highlights disruptive threats, pricing leverage, entry barriers and strategic implications for investors, advisors, and internal strategy use.

A one-sheet Porter's Five Forces for B2Gold—rapidly highlights competitive pressures, supplier/buyer leverage, substitution threats and entry risks so you can spot strategic pain points and act decisively.

Customers Bargaining Power

Commodity pricing limits leverage

Gold is sold into a deep, liquid market where the LBMA price, set via twice-daily USD auctions, benchmarks realization; individual buyers such as refiners and bullion banks therefore have limited leverage over spot pricing. Assay and quality terms affect payability but rarely displace LBMA-linked settlement. B2Gold’s dore is marketed under standardized contract structures aligned to LBMA settlement conventions.

Diversified buyer base

B2Gold sells to multiple refiners and traders across geographies, giving the company optionality that reduces dependence on any single customer. Switching among accredited counterparties is relatively straightforward due to industry-standard contracts and common accreditation. Credit risk is mitigated through established reputable offtakers and the use of trade finance facilities. This diversified buyer base weakens customer bargaining power.

Specification and assay terms

Buyers can dictate penalties and premiums through impurity specs and settlement clauses, with assay disputes known to delay cash receipts by days to weeks and effectively nudging realized prices; in 2024 the average London gold fix was about $2,150/oz, amplifying the dollar impact of small discounts. Strong metallurgical control at B2Gold narrows discounts, while long relationships standardize terms and speed settlements.

ESG and chain-of-custody demands

- LBMA and OECD standards required

- Non-compliance: exclusion/penalties

- High-risk jurisdictions: increased audits

- Strong ESG: protects market breadth

Hedging and sales flexibility

B2Gold relies mainly on spot sales with a minimal hedge book entering 2024, and occasional streaming or royalty structures that shift price risk and buyer influence; structured contracts can trade price certainty for greater counterparty say. Flexibility across offtakers and the gold market liquidity (global spot market >$300bn/day) limits sustained buyer power.

- 2024 production guidance ~880,000 oz

- Minimal hedging increases spot exposure

- Streaming/royalty can reduce upfront risk

- High market liquidity enables rapid re-marketing

LBMA liquidity limits buyer power - 2024 London fix ~2,150 USD/oz

Buyers have limited pricing power due to deep LBMA-linked liquidity (2024 London fix ~2,150 USD/oz) and global spot turnover >300bn USD/day. B2Gold’s diversified offtakers, minimal hedge book and 2024 guidance ~880,000 oz reduce single-buyer dependence. ESG/OECD compliance is required to avoid exclusions and pricing penalties.

| Metric | 2024 |

|---|---|

| London fix | ~2,150 USD/oz |

| Spot market turnover | >300 bn USD/day |

| Production guidance | ~880,000 oz |

Preview the Actual Deliverable

B2Gold Porter's Five Forces Analysis

This preview presents the B2Gold Porter's Five Forces Analysis exactly as delivered—comprehensive, professionally formatted and ready for immediate download after purchase. You’re viewing the final document, with no placeholders or sample content, and it’s the same file you’ll receive upon payment.