Bâloise Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

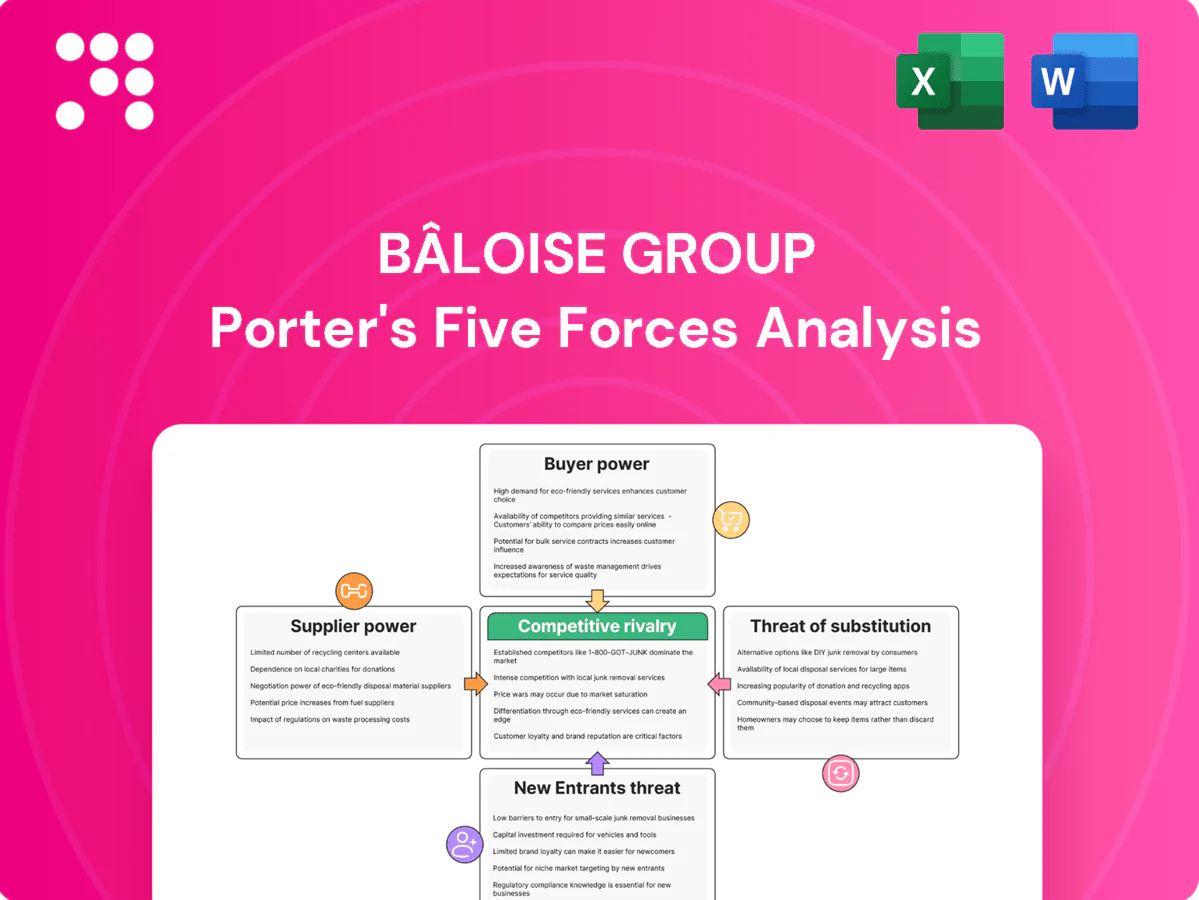

Bâloise Group faces moderate supplier and buyer power, rising substitution risks from insurtechs, and high regulatory barriers that limit new entrants, shaping a competitive yet stable market landscape. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Get the complete report for actionable insights tailored to Bâloise.

Suppliers Bargaining Power

Reinsurers and Retrocession Capacity

Reinsurers supply essential risk capacity and pricing, directly affecting Bâloise’s cost of capital for peak property, casualty and life exposures; 2024 saw reinsurance rate increases of roughly 15% in many commercial lines. Concentration among the top five reinsurers, which supply about half of global treaty capacity, heightens their bargaining power in hard markets. Long-term, multi-year treaties smooth volatility but reduce Bâloise’s ability to switch quickly. Bâloise’s diversified footprint across markets strengthens negotiation by balancing ceded volumes.

IT Platforms and Core Systems Vendors

In 2024 the market for core policy administration, claims and analytics is concentrated around three dominant vendors — Guidewire, Duck Creek and Sapiens — creating high switching costs and integration lock‑in. Vendor roadmaps materially affect Bâloise’s digital velocity and unit costs, so multi‑vendor strategies and selective in‑house development are used to reduce dependency. Cloud hyperscalers (AWS, Azure, GCP) held over 60% of global cloud market in 2024, shaping pricing and resilience requirements.

Data, Telematics, and Credit Bureaus

Bâloise underwriting depends on proprietary data sources, giving suppliers of unique or regulated data leverage, especially under GDPR (2018) constraints and the 2024 EU AI Act provisional rules that limit certain profiling uses. Telematics and IoT partners materially influence motor and property product design and loss-ratio dynamics. PSD2-enabled open finance and alternative data increasingly reduce supplier concentration risk.

Brokerage Networks and Affinity Partners

Independent brokers and bancassurance partners in CH/DE/BE/LU control customer access and extract commissions and service fees, giving them leverage over distribution; high-performing partners gain further bargaining power through superior conversion rates and cross-sell metrics. Exclusive and direct channels reduce dependency by securing captive flows and margin retention, while performance-linked remuneration and co-branded propositions align incentives between Bâloise and partners.

- Broker-driven distribution: commission & service fee leverage

- Top-performers: higher conversion = greater negotiation power

- Exclusive/direct channels: lower dependency, higher margins

- Performance-linked pay & co-branding: aligned incentives

Repair, Medical, and Assistance Networks

Repair shops, healthcare providers and roadside/home assistance firms materially drive claims costs and customer experience for Bâloise; supplier-driven parts, labour and specialist treatment pricing can swing motor and health claims by double-digit percentages in 2024. Regional concentration or niche specialists raise supplier bargaining power, while preferred networks and volume agreements secure better rates. Digital claims orchestration in 2024 is cutting leakage by up to 20% and improving transparency, strengthening insurer negotiating positions.

- Supplier impact on claims costs: double-digit % swings (2024)

- Concentration increases supplier power

- Preferred networks and volume deals improve terms

- Digital orchestration reduces leakage up to 20% (2024)

15% reinsurance hikes, concentrated capacity and supplier power raise insurer risks

Reinsurers raised commercial reinsurance rates ~15% in 2024; top‑5 reinsurers provide ~50% of treaty capacity, boosting their leverage. Core policy vendors (Guidewire/Duck Creek/Sapiens) and cloud hyperscalers (>60% market share in 2024) create high switching costs. Repair/health suppliers can swing claims by double‑digit %; brokers retain commission leverage across CH/DE/BE/LU.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +15% rates; top5≈50% cap | Higher cost of capital |

| Core vendors | 3 dominant players | Switching costs |

| Cloud | >60% market | Pricing power |

| Repair/health | Double‑digit % claims swing | Claims volatility |

| Brokers | High commission mix | Distribution leverage |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bâloise Group, with detailed evaluation of supplier and buyer power and industry-specific barriers. Identifies disruptive forces, emerging substitutes, and strategic levers that affect Bâloise Group’s pricing, profitability, and defensive positioning.

Clear, one-sheet Porter's Five Forces for Bâloise Group—instantly reveal competitive, supplier, buyer, entrant and substitute pressures so executives can pinpoint and relieve strategic pain points for faster, confident decisions.

Customers Bargaining Power

Price-Sensitive Retail Customers

Consumers increasingly compare premiums and coverage across aggregators and direct channels, intensifying price pressure on Bâloise; the group reported CHF 8.3 billion gross written premiums in 2024, amplifying sensitivity in commoditised lines. Switching is far easier in motor and simple property than in life or pensions, where portability and underwriting raise barriers. Loyalty programs and bundled policies materially reduce churn, while transparent claims handling and a strong NPS often outweigh small price differences.

SME and Corporate Clients

Larger SME and corporate buyers increasingly leverage bespoke coverage and multi-line discounts, pushing for tailored terms and pricing pressure. Risk engineering and captive solutions can move placement terms in favor of clients, while multi-year agreements and SLAs—more common since 2024—reduce tender frequency. Bâloise’s advisory depth lets it justify premium differentials through loss prevention and compliance support.

Intermediated Buyers via Brokers

Intermediated buyers via brokers consolidate demand and force competitive quotes, increasing buyer power as Bâloise faces panel placements that enforce pricing discipline and require clear service differentiation. Strong broker relationships lift placement rates and cross-sell, a key channel given Bâloise’s CHF 8.6bn premium book (2023). Fast data-sharing and sub-48-hour underwriting turnarounds win broker preference and market share.

Switching Costs and Product Complexity

Life, pension and health products create higher switching frictions for Bâloise customers because tax treatment, contractual guarantees and underwriting create long-term ties, while P&C products with short, often annual, terms reduce lock-in; digital self-service and straight-through processing can both lower friction for switching and simultaneously improve retention, and cross-selling banking and investment services increases customer embeddedness.

- High-friction lines: life, pension, health

- Low-friction: P&C annual terms

- Digital STP: eases switching but boosts retention

- Cross-selling: raises embeddedness

Regulatory and Consumer Protection Effects

Transparent disclosures and conduct rules let customers compare products and lodge complaints, constraining pricing freedom for insurers and limiting cross-sell opacity; regulatory caps on fees or mandated coverages further reduce Bâloise Group’s pricing latitude while its strong brand trust and compliance record soften adversarial customer interactions.

- Transparent disclosures empower comparison and complaints

- Fee caps and mandated covers limit pricing

- Brand trust and compliance mitigate adversarial dynamics

- Ombudsman outcomes shape perceived value

Customer bargaining power fuels P&C price pressure while life/pension retains switching friction

Customers exert moderate–high bargaining power: price sensitivity rises in commoditised P&C (Bâloise GWP CHF 8.3bn in 2024) while life/pension lines have high switching friction; brokers and SMEs demand tailored terms, driving competitive quoting; transparency, regulation and brand trust limit unilateral price increases.

| Metric | Value | Note |

|---|---|---|

| GWP 2024 | CHF 8.3bn | P&C price pressure |

| Broker influence | High | Consolidated panels |

Preview Before You Purchase

Bâloise Group Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The analysis applies Porter’s Five Forces to Bâloise Group, assessing competitive rivalry, buyer and supplier power, threat of new entrants, and substitute products. It highlights strategic implications and actionable recommendations for insurers and investors to inform risk and opportunity decisions.

Don't Miss the Bigger Picture

Bâloise Group faces moderate supplier and buyer power, rising substitution risks from insurtechs, and high regulatory barriers that limit new entrants, shaping a competitive yet stable market landscape. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Get the complete report for actionable insights tailored to Bâloise.

Suppliers Bargaining Power

Reinsurers and Retrocession Capacity

Reinsurers supply essential risk capacity and pricing, directly affecting Bâloise’s cost of capital for peak property, casualty and life exposures; 2024 saw reinsurance rate increases of roughly 15% in many commercial lines. Concentration among the top five reinsurers, which supply about half of global treaty capacity, heightens their bargaining power in hard markets. Long-term, multi-year treaties smooth volatility but reduce Bâloise’s ability to switch quickly. Bâloise’s diversified footprint across markets strengthens negotiation by balancing ceded volumes.

IT Platforms and Core Systems Vendors

In 2024 the market for core policy administration, claims and analytics is concentrated around three dominant vendors — Guidewire, Duck Creek and Sapiens — creating high switching costs and integration lock‑in. Vendor roadmaps materially affect Bâloise’s digital velocity and unit costs, so multi‑vendor strategies and selective in‑house development are used to reduce dependency. Cloud hyperscalers (AWS, Azure, GCP) held over 60% of global cloud market in 2024, shaping pricing and resilience requirements.

Data, Telematics, and Credit Bureaus

Bâloise underwriting depends on proprietary data sources, giving suppliers of unique or regulated data leverage, especially under GDPR (2018) constraints and the 2024 EU AI Act provisional rules that limit certain profiling uses. Telematics and IoT partners materially influence motor and property product design and loss-ratio dynamics. PSD2-enabled open finance and alternative data increasingly reduce supplier concentration risk.

Brokerage Networks and Affinity Partners

Independent brokers and bancassurance partners in CH/DE/BE/LU control customer access and extract commissions and service fees, giving them leverage over distribution; high-performing partners gain further bargaining power through superior conversion rates and cross-sell metrics. Exclusive and direct channels reduce dependency by securing captive flows and margin retention, while performance-linked remuneration and co-branded propositions align incentives between Bâloise and partners.

- Broker-driven distribution: commission & service fee leverage

- Top-performers: higher conversion = greater negotiation power

- Exclusive/direct channels: lower dependency, higher margins

- Performance-linked pay & co-branding: aligned incentives

Repair, Medical, and Assistance Networks

Repair shops, healthcare providers and roadside/home assistance firms materially drive claims costs and customer experience for Bâloise; supplier-driven parts, labour and specialist treatment pricing can swing motor and health claims by double-digit percentages in 2024. Regional concentration or niche specialists raise supplier bargaining power, while preferred networks and volume agreements secure better rates. Digital claims orchestration in 2024 is cutting leakage by up to 20% and improving transparency, strengthening insurer negotiating positions.

- Supplier impact on claims costs: double-digit % swings (2024)

- Concentration increases supplier power

- Preferred networks and volume deals improve terms

- Digital orchestration reduces leakage up to 20% (2024)

15% reinsurance hikes, concentrated capacity and supplier power raise insurer risks

Reinsurers raised commercial reinsurance rates ~15% in 2024; top‑5 reinsurers provide ~50% of treaty capacity, boosting their leverage. Core policy vendors (Guidewire/Duck Creek/Sapiens) and cloud hyperscalers (>60% market share in 2024) create high switching costs. Repair/health suppliers can swing claims by double‑digit %; brokers retain commission leverage across CH/DE/BE/LU.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +15% rates; top5≈50% cap | Higher cost of capital |

| Core vendors | 3 dominant players | Switching costs |

| Cloud | >60% market | Pricing power |

| Repair/health | Double‑digit % claims swing | Claims volatility |

| Brokers | High commission mix | Distribution leverage |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bâloise Group, with detailed evaluation of supplier and buyer power and industry-specific barriers. Identifies disruptive forces, emerging substitutes, and strategic levers that affect Bâloise Group’s pricing, profitability, and defensive positioning.

Clear, one-sheet Porter's Five Forces for Bâloise Group—instantly reveal competitive, supplier, buyer, entrant and substitute pressures so executives can pinpoint and relieve strategic pain points for faster, confident decisions.

Customers Bargaining Power

Price-Sensitive Retail Customers

Consumers increasingly compare premiums and coverage across aggregators and direct channels, intensifying price pressure on Bâloise; the group reported CHF 8.3 billion gross written premiums in 2024, amplifying sensitivity in commoditised lines. Switching is far easier in motor and simple property than in life or pensions, where portability and underwriting raise barriers. Loyalty programs and bundled policies materially reduce churn, while transparent claims handling and a strong NPS often outweigh small price differences.

SME and Corporate Clients

Larger SME and corporate buyers increasingly leverage bespoke coverage and multi-line discounts, pushing for tailored terms and pricing pressure. Risk engineering and captive solutions can move placement terms in favor of clients, while multi-year agreements and SLAs—more common since 2024—reduce tender frequency. Bâloise’s advisory depth lets it justify premium differentials through loss prevention and compliance support.

Intermediated Buyers via Brokers

Intermediated buyers via brokers consolidate demand and force competitive quotes, increasing buyer power as Bâloise faces panel placements that enforce pricing discipline and require clear service differentiation. Strong broker relationships lift placement rates and cross-sell, a key channel given Bâloise’s CHF 8.6bn premium book (2023). Fast data-sharing and sub-48-hour underwriting turnarounds win broker preference and market share.

Switching Costs and Product Complexity

Life, pension and health products create higher switching frictions for Bâloise customers because tax treatment, contractual guarantees and underwriting create long-term ties, while P&C products with short, often annual, terms reduce lock-in; digital self-service and straight-through processing can both lower friction for switching and simultaneously improve retention, and cross-selling banking and investment services increases customer embeddedness.

- High-friction lines: life, pension, health

- Low-friction: P&C annual terms

- Digital STP: eases switching but boosts retention

- Cross-selling: raises embeddedness

Regulatory and Consumer Protection Effects

Transparent disclosures and conduct rules let customers compare products and lodge complaints, constraining pricing freedom for insurers and limiting cross-sell opacity; regulatory caps on fees or mandated coverages further reduce Bâloise Group’s pricing latitude while its strong brand trust and compliance record soften adversarial customer interactions.

- Transparent disclosures empower comparison and complaints

- Fee caps and mandated covers limit pricing

- Brand trust and compliance mitigate adversarial dynamics

- Ombudsman outcomes shape perceived value

Customer bargaining power fuels P&C price pressure while life/pension retains switching friction

Customers exert moderate–high bargaining power: price sensitivity rises in commoditised P&C (Bâloise GWP CHF 8.3bn in 2024) while life/pension lines have high switching friction; brokers and SMEs demand tailored terms, driving competitive quoting; transparency, regulation and brand trust limit unilateral price increases.

| Metric | Value | Note |

|---|---|---|

| GWP 2024 | CHF 8.3bn | P&C price pressure |

| Broker influence | High | Consolidated panels |

Preview Before You Purchase

Bâloise Group Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The analysis applies Porter’s Five Forces to Bâloise Group, assessing competitive rivalry, buyer and supplier power, threat of new entrants, and substitute products. It highlights strategic implications and actionable recommendations for insurers and investors to inform risk and opportunity decisions.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Bâloise Group faces moderate supplier and buyer power, rising substitution risks from insurtechs, and high regulatory barriers that limit new entrants, shaping a competitive yet stable market landscape. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Get the complete report for actionable insights tailored to Bâloise.

Suppliers Bargaining Power

Reinsurers and Retrocession Capacity

Reinsurers supply essential risk capacity and pricing, directly affecting Bâloise’s cost of capital for peak property, casualty and life exposures; 2024 saw reinsurance rate increases of roughly 15% in many commercial lines. Concentration among the top five reinsurers, which supply about half of global treaty capacity, heightens their bargaining power in hard markets. Long-term, multi-year treaties smooth volatility but reduce Bâloise’s ability to switch quickly. Bâloise’s diversified footprint across markets strengthens negotiation by balancing ceded volumes.

IT Platforms and Core Systems Vendors

In 2024 the market for core policy administration, claims and analytics is concentrated around three dominant vendors — Guidewire, Duck Creek and Sapiens — creating high switching costs and integration lock‑in. Vendor roadmaps materially affect Bâloise’s digital velocity and unit costs, so multi‑vendor strategies and selective in‑house development are used to reduce dependency. Cloud hyperscalers (AWS, Azure, GCP) held over 60% of global cloud market in 2024, shaping pricing and resilience requirements.

Data, Telematics, and Credit Bureaus

Bâloise underwriting depends on proprietary data sources, giving suppliers of unique or regulated data leverage, especially under GDPR (2018) constraints and the 2024 EU AI Act provisional rules that limit certain profiling uses. Telematics and IoT partners materially influence motor and property product design and loss-ratio dynamics. PSD2-enabled open finance and alternative data increasingly reduce supplier concentration risk.

Brokerage Networks and Affinity Partners

Independent brokers and bancassurance partners in CH/DE/BE/LU control customer access and extract commissions and service fees, giving them leverage over distribution; high-performing partners gain further bargaining power through superior conversion rates and cross-sell metrics. Exclusive and direct channels reduce dependency by securing captive flows and margin retention, while performance-linked remuneration and co-branded propositions align incentives between Bâloise and partners.

- Broker-driven distribution: commission & service fee leverage

- Top-performers: higher conversion = greater negotiation power

- Exclusive/direct channels: lower dependency, higher margins

- Performance-linked pay & co-branding: aligned incentives

Repair, Medical, and Assistance Networks

Repair shops, healthcare providers and roadside/home assistance firms materially drive claims costs and customer experience for Bâloise; supplier-driven parts, labour and specialist treatment pricing can swing motor and health claims by double-digit percentages in 2024. Regional concentration or niche specialists raise supplier bargaining power, while preferred networks and volume agreements secure better rates. Digital claims orchestration in 2024 is cutting leakage by up to 20% and improving transparency, strengthening insurer negotiating positions.

- Supplier impact on claims costs: double-digit % swings (2024)

- Concentration increases supplier power

- Preferred networks and volume deals improve terms

- Digital orchestration reduces leakage up to 20% (2024)

15% reinsurance hikes, concentrated capacity and supplier power raise insurer risks

Reinsurers raised commercial reinsurance rates ~15% in 2024; top‑5 reinsurers provide ~50% of treaty capacity, boosting their leverage. Core policy vendors (Guidewire/Duck Creek/Sapiens) and cloud hyperscalers (>60% market share in 2024) create high switching costs. Repair/health suppliers can swing claims by double‑digit %; brokers retain commission leverage across CH/DE/BE/LU.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reinsurers | +15% rates; top5≈50% cap | Higher cost of capital |

| Core vendors | 3 dominant players | Switching costs |

| Cloud | >60% market | Pricing power |

| Repair/health | Double‑digit % claims swing | Claims volatility |

| Brokers | High commission mix | Distribution leverage |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Bâloise Group, with detailed evaluation of supplier and buyer power and industry-specific barriers. Identifies disruptive forces, emerging substitutes, and strategic levers that affect Bâloise Group’s pricing, profitability, and defensive positioning.

Clear, one-sheet Porter's Five Forces for Bâloise Group—instantly reveal competitive, supplier, buyer, entrant and substitute pressures so executives can pinpoint and relieve strategic pain points for faster, confident decisions.

Customers Bargaining Power

Price-Sensitive Retail Customers

Consumers increasingly compare premiums and coverage across aggregators and direct channels, intensifying price pressure on Bâloise; the group reported CHF 8.3 billion gross written premiums in 2024, amplifying sensitivity in commoditised lines. Switching is far easier in motor and simple property than in life or pensions, where portability and underwriting raise barriers. Loyalty programs and bundled policies materially reduce churn, while transparent claims handling and a strong NPS often outweigh small price differences.

SME and Corporate Clients

Larger SME and corporate buyers increasingly leverage bespoke coverage and multi-line discounts, pushing for tailored terms and pricing pressure. Risk engineering and captive solutions can move placement terms in favor of clients, while multi-year agreements and SLAs—more common since 2024—reduce tender frequency. Bâloise’s advisory depth lets it justify premium differentials through loss prevention and compliance support.

Intermediated Buyers via Brokers

Intermediated buyers via brokers consolidate demand and force competitive quotes, increasing buyer power as Bâloise faces panel placements that enforce pricing discipline and require clear service differentiation. Strong broker relationships lift placement rates and cross-sell, a key channel given Bâloise’s CHF 8.6bn premium book (2023). Fast data-sharing and sub-48-hour underwriting turnarounds win broker preference and market share.

Switching Costs and Product Complexity

Life, pension and health products create higher switching frictions for Bâloise customers because tax treatment, contractual guarantees and underwriting create long-term ties, while P&C products with short, often annual, terms reduce lock-in; digital self-service and straight-through processing can both lower friction for switching and simultaneously improve retention, and cross-selling banking and investment services increases customer embeddedness.

- High-friction lines: life, pension, health

- Low-friction: P&C annual terms

- Digital STP: eases switching but boosts retention

- Cross-selling: raises embeddedness

Regulatory and Consumer Protection Effects

Transparent disclosures and conduct rules let customers compare products and lodge complaints, constraining pricing freedom for insurers and limiting cross-sell opacity; regulatory caps on fees or mandated coverages further reduce Bâloise Group’s pricing latitude while its strong brand trust and compliance record soften adversarial customer interactions.

- Transparent disclosures empower comparison and complaints

- Fee caps and mandated covers limit pricing

- Brand trust and compliance mitigate adversarial dynamics

- Ombudsman outcomes shape perceived value

Customer bargaining power fuels P&C price pressure while life/pension retains switching friction

Customers exert moderate–high bargaining power: price sensitivity rises in commoditised P&C (Bâloise GWP CHF 8.3bn in 2024) while life/pension lines have high switching friction; brokers and SMEs demand tailored terms, driving competitive quoting; transparency, regulation and brand trust limit unilateral price increases.

| Metric | Value | Note |

|---|---|---|

| GWP 2024 | CHF 8.3bn | P&C price pressure |

| Broker influence | High | Consolidated panels |

Preview Before You Purchase

Bâloise Group Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The analysis applies Porter’s Five Forces to Bâloise Group, assessing competitive rivalry, buyer and supplier power, threat of new entrants, and substitute products. It highlights strategic implications and actionable recommendations for insurers and investors to inform risk and opportunity decisions.