Ball PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain an edge with our concise PESTLE Analysis of Ball, revealing how political, economic, and technological trends shape its outlook. Ideal for investors, strategists, and consultants, it translates complex external forces into actionable risks and opportunities. Buy the full report to access the detailed breakdown, editable charts, and immediate download for boardroom-ready insights.

Political factors

Trade and tariff exposure

Aluminum sheet and ingot flows face tariffs, sanctions and quotas — notably the US Section 232 10% aluminum tariff (2018) — that can raise Ball’s input costs and constrain sourcing. China accounts for roughly 55% of global primary aluminium production (2023–24), so shifts in US, EU or China trade policy ripple through the beverage can supply chain. Proactive hedging and diversified suppliers mitigate these shocks.

Recycling and EPR policies

Deposit return schemes and EPR laws significantly affect can recovery and design; DRS in Norway and Germany yield return rates around 97–98%, boosting collection quality and secondary supply. Jurisdictional variance forces Ball to adapt logistics, labeling and compliance budgets across markets, increasing operating and capex requirements in fragmented regions. Higher collection targets favor aluminum, which saves up to 95% energy vs primary production and retains strong scrap value.

Subsidies for decarbonization

The US Inflation Reduction Act mobilizes roughly $369 billion for clean energy and industrial decarbonization and the EU Green Deal aims to unlock €1 trillion over the next decade; both offer grants, production/investment tax credits and accelerated depreciation. Accessing IRA tax credits and EU grants can cut electrification CAPEX by 20–40% and de‑risk renewable PPA pricing. Policy stability directly influences timing of multi‑year capital deployment and payback assumptions.

Government aerospace budgets

Government defense and space spending cycles drive Ball’s aerospace backlog and margin profile; US DoD/FY2025 topline hovered near $842 billion while NASA’s FY2025 request was about $27.2 billion, influencing contract pacing and margins. Appropriations, continuing resolutions and shifting priorities can delay awards and cash flows. International collaboration depends on alliances and export regimes (ITAR/Export Control) that affect timing and eligible partners.

- Backlog sensitivity: high to US defense budget (~$842B FY2025)

- Program risk: delays from CRs/appropriations

- Export/alliance constraints: ITAR impacts international sales

Geopolitical energy volatility

Geopolitical energy volatility drives spikes—European TTF gas surged over 300% in 2022, increasing power costs that directly raise smelting and can-making input costs; aluminium smelting consumes roughly 13–15 MWh per tonne.

Political risk in bauxite and alumina regions (notably Guinea and parts of Brazil) threatens supply; Guinea holds about 25% of global bauxite reserves (USGS 2023).

Contingency planning via diversified sourcing, longer inventory buffers and alternative energy contracts reduces production disruption and outage exposure.

- Energy shock: TTF gas +300% (2022)

- Smelting energy: ~13–15 MWh/tonne

- Guinea bauxite: ~25% of global reserves (USGS 2023)

China ~55% and Guinea ~25% reshape aluminium geopolitics

Tariffs (US Section 232 10%) and China’s ~55% of primary aluminium (2024) concentrate trade risk, while Guinea’s ~25% bauxite reserves create supply geopolitics; DRS/EPR (Norway/Germany ~97–98% return) shift demand to recycled aluminium; US defense ($842B FY2025) and IRA (~$369B) influence aerospace orders and decarbonization CAPEX.

| Metric | Value |

|---|---|

| US tariff | 10% |

| China share | ~55% (2024) |

| Guinea reserves | ~25% |

| US defense | $842B FY2025 |

| IRA funding | $369B |

| DRS return | 97–98% |

What is included in the product

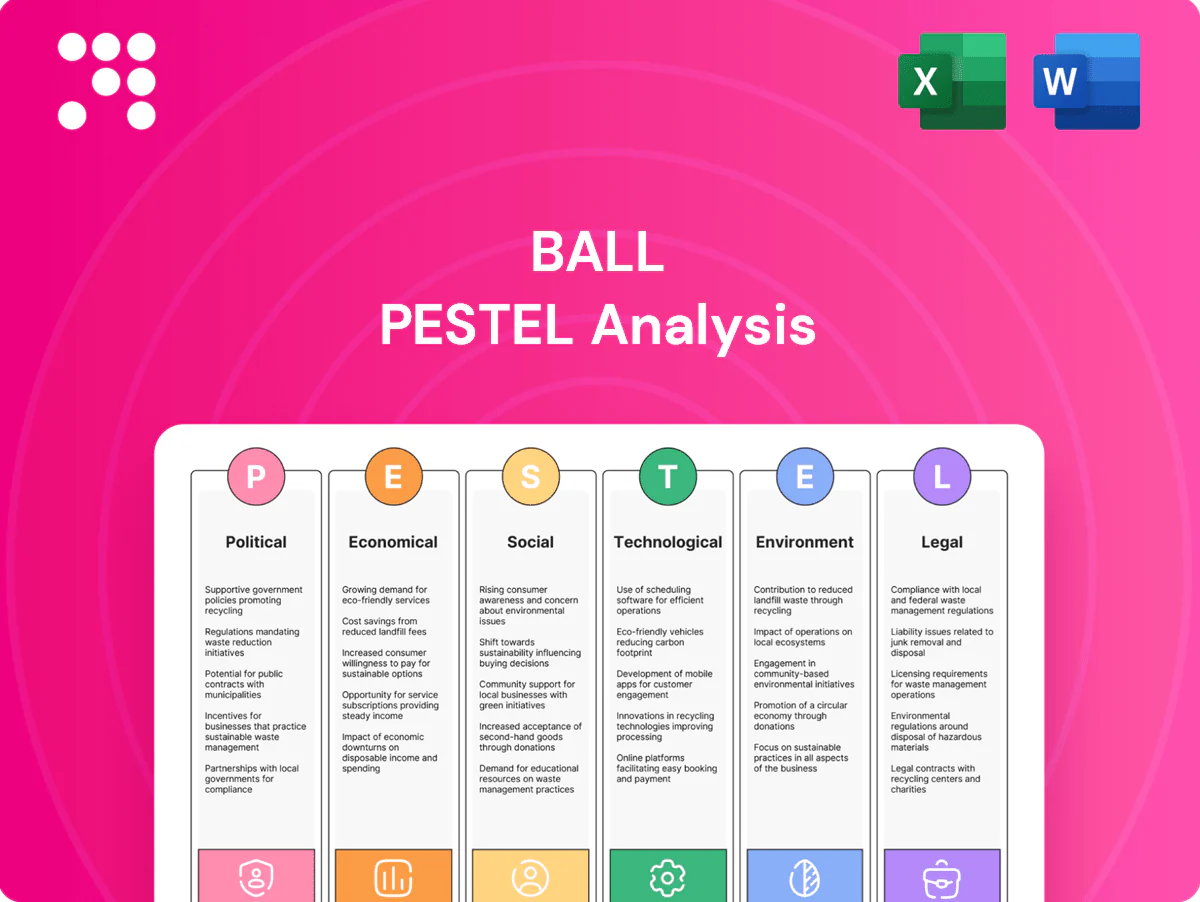

Explores how external macro-environmental factors uniquely affect Ball across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends. Designed for executives and investors, it reflects real market and regulatory dynamics, offers forward-looking insights, and is formatted for direct use in plans, decks, or reports.

Provides a clean, summarized PESTLE of Ball, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Aluminum price volatility

LME aluminium price volatility (≈$2,400/ton mid‑2025) plus Midwest premiums (~$150/ton) and European premiums (~€250/ton) drive Ball's COGS and contract pass‑through timing. Hedging programs smooth earnings volatility but do not alter volume elasticity tied to end‑market demand. Scrap spreads (~$300/ton) improve the economics of higher recycled content, reducing marginal COGS when scrap is available.

Beverage demand cycles

Macro conditions and category mix drove can volumes across beer, soft drinks, energy and seltzers in 2024, with premium seltzer and energy up while mainstream beer was flat; overall aluminum can demand rose modestly. Retail channel shifts and private label penetration (about 15–20% in several markets) changed SKU mix and utilization. Emerging markets grew roughly 5–7% in 2024, offsetting mature market stagnation near 0–1%.

FX and interest rates

Multi-currency revenues and costs expose Ball to translation and transaction risk given its significant international footprint, affecting reported results when USD moves against EUR, CAD and BRL. Elevated policy rates (US federal funds 5.25–5.50% in 2024; ECB deposit rate 4.00% in 2024) influence Ball’s capex, refinancing costs and customer investment timing. Balanced regional funding reduces currency and maturity mismatches and supports liquidity resilience.

Energy and logistics costs

Rising power and gas costs drive smelter and can-plant margins—US industrial electricity averaged about $0.094/kWh in 2024 and Henry Hub gas averaged ~$3.64/MMBtu, raising aluminum input costs that can be 30–40% of smelter cost; freight volatility and port congestion (BDI ~1,200 average in 2024; Shanghai–LA container rates ~ $1,500/TEU in 2024) lengthen lead times and inflate inventory; network optimization and modal shifts protect margins.

- Energy: US industrial power $0.094/kWh (2024)

- Gas: Henry Hub ~$3.64/MMBtu (2024)

- Freight: BDI ~1,200 (2024), Shanghai–LA ~$1,500/TEU (2024)

- Impact: aluminum energy share 30–40% of smelter costs

Labor availability and wages

Tight labor markets pushed US manufacturing average hourly earnings up ~4.5% year‑over‑year in 2024 (BLS), raising wages and training costs in Ball’s production hubs; automation investments have offset some labor pressure by stabilizing throughput and improving quality metrics. Union dynamics and retention influence uptime, with negotiated work rules and turnover directly affecting utilization and OEE.

- Wage growth: ~4.5% (US manufacturing, 2024)

- Automation: reduces variability, raises capex but lowers labor per unit

- Union/retention: impacts uptime and maintenance scheduling

China ~55% and Guinea ~25% reshape aluminium geopolitics

LME aluminium ~ $2,400/ton (mid‑2025) plus Midwest premium ~$150/ton and EU premium ~€250/ton drive Ball’s COGS and pass‑through timing; scrap spreads ~ $300/ton lower marginal costs when available. Energy/gas (US power $0.094/kWh; Henry Hub ~$3.64/MMBtu in 2024), freight (BDI ~1,200; SH‑LA ~$1,500/TEU) and wage growth ~4.5% (US, 2024) compress margins; hedging and automation mitigate volatility.

| Metric | Value |

|---|---|

| LME | $2,400/ton |

| Midwest premium | $150/ton |

| EU premium | €250/ton |

| Scrap spread | $300/ton |

| US power | $0.094/kWh (2024) |

| Henry Hub | $3.64/MMBtu (2024) |

| BDI | ~1,200 (2024) |

| SH‑LA | $1,500/TEU (2024) |

| Wage growth | ~4.5% (US manufacturing, 2024) |

Preview the Actual Deliverable

Ball PESTLE Analysis

The Ball PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the final version with no placeholders or teasers, delivered exactly as displayed. The layout, content, and structure are identical to the downloadable file you’ll get immediately after checkout. What you see is the real, finished product.

Your Shortcut to Market Insight Starts Here

Gain an edge with our concise PESTLE Analysis of Ball, revealing how political, economic, and technological trends shape its outlook. Ideal for investors, strategists, and consultants, it translates complex external forces into actionable risks and opportunities. Buy the full report to access the detailed breakdown, editable charts, and immediate download for boardroom-ready insights.

Political factors

Trade and tariff exposure

Aluminum sheet and ingot flows face tariffs, sanctions and quotas — notably the US Section 232 10% aluminum tariff (2018) — that can raise Ball’s input costs and constrain sourcing. China accounts for roughly 55% of global primary aluminium production (2023–24), so shifts in US, EU or China trade policy ripple through the beverage can supply chain. Proactive hedging and diversified suppliers mitigate these shocks.

Recycling and EPR policies

Deposit return schemes and EPR laws significantly affect can recovery and design; DRS in Norway and Germany yield return rates around 97–98%, boosting collection quality and secondary supply. Jurisdictional variance forces Ball to adapt logistics, labeling and compliance budgets across markets, increasing operating and capex requirements in fragmented regions. Higher collection targets favor aluminum, which saves up to 95% energy vs primary production and retains strong scrap value.

Subsidies for decarbonization

The US Inflation Reduction Act mobilizes roughly $369 billion for clean energy and industrial decarbonization and the EU Green Deal aims to unlock €1 trillion over the next decade; both offer grants, production/investment tax credits and accelerated depreciation. Accessing IRA tax credits and EU grants can cut electrification CAPEX by 20–40% and de‑risk renewable PPA pricing. Policy stability directly influences timing of multi‑year capital deployment and payback assumptions.

Government aerospace budgets

Government defense and space spending cycles drive Ball’s aerospace backlog and margin profile; US DoD/FY2025 topline hovered near $842 billion while NASA’s FY2025 request was about $27.2 billion, influencing contract pacing and margins. Appropriations, continuing resolutions and shifting priorities can delay awards and cash flows. International collaboration depends on alliances and export regimes (ITAR/Export Control) that affect timing and eligible partners.

- Backlog sensitivity: high to US defense budget (~$842B FY2025)

- Program risk: delays from CRs/appropriations

- Export/alliance constraints: ITAR impacts international sales

Geopolitical energy volatility

Geopolitical energy volatility drives spikes—European TTF gas surged over 300% in 2022, increasing power costs that directly raise smelting and can-making input costs; aluminium smelting consumes roughly 13–15 MWh per tonne.

Political risk in bauxite and alumina regions (notably Guinea and parts of Brazil) threatens supply; Guinea holds about 25% of global bauxite reserves (USGS 2023).

Contingency planning via diversified sourcing, longer inventory buffers and alternative energy contracts reduces production disruption and outage exposure.

- Energy shock: TTF gas +300% (2022)

- Smelting energy: ~13–15 MWh/tonne

- Guinea bauxite: ~25% of global reserves (USGS 2023)

China ~55% and Guinea ~25% reshape aluminium geopolitics

Tariffs (US Section 232 10%) and China’s ~55% of primary aluminium (2024) concentrate trade risk, while Guinea’s ~25% bauxite reserves create supply geopolitics; DRS/EPR (Norway/Germany ~97–98% return) shift demand to recycled aluminium; US defense ($842B FY2025) and IRA (~$369B) influence aerospace orders and decarbonization CAPEX.

| Metric | Value |

|---|---|

| US tariff | 10% |

| China share | ~55% (2024) |

| Guinea reserves | ~25% |

| US defense | $842B FY2025 |

| IRA funding | $369B |

| DRS return | 97–98% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ball across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends. Designed for executives and investors, it reflects real market and regulatory dynamics, offers forward-looking insights, and is formatted for direct use in plans, decks, or reports.

Provides a clean, summarized PESTLE of Ball, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Aluminum price volatility

LME aluminium price volatility (≈$2,400/ton mid‑2025) plus Midwest premiums (~$150/ton) and European premiums (~€250/ton) drive Ball's COGS and contract pass‑through timing. Hedging programs smooth earnings volatility but do not alter volume elasticity tied to end‑market demand. Scrap spreads (~$300/ton) improve the economics of higher recycled content, reducing marginal COGS when scrap is available.

Beverage demand cycles

Macro conditions and category mix drove can volumes across beer, soft drinks, energy and seltzers in 2024, with premium seltzer and energy up while mainstream beer was flat; overall aluminum can demand rose modestly. Retail channel shifts and private label penetration (about 15–20% in several markets) changed SKU mix and utilization. Emerging markets grew roughly 5–7% in 2024, offsetting mature market stagnation near 0–1%.

FX and interest rates

Multi-currency revenues and costs expose Ball to translation and transaction risk given its significant international footprint, affecting reported results when USD moves against EUR, CAD and BRL. Elevated policy rates (US federal funds 5.25–5.50% in 2024; ECB deposit rate 4.00% in 2024) influence Ball’s capex, refinancing costs and customer investment timing. Balanced regional funding reduces currency and maturity mismatches and supports liquidity resilience.

Energy and logistics costs

Rising power and gas costs drive smelter and can-plant margins—US industrial electricity averaged about $0.094/kWh in 2024 and Henry Hub gas averaged ~$3.64/MMBtu, raising aluminum input costs that can be 30–40% of smelter cost; freight volatility and port congestion (BDI ~1,200 average in 2024; Shanghai–LA container rates ~ $1,500/TEU in 2024) lengthen lead times and inflate inventory; network optimization and modal shifts protect margins.

- Energy: US industrial power $0.094/kWh (2024)

- Gas: Henry Hub ~$3.64/MMBtu (2024)

- Freight: BDI ~1,200 (2024), Shanghai–LA ~$1,500/TEU (2024)

- Impact: aluminum energy share 30–40% of smelter costs

Labor availability and wages

Tight labor markets pushed US manufacturing average hourly earnings up ~4.5% year‑over‑year in 2024 (BLS), raising wages and training costs in Ball’s production hubs; automation investments have offset some labor pressure by stabilizing throughput and improving quality metrics. Union dynamics and retention influence uptime, with negotiated work rules and turnover directly affecting utilization and OEE.

- Wage growth: ~4.5% (US manufacturing, 2024)

- Automation: reduces variability, raises capex but lowers labor per unit

- Union/retention: impacts uptime and maintenance scheduling

China ~55% and Guinea ~25% reshape aluminium geopolitics

LME aluminium ~ $2,400/ton (mid‑2025) plus Midwest premium ~$150/ton and EU premium ~€250/ton drive Ball’s COGS and pass‑through timing; scrap spreads ~ $300/ton lower marginal costs when available. Energy/gas (US power $0.094/kWh; Henry Hub ~$3.64/MMBtu in 2024), freight (BDI ~1,200; SH‑LA ~$1,500/TEU) and wage growth ~4.5% (US, 2024) compress margins; hedging and automation mitigate volatility.

| Metric | Value |

|---|---|

| LME | $2,400/ton |

| Midwest premium | $150/ton |

| EU premium | €250/ton |

| Scrap spread | $300/ton |

| US power | $0.094/kWh (2024) |

| Henry Hub | $3.64/MMBtu (2024) |

| BDI | ~1,200 (2024) |

| SH‑LA | $1,500/TEU (2024) |

| Wage growth | ~4.5% (US manufacturing, 2024) |

Preview the Actual Deliverable

Ball PESTLE Analysis

The Ball PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the final version with no placeholders or teasers, delivered exactly as displayed. The layout, content, and structure are identical to the downloadable file you’ll get immediately after checkout. What you see is the real, finished product.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain an edge with our concise PESTLE Analysis of Ball, revealing how political, economic, and technological trends shape its outlook. Ideal for investors, strategists, and consultants, it translates complex external forces into actionable risks and opportunities. Buy the full report to access the detailed breakdown, editable charts, and immediate download for boardroom-ready insights.

Political factors

Trade and tariff exposure

Aluminum sheet and ingot flows face tariffs, sanctions and quotas — notably the US Section 232 10% aluminum tariff (2018) — that can raise Ball’s input costs and constrain sourcing. China accounts for roughly 55% of global primary aluminium production (2023–24), so shifts in US, EU or China trade policy ripple through the beverage can supply chain. Proactive hedging and diversified suppliers mitigate these shocks.

Recycling and EPR policies

Deposit return schemes and EPR laws significantly affect can recovery and design; DRS in Norway and Germany yield return rates around 97–98%, boosting collection quality and secondary supply. Jurisdictional variance forces Ball to adapt logistics, labeling and compliance budgets across markets, increasing operating and capex requirements in fragmented regions. Higher collection targets favor aluminum, which saves up to 95% energy vs primary production and retains strong scrap value.

Subsidies for decarbonization

The US Inflation Reduction Act mobilizes roughly $369 billion for clean energy and industrial decarbonization and the EU Green Deal aims to unlock €1 trillion over the next decade; both offer grants, production/investment tax credits and accelerated depreciation. Accessing IRA tax credits and EU grants can cut electrification CAPEX by 20–40% and de‑risk renewable PPA pricing. Policy stability directly influences timing of multi‑year capital deployment and payback assumptions.

Government aerospace budgets

Government defense and space spending cycles drive Ball’s aerospace backlog and margin profile; US DoD/FY2025 topline hovered near $842 billion while NASA’s FY2025 request was about $27.2 billion, influencing contract pacing and margins. Appropriations, continuing resolutions and shifting priorities can delay awards and cash flows. International collaboration depends on alliances and export regimes (ITAR/Export Control) that affect timing and eligible partners.

- Backlog sensitivity: high to US defense budget (~$842B FY2025)

- Program risk: delays from CRs/appropriations

- Export/alliance constraints: ITAR impacts international sales

Geopolitical energy volatility

Geopolitical energy volatility drives spikes—European TTF gas surged over 300% in 2022, increasing power costs that directly raise smelting and can-making input costs; aluminium smelting consumes roughly 13–15 MWh per tonne.

Political risk in bauxite and alumina regions (notably Guinea and parts of Brazil) threatens supply; Guinea holds about 25% of global bauxite reserves (USGS 2023).

Contingency planning via diversified sourcing, longer inventory buffers and alternative energy contracts reduces production disruption and outage exposure.

- Energy shock: TTF gas +300% (2022)

- Smelting energy: ~13–15 MWh/tonne

- Guinea bauxite: ~25% of global reserves (USGS 2023)

China ~55% and Guinea ~25% reshape aluminium geopolitics

Tariffs (US Section 232 10%) and China’s ~55% of primary aluminium (2024) concentrate trade risk, while Guinea’s ~25% bauxite reserves create supply geopolitics; DRS/EPR (Norway/Germany ~97–98% return) shift demand to recycled aluminium; US defense ($842B FY2025) and IRA (~$369B) influence aerospace orders and decarbonization CAPEX.

| Metric | Value |

|---|---|

| US tariff | 10% |

| China share | ~55% (2024) |

| Guinea reserves | ~25% |

| US defense | $842B FY2025 |

| IRA funding | $369B |

| DRS return | 97–98% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ball across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends. Designed for executives and investors, it reflects real market and regulatory dynamics, offers forward-looking insights, and is formatted for direct use in plans, decks, or reports.

Provides a clean, summarized PESTLE of Ball, visually segmented by category for quick interpretation and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Aluminum price volatility

LME aluminium price volatility (≈$2,400/ton mid‑2025) plus Midwest premiums (~$150/ton) and European premiums (~€250/ton) drive Ball's COGS and contract pass‑through timing. Hedging programs smooth earnings volatility but do not alter volume elasticity tied to end‑market demand. Scrap spreads (~$300/ton) improve the economics of higher recycled content, reducing marginal COGS when scrap is available.

Beverage demand cycles

Macro conditions and category mix drove can volumes across beer, soft drinks, energy and seltzers in 2024, with premium seltzer and energy up while mainstream beer was flat; overall aluminum can demand rose modestly. Retail channel shifts and private label penetration (about 15–20% in several markets) changed SKU mix and utilization. Emerging markets grew roughly 5–7% in 2024, offsetting mature market stagnation near 0–1%.

FX and interest rates

Multi-currency revenues and costs expose Ball to translation and transaction risk given its significant international footprint, affecting reported results when USD moves against EUR, CAD and BRL. Elevated policy rates (US federal funds 5.25–5.50% in 2024; ECB deposit rate 4.00% in 2024) influence Ball’s capex, refinancing costs and customer investment timing. Balanced regional funding reduces currency and maturity mismatches and supports liquidity resilience.

Energy and logistics costs

Rising power and gas costs drive smelter and can-plant margins—US industrial electricity averaged about $0.094/kWh in 2024 and Henry Hub gas averaged ~$3.64/MMBtu, raising aluminum input costs that can be 30–40% of smelter cost; freight volatility and port congestion (BDI ~1,200 average in 2024; Shanghai–LA container rates ~ $1,500/TEU in 2024) lengthen lead times and inflate inventory; network optimization and modal shifts protect margins.

- Energy: US industrial power $0.094/kWh (2024)

- Gas: Henry Hub ~$3.64/MMBtu (2024)

- Freight: BDI ~1,200 (2024), Shanghai–LA ~$1,500/TEU (2024)

- Impact: aluminum energy share 30–40% of smelter costs

Labor availability and wages

Tight labor markets pushed US manufacturing average hourly earnings up ~4.5% year‑over‑year in 2024 (BLS), raising wages and training costs in Ball’s production hubs; automation investments have offset some labor pressure by stabilizing throughput and improving quality metrics. Union dynamics and retention influence uptime, with negotiated work rules and turnover directly affecting utilization and OEE.

- Wage growth: ~4.5% (US manufacturing, 2024)

- Automation: reduces variability, raises capex but lowers labor per unit

- Union/retention: impacts uptime and maintenance scheduling

China ~55% and Guinea ~25% reshape aluminium geopolitics

LME aluminium ~ $2,400/ton (mid‑2025) plus Midwest premium ~$150/ton and EU premium ~€250/ton drive Ball’s COGS and pass‑through timing; scrap spreads ~ $300/ton lower marginal costs when available. Energy/gas (US power $0.094/kWh; Henry Hub ~$3.64/MMBtu in 2024), freight (BDI ~1,200; SH‑LA ~$1,500/TEU) and wage growth ~4.5% (US, 2024) compress margins; hedging and automation mitigate volatility.

| Metric | Value |

|---|---|

| LME | $2,400/ton |

| Midwest premium | $150/ton |

| EU premium | €250/ton |

| Scrap spread | $300/ton |

| US power | $0.094/kWh (2024) |

| Henry Hub | $3.64/MMBtu (2024) |

| BDI | ~1,200 (2024) |

| SH‑LA | $1,500/TEU (2024) |

| Wage growth | ~4.5% (US manufacturing, 2024) |

Preview the Actual Deliverable

Ball PESTLE Analysis

The Ball PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the final version with no placeholders or teasers, delivered exactly as displayed. The layout, content, and structure are identical to the downloadable file you’ll get immediately after checkout. What you see is the real, finished product.