Baguio Green Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

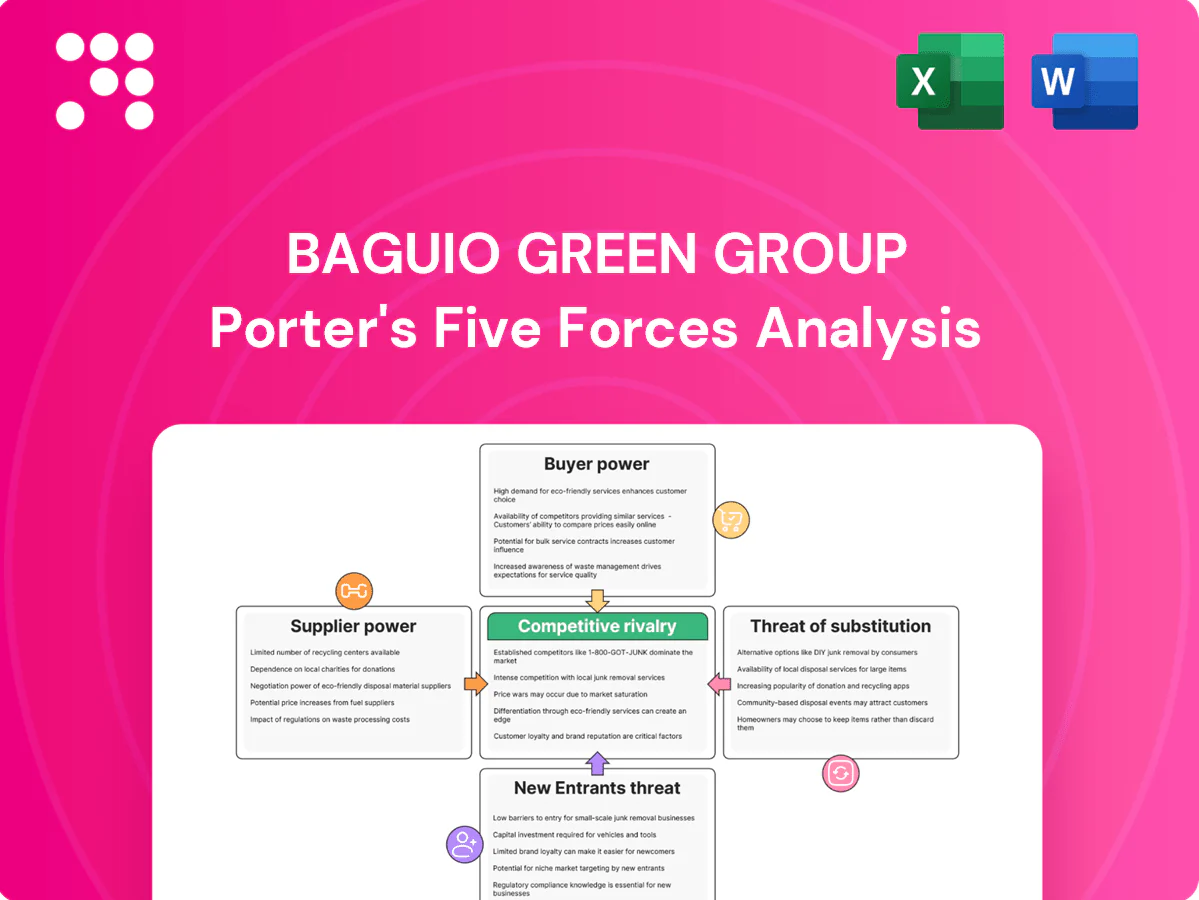

Baguio Green Group faces moderate buyer power and supplier concentration, with high competitive rivalry in waste-to-energy and recycling niches and low threat from substitutes due to specialized services. Regulatory and capital barriers limit new entrants but operational scale is crucial. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated disposal outlets

Concentrated access to government transfer stations, landfills and WtE facilities gives those nodes pricing and contractual leverage over Baguio Green Group, with gate fees and capacity limits compressing margins for contractors. Long-term disposal agreements provide cost stability but lock in terms and reduce operational flexibility. Regulatory fee or policy changes are rapidly passed through to service providers, tightening cashflow predictability.

Specialized equipment vendors

Supply of sweepers, refuse compactor trucks, robotic cleaners, IoT-enabled bins and sorting lines is concentrated among OEMs such as Volvo Group, Oshkosh/FAUN, Johnston/Hako, Nilfisk and Tomra; lead times frequently reach 6–12 months and spare-part delays directly affect uptime and SLAs; volume purchasing and multi-year service contracts reduce unit cost; entrenched software/hardware integration creates technology lock-in and high switching costs for buyers.

Labor as a critical input

Frontline labor availability directly affects Baguio Green Group costs as 2024 regional minimum wages in the Philippines range roughly PHP 316–610 per day and statutory overtime premiums start at 125%, pressuring margins. Heavy reliance on subcontracted crews or agencies shifts bargaining power to manpower suppliers and can add 10–20% markup on labor costs. Robust training and retention programs lower churn and reduce supplier dependence. Union or regulatory changes can rapidly reprice labor risks.

Sustainable consumables

Sustainable consumables—green chemicals, biodegradable bags, PPE and eco-certified materials—face high supplier concentration, with the global biodegradable plastics market valued at about US$5.7B in 2024, tightening options for Baguio Green Group and enabling suppliers to command premiums. ESG-driven client specs further narrow sourcing and can increase procurement costs; framework agreements and dual-sourcing mitigate disruption, but certification lapses or material shortages risk contract non-compliance.

- fewer qualified suppliers

- US$5.7B biodegradable plastics (2024)

- ESG specs raise costs

- use framework agreements

- dual-sourcing mitigates risk

- certification lapses disrupt contracts

Recyclables offtakers

Recyclables offtakers for paper, plastics, metals and organics show high volatility and regional concentration; in Southeast Asia the top five buyers commonly account for over 50% of demand, so price drops force offtakers to tighten specs or cut acceptance, shifting costs upstream. Long-term offtake MOUs and strict QC protocols preserved throughput for Baguio Green Group during 2024 market dips.

- concentration: top5 >50%

- price risk: acceptance cuts common in downturns

- mitigation: long-term MOUs + QC

- diversification: geographic spread lowers exposure

Suppliers pressure margins; >50% offtaker share raises volatility; dual-source

Suppliers hold moderate-to-high power: disposal nodes and OEMs create pricing and tech lock-in, while labor and sustainable-materials concentration raise costs; recyclables offtaker concentration (>50% top5) adds volume/price volatility; long-term contracts, volume buying and dual-sourcing are key mitigants.

| Metric | 2024 Value |

|---|---|

| Biodegradable plastics market | US$5.7B |

| Top5 offtakers share | >50% |

| Labor min wage (PH) | PHP316–610/day |

What is included in the product

Tailored Porter's Five Forces analysis for Baguio Green Group that uncovers key drivers of competition, evaluates supplier and buyer power, and identifies disruptive substitutes and entry barriers shaping its pricing and profitability.

A one-sheet Porter's Five Forces for Baguio Green Group that instantly reveals competitive pressures and strategic pain points—customizable, cleanly formatted, and ready to drop into pitch decks or strategy reports for fast, boardroom-ready decisions.

Customers Bargaining Power

Government tender dominance

Large, transparent public tenders concentrate buying power: public procurement represents about 12% of GDP in OECD countries, funneling significant volumes to few vendors. Price-weighted evaluation criteria compress service margins even as contracts require strict KPI compliance. Multi-year awards deliver predictable volume but intensify bidder competition and downward price pressure. Performance scorecards allow rapid vendor replacement when KPIs slip, raising service-risk for incumbents.

Private property portfolios

In 2024 private property portfolios give customers strong leverage as developers and facility managers bundle multiple sites to secure scale discounts, while sophisticated buyers increasingly unbundle services across vendors to extract price concessions. Rigorous SLA benchmarking and more frequent re-tendering cycles heighten buyer power. Baguio Green Group’s cross-selling of integrated ESG and maintenance services can partially offset this pressure by locking in broader contracts.

Low switching costs

Standardized scopes and clear handover processes make vendor changes feasible, and in 2024 about 62% of corporate buyers reported using trial periods to evaluate new suppliers. Buyers routinely include penalty clauses to keep suppliers responsive, reducing lock-in. Strong brand and safety records offer some stickiness but not full retention. Widespread digital reporting (≈65% adoption in 2024) makes performance comparability easier.

In-house alternatives

Large campuses and malls can internalize cleaning or landscaping to hedge costs, which strengthens buyer negotiation positions and pressures vendors to prove superior total cost of ownership and compliance benefits.

Suppliers must quantify labor, equipment, and regulatory compliance savings versus insourcing; specialized waste permits and heavy equipment requirements enforced by environmental authorities create a barrier that deters full insourcing.

- Insourcing leverage: operational control, potential labor cost savings

- TCO focus: lifecycle costs, training, compliance documentation

- Regulatory deterrent: specialized waste permits and heavy-equipment capital needs

ESG and compliance demands

Buyers increasingly demand measurable sustainability and data transparency; EU CSRD expansion in 2024 extended mandatory reporting to roughly 50,000 companies, forcing vendors to invest in reporting tech and certifications and making costs more visible. Non-compliance risks rapid contract loss, while proven ESG outcomes can justify premium pricing and reduce buyer power.

- 2024: CSRD ~50,000 companies

- Higher reporting tech and certification spend

- Non-compliance = contract risk

- Proven ESG supports premium pricing

Concentrated buyers, 62% trials and 65% digital reporting increase switching and price pressure

Buyers wield strong price and contract power via concentrated public tenders (public procurement ~12% GDP) and bundled private portfolios; 62% use trial periods and 65% adopted digital reporting in 2024. Rigorous SLAs, frequent retenders and CSRD expansion (~50,000 firms) increase transparency and switching. Baguio Green offsets with integrated ESG services that can command premiums.

| Metric | 2024 | Implication |

|---|---|---|

| Public procurement | ~12% GDP | Concentrated buy power |

| Trial adoption | 62% | Easy switching |

| Digital reporting | 65% | Performance comparability |

| CSRD scope | ~50,000 firms | Reporting costs↑ |

Full Version Awaits

Baguio Green Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Baguio Green Group you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical complete document.

Don't Miss the Bigger Picture

Baguio Green Group faces moderate buyer power and supplier concentration, with high competitive rivalry in waste-to-energy and recycling niches and low threat from substitutes due to specialized services. Regulatory and capital barriers limit new entrants but operational scale is crucial. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated disposal outlets

Concentrated access to government transfer stations, landfills and WtE facilities gives those nodes pricing and contractual leverage over Baguio Green Group, with gate fees and capacity limits compressing margins for contractors. Long-term disposal agreements provide cost stability but lock in terms and reduce operational flexibility. Regulatory fee or policy changes are rapidly passed through to service providers, tightening cashflow predictability.

Specialized equipment vendors

Supply of sweepers, refuse compactor trucks, robotic cleaners, IoT-enabled bins and sorting lines is concentrated among OEMs such as Volvo Group, Oshkosh/FAUN, Johnston/Hako, Nilfisk and Tomra; lead times frequently reach 6–12 months and spare-part delays directly affect uptime and SLAs; volume purchasing and multi-year service contracts reduce unit cost; entrenched software/hardware integration creates technology lock-in and high switching costs for buyers.

Labor as a critical input

Frontline labor availability directly affects Baguio Green Group costs as 2024 regional minimum wages in the Philippines range roughly PHP 316–610 per day and statutory overtime premiums start at 125%, pressuring margins. Heavy reliance on subcontracted crews or agencies shifts bargaining power to manpower suppliers and can add 10–20% markup on labor costs. Robust training and retention programs lower churn and reduce supplier dependence. Union or regulatory changes can rapidly reprice labor risks.

Sustainable consumables

Sustainable consumables—green chemicals, biodegradable bags, PPE and eco-certified materials—face high supplier concentration, with the global biodegradable plastics market valued at about US$5.7B in 2024, tightening options for Baguio Green Group and enabling suppliers to command premiums. ESG-driven client specs further narrow sourcing and can increase procurement costs; framework agreements and dual-sourcing mitigate disruption, but certification lapses or material shortages risk contract non-compliance.

- fewer qualified suppliers

- US$5.7B biodegradable plastics (2024)

- ESG specs raise costs

- use framework agreements

- dual-sourcing mitigates risk

- certification lapses disrupt contracts

Recyclables offtakers

Recyclables offtakers for paper, plastics, metals and organics show high volatility and regional concentration; in Southeast Asia the top five buyers commonly account for over 50% of demand, so price drops force offtakers to tighten specs or cut acceptance, shifting costs upstream. Long-term offtake MOUs and strict QC protocols preserved throughput for Baguio Green Group during 2024 market dips.

- concentration: top5 >50%

- price risk: acceptance cuts common in downturns

- mitigation: long-term MOUs + QC

- diversification: geographic spread lowers exposure

Suppliers pressure margins; >50% offtaker share raises volatility; dual-source

Suppliers hold moderate-to-high power: disposal nodes and OEMs create pricing and tech lock-in, while labor and sustainable-materials concentration raise costs; recyclables offtaker concentration (>50% top5) adds volume/price volatility; long-term contracts, volume buying and dual-sourcing are key mitigants.

| Metric | 2024 Value |

|---|---|

| Biodegradable plastics market | US$5.7B |

| Top5 offtakers share | >50% |

| Labor min wage (PH) | PHP316–610/day |

What is included in the product

Tailored Porter's Five Forces analysis for Baguio Green Group that uncovers key drivers of competition, evaluates supplier and buyer power, and identifies disruptive substitutes and entry barriers shaping its pricing and profitability.

A one-sheet Porter's Five Forces for Baguio Green Group that instantly reveals competitive pressures and strategic pain points—customizable, cleanly formatted, and ready to drop into pitch decks or strategy reports for fast, boardroom-ready decisions.

Customers Bargaining Power

Government tender dominance

Large, transparent public tenders concentrate buying power: public procurement represents about 12% of GDP in OECD countries, funneling significant volumes to few vendors. Price-weighted evaluation criteria compress service margins even as contracts require strict KPI compliance. Multi-year awards deliver predictable volume but intensify bidder competition and downward price pressure. Performance scorecards allow rapid vendor replacement when KPIs slip, raising service-risk for incumbents.

Private property portfolios

In 2024 private property portfolios give customers strong leverage as developers and facility managers bundle multiple sites to secure scale discounts, while sophisticated buyers increasingly unbundle services across vendors to extract price concessions. Rigorous SLA benchmarking and more frequent re-tendering cycles heighten buyer power. Baguio Green Group’s cross-selling of integrated ESG and maintenance services can partially offset this pressure by locking in broader contracts.

Low switching costs

Standardized scopes and clear handover processes make vendor changes feasible, and in 2024 about 62% of corporate buyers reported using trial periods to evaluate new suppliers. Buyers routinely include penalty clauses to keep suppliers responsive, reducing lock-in. Strong brand and safety records offer some stickiness but not full retention. Widespread digital reporting (≈65% adoption in 2024) makes performance comparability easier.

In-house alternatives

Large campuses and malls can internalize cleaning or landscaping to hedge costs, which strengthens buyer negotiation positions and pressures vendors to prove superior total cost of ownership and compliance benefits.

Suppliers must quantify labor, equipment, and regulatory compliance savings versus insourcing; specialized waste permits and heavy equipment requirements enforced by environmental authorities create a barrier that deters full insourcing.

- Insourcing leverage: operational control, potential labor cost savings

- TCO focus: lifecycle costs, training, compliance documentation

- Regulatory deterrent: specialized waste permits and heavy-equipment capital needs

ESG and compliance demands

Buyers increasingly demand measurable sustainability and data transparency; EU CSRD expansion in 2024 extended mandatory reporting to roughly 50,000 companies, forcing vendors to invest in reporting tech and certifications and making costs more visible. Non-compliance risks rapid contract loss, while proven ESG outcomes can justify premium pricing and reduce buyer power.

- 2024: CSRD ~50,000 companies

- Higher reporting tech and certification spend

- Non-compliance = contract risk

- Proven ESG supports premium pricing

Concentrated buyers, 62% trials and 65% digital reporting increase switching and price pressure

Buyers wield strong price and contract power via concentrated public tenders (public procurement ~12% GDP) and bundled private portfolios; 62% use trial periods and 65% adopted digital reporting in 2024. Rigorous SLAs, frequent retenders and CSRD expansion (~50,000 firms) increase transparency and switching. Baguio Green offsets with integrated ESG services that can command premiums.

| Metric | 2024 | Implication |

|---|---|---|

| Public procurement | ~12% GDP | Concentrated buy power |

| Trial adoption | 62% | Easy switching |

| Digital reporting | 65% | Performance comparability |

| CSRD scope | ~50,000 firms | Reporting costs↑ |

Full Version Awaits

Baguio Green Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Baguio Green Group you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical complete document.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Baguio Green Group faces moderate buyer power and supplier concentration, with high competitive rivalry in waste-to-energy and recycling niches and low threat from substitutes due to specialized services. Regulatory and capital barriers limit new entrants but operational scale is crucial. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated disposal outlets

Concentrated access to government transfer stations, landfills and WtE facilities gives those nodes pricing and contractual leverage over Baguio Green Group, with gate fees and capacity limits compressing margins for contractors. Long-term disposal agreements provide cost stability but lock in terms and reduce operational flexibility. Regulatory fee or policy changes are rapidly passed through to service providers, tightening cashflow predictability.

Specialized equipment vendors

Supply of sweepers, refuse compactor trucks, robotic cleaners, IoT-enabled bins and sorting lines is concentrated among OEMs such as Volvo Group, Oshkosh/FAUN, Johnston/Hako, Nilfisk and Tomra; lead times frequently reach 6–12 months and spare-part delays directly affect uptime and SLAs; volume purchasing and multi-year service contracts reduce unit cost; entrenched software/hardware integration creates technology lock-in and high switching costs for buyers.

Labor as a critical input

Frontline labor availability directly affects Baguio Green Group costs as 2024 regional minimum wages in the Philippines range roughly PHP 316–610 per day and statutory overtime premiums start at 125%, pressuring margins. Heavy reliance on subcontracted crews or agencies shifts bargaining power to manpower suppliers and can add 10–20% markup on labor costs. Robust training and retention programs lower churn and reduce supplier dependence. Union or regulatory changes can rapidly reprice labor risks.

Sustainable consumables

Sustainable consumables—green chemicals, biodegradable bags, PPE and eco-certified materials—face high supplier concentration, with the global biodegradable plastics market valued at about US$5.7B in 2024, tightening options for Baguio Green Group and enabling suppliers to command premiums. ESG-driven client specs further narrow sourcing and can increase procurement costs; framework agreements and dual-sourcing mitigate disruption, but certification lapses or material shortages risk contract non-compliance.

- fewer qualified suppliers

- US$5.7B biodegradable plastics (2024)

- ESG specs raise costs

- use framework agreements

- dual-sourcing mitigates risk

- certification lapses disrupt contracts

Recyclables offtakers

Recyclables offtakers for paper, plastics, metals and organics show high volatility and regional concentration; in Southeast Asia the top five buyers commonly account for over 50% of demand, so price drops force offtakers to tighten specs or cut acceptance, shifting costs upstream. Long-term offtake MOUs and strict QC protocols preserved throughput for Baguio Green Group during 2024 market dips.

- concentration: top5 >50%

- price risk: acceptance cuts common in downturns

- mitigation: long-term MOUs + QC

- diversification: geographic spread lowers exposure

Suppliers pressure margins; >50% offtaker share raises volatility; dual-source

Suppliers hold moderate-to-high power: disposal nodes and OEMs create pricing and tech lock-in, while labor and sustainable-materials concentration raise costs; recyclables offtaker concentration (>50% top5) adds volume/price volatility; long-term contracts, volume buying and dual-sourcing are key mitigants.

| Metric | 2024 Value |

|---|---|

| Biodegradable plastics market | US$5.7B |

| Top5 offtakers share | >50% |

| Labor min wage (PH) | PHP316–610/day |

What is included in the product

Tailored Porter's Five Forces analysis for Baguio Green Group that uncovers key drivers of competition, evaluates supplier and buyer power, and identifies disruptive substitutes and entry barriers shaping its pricing and profitability.

A one-sheet Porter's Five Forces for Baguio Green Group that instantly reveals competitive pressures and strategic pain points—customizable, cleanly formatted, and ready to drop into pitch decks or strategy reports for fast, boardroom-ready decisions.

Customers Bargaining Power

Government tender dominance

Large, transparent public tenders concentrate buying power: public procurement represents about 12% of GDP in OECD countries, funneling significant volumes to few vendors. Price-weighted evaluation criteria compress service margins even as contracts require strict KPI compliance. Multi-year awards deliver predictable volume but intensify bidder competition and downward price pressure. Performance scorecards allow rapid vendor replacement when KPIs slip, raising service-risk for incumbents.

Private property portfolios

In 2024 private property portfolios give customers strong leverage as developers and facility managers bundle multiple sites to secure scale discounts, while sophisticated buyers increasingly unbundle services across vendors to extract price concessions. Rigorous SLA benchmarking and more frequent re-tendering cycles heighten buyer power. Baguio Green Group’s cross-selling of integrated ESG and maintenance services can partially offset this pressure by locking in broader contracts.

Low switching costs

Standardized scopes and clear handover processes make vendor changes feasible, and in 2024 about 62% of corporate buyers reported using trial periods to evaluate new suppliers. Buyers routinely include penalty clauses to keep suppliers responsive, reducing lock-in. Strong brand and safety records offer some stickiness but not full retention. Widespread digital reporting (≈65% adoption in 2024) makes performance comparability easier.

In-house alternatives

Large campuses and malls can internalize cleaning or landscaping to hedge costs, which strengthens buyer negotiation positions and pressures vendors to prove superior total cost of ownership and compliance benefits.

Suppliers must quantify labor, equipment, and regulatory compliance savings versus insourcing; specialized waste permits and heavy equipment requirements enforced by environmental authorities create a barrier that deters full insourcing.

- Insourcing leverage: operational control, potential labor cost savings

- TCO focus: lifecycle costs, training, compliance documentation

- Regulatory deterrent: specialized waste permits and heavy-equipment capital needs

ESG and compliance demands

Buyers increasingly demand measurable sustainability and data transparency; EU CSRD expansion in 2024 extended mandatory reporting to roughly 50,000 companies, forcing vendors to invest in reporting tech and certifications and making costs more visible. Non-compliance risks rapid contract loss, while proven ESG outcomes can justify premium pricing and reduce buyer power.

- 2024: CSRD ~50,000 companies

- Higher reporting tech and certification spend

- Non-compliance = contract risk

- Proven ESG supports premium pricing

Concentrated buyers, 62% trials and 65% digital reporting increase switching and price pressure

Buyers wield strong price and contract power via concentrated public tenders (public procurement ~12% GDP) and bundled private portfolios; 62% use trial periods and 65% adopted digital reporting in 2024. Rigorous SLAs, frequent retenders and CSRD expansion (~50,000 firms) increase transparency and switching. Baguio Green offsets with integrated ESG services that can command premiums.

| Metric | 2024 | Implication |

|---|---|---|

| Public procurement | ~12% GDP | Concentrated buy power |

| Trial adoption | 62% | Easy switching |

| Digital reporting | 65% | Performance comparability |

| CSRD scope | ~50,000 firms | Reporting costs↑ |

Full Version Awaits

Baguio Green Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Baguio Green Group you'll receive after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical complete document.