BAE System Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

BAE Systems faces intense industry rivalry, powerful governments as buyers, concentrated suppliers for specialized tech, high barriers to new entrants but evolving substitute threats from dual-use tech and cyber solutions. This snapshot highlights key pressures shaping strategy and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Specialized inputs concentration

BAE relies on scarce suppliers for advanced semiconductors, composites, radars and propulsion, with advanced-node foundry capacity concentrated (TSMC ~54% of global foundry revenue in 2023–24), tightening supply for defense chips. Qualification and security clearances shrink approved vendor pools, increasing supplier leverage. Single-source components create bottlenecks and price stickiness, with specialty lead times reported up to 52 weeks. Dual-sourcing is constrained by costly recertification and performance risks.

High switching and certification costs

Switching a critical supplier for BAE can require 2–5 years of testing, airworthiness certification and ITAR requalification, creating multi‑million sunk costs that heighten dependence on incumbents. These sunk costs and lengthy requalification windows amplify supplier leverage, as program delays translate into higher escalation risk and schedule penalties. Long design lives of 20–40 years lock programs into established parts ecosystems, further entrenching supplier bargaining power.

Mitigating via LTAs and vertical partnerships

BAE mitigates supplier power through long-term agreements, risk-sharing and supplier development to stabilize pricing and capacity. Strategic inventory, design-for-multi-sourcing and dual-sourcing reduce disruption risk. Co-investment and performance-based logistics align incentives and improve uptime. Critical, single-source components remain hard to multi-source, leaving residual supplier leverage.

Geopolitical and materials exposure

Rare earths, specialty alloys and chokepoints raise supplier leverage for BAE; China accounted for about 60% of global refined rare-earth production in 2024, concentrating upstream risk. 2023–24 export controls and sanctions have already curtailed alternative sources, while logistics bottlenecks and rising cyber incidents among tier-2/3 vendors increase fragility and allow suppliers to price risk premia.

- 60%: China share of refined rare-earths (2024)

- Export controls: tightened 2023–24, reducing alternatives

- Tier-2/3 fragility: logistics + cyber breaches rising

- Suppliers embed risk premia, boosting bargaining power

Digital and IP lock-in

Proprietary tooling, firmware and bespoke test benches create strong digital and IP lock-in for BAE Systems, concentrating leverage with a small set of subsystem suppliers; BAE reported group revenue of about £24.6bn in 2024, amplifying the cost impact of supplier constraints. Data rights and software keys limit integration flexibility, while obsolescence management often requires OEM cooperation, increasing supplier bargaining power.

- Proprietary tooling => vendor lock-in

- Data rights/software keys => constrained integration

- OEM cooperation needed => obsolescence risk

- 2024 revenue context => higher supplier leverage

Suppliers wield outsized leverage: scarce chips, 52-week lead times, 2-5yr recert risk

Suppliers hold high leverage over BAE due to scarce advanced chips, single‑source subs, long qual times (2–5 years) and 52‑week lead times, raising delay and cost risk. Long program lives and IP/tooling lock‑in deepen dependence despite long‑term contracts and co‑investment. Concentrated upstream supply (TSMC ~54% foundry; China ~60% rare‑earths) sustains supplier price premia.

| Metric | Value |

|---|---|

| BAE revenue (2024) | £24.6bn |

| TSMC share (2023–24) | ~54% |

| China refined rare‑earths (2024) | ~60% |

| Max lead time | 52 weeks |

| Switching/recert | 2–5 years |

What is included in the product

Tailored Porter's Five Forces analysis for BAE Systems that uncovers key drivers of competition, supplier and buyer power, threat of new entrants and substitutes, and intensity of rivalry. Identifies disruptive technologies, regulatory and defense procurement dynamics shaping pricing, margins, and strategic positioning.

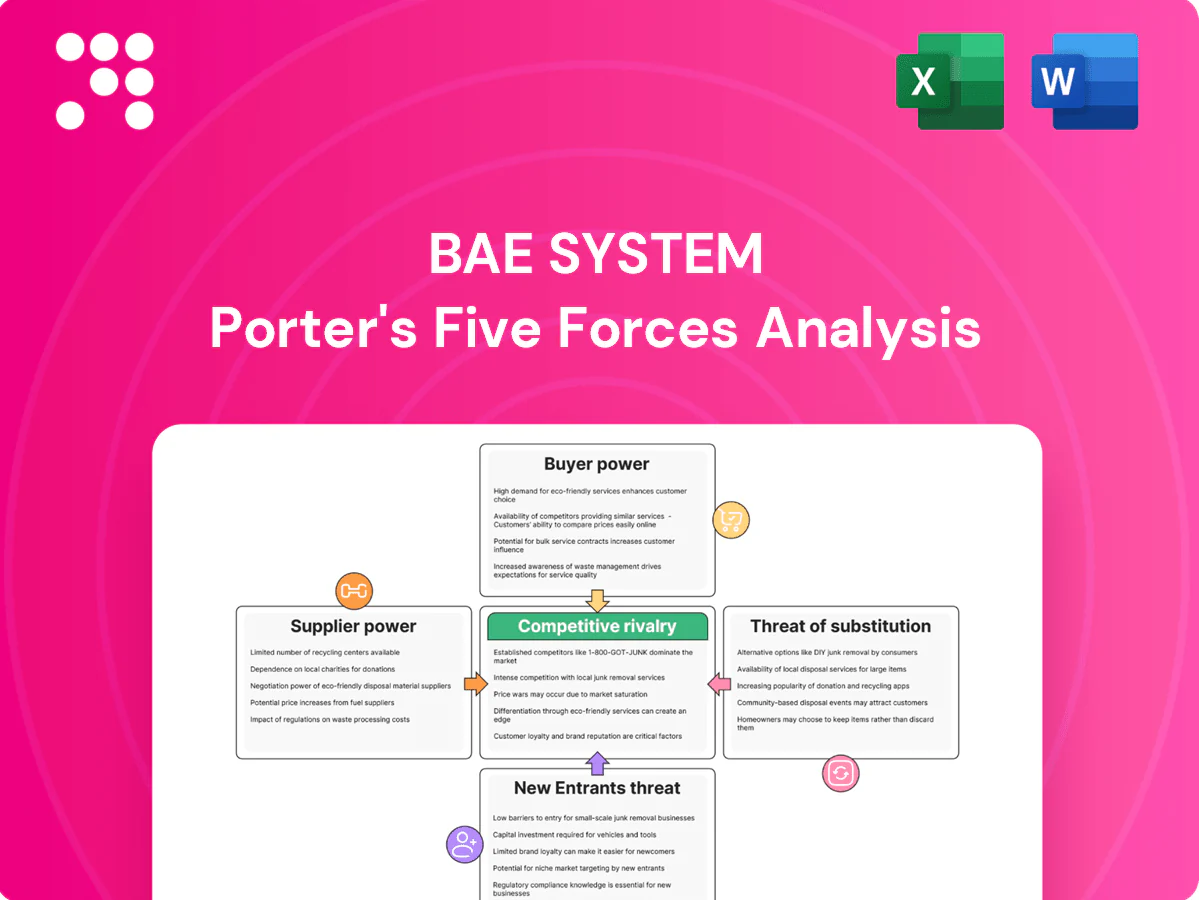

One-sheet Porter's Five Forces for BAE Systems — instantly visualize competitive pressure across suppliers, buyers, new entrants, substitutes and rivalry with a customizable radar chart to support rapid strategic decisions.

Customers Bargaining Power

Government monopsony dynamics

National governments and defense ministries dominate demand in the sector, with global military spending at about $2.24 trillion in 2023 (SIPRI), concentrating buying power in a few state customers. Budgetary oversight, capability roadmaps and parliamentary approval shape contract terms and payment profiles. Political shifts can delay or cancel programs, giving buyers strong leverage over suppliers despite multi-year lead times.

Competitive tendering and pricing pressure

Intense RFP cycles, down-selects and should-cost reviews compress margins for BAE as programs compete for a finite pool of spending (US FY2024 defence budget $858bn). Fixed-price and performance-based contracts increasingly shift cost risk to BAE, reducing upside on cost overruns. Open-architecture mandates lower proprietary rents by forcing interoperability. Bid protests and audits (GAO/DOJ scrutiny) further discipline bid pricing and acceptance.

Offsets and localization demands

Buyers increasingly demand industrial participation, tech transfer and local content—offsets commonly exceed 30% in major sovereign deals—forcing BAE to build local supply chains and joint ventures. These requirements raise delivery complexity and program cost, dilute IP advantages and constrain pricing and contract flexibility. Compliance is often mandatory to secure sovereign programs, affecting margins and capital allocation.

Lifecycle and sustainment lock-in

Once fielded, platforms require decades of upgrades and MRO, and technical data packages plus certification create sustainment lock-in that reduces buyer power; lifecycle sustainment can account for up to 70% of total platform cost (2024). Governments increasingly mandate open systems (US DoD, NATO allies) to foster competition, partially restoring buyer leverage.

- Decades-long MRO drives incumbency

- Technical data/ certification = leverage

- Up to 70% lifecycle cost in sustainment (2024)

- Policy shift: open systems to boost competition

Budget cycles and multi-year buys

Funding volatility — exemplified by the US FY2024 defense budget of about $858bn — creates volume uncertainty and prompts contract renegotiation, while multi-year and framework buys stabilize demand and reduce supplier risk; buyers often accept price concessions in exchange for schedule and availability guarantees, leaving net buyer power high but varying by program criticality.

- Multi-year buys: stabilize supply

- Renegotiation: driven by funding volatility

- Trade-offs: price vs schedule guarantees

- Buyer power: high, program-dependent

Government Buyers Dominate Defense Procurement: High Oversight, Tight Margins, Big Sustainment

Governments concentrate buying power (global military spend $2.24T 2023; US FY2024 $858B), giving buyers leverage via budgets, oversight and program cancellations. RFPs, fixed-price contracts and open-architecture mandates compress margins; offsets often exceed 30% and sustainment can be up to 70% of lifecycle costs (2024). Buyer power is high but varies by program criticality.

| Metric | Value |

|---|---|

| Global military spend (2023) | $2.24T |

| US FY2024 budget | $858B |

| Offsets | >30% |

| Sustainment share | Up to 70% (2024) |

Preview Before You Purchase

BAE System Porter's Five Forces Analysis

This preview shows the exact BAE Systems Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the full, professionally formatted document ready for download and use the moment you buy. The file covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights.

Go Beyond the Preview—Access the Full Strategic Report

BAE Systems faces intense industry rivalry, powerful governments as buyers, concentrated suppliers for specialized tech, high barriers to new entrants but evolving substitute threats from dual-use tech and cyber solutions. This snapshot highlights key pressures shaping strategy and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Specialized inputs concentration

BAE relies on scarce suppliers for advanced semiconductors, composites, radars and propulsion, with advanced-node foundry capacity concentrated (TSMC ~54% of global foundry revenue in 2023–24), tightening supply for defense chips. Qualification and security clearances shrink approved vendor pools, increasing supplier leverage. Single-source components create bottlenecks and price stickiness, with specialty lead times reported up to 52 weeks. Dual-sourcing is constrained by costly recertification and performance risks.

High switching and certification costs

Switching a critical supplier for BAE can require 2–5 years of testing, airworthiness certification and ITAR requalification, creating multi‑million sunk costs that heighten dependence on incumbents. These sunk costs and lengthy requalification windows amplify supplier leverage, as program delays translate into higher escalation risk and schedule penalties. Long design lives of 20–40 years lock programs into established parts ecosystems, further entrenching supplier bargaining power.

Mitigating via LTAs and vertical partnerships

BAE mitigates supplier power through long-term agreements, risk-sharing and supplier development to stabilize pricing and capacity. Strategic inventory, design-for-multi-sourcing and dual-sourcing reduce disruption risk. Co-investment and performance-based logistics align incentives and improve uptime. Critical, single-source components remain hard to multi-source, leaving residual supplier leverage.

Geopolitical and materials exposure

Rare earths, specialty alloys and chokepoints raise supplier leverage for BAE; China accounted for about 60% of global refined rare-earth production in 2024, concentrating upstream risk. 2023–24 export controls and sanctions have already curtailed alternative sources, while logistics bottlenecks and rising cyber incidents among tier-2/3 vendors increase fragility and allow suppliers to price risk premia.

- 60%: China share of refined rare-earths (2024)

- Export controls: tightened 2023–24, reducing alternatives

- Tier-2/3 fragility: logistics + cyber breaches rising

- Suppliers embed risk premia, boosting bargaining power

Digital and IP lock-in

Proprietary tooling, firmware and bespoke test benches create strong digital and IP lock-in for BAE Systems, concentrating leverage with a small set of subsystem suppliers; BAE reported group revenue of about £24.6bn in 2024, amplifying the cost impact of supplier constraints. Data rights and software keys limit integration flexibility, while obsolescence management often requires OEM cooperation, increasing supplier bargaining power.

- Proprietary tooling => vendor lock-in

- Data rights/software keys => constrained integration

- OEM cooperation needed => obsolescence risk

- 2024 revenue context => higher supplier leverage

Suppliers wield outsized leverage: scarce chips, 52-week lead times, 2-5yr recert risk

Suppliers hold high leverage over BAE due to scarce advanced chips, single‑source subs, long qual times (2–5 years) and 52‑week lead times, raising delay and cost risk. Long program lives and IP/tooling lock‑in deepen dependence despite long‑term contracts and co‑investment. Concentrated upstream supply (TSMC ~54% foundry; China ~60% rare‑earths) sustains supplier price premia.

| Metric | Value |

|---|---|

| BAE revenue (2024) | £24.6bn |

| TSMC share (2023–24) | ~54% |

| China refined rare‑earths (2024) | ~60% |

| Max lead time | 52 weeks |

| Switching/recert | 2–5 years |

What is included in the product

Tailored Porter's Five Forces analysis for BAE Systems that uncovers key drivers of competition, supplier and buyer power, threat of new entrants and substitutes, and intensity of rivalry. Identifies disruptive technologies, regulatory and defense procurement dynamics shaping pricing, margins, and strategic positioning.

One-sheet Porter's Five Forces for BAE Systems — instantly visualize competitive pressure across suppliers, buyers, new entrants, substitutes and rivalry with a customizable radar chart to support rapid strategic decisions.

Customers Bargaining Power

Government monopsony dynamics

National governments and defense ministries dominate demand in the sector, with global military spending at about $2.24 trillion in 2023 (SIPRI), concentrating buying power in a few state customers. Budgetary oversight, capability roadmaps and parliamentary approval shape contract terms and payment profiles. Political shifts can delay or cancel programs, giving buyers strong leverage over suppliers despite multi-year lead times.

Competitive tendering and pricing pressure

Intense RFP cycles, down-selects and should-cost reviews compress margins for BAE as programs compete for a finite pool of spending (US FY2024 defence budget $858bn). Fixed-price and performance-based contracts increasingly shift cost risk to BAE, reducing upside on cost overruns. Open-architecture mandates lower proprietary rents by forcing interoperability. Bid protests and audits (GAO/DOJ scrutiny) further discipline bid pricing and acceptance.

Offsets and localization demands

Buyers increasingly demand industrial participation, tech transfer and local content—offsets commonly exceed 30% in major sovereign deals—forcing BAE to build local supply chains and joint ventures. These requirements raise delivery complexity and program cost, dilute IP advantages and constrain pricing and contract flexibility. Compliance is often mandatory to secure sovereign programs, affecting margins and capital allocation.

Lifecycle and sustainment lock-in

Once fielded, platforms require decades of upgrades and MRO, and technical data packages plus certification create sustainment lock-in that reduces buyer power; lifecycle sustainment can account for up to 70% of total platform cost (2024). Governments increasingly mandate open systems (US DoD, NATO allies) to foster competition, partially restoring buyer leverage.

- Decades-long MRO drives incumbency

- Technical data/ certification = leverage

- Up to 70% lifecycle cost in sustainment (2024)

- Policy shift: open systems to boost competition

Budget cycles and multi-year buys

Funding volatility — exemplified by the US FY2024 defense budget of about $858bn — creates volume uncertainty and prompts contract renegotiation, while multi-year and framework buys stabilize demand and reduce supplier risk; buyers often accept price concessions in exchange for schedule and availability guarantees, leaving net buyer power high but varying by program criticality.

- Multi-year buys: stabilize supply

- Renegotiation: driven by funding volatility

- Trade-offs: price vs schedule guarantees

- Buyer power: high, program-dependent

Government Buyers Dominate Defense Procurement: High Oversight, Tight Margins, Big Sustainment

Governments concentrate buying power (global military spend $2.24T 2023; US FY2024 $858B), giving buyers leverage via budgets, oversight and program cancellations. RFPs, fixed-price contracts and open-architecture mandates compress margins; offsets often exceed 30% and sustainment can be up to 70% of lifecycle costs (2024). Buyer power is high but varies by program criticality.

| Metric | Value |

|---|---|

| Global military spend (2023) | $2.24T |

| US FY2024 budget | $858B |

| Offsets | >30% |

| Sustainment share | Up to 70% (2024) |

Preview Before You Purchase

BAE System Porter's Five Forces Analysis

This preview shows the exact BAE Systems Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the full, professionally formatted document ready for download and use the moment you buy. The file covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

BAE Systems faces intense industry rivalry, powerful governments as buyers, concentrated suppliers for specialized tech, high barriers to new entrants but evolving substitute threats from dual-use tech and cyber solutions. This snapshot highlights key pressures shaping strategy and margins. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Specialized inputs concentration

BAE relies on scarce suppliers for advanced semiconductors, composites, radars and propulsion, with advanced-node foundry capacity concentrated (TSMC ~54% of global foundry revenue in 2023–24), tightening supply for defense chips. Qualification and security clearances shrink approved vendor pools, increasing supplier leverage. Single-source components create bottlenecks and price stickiness, with specialty lead times reported up to 52 weeks. Dual-sourcing is constrained by costly recertification and performance risks.

High switching and certification costs

Switching a critical supplier for BAE can require 2–5 years of testing, airworthiness certification and ITAR requalification, creating multi‑million sunk costs that heighten dependence on incumbents. These sunk costs and lengthy requalification windows amplify supplier leverage, as program delays translate into higher escalation risk and schedule penalties. Long design lives of 20–40 years lock programs into established parts ecosystems, further entrenching supplier bargaining power.

Mitigating via LTAs and vertical partnerships

BAE mitigates supplier power through long-term agreements, risk-sharing and supplier development to stabilize pricing and capacity. Strategic inventory, design-for-multi-sourcing and dual-sourcing reduce disruption risk. Co-investment and performance-based logistics align incentives and improve uptime. Critical, single-source components remain hard to multi-source, leaving residual supplier leverage.

Geopolitical and materials exposure

Rare earths, specialty alloys and chokepoints raise supplier leverage for BAE; China accounted for about 60% of global refined rare-earth production in 2024, concentrating upstream risk. 2023–24 export controls and sanctions have already curtailed alternative sources, while logistics bottlenecks and rising cyber incidents among tier-2/3 vendors increase fragility and allow suppliers to price risk premia.

- 60%: China share of refined rare-earths (2024)

- Export controls: tightened 2023–24, reducing alternatives

- Tier-2/3 fragility: logistics + cyber breaches rising

- Suppliers embed risk premia, boosting bargaining power

Digital and IP lock-in

Proprietary tooling, firmware and bespoke test benches create strong digital and IP lock-in for BAE Systems, concentrating leverage with a small set of subsystem suppliers; BAE reported group revenue of about £24.6bn in 2024, amplifying the cost impact of supplier constraints. Data rights and software keys limit integration flexibility, while obsolescence management often requires OEM cooperation, increasing supplier bargaining power.

- Proprietary tooling => vendor lock-in

- Data rights/software keys => constrained integration

- OEM cooperation needed => obsolescence risk

- 2024 revenue context => higher supplier leverage

Suppliers wield outsized leverage: scarce chips, 52-week lead times, 2-5yr recert risk

Suppliers hold high leverage over BAE due to scarce advanced chips, single‑source subs, long qual times (2–5 years) and 52‑week lead times, raising delay and cost risk. Long program lives and IP/tooling lock‑in deepen dependence despite long‑term contracts and co‑investment. Concentrated upstream supply (TSMC ~54% foundry; China ~60% rare‑earths) sustains supplier price premia.

| Metric | Value |

|---|---|

| BAE revenue (2024) | £24.6bn |

| TSMC share (2023–24) | ~54% |

| China refined rare‑earths (2024) | ~60% |

| Max lead time | 52 weeks |

| Switching/recert | 2–5 years |

What is included in the product

Tailored Porter's Five Forces analysis for BAE Systems that uncovers key drivers of competition, supplier and buyer power, threat of new entrants and substitutes, and intensity of rivalry. Identifies disruptive technologies, regulatory and defense procurement dynamics shaping pricing, margins, and strategic positioning.

One-sheet Porter's Five Forces for BAE Systems — instantly visualize competitive pressure across suppliers, buyers, new entrants, substitutes and rivalry with a customizable radar chart to support rapid strategic decisions.

Customers Bargaining Power

Government monopsony dynamics

National governments and defense ministries dominate demand in the sector, with global military spending at about $2.24 trillion in 2023 (SIPRI), concentrating buying power in a few state customers. Budgetary oversight, capability roadmaps and parliamentary approval shape contract terms and payment profiles. Political shifts can delay or cancel programs, giving buyers strong leverage over suppliers despite multi-year lead times.

Competitive tendering and pricing pressure

Intense RFP cycles, down-selects and should-cost reviews compress margins for BAE as programs compete for a finite pool of spending (US FY2024 defence budget $858bn). Fixed-price and performance-based contracts increasingly shift cost risk to BAE, reducing upside on cost overruns. Open-architecture mandates lower proprietary rents by forcing interoperability. Bid protests and audits (GAO/DOJ scrutiny) further discipline bid pricing and acceptance.

Offsets and localization demands

Buyers increasingly demand industrial participation, tech transfer and local content—offsets commonly exceed 30% in major sovereign deals—forcing BAE to build local supply chains and joint ventures. These requirements raise delivery complexity and program cost, dilute IP advantages and constrain pricing and contract flexibility. Compliance is often mandatory to secure sovereign programs, affecting margins and capital allocation.

Lifecycle and sustainment lock-in

Once fielded, platforms require decades of upgrades and MRO, and technical data packages plus certification create sustainment lock-in that reduces buyer power; lifecycle sustainment can account for up to 70% of total platform cost (2024). Governments increasingly mandate open systems (US DoD, NATO allies) to foster competition, partially restoring buyer leverage.

- Decades-long MRO drives incumbency

- Technical data/ certification = leverage

- Up to 70% lifecycle cost in sustainment (2024)

- Policy shift: open systems to boost competition

Budget cycles and multi-year buys

Funding volatility — exemplified by the US FY2024 defense budget of about $858bn — creates volume uncertainty and prompts contract renegotiation, while multi-year and framework buys stabilize demand and reduce supplier risk; buyers often accept price concessions in exchange for schedule and availability guarantees, leaving net buyer power high but varying by program criticality.

- Multi-year buys: stabilize supply

- Renegotiation: driven by funding volatility

- Trade-offs: price vs schedule guarantees

- Buyer power: high, program-dependent

Government Buyers Dominate Defense Procurement: High Oversight, Tight Margins, Big Sustainment

Governments concentrate buying power (global military spend $2.24T 2023; US FY2024 $858B), giving buyers leverage via budgets, oversight and program cancellations. RFPs, fixed-price contracts and open-architecture mandates compress margins; offsets often exceed 30% and sustainment can be up to 70% of lifecycle costs (2024). Buyer power is high but varies by program criticality.

| Metric | Value |

|---|---|

| Global military spend (2023) | $2.24T |

| US FY2024 budget | $858B |

| Offsets | >30% |

| Sustainment share | Up to 70% (2024) |

Preview Before You Purchase

BAE System Porter's Five Forces Analysis

This preview shows the exact BAE Systems Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the full, professionally formatted document ready for download and use the moment you buy. The file covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights.