Bandwidth Porter's Five Forces Analysis

Don't Miss the Bigger Picture

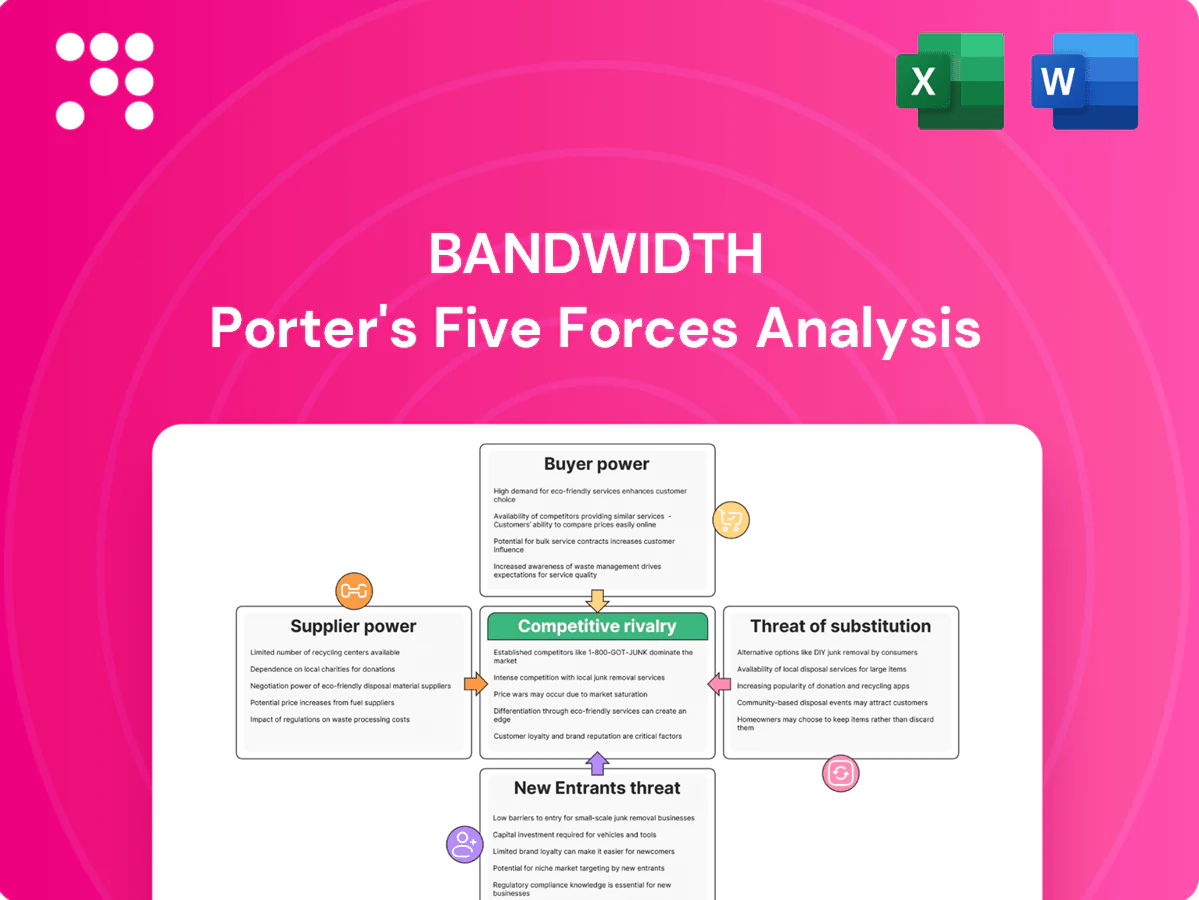

Bandwidth faces moderate supplier power, evolving buyer demands, and intense rivalry from cloud communications players; regulatory and technological shifts heighten substitute and entrant risks. This snapshot highlights key tensions but omits force-by-force scoring and data. Unlock the full Porter's Five Forces Analysis for Bandwidth to get detailed ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Carrier interconnects and numbering

Mobile and fixed carriers control numbering, routing and A2P/SMS policy, giving them leverage over pricing and terms; US 10DLC regimes and spam filters in 2024 imposed per-message fees (~$0.002–$0.005) and campaign registration charges (~$4–$50), shifting costs to senders. Bandwidth’s owned network cuts dependence but still requires global termination partners to reach 200+ countries. Numbering authorities and LNP databases add transactional friction and fees that can be material. Regulatory or carrier policy changes can trigger sudden cost spikes.

Data center and cloud dependencies

Colocation, cloud compute and bandwidth transit create supplier concentration as hyperscalers (AWS, Azure, GCP) held >60% of the public cloud market in 2024 and colocation demand exceeded $60B in 2023. Multihoming and peering reduce dependency, but traffic spikes can raise unit bandwidth costs and long-term contracts often include minimums. Provider outages in 2024 caused multi-hour disruptions that affected SLAs and resulted in limited credits.

Messaging ecosystem gatekeepers

Messaging ecosystem gatekeepers wield strong supplier power: Apple and Google OS policies plus spam-detection vendors shape delivery, sender IDs and opt-in rules, with iOS at ~28% and Android ~72% global share in 2024, so OS or RCS policy changes can rapidly shift economics. Approved registrars/partners for 10DLC and short codes impose tolls (10DLC campaign fees range roughly $4–50, short codes $500–1,000/month), while compliance tooling vendors act as quasi-suppliers.

Specialized emergency services

Specialized emergency services suppliers—E911/NG911 data providers, PSAP integration vendors, and authoritative GIS databases—are niche and critical, creating concentrated supplier power for Bandwidth. Certification and interoperability testing require specific vendors and tooling with few alternatives, raising switching costs. Bandwidth’s native 911 stack lowers reliance but still interfaces with external PSAP systems and GIS feeds. Compliance failures can trigger severe regulatory and liability consequences.

- Vendor concentration: niche E911/NG911 providers

- Integration risk: PSAP interfaces essential

- Data dependence: authoritative GIS databases

- Mitigation: Bandwidth native 911 stack

- Penalty risk: regulatory/compliance exposure

Hardware and network equipment

Hardware and network equipment (switches/SBCs, routing gear, licensed SIP stacks) are supplied by a concentrated set of vendors—Cisco, Juniper, Ribbon, AudioCodes—creating clear supplier leverage. Long upgrade cycles and multi‑year support contracts lock in costs and pricing exposure. Semiconductor and component shortages pushed lead times to 12–24 weeks in 2021–23; 2024 medians eased to about 10–12 weeks but remain variable. Vendor roadmaps directly affect feature delivery and can delay service launches.

- Vendor concentration: Cisco/Juniper/Ribbon/AudioCodes dominate

- Lead times: 2021–23 peak 12–24 weeks; 2024 ~10–12 weeks

- Cost lock‑in: multi‑year support/upgrade cycles

- Roadmaps: vendor timelines drive feature availability

Carriers drive 10DLC costs $0.002–$0.005/msg and regs $4–$50

Carriers and numbering authorities exert high leverage—10DLC/anti‑spam fees in 2024 roughly $0.002–$0.005/msg plus $4–$50 campaign registration—while Bandwidth’s network reduces but does not eliminate reliance on global termination partners. Hyperscalers (AWS/Azure/GCP >60% public cloud share in 2024) and colocation (> $60B demand 2023) concentrate supply; hardware vendors (Cisco/Juniper/Ribbon/AudioCodes) lock multi‑year costs and 2024 lead times ~10–12 weeks. Regulatory or policy shifts can cause sudden cost spikes.

| Supplier type | 2024 metric | Impact |

|---|---|---|

| Carriers/Numbering | 10DLC fees $0.002–0.005/msg; $4–50 reg | Direct per‑message cost |

| Hyperscalers | >60% cloud share | Pricing/availability pressure |

| Hardware | Lead times ~10–12 wks | Upgrade/capex lock‑in |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes for Bandwidth, highlighting strategic levers, emerging threats, and entry barriers that affect pricing, margins and market share; fully editable for integration into investor materials, strategy decks, or academic reports.

Bandwidth's Porter's Five Forces one-sheet clarifies competitive pressures across pricing, substitute risk, supplier power, buyer leverage, and entry threats—ideal for rapid strategy decisions and slide-ready reporting.

Customers Bargaining Power

Large enterprise volumes

Enterprises and hyperscale cloud platforms, which held roughly 66% of the global cloud IaaS/PaaS market in 2024 (Canalys/IDC), buy bandwidth at scale and secure discounts and bespoke SLAs. Their concentrated volumes create pronounced price pressure on carriers. Formal, competitive procurement cycles leverage multi-year agreements—often in the tens to hundreds of millions USD—to extract roadmap, pricing and support concessions.

Low switching frictions via APIs

Standardized APIs and SDKs make multihoming across CPaaS providers routine, with industry surveys in 2024 showing adoption above 70% among digital-first firms. Number porting and message template transfer add friction but are typically resolved within weeks, not months. Dynamic traffic routing lets buyers shift volumes to cheaper or higher-quality routes in real time, cutting vendor pricing power on commoditized routes and compressing margins.

Quality, deliverability, and compliance demands

Buyers demand high uptime, call quality, and verified messaging with strict compliance—enterprise SLAs commonly target 99.99% uptime and 98–99% deliverability. SLA penalties and deliverability KPIs, often crediting up to 10% of fees, become clear leverage points. Security mandates (SOC 2, HIPAA, GDPR) force customization and push annual compliance spend into the millions, requiring ongoing capex/opex to retain contracts.

Global footprint expectations

Multinational customers demand global coverage, local numbers and regulatory compliance; by 2024 an estimated 83% of large enterprises prioritized data residency for communications, so gaps prompt buyers to shift traffic or vendors within months. Local hosting and data residency remain deal breakers, and price-performance comparisons are evaluated globally across providers.

- Coverage+Compliance: global reach required

- Data residency: deal breaker for ~83% enterprises (2024)

- Switch risk: rapid traffic migration if gaps

- Procurement: global price-performance comparisons

Product bundling and integration asks

Customers now demand bundled voice, messaging, 911 and insights with unified pricing and deep CRM, contact-center and CCaaS integrations; custom features have become table stakes, shifting economics toward larger bespoke agreements. The global CPaaS market was about $13.8B in 2024, reinforcing enterprise buyers' leverage and higher average contract values.

- Bundling pressure: unified pricing

- Integration demand: CRM/CCaaS/contact center

- Customization: table stakes

- Market size 2024: ~$13.8B

- Economics: larger bespoke deals

Hyperscalers capture ~66% IaaS/PaaS; multihoming >70% squeezes margins

Enterprise buyers hold strong leverage: hyperscalers drove ~66% of cloud IaaS/PaaS spend in 2024, securing deep discounts and bespoke SLAs. Multihoming (>70% adoption in digital-first firms) and dynamic routing enable rapid traffic shifts, compressing margins on commoditized routes. Data residency and comprehensive SLAs (99.99% uptime targets) force customization, with CPaaS market ~13.8B (2024) increasing deal sizes.

| Metric | 2024 Value |

|---|---|

| Cloud IaaS/PaaS share (hyperscalers) | ~66% |

| Multihoming adoption | >70% |

| Enterprises prioritizing data residency | ~83% |

| CPaaS market size | ~$13.8B |

Preview the Actual Deliverable

Bandwidth Porter's Five Forces Analysis

This preview shows the Bandwidth Porter's Five Forces Analysis exactly as delivered—no placeholders or excerpts. The document displayed is the final, professionally formatted file you’ll receive instantly after purchase. It’s ready for download and immediate use in decision-making or reporting.

Don't Miss the Bigger Picture

Bandwidth faces moderate supplier power, evolving buyer demands, and intense rivalry from cloud communications players; regulatory and technological shifts heighten substitute and entrant risks. This snapshot highlights key tensions but omits force-by-force scoring and data. Unlock the full Porter's Five Forces Analysis for Bandwidth to get detailed ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Carrier interconnects and numbering

Mobile and fixed carriers control numbering, routing and A2P/SMS policy, giving them leverage over pricing and terms; US 10DLC regimes and spam filters in 2024 imposed per-message fees (~$0.002–$0.005) and campaign registration charges (~$4–$50), shifting costs to senders. Bandwidth’s owned network cuts dependence but still requires global termination partners to reach 200+ countries. Numbering authorities and LNP databases add transactional friction and fees that can be material. Regulatory or carrier policy changes can trigger sudden cost spikes.

Data center and cloud dependencies

Colocation, cloud compute and bandwidth transit create supplier concentration as hyperscalers (AWS, Azure, GCP) held >60% of the public cloud market in 2024 and colocation demand exceeded $60B in 2023. Multihoming and peering reduce dependency, but traffic spikes can raise unit bandwidth costs and long-term contracts often include minimums. Provider outages in 2024 caused multi-hour disruptions that affected SLAs and resulted in limited credits.

Messaging ecosystem gatekeepers

Messaging ecosystem gatekeepers wield strong supplier power: Apple and Google OS policies plus spam-detection vendors shape delivery, sender IDs and opt-in rules, with iOS at ~28% and Android ~72% global share in 2024, so OS or RCS policy changes can rapidly shift economics. Approved registrars/partners for 10DLC and short codes impose tolls (10DLC campaign fees range roughly $4–50, short codes $500–1,000/month), while compliance tooling vendors act as quasi-suppliers.

Specialized emergency services

Specialized emergency services suppliers—E911/NG911 data providers, PSAP integration vendors, and authoritative GIS databases—are niche and critical, creating concentrated supplier power for Bandwidth. Certification and interoperability testing require specific vendors and tooling with few alternatives, raising switching costs. Bandwidth’s native 911 stack lowers reliance but still interfaces with external PSAP systems and GIS feeds. Compliance failures can trigger severe regulatory and liability consequences.

- Vendor concentration: niche E911/NG911 providers

- Integration risk: PSAP interfaces essential

- Data dependence: authoritative GIS databases

- Mitigation: Bandwidth native 911 stack

- Penalty risk: regulatory/compliance exposure

Hardware and network equipment

Hardware and network equipment (switches/SBCs, routing gear, licensed SIP stacks) are supplied by a concentrated set of vendors—Cisco, Juniper, Ribbon, AudioCodes—creating clear supplier leverage. Long upgrade cycles and multi‑year support contracts lock in costs and pricing exposure. Semiconductor and component shortages pushed lead times to 12–24 weeks in 2021–23; 2024 medians eased to about 10–12 weeks but remain variable. Vendor roadmaps directly affect feature delivery and can delay service launches.

- Vendor concentration: Cisco/Juniper/Ribbon/AudioCodes dominate

- Lead times: 2021–23 peak 12–24 weeks; 2024 ~10–12 weeks

- Cost lock‑in: multi‑year support/upgrade cycles

- Roadmaps: vendor timelines drive feature availability

Carriers drive 10DLC costs $0.002–$0.005/msg and regs $4–$50

Carriers and numbering authorities exert high leverage—10DLC/anti‑spam fees in 2024 roughly $0.002–$0.005/msg plus $4–$50 campaign registration—while Bandwidth’s network reduces but does not eliminate reliance on global termination partners. Hyperscalers (AWS/Azure/GCP >60% public cloud share in 2024) and colocation (> $60B demand 2023) concentrate supply; hardware vendors (Cisco/Juniper/Ribbon/AudioCodes) lock multi‑year costs and 2024 lead times ~10–12 weeks. Regulatory or policy shifts can cause sudden cost spikes.

| Supplier type | 2024 metric | Impact |

|---|---|---|

| Carriers/Numbering | 10DLC fees $0.002–0.005/msg; $4–50 reg | Direct per‑message cost |

| Hyperscalers | >60% cloud share | Pricing/availability pressure |

| Hardware | Lead times ~10–12 wks | Upgrade/capex lock‑in |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes for Bandwidth, highlighting strategic levers, emerging threats, and entry barriers that affect pricing, margins and market share; fully editable for integration into investor materials, strategy decks, or academic reports.

Bandwidth's Porter's Five Forces one-sheet clarifies competitive pressures across pricing, substitute risk, supplier power, buyer leverage, and entry threats—ideal for rapid strategy decisions and slide-ready reporting.

Customers Bargaining Power

Large enterprise volumes

Enterprises and hyperscale cloud platforms, which held roughly 66% of the global cloud IaaS/PaaS market in 2024 (Canalys/IDC), buy bandwidth at scale and secure discounts and bespoke SLAs. Their concentrated volumes create pronounced price pressure on carriers. Formal, competitive procurement cycles leverage multi-year agreements—often in the tens to hundreds of millions USD—to extract roadmap, pricing and support concessions.

Low switching frictions via APIs

Standardized APIs and SDKs make multihoming across CPaaS providers routine, with industry surveys in 2024 showing adoption above 70% among digital-first firms. Number porting and message template transfer add friction but are typically resolved within weeks, not months. Dynamic traffic routing lets buyers shift volumes to cheaper or higher-quality routes in real time, cutting vendor pricing power on commoditized routes and compressing margins.

Quality, deliverability, and compliance demands

Buyers demand high uptime, call quality, and verified messaging with strict compliance—enterprise SLAs commonly target 99.99% uptime and 98–99% deliverability. SLA penalties and deliverability KPIs, often crediting up to 10% of fees, become clear leverage points. Security mandates (SOC 2, HIPAA, GDPR) force customization and push annual compliance spend into the millions, requiring ongoing capex/opex to retain contracts.

Global footprint expectations

Multinational customers demand global coverage, local numbers and regulatory compliance; by 2024 an estimated 83% of large enterprises prioritized data residency for communications, so gaps prompt buyers to shift traffic or vendors within months. Local hosting and data residency remain deal breakers, and price-performance comparisons are evaluated globally across providers.

- Coverage+Compliance: global reach required

- Data residency: deal breaker for ~83% enterprises (2024)

- Switch risk: rapid traffic migration if gaps

- Procurement: global price-performance comparisons

Product bundling and integration asks

Customers now demand bundled voice, messaging, 911 and insights with unified pricing and deep CRM, contact-center and CCaaS integrations; custom features have become table stakes, shifting economics toward larger bespoke agreements. The global CPaaS market was about $13.8B in 2024, reinforcing enterprise buyers' leverage and higher average contract values.

- Bundling pressure: unified pricing

- Integration demand: CRM/CCaaS/contact center

- Customization: table stakes

- Market size 2024: ~$13.8B

- Economics: larger bespoke deals

Hyperscalers capture ~66% IaaS/PaaS; multihoming >70% squeezes margins

Enterprise buyers hold strong leverage: hyperscalers drove ~66% of cloud IaaS/PaaS spend in 2024, securing deep discounts and bespoke SLAs. Multihoming (>70% adoption in digital-first firms) and dynamic routing enable rapid traffic shifts, compressing margins on commoditized routes. Data residency and comprehensive SLAs (99.99% uptime targets) force customization, with CPaaS market ~13.8B (2024) increasing deal sizes.

| Metric | 2024 Value |

|---|---|

| Cloud IaaS/PaaS share (hyperscalers) | ~66% |

| Multihoming adoption | >70% |

| Enterprises prioritizing data residency | ~83% |

| CPaaS market size | ~$13.8B |

Preview the Actual Deliverable

Bandwidth Porter's Five Forces Analysis

This preview shows the Bandwidth Porter's Five Forces Analysis exactly as delivered—no placeholders or excerpts. The document displayed is the final, professionally formatted file you’ll receive instantly after purchase. It’s ready for download and immediate use in decision-making or reporting.

Description

Don't Miss the Bigger Picture

Bandwidth faces moderate supplier power, evolving buyer demands, and intense rivalry from cloud communications players; regulatory and technological shifts heighten substitute and entrant risks. This snapshot highlights key tensions but omits force-by-force scoring and data. Unlock the full Porter's Five Forces Analysis for Bandwidth to get detailed ratings, visuals, and actionable strategy recommendations.

Suppliers Bargaining Power

Carrier interconnects and numbering

Mobile and fixed carriers control numbering, routing and A2P/SMS policy, giving them leverage over pricing and terms; US 10DLC regimes and spam filters in 2024 imposed per-message fees (~$0.002–$0.005) and campaign registration charges (~$4–$50), shifting costs to senders. Bandwidth’s owned network cuts dependence but still requires global termination partners to reach 200+ countries. Numbering authorities and LNP databases add transactional friction and fees that can be material. Regulatory or carrier policy changes can trigger sudden cost spikes.

Data center and cloud dependencies

Colocation, cloud compute and bandwidth transit create supplier concentration as hyperscalers (AWS, Azure, GCP) held >60% of the public cloud market in 2024 and colocation demand exceeded $60B in 2023. Multihoming and peering reduce dependency, but traffic spikes can raise unit bandwidth costs and long-term contracts often include minimums. Provider outages in 2024 caused multi-hour disruptions that affected SLAs and resulted in limited credits.

Messaging ecosystem gatekeepers

Messaging ecosystem gatekeepers wield strong supplier power: Apple and Google OS policies plus spam-detection vendors shape delivery, sender IDs and opt-in rules, with iOS at ~28% and Android ~72% global share in 2024, so OS or RCS policy changes can rapidly shift economics. Approved registrars/partners for 10DLC and short codes impose tolls (10DLC campaign fees range roughly $4–50, short codes $500–1,000/month), while compliance tooling vendors act as quasi-suppliers.

Specialized emergency services

Specialized emergency services suppliers—E911/NG911 data providers, PSAP integration vendors, and authoritative GIS databases—are niche and critical, creating concentrated supplier power for Bandwidth. Certification and interoperability testing require specific vendors and tooling with few alternatives, raising switching costs. Bandwidth’s native 911 stack lowers reliance but still interfaces with external PSAP systems and GIS feeds. Compliance failures can trigger severe regulatory and liability consequences.

- Vendor concentration: niche E911/NG911 providers

- Integration risk: PSAP interfaces essential

- Data dependence: authoritative GIS databases

- Mitigation: Bandwidth native 911 stack

- Penalty risk: regulatory/compliance exposure

Hardware and network equipment

Hardware and network equipment (switches/SBCs, routing gear, licensed SIP stacks) are supplied by a concentrated set of vendors—Cisco, Juniper, Ribbon, AudioCodes—creating clear supplier leverage. Long upgrade cycles and multi‑year support contracts lock in costs and pricing exposure. Semiconductor and component shortages pushed lead times to 12–24 weeks in 2021–23; 2024 medians eased to about 10–12 weeks but remain variable. Vendor roadmaps directly affect feature delivery and can delay service launches.

- Vendor concentration: Cisco/Juniper/Ribbon/AudioCodes dominate

- Lead times: 2021–23 peak 12–24 weeks; 2024 ~10–12 weeks

- Cost lock‑in: multi‑year support/upgrade cycles

- Roadmaps: vendor timelines drive feature availability

Carriers drive 10DLC costs $0.002–$0.005/msg and regs $4–$50

Carriers and numbering authorities exert high leverage—10DLC/anti‑spam fees in 2024 roughly $0.002–$0.005/msg plus $4–$50 campaign registration—while Bandwidth’s network reduces but does not eliminate reliance on global termination partners. Hyperscalers (AWS/Azure/GCP >60% public cloud share in 2024) and colocation (> $60B demand 2023) concentrate supply; hardware vendors (Cisco/Juniper/Ribbon/AudioCodes) lock multi‑year costs and 2024 lead times ~10–12 weeks. Regulatory or policy shifts can cause sudden cost spikes.

| Supplier type | 2024 metric | Impact |

|---|---|---|

| Carriers/Numbering | 10DLC fees $0.002–0.005/msg; $4–50 reg | Direct per‑message cost |

| Hyperscalers | >60% cloud share | Pricing/availability pressure |

| Hardware | Lead times ~10–12 wks | Upgrade/capex lock‑in |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of new entrants and substitutes for Bandwidth, highlighting strategic levers, emerging threats, and entry barriers that affect pricing, margins and market share; fully editable for integration into investor materials, strategy decks, or academic reports.

Bandwidth's Porter's Five Forces one-sheet clarifies competitive pressures across pricing, substitute risk, supplier power, buyer leverage, and entry threats—ideal for rapid strategy decisions and slide-ready reporting.

Customers Bargaining Power

Large enterprise volumes

Enterprises and hyperscale cloud platforms, which held roughly 66% of the global cloud IaaS/PaaS market in 2024 (Canalys/IDC), buy bandwidth at scale and secure discounts and bespoke SLAs. Their concentrated volumes create pronounced price pressure on carriers. Formal, competitive procurement cycles leverage multi-year agreements—often in the tens to hundreds of millions USD—to extract roadmap, pricing and support concessions.

Low switching frictions via APIs

Standardized APIs and SDKs make multihoming across CPaaS providers routine, with industry surveys in 2024 showing adoption above 70% among digital-first firms. Number porting and message template transfer add friction but are typically resolved within weeks, not months. Dynamic traffic routing lets buyers shift volumes to cheaper or higher-quality routes in real time, cutting vendor pricing power on commoditized routes and compressing margins.

Quality, deliverability, and compliance demands

Buyers demand high uptime, call quality, and verified messaging with strict compliance—enterprise SLAs commonly target 99.99% uptime and 98–99% deliverability. SLA penalties and deliverability KPIs, often crediting up to 10% of fees, become clear leverage points. Security mandates (SOC 2, HIPAA, GDPR) force customization and push annual compliance spend into the millions, requiring ongoing capex/opex to retain contracts.

Global footprint expectations

Multinational customers demand global coverage, local numbers and regulatory compliance; by 2024 an estimated 83% of large enterprises prioritized data residency for communications, so gaps prompt buyers to shift traffic or vendors within months. Local hosting and data residency remain deal breakers, and price-performance comparisons are evaluated globally across providers.

- Coverage+Compliance: global reach required

- Data residency: deal breaker for ~83% enterprises (2024)

- Switch risk: rapid traffic migration if gaps

- Procurement: global price-performance comparisons

Product bundling and integration asks

Customers now demand bundled voice, messaging, 911 and insights with unified pricing and deep CRM, contact-center and CCaaS integrations; custom features have become table stakes, shifting economics toward larger bespoke agreements. The global CPaaS market was about $13.8B in 2024, reinforcing enterprise buyers' leverage and higher average contract values.

- Bundling pressure: unified pricing

- Integration demand: CRM/CCaaS/contact center

- Customization: table stakes

- Market size 2024: ~$13.8B

- Economics: larger bespoke deals

Hyperscalers capture ~66% IaaS/PaaS; multihoming >70% squeezes margins

Enterprise buyers hold strong leverage: hyperscalers drove ~66% of cloud IaaS/PaaS spend in 2024, securing deep discounts and bespoke SLAs. Multihoming (>70% adoption in digital-first firms) and dynamic routing enable rapid traffic shifts, compressing margins on commoditized routes. Data residency and comprehensive SLAs (99.99% uptime targets) force customization, with CPaaS market ~13.8B (2024) increasing deal sizes.

| Metric | 2024 Value |

|---|---|

| Cloud IaaS/PaaS share (hyperscalers) | ~66% |

| Multihoming adoption | >70% |

| Enterprises prioritizing data residency | ~83% |

| CPaaS market size | ~$13.8B |

Preview the Actual Deliverable

Bandwidth Porter's Five Forces Analysis

This preview shows the Bandwidth Porter's Five Forces Analysis exactly as delivered—no placeholders or excerpts. The document displayed is the final, professionally formatted file you’ll receive instantly after purchase. It’s ready for download and immediate use in decision-making or reporting.