Koninklijke Bam Groep Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

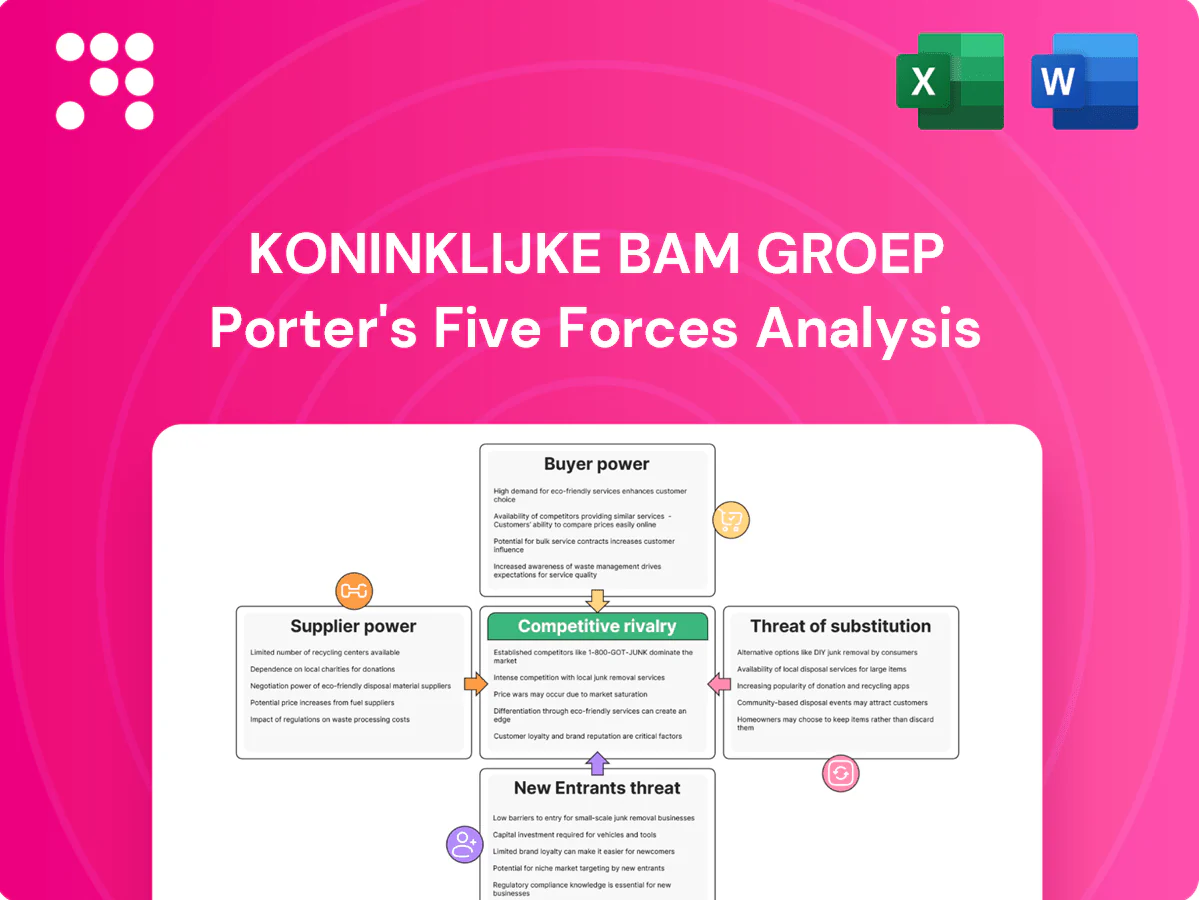

Koninklijke BAM Groep faces moderate supplier power, high buyer scrutiny, and intense rivalry driven by public tendering and margin pressure; substitutes and entrant threats vary by region and project type. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Koninklijke Bam Groep’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration in key materials

Steel, cement, asphalt and aggregates in Europe are supplied by a relatively concentrated set of large producers, which raises switching costs and gives suppliers leverage over price and delivery. Long-term framework contracts used by BAM partially mitigate short-term price spikes and supply interruptions. BAM’s scale strengthens negotiating power but does not fully insulate it from volatile commodity cycles. Suppliers can thus exert meaningful bargaining pressure.

Specialist subcontractor dependency

MEP, tunneling, piling and façade works for Koninklijke BAM depend on niche subcontractors whose specialist pools are limited; industry studies in 2024 show specialist subcontracting can represent roughly 50–70% of on-site scope, concentrating bargaining power. Peak-cycle capacity tightness raised bid premiums by about 10–20% in 2024, while stringent prequalification often shrinks eligible vendors by over 50%. BAM mitigates pressure through partnering models and multi-year pipeline visibility, trading margin for delivery reliability.

Equipment and technology lock-in

Equipment and technology lock-in is significant for Koninklijke BAM Groep as heavy plant lessors and dominant BIM/DFMA providers such as Autodesk, Bentley and Trimble create operational dependency. License ecosystems and limited data portability constrain switching, while UK public-project BIM mandates keep adoption above 90% in 2024, reinforcing vendor leverage. Multi-vendor leasing and standardized processes across NL, UK, IE and DE reduce single-supplier exposure and improve negotiating power.

Labor availability and unions

Skilled labor shortages across Western Europe in 2024 increased wage pressure for Koninklijke BAM Groep, with BAM reporting a workforce of about 13,000 in 2024 and higher hourly labor costs compressing margins. Strong union agreements and strict regulatory standards reduce scheduling and pay flexibility, raising supplier bargaining power. Temporary labor agencies gained leverage during peaks, though BAM’s apprenticeship and workforce development programs aim to lower dependence over time.

- 2024 workforce: c.13,000

- Union/regulatory constraints: limit flexibility

- Temp agencies: higher bargaining power in peaks

- Apprenticeships: medium-term mitigation

Logistics and energy volatility

Logistics, transport and fuel cost inflation feed directly into supplier pricing for Koninklijke BAM, with EU diesel averaging around €1.60/L and industrial electricity near €0.20/kWh in 2024, raising bid prices and margins pressure. EU supply‑chain disruptions since 2021 have delayed projects and increased claims; indexed contracts mitigate some volatility, while early procurement and local sourcing lower risk premiums.

- Fuel pass‑through: higher supplier bids

- Indexed contracts: partial hedge

- Early procurement: lowers premiums

- Local sourcing: reduces delay risk

Suppliers squeeze margins: concentrated materials, niche subs, energy costs raise delivery risk

Suppliers exert meaningful pressure: concentrated materials market, niche subcontractor limits, equipment/license lock‑in, labor shortages and fuel/electricity cost inflation raise costs and delivery risk; BAM’s scale, contracts and apprenticeships only partially mitigate.

| Metric | 2024 |

|---|---|

| Materials concentration (top 5) | ~60% market share |

| Specialist subcontract share | 50–70% |

| BIM adoption (UK) | >90% |

| Workforce | c.13,000 |

| EU diesel avg | €1.60/L |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Koninklijke Bam Groep, revealing competitive intensity, buyer and supplier power, entry barriers, and substitution risks that influence its margins and strategic positioning. Identifies disruptive threats, regulatory pressures, and defensive advantages to inform investor materials, strategy decks, and corporate planning.

Compact Porter's Five Forces for Koninklijke BAM: a one-sheet, customizable assessment that visualizes supplier/buyer power, rivalry, substitutes and entry threats with an instant spider chart—no macros, easy to edit and drop straight into pitch decks or reports to remove decision-making friction.

Customers Bargaining Power

Public sector dominance

Governments and agencies in NL, UK, IE and DE are core clients, aligning with EU public procurement worth about 14% of GDP (roughly €2 trillion annually), giving buyers strong leverage. Competitive tendering and framework lots systematically compress margins, forcing fixed-price bids and tight cost controls. Rigorous performance metrics, liquidated damages and KPIs further strengthen buyer power. BAM’s track record secures wins but rarely permits premium pricing.

Project size and bundling

Large bundled infrastructure and hospital/school programs give buyers leverage to dictate contract terms and enforce volume-for-discount dynamics that compress BAMs unit margins. Buyers increasingly insist on transferring time, cost and ESG risks to contractors, raising demand for fixed-price, performance-linked contracts. BAM can trade lower prices for multi-year pipeline visibility to stabilize utilization and protect margins.

Design-and-build risk allocation

Clients increasingly prefer D&B and PPP models that shift design and lifecycle risks to contractors, raising warranty and financing burdens and thus strengthening buyer bargaining power; BAM reported a 2024 order book of about €5.5bn, amplifying exposure to these contract types. BAM’s integrated design and FM capabilities partly offset this pressure by internalizing lifecycle expertise and reducing subcontracting risk. Rigorous bid/no-bid discipline is essential to protect margins and balance risk-return.

Information symmetry in tenders

Transparent tender portals and public benchmarks compress information asymmetry, strengthening buyer negotiation power; Koninklijke BAM Groep reported revenue around €6.1bn in 2023, illustrating scale in competitive public tenders. Cost models across bidders are often comparable, so differentiation shifts to delivery certainty and innovation, while early contractor involvement can rebalance gaps and reduce change orders.

- Transparent portals: raise buyer leverage

- Comparable cost models: lowers price variance

- Diff: delivery certainty & innovation

- ECI: rebalances info, reduces overruns

Sustainability and compliance demands

Clients now mandate low-carbon materials, circularity, and safety excellence, pressuring suppliers as EU carbon prices rose to about €100/ton in mid-2024, lifting input costs while buyers resist price increases. Certifications (BREEAM, LEED, ISO) are table stakes, not premium drivers, so BAM can only monetize sustainability when linked to measurable lifecycle savings and verified operational OPEX reductions.

- Clients mandate: low-carbon, circularity, safety

- 2024 EU carbon price: ~€100/ton

- Certifications = table stakes; monetize via lifecycle savings

Public buyers €2tn and order book €5.5bn squeeze margins

Public clients and EU procurement (~€2tn, 14% GDP) create strong buyer leverage; competitive tenders compress margins. BAM order book €5.5bn (2024) vs €6.1bn revenue (2023) limits premium pricing. EU carbon price ~€100/t (mid‑2024) makes certifications table stakes—value only via verified lifecycle OPEX savings.

| Item | 2024 | Effect |

|---|---|---|

| Public procurement | ~€2tn | High buyer power |

| Order book | €5.5bn | Fixed‑price exposure |

| EU carbon price | ~€100/t | ↑ input costs |

Full Version Awaits

Koninklijke Bam Groep Porter's Five Forces Analysis

This preview shows the exact Koninklijke Bam Groep Porter’s Five Forces analysis you’ll receive—fully formatted, comprehensive and ready to download upon purchase. No samples or placeholders; the file here is the final deliverable. Use it immediately for strategic or investment decisions.

Go Beyond the Preview—Access the Full Strategic Report

Koninklijke BAM Groep faces moderate supplier power, high buyer scrutiny, and intense rivalry driven by public tendering and margin pressure; substitutes and entrant threats vary by region and project type. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Koninklijke Bam Groep’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration in key materials

Steel, cement, asphalt and aggregates in Europe are supplied by a relatively concentrated set of large producers, which raises switching costs and gives suppliers leverage over price and delivery. Long-term framework contracts used by BAM partially mitigate short-term price spikes and supply interruptions. BAM’s scale strengthens negotiating power but does not fully insulate it from volatile commodity cycles. Suppliers can thus exert meaningful bargaining pressure.

Specialist subcontractor dependency

MEP, tunneling, piling and façade works for Koninklijke BAM depend on niche subcontractors whose specialist pools are limited; industry studies in 2024 show specialist subcontracting can represent roughly 50–70% of on-site scope, concentrating bargaining power. Peak-cycle capacity tightness raised bid premiums by about 10–20% in 2024, while stringent prequalification often shrinks eligible vendors by over 50%. BAM mitigates pressure through partnering models and multi-year pipeline visibility, trading margin for delivery reliability.

Equipment and technology lock-in

Equipment and technology lock-in is significant for Koninklijke BAM Groep as heavy plant lessors and dominant BIM/DFMA providers such as Autodesk, Bentley and Trimble create operational dependency. License ecosystems and limited data portability constrain switching, while UK public-project BIM mandates keep adoption above 90% in 2024, reinforcing vendor leverage. Multi-vendor leasing and standardized processes across NL, UK, IE and DE reduce single-supplier exposure and improve negotiating power.

Labor availability and unions

Skilled labor shortages across Western Europe in 2024 increased wage pressure for Koninklijke BAM Groep, with BAM reporting a workforce of about 13,000 in 2024 and higher hourly labor costs compressing margins. Strong union agreements and strict regulatory standards reduce scheduling and pay flexibility, raising supplier bargaining power. Temporary labor agencies gained leverage during peaks, though BAM’s apprenticeship and workforce development programs aim to lower dependence over time.

- 2024 workforce: c.13,000

- Union/regulatory constraints: limit flexibility

- Temp agencies: higher bargaining power in peaks

- Apprenticeships: medium-term mitigation

Logistics and energy volatility

Logistics, transport and fuel cost inflation feed directly into supplier pricing for Koninklijke BAM, with EU diesel averaging around €1.60/L and industrial electricity near €0.20/kWh in 2024, raising bid prices and margins pressure. EU supply‑chain disruptions since 2021 have delayed projects and increased claims; indexed contracts mitigate some volatility, while early procurement and local sourcing lower risk premiums.

- Fuel pass‑through: higher supplier bids

- Indexed contracts: partial hedge

- Early procurement: lowers premiums

- Local sourcing: reduces delay risk

Suppliers squeeze margins: concentrated materials, niche subs, energy costs raise delivery risk

Suppliers exert meaningful pressure: concentrated materials market, niche subcontractor limits, equipment/license lock‑in, labor shortages and fuel/electricity cost inflation raise costs and delivery risk; BAM’s scale, contracts and apprenticeships only partially mitigate.

| Metric | 2024 |

|---|---|

| Materials concentration (top 5) | ~60% market share |

| Specialist subcontract share | 50–70% |

| BIM adoption (UK) | >90% |

| Workforce | c.13,000 |

| EU diesel avg | €1.60/L |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Koninklijke Bam Groep, revealing competitive intensity, buyer and supplier power, entry barriers, and substitution risks that influence its margins and strategic positioning. Identifies disruptive threats, regulatory pressures, and defensive advantages to inform investor materials, strategy decks, and corporate planning.

Compact Porter's Five Forces for Koninklijke BAM: a one-sheet, customizable assessment that visualizes supplier/buyer power, rivalry, substitutes and entry threats with an instant spider chart—no macros, easy to edit and drop straight into pitch decks or reports to remove decision-making friction.

Customers Bargaining Power

Public sector dominance

Governments and agencies in NL, UK, IE and DE are core clients, aligning with EU public procurement worth about 14% of GDP (roughly €2 trillion annually), giving buyers strong leverage. Competitive tendering and framework lots systematically compress margins, forcing fixed-price bids and tight cost controls. Rigorous performance metrics, liquidated damages and KPIs further strengthen buyer power. BAM’s track record secures wins but rarely permits premium pricing.

Project size and bundling

Large bundled infrastructure and hospital/school programs give buyers leverage to dictate contract terms and enforce volume-for-discount dynamics that compress BAMs unit margins. Buyers increasingly insist on transferring time, cost and ESG risks to contractors, raising demand for fixed-price, performance-linked contracts. BAM can trade lower prices for multi-year pipeline visibility to stabilize utilization and protect margins.

Design-and-build risk allocation

Clients increasingly prefer D&B and PPP models that shift design and lifecycle risks to contractors, raising warranty and financing burdens and thus strengthening buyer bargaining power; BAM reported a 2024 order book of about €5.5bn, amplifying exposure to these contract types. BAM’s integrated design and FM capabilities partly offset this pressure by internalizing lifecycle expertise and reducing subcontracting risk. Rigorous bid/no-bid discipline is essential to protect margins and balance risk-return.

Information symmetry in tenders

Transparent tender portals and public benchmarks compress information asymmetry, strengthening buyer negotiation power; Koninklijke BAM Groep reported revenue around €6.1bn in 2023, illustrating scale in competitive public tenders. Cost models across bidders are often comparable, so differentiation shifts to delivery certainty and innovation, while early contractor involvement can rebalance gaps and reduce change orders.

- Transparent portals: raise buyer leverage

- Comparable cost models: lowers price variance

- Diff: delivery certainty & innovation

- ECI: rebalances info, reduces overruns

Sustainability and compliance demands

Clients now mandate low-carbon materials, circularity, and safety excellence, pressuring suppliers as EU carbon prices rose to about €100/ton in mid-2024, lifting input costs while buyers resist price increases. Certifications (BREEAM, LEED, ISO) are table stakes, not premium drivers, so BAM can only monetize sustainability when linked to measurable lifecycle savings and verified operational OPEX reductions.

- Clients mandate: low-carbon, circularity, safety

- 2024 EU carbon price: ~€100/ton

- Certifications = table stakes; monetize via lifecycle savings

Public buyers €2tn and order book €5.5bn squeeze margins

Public clients and EU procurement (~€2tn, 14% GDP) create strong buyer leverage; competitive tenders compress margins. BAM order book €5.5bn (2024) vs €6.1bn revenue (2023) limits premium pricing. EU carbon price ~€100/t (mid‑2024) makes certifications table stakes—value only via verified lifecycle OPEX savings.

| Item | 2024 | Effect |

|---|---|---|

| Public procurement | ~€2tn | High buyer power |

| Order book | €5.5bn | Fixed‑price exposure |

| EU carbon price | ~€100/t | ↑ input costs |

Full Version Awaits

Koninklijke Bam Groep Porter's Five Forces Analysis

This preview shows the exact Koninklijke Bam Groep Porter’s Five Forces analysis you’ll receive—fully formatted, comprehensive and ready to download upon purchase. No samples or placeholders; the file here is the final deliverable. Use it immediately for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Koninklijke BAM Groep faces moderate supplier power, high buyer scrutiny, and intense rivalry driven by public tendering and margin pressure; substitutes and entrant threats vary by region and project type. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Koninklijke Bam Groep’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration in key materials

Steel, cement, asphalt and aggregates in Europe are supplied by a relatively concentrated set of large producers, which raises switching costs and gives suppliers leverage over price and delivery. Long-term framework contracts used by BAM partially mitigate short-term price spikes and supply interruptions. BAM’s scale strengthens negotiating power but does not fully insulate it from volatile commodity cycles. Suppliers can thus exert meaningful bargaining pressure.

Specialist subcontractor dependency

MEP, tunneling, piling and façade works for Koninklijke BAM depend on niche subcontractors whose specialist pools are limited; industry studies in 2024 show specialist subcontracting can represent roughly 50–70% of on-site scope, concentrating bargaining power. Peak-cycle capacity tightness raised bid premiums by about 10–20% in 2024, while stringent prequalification often shrinks eligible vendors by over 50%. BAM mitigates pressure through partnering models and multi-year pipeline visibility, trading margin for delivery reliability.

Equipment and technology lock-in

Equipment and technology lock-in is significant for Koninklijke BAM Groep as heavy plant lessors and dominant BIM/DFMA providers such as Autodesk, Bentley and Trimble create operational dependency. License ecosystems and limited data portability constrain switching, while UK public-project BIM mandates keep adoption above 90% in 2024, reinforcing vendor leverage. Multi-vendor leasing and standardized processes across NL, UK, IE and DE reduce single-supplier exposure and improve negotiating power.

Labor availability and unions

Skilled labor shortages across Western Europe in 2024 increased wage pressure for Koninklijke BAM Groep, with BAM reporting a workforce of about 13,000 in 2024 and higher hourly labor costs compressing margins. Strong union agreements and strict regulatory standards reduce scheduling and pay flexibility, raising supplier bargaining power. Temporary labor agencies gained leverage during peaks, though BAM’s apprenticeship and workforce development programs aim to lower dependence over time.

- 2024 workforce: c.13,000

- Union/regulatory constraints: limit flexibility

- Temp agencies: higher bargaining power in peaks

- Apprenticeships: medium-term mitigation

Logistics and energy volatility

Logistics, transport and fuel cost inflation feed directly into supplier pricing for Koninklijke BAM, with EU diesel averaging around €1.60/L and industrial electricity near €0.20/kWh in 2024, raising bid prices and margins pressure. EU supply‑chain disruptions since 2021 have delayed projects and increased claims; indexed contracts mitigate some volatility, while early procurement and local sourcing lower risk premiums.

- Fuel pass‑through: higher supplier bids

- Indexed contracts: partial hedge

- Early procurement: lowers premiums

- Local sourcing: reduces delay risk

Suppliers squeeze margins: concentrated materials, niche subs, energy costs raise delivery risk

Suppliers exert meaningful pressure: concentrated materials market, niche subcontractor limits, equipment/license lock‑in, labor shortages and fuel/electricity cost inflation raise costs and delivery risk; BAM’s scale, contracts and apprenticeships only partially mitigate.

| Metric | 2024 |

|---|---|

| Materials concentration (top 5) | ~60% market share |

| Specialist subcontract share | 50–70% |

| BIM adoption (UK) | >90% |

| Workforce | c.13,000 |

| EU diesel avg | €1.60/L |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Koninklijke Bam Groep, revealing competitive intensity, buyer and supplier power, entry barriers, and substitution risks that influence its margins and strategic positioning. Identifies disruptive threats, regulatory pressures, and defensive advantages to inform investor materials, strategy decks, and corporate planning.

Compact Porter's Five Forces for Koninklijke BAM: a one-sheet, customizable assessment that visualizes supplier/buyer power, rivalry, substitutes and entry threats with an instant spider chart—no macros, easy to edit and drop straight into pitch decks or reports to remove decision-making friction.

Customers Bargaining Power

Public sector dominance

Governments and agencies in NL, UK, IE and DE are core clients, aligning with EU public procurement worth about 14% of GDP (roughly €2 trillion annually), giving buyers strong leverage. Competitive tendering and framework lots systematically compress margins, forcing fixed-price bids and tight cost controls. Rigorous performance metrics, liquidated damages and KPIs further strengthen buyer power. BAM’s track record secures wins but rarely permits premium pricing.

Project size and bundling

Large bundled infrastructure and hospital/school programs give buyers leverage to dictate contract terms and enforce volume-for-discount dynamics that compress BAMs unit margins. Buyers increasingly insist on transferring time, cost and ESG risks to contractors, raising demand for fixed-price, performance-linked contracts. BAM can trade lower prices for multi-year pipeline visibility to stabilize utilization and protect margins.

Design-and-build risk allocation

Clients increasingly prefer D&B and PPP models that shift design and lifecycle risks to contractors, raising warranty and financing burdens and thus strengthening buyer bargaining power; BAM reported a 2024 order book of about €5.5bn, amplifying exposure to these contract types. BAM’s integrated design and FM capabilities partly offset this pressure by internalizing lifecycle expertise and reducing subcontracting risk. Rigorous bid/no-bid discipline is essential to protect margins and balance risk-return.

Information symmetry in tenders

Transparent tender portals and public benchmarks compress information asymmetry, strengthening buyer negotiation power; Koninklijke BAM Groep reported revenue around €6.1bn in 2023, illustrating scale in competitive public tenders. Cost models across bidders are often comparable, so differentiation shifts to delivery certainty and innovation, while early contractor involvement can rebalance gaps and reduce change orders.

- Transparent portals: raise buyer leverage

- Comparable cost models: lowers price variance

- Diff: delivery certainty & innovation

- ECI: rebalances info, reduces overruns

Sustainability and compliance demands

Clients now mandate low-carbon materials, circularity, and safety excellence, pressuring suppliers as EU carbon prices rose to about €100/ton in mid-2024, lifting input costs while buyers resist price increases. Certifications (BREEAM, LEED, ISO) are table stakes, not premium drivers, so BAM can only monetize sustainability when linked to measurable lifecycle savings and verified operational OPEX reductions.

- Clients mandate: low-carbon, circularity, safety

- 2024 EU carbon price: ~€100/ton

- Certifications = table stakes; monetize via lifecycle savings

Public buyers €2tn and order book €5.5bn squeeze margins

Public clients and EU procurement (~€2tn, 14% GDP) create strong buyer leverage; competitive tenders compress margins. BAM order book €5.5bn (2024) vs €6.1bn revenue (2023) limits premium pricing. EU carbon price ~€100/t (mid‑2024) makes certifications table stakes—value only via verified lifecycle OPEX savings.

| Item | 2024 | Effect |

|---|---|---|

| Public procurement | ~€2tn | High buyer power |

| Order book | €5.5bn | Fixed‑price exposure |

| EU carbon price | ~€100/t | ↑ input costs |

Full Version Awaits

Koninklijke Bam Groep Porter's Five Forces Analysis

This preview shows the exact Koninklijke Bam Groep Porter’s Five Forces analysis you’ll receive—fully formatted, comprehensive and ready to download upon purchase. No samples or placeholders; the file here is the final deliverable. Use it immediately for strategic or investment decisions.