Bakkt Porter's Five Forces Analysis

Don't Miss the Bigger Picture

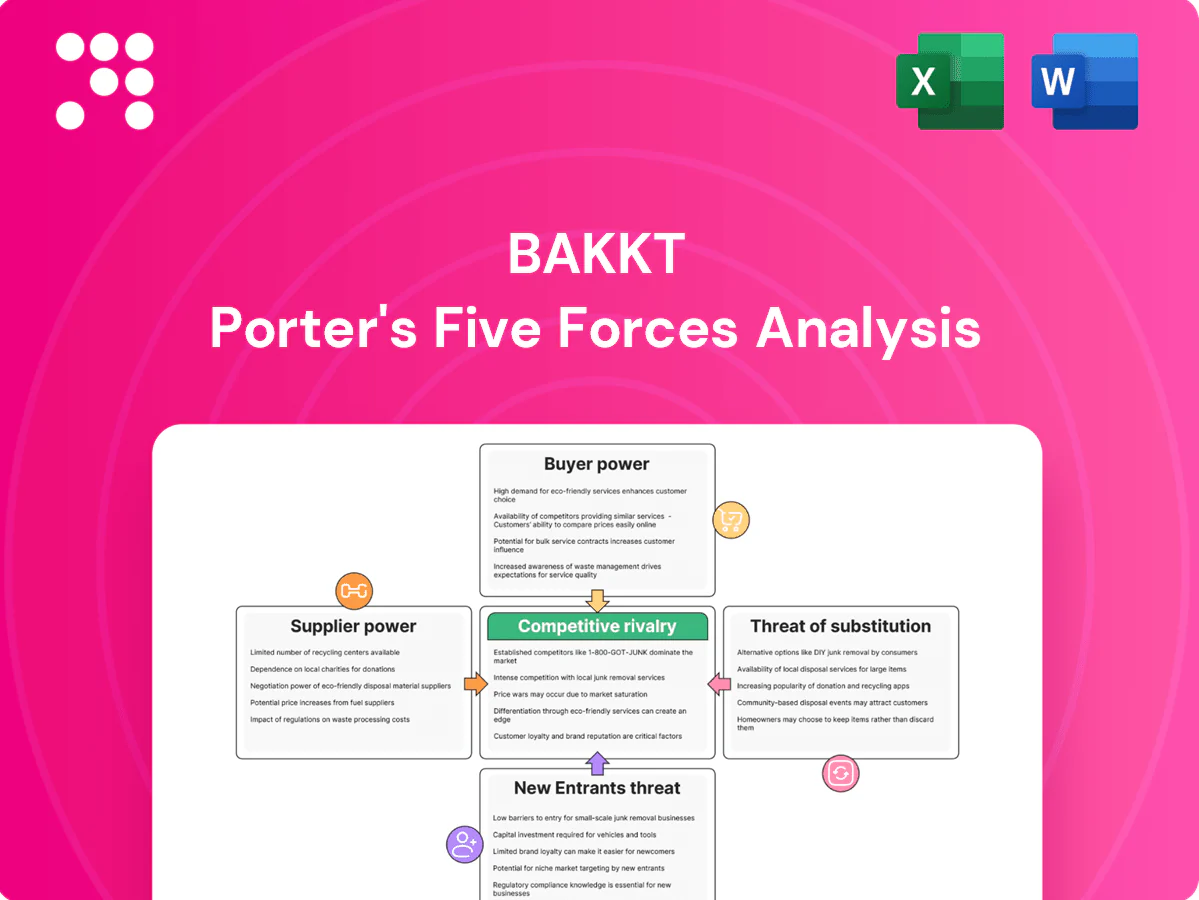

Bakkt navigates intense competitive pressures from incumbents, shifting buyer preferences, and emerging crypto-native substitutes, while supplier and regulatory forces shape its margins and scalability. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get a consultant-grade breakdown and actionable strategic insights.

Suppliers Bargaining Power

Dependence on blockchain networks

Core protocols like Bitcoin and Ethereum act as de facto monopolistic suppliers of blockspace and settlement; Bitcoin's April 2024 halving triggered measurable mempool congestion and fee spikes that raised costs for custodial services. Network upgrades and potential hard forks force Bakkt to adapt without influence. Supporting multiple chains reduces exposure but does not eliminate dependence on dominant networks.

Liquidity and market maker concentration

Bakkt depends on a limited set of liquidity providers and market makers to maintain tight spreads and reliable execution, creating high switching costs that give those providers measurable pricing leverage. Concentration means market stress can quickly reduce available liquidity and widen spreads, as seen in crypto market drawdowns. Strategic partnerships and routing across multiple venues mitigate but do not eliminate counterparty or depth risk.

Banking, fiat rails, and stablecoin issuers

Access to fiat on/off-ramps and stablecoin issuers is essential for conversions and settlement; USDT and USDC together held over 85% of the stablecoin market cap in 2024, concentrating supplier power. Compliance demands let banks and issuers set fees and service terms, squeezing margins and raising settlement costs. Offboarding or de-banking can abruptly disrupt operations, so redundant relationships and diversified rails materially reduce exposure.

Cloud, security, and compliance vendors

Cloud, security, and compliance vendors are highly sticky suppliers; top cloud providers held roughly 66% market share in 2024 (AWS 32%, Azure 23%, GCP 11%) and global cybersecurity spending reached about $188B in 2024. Migration costs and regulatory validation amplify vendor lock-in. Price hikes or service limits can compress margins and threaten uptime. Multi-cloud, building in-house controls, and strict vendor management reduce supplier power.

- Dependency: high

- Cost risk: material

- Regulatory lock-in: significant

- Mitigants: multi-cloud, internal tooling, vendor SLAs

Data and market infrastructure providers

Price feeds, analytics, and custody tooling from niche providers are hard to substitute, with many trading ops demanding sub-100ms latency and institutional custody SLAs; this concentration increases supplier leverage. Outages or data inaccuracies create operational and regulatory risks that can cost firms millions in remediation and fines. Building proprietary pipelines can reduce dependency over time.

- Concentration: limited vendors

- Latency: sub-100ms needs

- Risk: outages → multimillion costs

- Mitigation: invest in in-house data

Halving fee spikes and settlement concentration: stablecoins 85%

Core protocols (Bitcoin halving Apr 2024) created fee spikes and act as monopolistic settlement rails; Bakkt must adapt to chain-level changes. Limited liquidity providers raise switching costs and widen spreads in stress. USDT+USDC ≈85% stablecoin share in 2024, concentrating fiat/settlement power. Top cloud providers (AWS 32%, Azure 23%, GCP 11%) and $188B cyber spend create vendor lock-in; multi-cloud and in-house tooling mitigate.

| Supplier | Key stat 2024 | Impact | Mitigant |

|---|---|---|---|

| Protocols | Bitcoin halving Apr 2024 → fees↑ | Higher settlement costs | Multi-chain support |

| Liquidity | Concentrated MM | Wider spreads | Multiple LPs/routing |

| Stablecoins | USDT+USDC ≈85% | Conversion risk | Diversified rails |

| Cloud/Sec | AWS32/AZ23/GCP11; $188B | Vendor lock-in | Multi-cloud/SLA |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Bakkt, uncovering key competitive drivers, buyer and supplier power, barriers to entry, substitutes and disruptive threats that shape pricing, market share and strategic positioning.

A concise one-sheet Porter's Five Forces for Bakkt that visualizes competitive pressures, regulatory risk, and partner dynamics—perfect for quickly identifying threats and opportunities and guiding strategic responses.

Customers Bargaining Power

High multi-homing among users

Consumers and institutions commonly multi-home across exchanges, brokers, and wallets, and 2024 surveys indicate a majority of crypto participants hold accounts on multiple platforms. Easy onboarding and similar feature sets keep switching costs low, letting buyers move volume rapidly to chase better price or liquidity. To retain flow Bakkt must emphasize trust, custodial security, and seamless integrations with clearing and institutional rails.

Price sensitivity and fee transparency

Trading, custody and withdrawal fees are benchmarked tightly across venues, with institutional clients demanding tiered pricing and rebates to match volume-driven economics. Buyers push for best execution and spreads compression, forcing Bakkt to price competitively. This persistent pricing pressure limits margin expansion on trading and custody services. Platform fee transparency becomes a table-stakes competitive requirement.

Institutional requirements and customization

Institutional clients in 2024 insist on strict SLAs, comprehensive reporting, auditability and tailored workflows, elevating procurement demands and giving buyers leverage. The requirement for bespoke integrations and RFP-driven procurement lengthens sales cycles and strengthens negotiation power, pressuring pricing and contract terms. Value-added services can command premiums only when providers demonstrate clear ROI and measurable metrics within enterprise audits.

Security and regulatory assurance expectations

Clients demand robust compliance, insurance and regulated custody; Bakkt Trust Company is a NYDFS‑licensed trust company as of 2024, so any perceived lapse triggers rapid attrition. Buyers can require SOC 2 or ISO 27001 attestations and third‑party insurance proofs. Superior governance and visible certifications reduce buyer bargaining power by increasing trust and stickiness.

- NYDFS license (Bakkt Trust Co., 2024)

- SOC 2 / ISO 27001 attestations

- Third‑party insurance proofs

- Governance reduces churn

Ecosystem integration demands

Ecosystem integration drives customer bargaining: API breadth, ERP/treasury connectors and analytics are top selection criteria, with a 2024 survey showing 68% of finance teams prioritize integration when choosing vendors.

Clients prefer vendors that reduce operational complexity; integration stickiness lowers switching but is treated as table stakes, and continuous alignment with client stacks is essential to retain enterprise accounts.

- API breadth: Enables rapid onboarding, reduces TCO

- ERP/treasury connectivity: Critical for cash management and reconciliation

- Analytics: Key differentiator shaping platform choice

Buyers hold leverage: 68% prioritize integration; compliance and tiered pricing squeeze margins

Buyers hold strong leverage: 2024 surveys show 68% of finance teams prioritize integration, while multi‑platform custody remains common, keeping switching costs low. Tight benchmarking of fees and demand for tiered pricing compresses margins and forces competitive pricing. Institutional SLAs, compliance proofs and NYDFS licensing (Bakkt Trust Co., 2024) shape contract terms and reduce churn.

| Metric | 2024 Fact |

|---|---|

| Integration priority | 68% of finance teams |

| Regulatory status | NYDFS license (Bakkt Trust Co., 2024) |

| Compliance proofs | SOC 2 / ISO 27001 common requirement |

What You See Is What You Get

Bakkt Porter's Five Forces Analysis

This preview shows the exact Bakkt Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase. No placeholders, mockups, or samples; the document shown is the deliverable. Use it as-is for research, presentations, or decision-making.

Don't Miss the Bigger Picture

Bakkt navigates intense competitive pressures from incumbents, shifting buyer preferences, and emerging crypto-native substitutes, while supplier and regulatory forces shape its margins and scalability. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get a consultant-grade breakdown and actionable strategic insights.

Suppliers Bargaining Power

Dependence on blockchain networks

Core protocols like Bitcoin and Ethereum act as de facto monopolistic suppliers of blockspace and settlement; Bitcoin's April 2024 halving triggered measurable mempool congestion and fee spikes that raised costs for custodial services. Network upgrades and potential hard forks force Bakkt to adapt without influence. Supporting multiple chains reduces exposure but does not eliminate dependence on dominant networks.

Liquidity and market maker concentration

Bakkt depends on a limited set of liquidity providers and market makers to maintain tight spreads and reliable execution, creating high switching costs that give those providers measurable pricing leverage. Concentration means market stress can quickly reduce available liquidity and widen spreads, as seen in crypto market drawdowns. Strategic partnerships and routing across multiple venues mitigate but do not eliminate counterparty or depth risk.

Banking, fiat rails, and stablecoin issuers

Access to fiat on/off-ramps and stablecoin issuers is essential for conversions and settlement; USDT and USDC together held over 85% of the stablecoin market cap in 2024, concentrating supplier power. Compliance demands let banks and issuers set fees and service terms, squeezing margins and raising settlement costs. Offboarding or de-banking can abruptly disrupt operations, so redundant relationships and diversified rails materially reduce exposure.

Cloud, security, and compliance vendors

Cloud, security, and compliance vendors are highly sticky suppliers; top cloud providers held roughly 66% market share in 2024 (AWS 32%, Azure 23%, GCP 11%) and global cybersecurity spending reached about $188B in 2024. Migration costs and regulatory validation amplify vendor lock-in. Price hikes or service limits can compress margins and threaten uptime. Multi-cloud, building in-house controls, and strict vendor management reduce supplier power.

- Dependency: high

- Cost risk: material

- Regulatory lock-in: significant

- Mitigants: multi-cloud, internal tooling, vendor SLAs

Data and market infrastructure providers

Price feeds, analytics, and custody tooling from niche providers are hard to substitute, with many trading ops demanding sub-100ms latency and institutional custody SLAs; this concentration increases supplier leverage. Outages or data inaccuracies create operational and regulatory risks that can cost firms millions in remediation and fines. Building proprietary pipelines can reduce dependency over time.

- Concentration: limited vendors

- Latency: sub-100ms needs

- Risk: outages → multimillion costs

- Mitigation: invest in in-house data

Halving fee spikes and settlement concentration: stablecoins 85%

Core protocols (Bitcoin halving Apr 2024) created fee spikes and act as monopolistic settlement rails; Bakkt must adapt to chain-level changes. Limited liquidity providers raise switching costs and widen spreads in stress. USDT+USDC ≈85% stablecoin share in 2024, concentrating fiat/settlement power. Top cloud providers (AWS 32%, Azure 23%, GCP 11%) and $188B cyber spend create vendor lock-in; multi-cloud and in-house tooling mitigate.

| Supplier | Key stat 2024 | Impact | Mitigant |

|---|---|---|---|

| Protocols | Bitcoin halving Apr 2024 → fees↑ | Higher settlement costs | Multi-chain support |

| Liquidity | Concentrated MM | Wider spreads | Multiple LPs/routing |

| Stablecoins | USDT+USDC ≈85% | Conversion risk | Diversified rails |

| Cloud/Sec | AWS32/AZ23/GCP11; $188B | Vendor lock-in | Multi-cloud/SLA |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Bakkt, uncovering key competitive drivers, buyer and supplier power, barriers to entry, substitutes and disruptive threats that shape pricing, market share and strategic positioning.

A concise one-sheet Porter's Five Forces for Bakkt that visualizes competitive pressures, regulatory risk, and partner dynamics—perfect for quickly identifying threats and opportunities and guiding strategic responses.

Customers Bargaining Power

High multi-homing among users

Consumers and institutions commonly multi-home across exchanges, brokers, and wallets, and 2024 surveys indicate a majority of crypto participants hold accounts on multiple platforms. Easy onboarding and similar feature sets keep switching costs low, letting buyers move volume rapidly to chase better price or liquidity. To retain flow Bakkt must emphasize trust, custodial security, and seamless integrations with clearing and institutional rails.

Price sensitivity and fee transparency

Trading, custody and withdrawal fees are benchmarked tightly across venues, with institutional clients demanding tiered pricing and rebates to match volume-driven economics. Buyers push for best execution and spreads compression, forcing Bakkt to price competitively. This persistent pricing pressure limits margin expansion on trading and custody services. Platform fee transparency becomes a table-stakes competitive requirement.

Institutional requirements and customization

Institutional clients in 2024 insist on strict SLAs, comprehensive reporting, auditability and tailored workflows, elevating procurement demands and giving buyers leverage. The requirement for bespoke integrations and RFP-driven procurement lengthens sales cycles and strengthens negotiation power, pressuring pricing and contract terms. Value-added services can command premiums only when providers demonstrate clear ROI and measurable metrics within enterprise audits.

Security and regulatory assurance expectations

Clients demand robust compliance, insurance and regulated custody; Bakkt Trust Company is a NYDFS‑licensed trust company as of 2024, so any perceived lapse triggers rapid attrition. Buyers can require SOC 2 or ISO 27001 attestations and third‑party insurance proofs. Superior governance and visible certifications reduce buyer bargaining power by increasing trust and stickiness.

- NYDFS license (Bakkt Trust Co., 2024)

- SOC 2 / ISO 27001 attestations

- Third‑party insurance proofs

- Governance reduces churn

Ecosystem integration demands

Ecosystem integration drives customer bargaining: API breadth, ERP/treasury connectors and analytics are top selection criteria, with a 2024 survey showing 68% of finance teams prioritize integration when choosing vendors.

Clients prefer vendors that reduce operational complexity; integration stickiness lowers switching but is treated as table stakes, and continuous alignment with client stacks is essential to retain enterprise accounts.

- API breadth: Enables rapid onboarding, reduces TCO

- ERP/treasury connectivity: Critical for cash management and reconciliation

- Analytics: Key differentiator shaping platform choice

Buyers hold leverage: 68% prioritize integration; compliance and tiered pricing squeeze margins

Buyers hold strong leverage: 2024 surveys show 68% of finance teams prioritize integration, while multi‑platform custody remains common, keeping switching costs low. Tight benchmarking of fees and demand for tiered pricing compresses margins and forces competitive pricing. Institutional SLAs, compliance proofs and NYDFS licensing (Bakkt Trust Co., 2024) shape contract terms and reduce churn.

| Metric | 2024 Fact |

|---|---|

| Integration priority | 68% of finance teams |

| Regulatory status | NYDFS license (Bakkt Trust Co., 2024) |

| Compliance proofs | SOC 2 / ISO 27001 common requirement |

What You See Is What You Get

Bakkt Porter's Five Forces Analysis

This preview shows the exact Bakkt Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase. No placeholders, mockups, or samples; the document shown is the deliverable. Use it as-is for research, presentations, or decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Bakkt navigates intense competitive pressures from incumbents, shifting buyer preferences, and emerging crypto-native substitutes, while supplier and regulatory forces shape its margins and scalability. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to get a consultant-grade breakdown and actionable strategic insights.

Suppliers Bargaining Power

Dependence on blockchain networks

Core protocols like Bitcoin and Ethereum act as de facto monopolistic suppliers of blockspace and settlement; Bitcoin's April 2024 halving triggered measurable mempool congestion and fee spikes that raised costs for custodial services. Network upgrades and potential hard forks force Bakkt to adapt without influence. Supporting multiple chains reduces exposure but does not eliminate dependence on dominant networks.

Liquidity and market maker concentration

Bakkt depends on a limited set of liquidity providers and market makers to maintain tight spreads and reliable execution, creating high switching costs that give those providers measurable pricing leverage. Concentration means market stress can quickly reduce available liquidity and widen spreads, as seen in crypto market drawdowns. Strategic partnerships and routing across multiple venues mitigate but do not eliminate counterparty or depth risk.

Banking, fiat rails, and stablecoin issuers

Access to fiat on/off-ramps and stablecoin issuers is essential for conversions and settlement; USDT and USDC together held over 85% of the stablecoin market cap in 2024, concentrating supplier power. Compliance demands let banks and issuers set fees and service terms, squeezing margins and raising settlement costs. Offboarding or de-banking can abruptly disrupt operations, so redundant relationships and diversified rails materially reduce exposure.

Cloud, security, and compliance vendors

Cloud, security, and compliance vendors are highly sticky suppliers; top cloud providers held roughly 66% market share in 2024 (AWS 32%, Azure 23%, GCP 11%) and global cybersecurity spending reached about $188B in 2024. Migration costs and regulatory validation amplify vendor lock-in. Price hikes or service limits can compress margins and threaten uptime. Multi-cloud, building in-house controls, and strict vendor management reduce supplier power.

- Dependency: high

- Cost risk: material

- Regulatory lock-in: significant

- Mitigants: multi-cloud, internal tooling, vendor SLAs

Data and market infrastructure providers

Price feeds, analytics, and custody tooling from niche providers are hard to substitute, with many trading ops demanding sub-100ms latency and institutional custody SLAs; this concentration increases supplier leverage. Outages or data inaccuracies create operational and regulatory risks that can cost firms millions in remediation and fines. Building proprietary pipelines can reduce dependency over time.

- Concentration: limited vendors

- Latency: sub-100ms needs

- Risk: outages → multimillion costs

- Mitigation: invest in in-house data

Halving fee spikes and settlement concentration: stablecoins 85%

Core protocols (Bitcoin halving Apr 2024) created fee spikes and act as monopolistic settlement rails; Bakkt must adapt to chain-level changes. Limited liquidity providers raise switching costs and widen spreads in stress. USDT+USDC ≈85% stablecoin share in 2024, concentrating fiat/settlement power. Top cloud providers (AWS 32%, Azure 23%, GCP 11%) and $188B cyber spend create vendor lock-in; multi-cloud and in-house tooling mitigate.

| Supplier | Key stat 2024 | Impact | Mitigant |

|---|---|---|---|

| Protocols | Bitcoin halving Apr 2024 → fees↑ | Higher settlement costs | Multi-chain support |

| Liquidity | Concentrated MM | Wider spreads | Multiple LPs/routing |

| Stablecoins | USDT+USDC ≈85% | Conversion risk | Diversified rails |

| Cloud/Sec | AWS32/AZ23/GCP11; $188B | Vendor lock-in | Multi-cloud/SLA |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Bakkt, uncovering key competitive drivers, buyer and supplier power, barriers to entry, substitutes and disruptive threats that shape pricing, market share and strategic positioning.

A concise one-sheet Porter's Five Forces for Bakkt that visualizes competitive pressures, regulatory risk, and partner dynamics—perfect for quickly identifying threats and opportunities and guiding strategic responses.

Customers Bargaining Power

High multi-homing among users

Consumers and institutions commonly multi-home across exchanges, brokers, and wallets, and 2024 surveys indicate a majority of crypto participants hold accounts on multiple platforms. Easy onboarding and similar feature sets keep switching costs low, letting buyers move volume rapidly to chase better price or liquidity. To retain flow Bakkt must emphasize trust, custodial security, and seamless integrations with clearing and institutional rails.

Price sensitivity and fee transparency

Trading, custody and withdrawal fees are benchmarked tightly across venues, with institutional clients demanding tiered pricing and rebates to match volume-driven economics. Buyers push for best execution and spreads compression, forcing Bakkt to price competitively. This persistent pricing pressure limits margin expansion on trading and custody services. Platform fee transparency becomes a table-stakes competitive requirement.

Institutional requirements and customization

Institutional clients in 2024 insist on strict SLAs, comprehensive reporting, auditability and tailored workflows, elevating procurement demands and giving buyers leverage. The requirement for bespoke integrations and RFP-driven procurement lengthens sales cycles and strengthens negotiation power, pressuring pricing and contract terms. Value-added services can command premiums only when providers demonstrate clear ROI and measurable metrics within enterprise audits.

Security and regulatory assurance expectations

Clients demand robust compliance, insurance and regulated custody; Bakkt Trust Company is a NYDFS‑licensed trust company as of 2024, so any perceived lapse triggers rapid attrition. Buyers can require SOC 2 or ISO 27001 attestations and third‑party insurance proofs. Superior governance and visible certifications reduce buyer bargaining power by increasing trust and stickiness.

- NYDFS license (Bakkt Trust Co., 2024)

- SOC 2 / ISO 27001 attestations

- Third‑party insurance proofs

- Governance reduces churn

Ecosystem integration demands

Ecosystem integration drives customer bargaining: API breadth, ERP/treasury connectors and analytics are top selection criteria, with a 2024 survey showing 68% of finance teams prioritize integration when choosing vendors.

Clients prefer vendors that reduce operational complexity; integration stickiness lowers switching but is treated as table stakes, and continuous alignment with client stacks is essential to retain enterprise accounts.

- API breadth: Enables rapid onboarding, reduces TCO

- ERP/treasury connectivity: Critical for cash management and reconciliation

- Analytics: Key differentiator shaping platform choice

Buyers hold leverage: 68% prioritize integration; compliance and tiered pricing squeeze margins

Buyers hold strong leverage: 2024 surveys show 68% of finance teams prioritize integration, while multi‑platform custody remains common, keeping switching costs low. Tight benchmarking of fees and demand for tiered pricing compresses margins and forces competitive pricing. Institutional SLAs, compliance proofs and NYDFS licensing (Bakkt Trust Co., 2024) shape contract terms and reduce churn.

| Metric | 2024 Fact |

|---|---|

| Integration priority | 68% of finance teams |

| Regulatory status | NYDFS license (Bakkt Trust Co., 2024) |

| Compliance proofs | SOC 2 / ISO 27001 common requirement |

What You See Is What You Get

Bakkt Porter's Five Forces Analysis

This preview shows the exact Bakkt Porter's Five Forces Analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase. No placeholders, mockups, or samples; the document shown is the deliverable. Use it as-is for research, presentations, or decision-making.