Baldwin Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

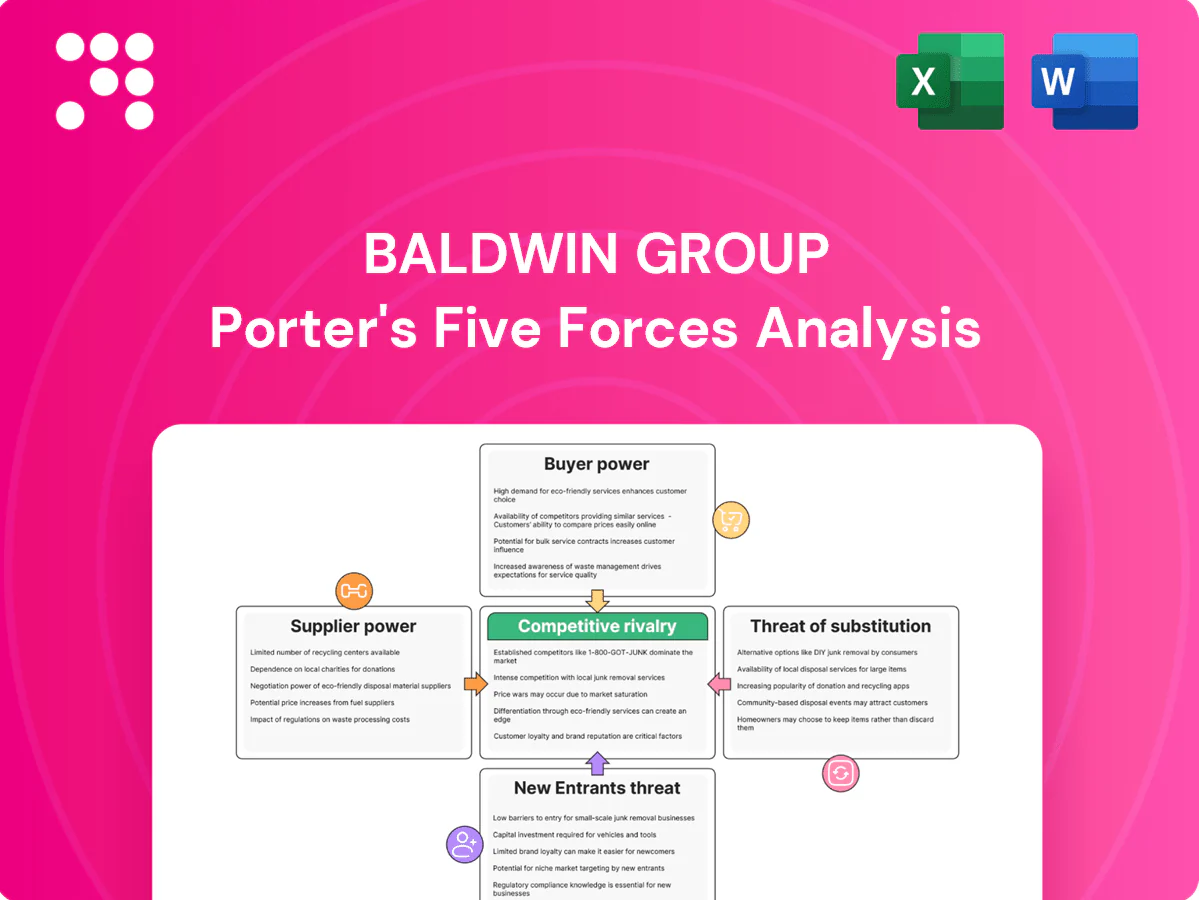

Baldwin Group faces moderate buyer power, concentrated supplier channels, and evolving substitute threats that shape its margin outlook; competitive rivalry is intensifying with niche entrants. This concise snapshot highlights key pressure points and strategic implications. Unlock the full Porter’s Five Forces Analysis to get detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Carrier concentration and terms

BRP Group relies on insurance carriers for capacity, product breadth and pricing, and in 2024 large national carriers retain outsized leverage through commission schedules, underwriting guidelines and profit‑sharing terms. Diversifying carrier panels and preserving production volume improves negotiating leverage. Strong loss‑ratio performance and niche expertise further moderate carrier power by making BRP a more attractive partner.

Reinsurer and MGA capacity

Specialty lines often depend on reinsurance-backed MGAs and programs, making reinsurer and MGA capacity a key supplier lever. Tight markets and catastrophe losses pushed reinsurance pricing up—Aon reported renewals rose roughly 20% in 2024—reducing capacity and increasing supplier power. BRP’s program scale and proprietary data help secure capacity continuity with reinsurers. Multi-year deals and panel optionality further mitigate disruption and pricing shocks.

Data, analytics, and tech vendors

Rating engines, comparative raters, AMS/CRM platforms and data providers form critical infrastructure for Baldwin Group, and with the global enterprise software market near $600 billion in 2024 these vendors hold significant leverage. Vendor switching costs, complex integrations and training create durable lock-in that raises supplier power. Baldwin's scale enables negotiation of enterprise contracts and owning data models and middleware progressively reduces dependency.

Talent and producer pipelines

Experienced producers and niche advisors act as quasi-suppliers of revenue for Baldwin Group; scarcity in specialty verticals drives higher compensation and retention costs, with 2024 industry reports noting turnover premiums up to 20% in specialist roles.

BRP’s equity-based incentives and clear career pathways can mitigate supplier power; training academies and M&A acquihires have expanded the talent pipeline by reported gains of ~15% in hire velocity in 2024.

- Producers as revenue suppliers: high leverage

- Scarcity premiums: ~20% uplift

- Equity incentives: retention lever

- Training/M&A: ~15% faster hiring

Lead, referral, and channel partners

- Channel concentration risk: mitigated by multi-vertical presence

- Referral costs: volume/fee clauses raise CPA

- Owned demand gen: lowers partner bargaining power

2024 suppliers command leverage: +~20%, $600B

BRP's suppliers—carriers, reinsurers, software vendors and producers—exert high bargaining power in 2024: reinsurance renewals +~20%, global enterprise software market ~$600B, specialist turnover premium ~20%. Scale, strong loss ratios, equity incentives and owned demand gen reduce supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +~20% renewals | High |

| Carriers | Concentrated panels | High |

| Software | $600B market | Medium |

| Producers | +~20% premiums | High |

What is included in the product

Combines a focused Porter’s Five Forces assessment tailored to Baldwin Group, uncovering competitive intensity, buyer and supplier power, substitute threats, and entry barriers to reveal strategic vulnerabilities and opportunities for profitability and market defense.

A concise, one-sheet Porter’s Five Forces analysis for Baldwin Group—instantly reveals competitive pressure and strategic pain points for quick decisions or boardroom slides.

Customers Bargaining Power

Price sensitivity in commercial lines

Middle-market clients benchmark rates and broker fees annually, driving intense price sensitivity as competitive quoting and 2024 market cycles increase buyer leverage on pricing. BRP can offset this by bundling risk advisory and claims advocacy to deepen value capture. Demonstrable loss cost reduction and documented claims outcomes reduce pure price shopping and improve retention.

Switching costs and relationships

Broker-of-record changes are administratively simple but remain relationship-driven, so many clients delay moves despite ease of paperwork. Deep service integration, captive/program design and multi-year plans (commonly 3-year terms) materially raise switching costs. BRP’s partner-firm local presence strengthens client stickiness through face-to-face servicing. Client portals and analytics create continuity benefits by preserving data and plan history across transitions.

Large accounts and benefits buyers

Enterprise clients and benefits committees command bespoke terms and service SLAs, insisting on data transparency, fee disclosure and measurable outcomes. Large accounts drive scale: employer-sponsored plans covered about 155 million people in the US by 2023, concentrating negotiating power. BRP must deploy specialized client teams and benchmarking analytics to retain them. Multi-line cross-sell across benefits lines can dilute individual account bargaining leverage.

SMB and personal lines shoppers

SMB and personal-lines shoppers are highly price-sensitive and quick to switch via online channels; 2024 studies show about 61% of SMBs research insurance digitally and aggregators captured roughly 35% of personal-lines quote volume, increasing buyer leverage. BRP can counter with instant digital quoting plus advisory upsells, while strong community presence and convenient service reduce churn.

- price-driven

- 61% research digitally (2024)

- aggregators ~35% quote share (2024)

- digital quoting + advisory

- community reduces churn

Demand for digital and self-service

Clients now expect instant quotes, certificates and real-time claims updates; Salesforce 2024 found 70% of customers expect firms to understand their needs and 64% prefer self-service channels. Lack of digital parity increases buyer leverage and churn risk, while BRP’s tech enablement can deliver self-service workflows without eroding advisory value. Embedded analytics personalize offers to boost retention and CLV.

- Instant access: reduces churn

- Digital parity: lowers buyer leverage

- BRP tech: preserves advice + self-service

- Analytics: improves retention, CLV

Buyers power: 155m covered; ~35% aggregator quote share

Buyers exert moderate-to-high power: enterprise accounts (155m covered in US, 2023) demand bespoke SLAs, while SMBs are price-sensitive (61% research digitally, 2024) and aggregators captured ~35% personal-lines quote volume (2024). Digital parity (70% expect firms to understand needs; 64% prefer self-service, Salesforce 2024) and instant quoting raise churn risk; BRP offsets via bundling, analytics and local service.

| Metric | Value |

|---|---|

| Employer-sponsored covered (US) | 155m (2023) |

| SMBs researching digitally | 61% (2024) |

| Aggregator quote share | ~35% (2024) |

| Customer expectations | 70% understand / 64% self-service (Salesforce 2024) |

Same Document Delivered

Baldwin Group Porter's Five Forces Analysis

This preview displays the Baldwin Group Porter's Five Forces Analysis exactly as delivered after purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use once you buy. What you see is the complete file you'll receive.

From Overview to Strategy Blueprint

Baldwin Group faces moderate buyer power, concentrated supplier channels, and evolving substitute threats that shape its margin outlook; competitive rivalry is intensifying with niche entrants. This concise snapshot highlights key pressure points and strategic implications. Unlock the full Porter’s Five Forces Analysis to get detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Carrier concentration and terms

BRP Group relies on insurance carriers for capacity, product breadth and pricing, and in 2024 large national carriers retain outsized leverage through commission schedules, underwriting guidelines and profit‑sharing terms. Diversifying carrier panels and preserving production volume improves negotiating leverage. Strong loss‑ratio performance and niche expertise further moderate carrier power by making BRP a more attractive partner.

Reinsurer and MGA capacity

Specialty lines often depend on reinsurance-backed MGAs and programs, making reinsurer and MGA capacity a key supplier lever. Tight markets and catastrophe losses pushed reinsurance pricing up—Aon reported renewals rose roughly 20% in 2024—reducing capacity and increasing supplier power. BRP’s program scale and proprietary data help secure capacity continuity with reinsurers. Multi-year deals and panel optionality further mitigate disruption and pricing shocks.

Data, analytics, and tech vendors

Rating engines, comparative raters, AMS/CRM platforms and data providers form critical infrastructure for Baldwin Group, and with the global enterprise software market near $600 billion in 2024 these vendors hold significant leverage. Vendor switching costs, complex integrations and training create durable lock-in that raises supplier power. Baldwin's scale enables negotiation of enterprise contracts and owning data models and middleware progressively reduces dependency.

Talent and producer pipelines

Experienced producers and niche advisors act as quasi-suppliers of revenue for Baldwin Group; scarcity in specialty verticals drives higher compensation and retention costs, with 2024 industry reports noting turnover premiums up to 20% in specialist roles.

BRP’s equity-based incentives and clear career pathways can mitigate supplier power; training academies and M&A acquihires have expanded the talent pipeline by reported gains of ~15% in hire velocity in 2024.

- Producers as revenue suppliers: high leverage

- Scarcity premiums: ~20% uplift

- Equity incentives: retention lever

- Training/M&A: ~15% faster hiring

Lead, referral, and channel partners

- Channel concentration risk: mitigated by multi-vertical presence

- Referral costs: volume/fee clauses raise CPA

- Owned demand gen: lowers partner bargaining power

2024 suppliers command leverage: +~20%, $600B

BRP's suppliers—carriers, reinsurers, software vendors and producers—exert high bargaining power in 2024: reinsurance renewals +~20%, global enterprise software market ~$600B, specialist turnover premium ~20%. Scale, strong loss ratios, equity incentives and owned demand gen reduce supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +~20% renewals | High |

| Carriers | Concentrated panels | High |

| Software | $600B market | Medium |

| Producers | +~20% premiums | High |

What is included in the product

Combines a focused Porter’s Five Forces assessment tailored to Baldwin Group, uncovering competitive intensity, buyer and supplier power, substitute threats, and entry barriers to reveal strategic vulnerabilities and opportunities for profitability and market defense.

A concise, one-sheet Porter’s Five Forces analysis for Baldwin Group—instantly reveals competitive pressure and strategic pain points for quick decisions or boardroom slides.

Customers Bargaining Power

Price sensitivity in commercial lines

Middle-market clients benchmark rates and broker fees annually, driving intense price sensitivity as competitive quoting and 2024 market cycles increase buyer leverage on pricing. BRP can offset this by bundling risk advisory and claims advocacy to deepen value capture. Demonstrable loss cost reduction and documented claims outcomes reduce pure price shopping and improve retention.

Switching costs and relationships

Broker-of-record changes are administratively simple but remain relationship-driven, so many clients delay moves despite ease of paperwork. Deep service integration, captive/program design and multi-year plans (commonly 3-year terms) materially raise switching costs. BRP’s partner-firm local presence strengthens client stickiness through face-to-face servicing. Client portals and analytics create continuity benefits by preserving data and plan history across transitions.

Large accounts and benefits buyers

Enterprise clients and benefits committees command bespoke terms and service SLAs, insisting on data transparency, fee disclosure and measurable outcomes. Large accounts drive scale: employer-sponsored plans covered about 155 million people in the US by 2023, concentrating negotiating power. BRP must deploy specialized client teams and benchmarking analytics to retain them. Multi-line cross-sell across benefits lines can dilute individual account bargaining leverage.

SMB and personal lines shoppers

SMB and personal-lines shoppers are highly price-sensitive and quick to switch via online channels; 2024 studies show about 61% of SMBs research insurance digitally and aggregators captured roughly 35% of personal-lines quote volume, increasing buyer leverage. BRP can counter with instant digital quoting plus advisory upsells, while strong community presence and convenient service reduce churn.

- price-driven

- 61% research digitally (2024)

- aggregators ~35% quote share (2024)

- digital quoting + advisory

- community reduces churn

Demand for digital and self-service

Clients now expect instant quotes, certificates and real-time claims updates; Salesforce 2024 found 70% of customers expect firms to understand their needs and 64% prefer self-service channels. Lack of digital parity increases buyer leverage and churn risk, while BRP’s tech enablement can deliver self-service workflows without eroding advisory value. Embedded analytics personalize offers to boost retention and CLV.

- Instant access: reduces churn

- Digital parity: lowers buyer leverage

- BRP tech: preserves advice + self-service

- Analytics: improves retention, CLV

Buyers power: 155m covered; ~35% aggregator quote share

Buyers exert moderate-to-high power: enterprise accounts (155m covered in US, 2023) demand bespoke SLAs, while SMBs are price-sensitive (61% research digitally, 2024) and aggregators captured ~35% personal-lines quote volume (2024). Digital parity (70% expect firms to understand needs; 64% prefer self-service, Salesforce 2024) and instant quoting raise churn risk; BRP offsets via bundling, analytics and local service.

| Metric | Value |

|---|---|

| Employer-sponsored covered (US) | 155m (2023) |

| SMBs researching digitally | 61% (2024) |

| Aggregator quote share | ~35% (2024) |

| Customer expectations | 70% understand / 64% self-service (Salesforce 2024) |

Same Document Delivered

Baldwin Group Porter's Five Forces Analysis

This preview displays the Baldwin Group Porter's Five Forces Analysis exactly as delivered after purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use once you buy. What you see is the complete file you'll receive.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Baldwin Group faces moderate buyer power, concentrated supplier channels, and evolving substitute threats that shape its margin outlook; competitive rivalry is intensifying with niche entrants. This concise snapshot highlights key pressure points and strategic implications. Unlock the full Porter’s Five Forces Analysis to get detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Carrier concentration and terms

BRP Group relies on insurance carriers for capacity, product breadth and pricing, and in 2024 large national carriers retain outsized leverage through commission schedules, underwriting guidelines and profit‑sharing terms. Diversifying carrier panels and preserving production volume improves negotiating leverage. Strong loss‑ratio performance and niche expertise further moderate carrier power by making BRP a more attractive partner.

Reinsurer and MGA capacity

Specialty lines often depend on reinsurance-backed MGAs and programs, making reinsurer and MGA capacity a key supplier lever. Tight markets and catastrophe losses pushed reinsurance pricing up—Aon reported renewals rose roughly 20% in 2024—reducing capacity and increasing supplier power. BRP’s program scale and proprietary data help secure capacity continuity with reinsurers. Multi-year deals and panel optionality further mitigate disruption and pricing shocks.

Data, analytics, and tech vendors

Rating engines, comparative raters, AMS/CRM platforms and data providers form critical infrastructure for Baldwin Group, and with the global enterprise software market near $600 billion in 2024 these vendors hold significant leverage. Vendor switching costs, complex integrations and training create durable lock-in that raises supplier power. Baldwin's scale enables negotiation of enterprise contracts and owning data models and middleware progressively reduces dependency.

Talent and producer pipelines

Experienced producers and niche advisors act as quasi-suppliers of revenue for Baldwin Group; scarcity in specialty verticals drives higher compensation and retention costs, with 2024 industry reports noting turnover premiums up to 20% in specialist roles.

BRP’s equity-based incentives and clear career pathways can mitigate supplier power; training academies and M&A acquihires have expanded the talent pipeline by reported gains of ~15% in hire velocity in 2024.

- Producers as revenue suppliers: high leverage

- Scarcity premiums: ~20% uplift

- Equity incentives: retention lever

- Training/M&A: ~15% faster hiring

Lead, referral, and channel partners

- Channel concentration risk: mitigated by multi-vertical presence

- Referral costs: volume/fee clauses raise CPA

- Owned demand gen: lowers partner bargaining power

2024 suppliers command leverage: +~20%, $600B

BRP's suppliers—carriers, reinsurers, software vendors and producers—exert high bargaining power in 2024: reinsurance renewals +~20%, global enterprise software market ~$600B, specialist turnover premium ~20%. Scale, strong loss ratios, equity incentives and owned demand gen reduce supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +~20% renewals | High |

| Carriers | Concentrated panels | High |

| Software | $600B market | Medium |

| Producers | +~20% premiums | High |

What is included in the product

Combines a focused Porter’s Five Forces assessment tailored to Baldwin Group, uncovering competitive intensity, buyer and supplier power, substitute threats, and entry barriers to reveal strategic vulnerabilities and opportunities for profitability and market defense.

A concise, one-sheet Porter’s Five Forces analysis for Baldwin Group—instantly reveals competitive pressure and strategic pain points for quick decisions or boardroom slides.

Customers Bargaining Power

Price sensitivity in commercial lines

Middle-market clients benchmark rates and broker fees annually, driving intense price sensitivity as competitive quoting and 2024 market cycles increase buyer leverage on pricing. BRP can offset this by bundling risk advisory and claims advocacy to deepen value capture. Demonstrable loss cost reduction and documented claims outcomes reduce pure price shopping and improve retention.

Switching costs and relationships

Broker-of-record changes are administratively simple but remain relationship-driven, so many clients delay moves despite ease of paperwork. Deep service integration, captive/program design and multi-year plans (commonly 3-year terms) materially raise switching costs. BRP’s partner-firm local presence strengthens client stickiness through face-to-face servicing. Client portals and analytics create continuity benefits by preserving data and plan history across transitions.

Large accounts and benefits buyers

Enterprise clients and benefits committees command bespoke terms and service SLAs, insisting on data transparency, fee disclosure and measurable outcomes. Large accounts drive scale: employer-sponsored plans covered about 155 million people in the US by 2023, concentrating negotiating power. BRP must deploy specialized client teams and benchmarking analytics to retain them. Multi-line cross-sell across benefits lines can dilute individual account bargaining leverage.

SMB and personal lines shoppers

SMB and personal-lines shoppers are highly price-sensitive and quick to switch via online channels; 2024 studies show about 61% of SMBs research insurance digitally and aggregators captured roughly 35% of personal-lines quote volume, increasing buyer leverage. BRP can counter with instant digital quoting plus advisory upsells, while strong community presence and convenient service reduce churn.

- price-driven

- 61% research digitally (2024)

- aggregators ~35% quote share (2024)

- digital quoting + advisory

- community reduces churn

Demand for digital and self-service

Clients now expect instant quotes, certificates and real-time claims updates; Salesforce 2024 found 70% of customers expect firms to understand their needs and 64% prefer self-service channels. Lack of digital parity increases buyer leverage and churn risk, while BRP’s tech enablement can deliver self-service workflows without eroding advisory value. Embedded analytics personalize offers to boost retention and CLV.

- Instant access: reduces churn

- Digital parity: lowers buyer leverage

- BRP tech: preserves advice + self-service

- Analytics: improves retention, CLV

Buyers power: 155m covered; ~35% aggregator quote share

Buyers exert moderate-to-high power: enterprise accounts (155m covered in US, 2023) demand bespoke SLAs, while SMBs are price-sensitive (61% research digitally, 2024) and aggregators captured ~35% personal-lines quote volume (2024). Digital parity (70% expect firms to understand needs; 64% prefer self-service, Salesforce 2024) and instant quoting raise churn risk; BRP offsets via bundling, analytics and local service.

| Metric | Value |

|---|---|

| Employer-sponsored covered (US) | 155m (2023) |

| SMBs researching digitally | 61% (2024) |

| Aggregator quote share | ~35% (2024) |

| Customer expectations | 70% understand / 64% self-service (Salesforce 2024) |

Same Document Delivered

Baldwin Group Porter's Five Forces Analysis

This preview displays the Baldwin Group Porter's Five Forces Analysis exactly as delivered after purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use once you buy. What you see is the complete file you'll receive.