Bank Albilad Business Model Canvas

Business Model Canvas: Strategic Blueprint for a Leading Bank

Unlock the full strategic blueprint behind Bank Albilad’s success with our Business Model Canvas — a concise, sector-specific map of value propositions, customer segments, channels, and revenue drivers. This professionally written canvas reveals competitive advantages, cost structure, and scaling levers to inform investors, consultants, and executives. Download the complete Word and Excel files to benchmark, plan, and act on proven strategies today.

Partnerships

Sharia supervisory boards

Partnership with qualified Sharia scholars ensures Bank Albilad products comply with Islamic principles and receive ongoing fatwa oversight. Scholars review structures like Murabaha, Ijarah and Mudarabah before launch, supporting governance as global Islamic finance assets surpassed 3 trillion dollars in 2024. Continuous audits and updates maintain credibility and customer trust. This formal Sharia oversight differentiates offerings in a competitive Islamic banking market.

Regulators and government bodies

Close coordination with the Saudi Central Bank (SAMA) and other authorities secures licenses and ensures ongoing regulatory compliance, enabling Bank Albilad to operate within Saudi Arabia’s Islamic banking framework. Regulatory engagement supports new product approvals and participation in SAMA sandbox initiatives that accelerate digital offerings. Alignment with national economic programs facilitates the bank’s role in Saudi development, reducing regulatory risk and speeding innovation.

Fintechs and payment networks

Alliances with fintechs accelerate digital onboarding, wallets and instant payments, tapping Saudi Arabia’s c.98% smartphone penetration in 2024 to boost uptake. Partnerships with payment schemes and switches (mada/Saudi Payments) expand card acceptance and real-time transfers across the kingdom. Open APIs enable embedded finance with ecosystem partners, improving customer experience and driving higher transaction volumes and frequency.

Corporate, SME, and institutional partners

Anchor corporate, SME and institutional partners co-create tailored financing and cash-management solutions that integrate trade, payroll and collections to deepen deposits and fee income. Supply-chain financiers and merchant networks extend the bank’s reach into SME corridors, improving origination and risk segmentation. Collaboration with public sector entities, NGOs and corporates drives sustained trade flows and recurring transaction volumes.

- Co-creation of tailored cash-management and trade solutions

- Supply-chain and merchant channels to scale SME access

- Public sector and corporate payrolls to anchor balances and fees

Technology and infrastructure vendors

Technology and infrastructure vendors — core banking, cloud, cybersecurity, and analytics providers — underpin resilient Bank Albilad operations, with leading cloud SLAs commonly at or above 99.9% and mission-critical contracts targeting 99.99% uptime.

Outsourcing selective services accelerates speed-to-market and scalability while data center and telecom partners ensure connectivity; vendor SLAs and reporting support regulatory and Sharia audit requirements.

- core-banking

- cloud-99.9+%‑sla

- cybersecurity

- analytics

- datacenter-connectivity

- sla-compliance

Sharia ties anchor digital deposits — assets > 3.0T$, 98% mobile

Partnerships with Sharia scholars, SAMA, fintechs, corporates and tech vendors drive compliance, digital adoption and deposit anchoring—Islamic finance assets >3.0T$ in 2024; smartphone penetration c.98% in 2024.

Vendor SLAs target 99.9–99.99% uptime; embedded APIs boost transaction frequency and fee income.

| Partner | Metric |

|---|---|

| Sharia | 3.0T$ market (2024) |

| Fintechs | 98% smartphone (2024) |

| Vendors | 99.9–99.99% SLA |

What is included in the product

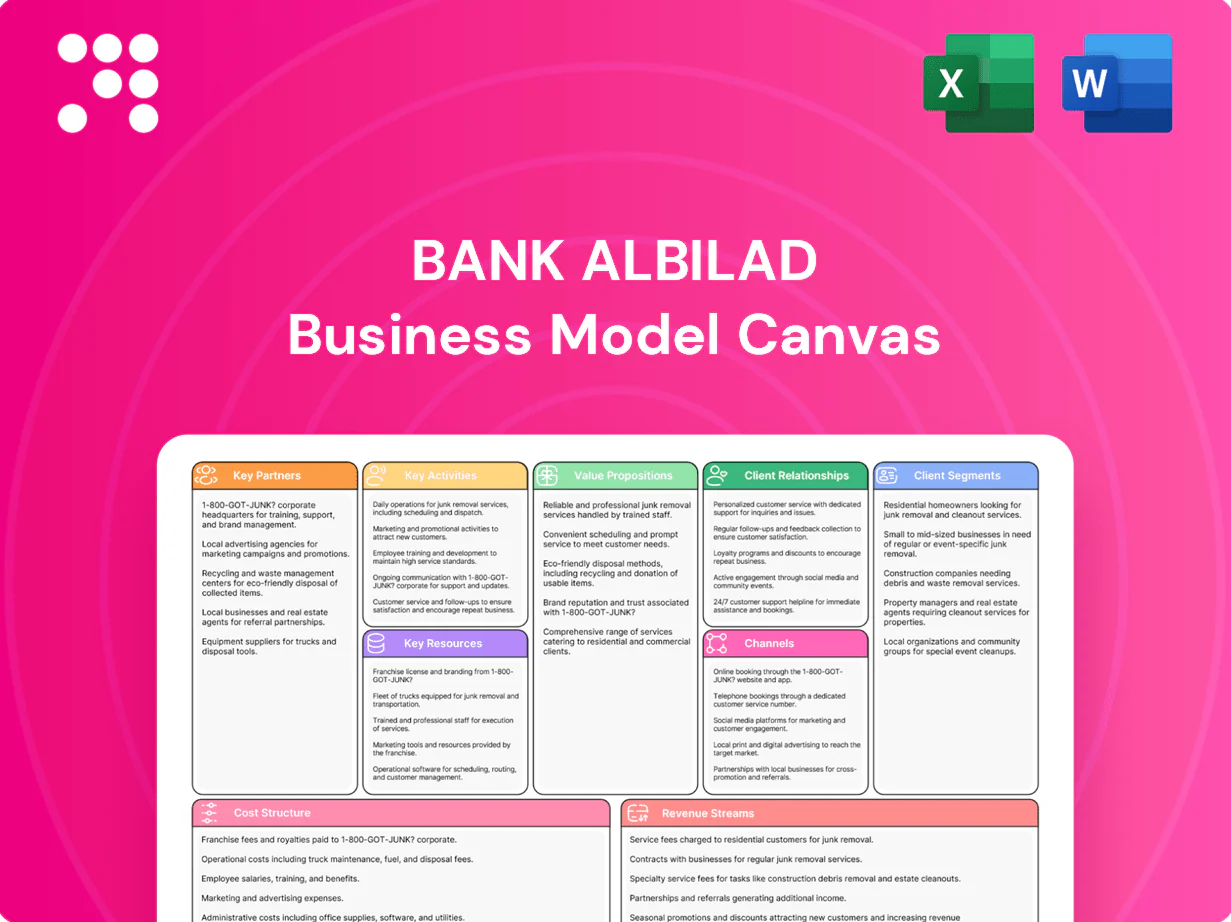

A comprehensive Business Model Canvas for Bank Albilad detailing customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages and linked SWOT insights—ideal for presentations, investor discussions and strategic decision-making.

High-level Business Model Canvas for Bank Albilad that condenses its strategy into an editable one-page snapshot, helping teams quickly identify core components and relieve planning bottlenecks. Perfect for boardrooms, fast deliverables, and collaborative adaptation of insights.

Activities

Designing Sharia-compliant products

Structuring financing and deposit products under Islamic contracts is central, with each product undergoing Sharia review and formal documentation to ensure permissibility and operational clarity. Pricing and risk terms are aligned with AAOIFI standards (established 1991) to maintain industry-accepted governance. Continuous product refinement keeps offerings competitive while preserving compliance.

Risk management and compliance

Credit, market, liquidity and operational risks are actively monitored through risk appetite limits, daily metrics and monthly board reporting in 2024. AML/CFT, KYC and conduct controls protect the franchise, aligned with SAMA and FATF standards and enhanced transaction monitoring in 2024. Sharia audit runs in parallel with internal audit while stress testing and ICAAP/ILAAP sustain capital and liquidity resilience.

Treasury and liquidity management

Treasury and liquidity management at Bank Albilad centers on managing liquidity via sukuk, interbank placements and commodity Murabaha to support day-to-day funding needs. Profit rate risk is hedged using Sharia-compliant tools (Waad/commodity structures) consistent with SAMA’s 2024 LCR framework requiring minimum 100% coverage. Funding-mix optimization balances stability and cost, while cash and collateral management underpin daily operations.

Digital banking and customer onboarding

Digital-first journeys enable Bank Albilad customers to open accounts, make payments and request financing via mobile apps, supported by APIs that integrate partners and power open banking. Data analytics personalize offers and help reduce churn, while cybersecurity and fraud controls protect users and transactions in a market with 99% internet penetration (2024).

- Mobile-first account opening, payments, financing

- APIs for partner integration and open banking

- Analytics-driven personalization and churn reduction

- Robust cybersecurity and fraud controls

Branch and relationship management

Branch and relationship management at Bank Albilad leverages over 170 branches across the kingdom to deliver advisory and complex transactions; relationship managers cover corporate, SME and affluent segments to deepen wallet share. Service operations process payments, trade and collections at scale, while service quality programs in 2024 focus on improving satisfaction and retention.

- Coverage: over 170 branches

- Segments: corporate, SME, affluent

- Operations: payments, trade, collections

- Focus: service quality and retention

Sharia-compliant finance, AAOIFI pricing, digital onboarding and 170+ branches

Structuring Islamic financing and deposit products with Sharia review and AAOIFI-aligned pricing (AAOIFI est. 1991) is core. Credit, market, liquidity and operational risks are monitored with daily metrics and monthly board reporting (2024). Digital-first channels, APIs and 170+ branches support onboarding, payments and advisory while cybersecurity and AML/CFT controls protect transactions.

| Metric | 2024 |

|---|---|

| Branches | over 170 |

| LCR requirement | 100% |

| Internet penetration (KSA) | 99% |

Full Version Awaits

Business Model Canvas

The Business Model Canvas for Bank Albilad shown here is the exact document you'll receive — not a mockup or teaser. Upon purchase you'll download this same fully formatted, editable file ready for presentation and analysis. No changes, no omissions, just the full deliverable.

Business Model Canvas: Strategic Blueprint for a Leading Bank

Unlock the full strategic blueprint behind Bank Albilad’s success with our Business Model Canvas — a concise, sector-specific map of value propositions, customer segments, channels, and revenue drivers. This professionally written canvas reveals competitive advantages, cost structure, and scaling levers to inform investors, consultants, and executives. Download the complete Word and Excel files to benchmark, plan, and act on proven strategies today.

Partnerships

Sharia supervisory boards

Partnership with qualified Sharia scholars ensures Bank Albilad products comply with Islamic principles and receive ongoing fatwa oversight. Scholars review structures like Murabaha, Ijarah and Mudarabah before launch, supporting governance as global Islamic finance assets surpassed 3 trillion dollars in 2024. Continuous audits and updates maintain credibility and customer trust. This formal Sharia oversight differentiates offerings in a competitive Islamic banking market.

Regulators and government bodies

Close coordination with the Saudi Central Bank (SAMA) and other authorities secures licenses and ensures ongoing regulatory compliance, enabling Bank Albilad to operate within Saudi Arabia’s Islamic banking framework. Regulatory engagement supports new product approvals and participation in SAMA sandbox initiatives that accelerate digital offerings. Alignment with national economic programs facilitates the bank’s role in Saudi development, reducing regulatory risk and speeding innovation.

Fintechs and payment networks

Alliances with fintechs accelerate digital onboarding, wallets and instant payments, tapping Saudi Arabia’s c.98% smartphone penetration in 2024 to boost uptake. Partnerships with payment schemes and switches (mada/Saudi Payments) expand card acceptance and real-time transfers across the kingdom. Open APIs enable embedded finance with ecosystem partners, improving customer experience and driving higher transaction volumes and frequency.

Corporate, SME, and institutional partners

Anchor corporate, SME and institutional partners co-create tailored financing and cash-management solutions that integrate trade, payroll and collections to deepen deposits and fee income. Supply-chain financiers and merchant networks extend the bank’s reach into SME corridors, improving origination and risk segmentation. Collaboration with public sector entities, NGOs and corporates drives sustained trade flows and recurring transaction volumes.

- Co-creation of tailored cash-management and trade solutions

- Supply-chain and merchant channels to scale SME access

- Public sector and corporate payrolls to anchor balances and fees

Technology and infrastructure vendors

Technology and infrastructure vendors — core banking, cloud, cybersecurity, and analytics providers — underpin resilient Bank Albilad operations, with leading cloud SLAs commonly at or above 99.9% and mission-critical contracts targeting 99.99% uptime.

Outsourcing selective services accelerates speed-to-market and scalability while data center and telecom partners ensure connectivity; vendor SLAs and reporting support regulatory and Sharia audit requirements.

- core-banking

- cloud-99.9+%‑sla

- cybersecurity

- analytics

- datacenter-connectivity

- sla-compliance

Sharia ties anchor digital deposits — assets > 3.0T$, 98% mobile

Partnerships with Sharia scholars, SAMA, fintechs, corporates and tech vendors drive compliance, digital adoption and deposit anchoring—Islamic finance assets >3.0T$ in 2024; smartphone penetration c.98% in 2024.

Vendor SLAs target 99.9–99.99% uptime; embedded APIs boost transaction frequency and fee income.

| Partner | Metric |

|---|---|

| Sharia | 3.0T$ market (2024) |

| Fintechs | 98% smartphone (2024) |

| Vendors | 99.9–99.99% SLA |

What is included in the product

A comprehensive Business Model Canvas for Bank Albilad detailing customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages and linked SWOT insights—ideal for presentations, investor discussions and strategic decision-making.

High-level Business Model Canvas for Bank Albilad that condenses its strategy into an editable one-page snapshot, helping teams quickly identify core components and relieve planning bottlenecks. Perfect for boardrooms, fast deliverables, and collaborative adaptation of insights.

Activities

Designing Sharia-compliant products

Structuring financing and deposit products under Islamic contracts is central, with each product undergoing Sharia review and formal documentation to ensure permissibility and operational clarity. Pricing and risk terms are aligned with AAOIFI standards (established 1991) to maintain industry-accepted governance. Continuous product refinement keeps offerings competitive while preserving compliance.

Risk management and compliance

Credit, market, liquidity and operational risks are actively monitored through risk appetite limits, daily metrics and monthly board reporting in 2024. AML/CFT, KYC and conduct controls protect the franchise, aligned with SAMA and FATF standards and enhanced transaction monitoring in 2024. Sharia audit runs in parallel with internal audit while stress testing and ICAAP/ILAAP sustain capital and liquidity resilience.

Treasury and liquidity management

Treasury and liquidity management at Bank Albilad centers on managing liquidity via sukuk, interbank placements and commodity Murabaha to support day-to-day funding needs. Profit rate risk is hedged using Sharia-compliant tools (Waad/commodity structures) consistent with SAMA’s 2024 LCR framework requiring minimum 100% coverage. Funding-mix optimization balances stability and cost, while cash and collateral management underpin daily operations.

Digital banking and customer onboarding

Digital-first journeys enable Bank Albilad customers to open accounts, make payments and request financing via mobile apps, supported by APIs that integrate partners and power open banking. Data analytics personalize offers and help reduce churn, while cybersecurity and fraud controls protect users and transactions in a market with 99% internet penetration (2024).

- Mobile-first account opening, payments, financing

- APIs for partner integration and open banking

- Analytics-driven personalization and churn reduction

- Robust cybersecurity and fraud controls

Branch and relationship management

Branch and relationship management at Bank Albilad leverages over 170 branches across the kingdom to deliver advisory and complex transactions; relationship managers cover corporate, SME and affluent segments to deepen wallet share. Service operations process payments, trade and collections at scale, while service quality programs in 2024 focus on improving satisfaction and retention.

- Coverage: over 170 branches

- Segments: corporate, SME, affluent

- Operations: payments, trade, collections

- Focus: service quality and retention

Sharia-compliant finance, AAOIFI pricing, digital onboarding and 170+ branches

Structuring Islamic financing and deposit products with Sharia review and AAOIFI-aligned pricing (AAOIFI est. 1991) is core. Credit, market, liquidity and operational risks are monitored with daily metrics and monthly board reporting (2024). Digital-first channels, APIs and 170+ branches support onboarding, payments and advisory while cybersecurity and AML/CFT controls protect transactions.

| Metric | 2024 |

|---|---|

| Branches | over 170 |

| LCR requirement | 100% |

| Internet penetration (KSA) | 99% |

Full Version Awaits

Business Model Canvas

The Business Model Canvas for Bank Albilad shown here is the exact document you'll receive — not a mockup or teaser. Upon purchase you'll download this same fully formatted, editable file ready for presentation and analysis. No changes, no omissions, just the full deliverable.

Description

Business Model Canvas: Strategic Blueprint for a Leading Bank

Unlock the full strategic blueprint behind Bank Albilad’s success with our Business Model Canvas — a concise, sector-specific map of value propositions, customer segments, channels, and revenue drivers. This professionally written canvas reveals competitive advantages, cost structure, and scaling levers to inform investors, consultants, and executives. Download the complete Word and Excel files to benchmark, plan, and act on proven strategies today.

Partnerships

Sharia supervisory boards

Partnership with qualified Sharia scholars ensures Bank Albilad products comply with Islamic principles and receive ongoing fatwa oversight. Scholars review structures like Murabaha, Ijarah and Mudarabah before launch, supporting governance as global Islamic finance assets surpassed 3 trillion dollars in 2024. Continuous audits and updates maintain credibility and customer trust. This formal Sharia oversight differentiates offerings in a competitive Islamic banking market.

Regulators and government bodies

Close coordination with the Saudi Central Bank (SAMA) and other authorities secures licenses and ensures ongoing regulatory compliance, enabling Bank Albilad to operate within Saudi Arabia’s Islamic banking framework. Regulatory engagement supports new product approvals and participation in SAMA sandbox initiatives that accelerate digital offerings. Alignment with national economic programs facilitates the bank’s role in Saudi development, reducing regulatory risk and speeding innovation.

Fintechs and payment networks

Alliances with fintechs accelerate digital onboarding, wallets and instant payments, tapping Saudi Arabia’s c.98% smartphone penetration in 2024 to boost uptake. Partnerships with payment schemes and switches (mada/Saudi Payments) expand card acceptance and real-time transfers across the kingdom. Open APIs enable embedded finance with ecosystem partners, improving customer experience and driving higher transaction volumes and frequency.

Corporate, SME, and institutional partners

Anchor corporate, SME and institutional partners co-create tailored financing and cash-management solutions that integrate trade, payroll and collections to deepen deposits and fee income. Supply-chain financiers and merchant networks extend the bank’s reach into SME corridors, improving origination and risk segmentation. Collaboration with public sector entities, NGOs and corporates drives sustained trade flows and recurring transaction volumes.

- Co-creation of tailored cash-management and trade solutions

- Supply-chain and merchant channels to scale SME access

- Public sector and corporate payrolls to anchor balances and fees

Technology and infrastructure vendors

Technology and infrastructure vendors — core banking, cloud, cybersecurity, and analytics providers — underpin resilient Bank Albilad operations, with leading cloud SLAs commonly at or above 99.9% and mission-critical contracts targeting 99.99% uptime.

Outsourcing selective services accelerates speed-to-market and scalability while data center and telecom partners ensure connectivity; vendor SLAs and reporting support regulatory and Sharia audit requirements.

- core-banking

- cloud-99.9+%‑sla

- cybersecurity

- analytics

- datacenter-connectivity

- sla-compliance

Sharia ties anchor digital deposits — assets > 3.0T$, 98% mobile

Partnerships with Sharia scholars, SAMA, fintechs, corporates and tech vendors drive compliance, digital adoption and deposit anchoring—Islamic finance assets >3.0T$ in 2024; smartphone penetration c.98% in 2024.

Vendor SLAs target 99.9–99.99% uptime; embedded APIs boost transaction frequency and fee income.

| Partner | Metric |

|---|---|

| Sharia | 3.0T$ market (2024) |

| Fintechs | 98% smartphone (2024) |

| Vendors | 99.9–99.99% SLA |

What is included in the product

A comprehensive Business Model Canvas for Bank Albilad detailing customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages and linked SWOT insights—ideal for presentations, investor discussions and strategic decision-making.

High-level Business Model Canvas for Bank Albilad that condenses its strategy into an editable one-page snapshot, helping teams quickly identify core components and relieve planning bottlenecks. Perfect for boardrooms, fast deliverables, and collaborative adaptation of insights.

Activities

Designing Sharia-compliant products

Structuring financing and deposit products under Islamic contracts is central, with each product undergoing Sharia review and formal documentation to ensure permissibility and operational clarity. Pricing and risk terms are aligned with AAOIFI standards (established 1991) to maintain industry-accepted governance. Continuous product refinement keeps offerings competitive while preserving compliance.

Risk management and compliance

Credit, market, liquidity and operational risks are actively monitored through risk appetite limits, daily metrics and monthly board reporting in 2024. AML/CFT, KYC and conduct controls protect the franchise, aligned with SAMA and FATF standards and enhanced transaction monitoring in 2024. Sharia audit runs in parallel with internal audit while stress testing and ICAAP/ILAAP sustain capital and liquidity resilience.

Treasury and liquidity management

Treasury and liquidity management at Bank Albilad centers on managing liquidity via sukuk, interbank placements and commodity Murabaha to support day-to-day funding needs. Profit rate risk is hedged using Sharia-compliant tools (Waad/commodity structures) consistent with SAMA’s 2024 LCR framework requiring minimum 100% coverage. Funding-mix optimization balances stability and cost, while cash and collateral management underpin daily operations.

Digital banking and customer onboarding

Digital-first journeys enable Bank Albilad customers to open accounts, make payments and request financing via mobile apps, supported by APIs that integrate partners and power open banking. Data analytics personalize offers and help reduce churn, while cybersecurity and fraud controls protect users and transactions in a market with 99% internet penetration (2024).

- Mobile-first account opening, payments, financing

- APIs for partner integration and open banking

- Analytics-driven personalization and churn reduction

- Robust cybersecurity and fraud controls

Branch and relationship management

Branch and relationship management at Bank Albilad leverages over 170 branches across the kingdom to deliver advisory and complex transactions; relationship managers cover corporate, SME and affluent segments to deepen wallet share. Service operations process payments, trade and collections at scale, while service quality programs in 2024 focus on improving satisfaction and retention.

- Coverage: over 170 branches

- Segments: corporate, SME, affluent

- Operations: payments, trade, collections

- Focus: service quality and retention

Sharia-compliant finance, AAOIFI pricing, digital onboarding and 170+ branches

Structuring Islamic financing and deposit products with Sharia review and AAOIFI-aligned pricing (AAOIFI est. 1991) is core. Credit, market, liquidity and operational risks are monitored with daily metrics and monthly board reporting (2024). Digital-first channels, APIs and 170+ branches support onboarding, payments and advisory while cybersecurity and AML/CFT controls protect transactions.

| Metric | 2024 |

|---|---|

| Branches | over 170 |

| LCR requirement | 100% |

| Internet penetration (KSA) | 99% |

Full Version Awaits

Business Model Canvas

The Business Model Canvas for Bank Albilad shown here is the exact document you'll receive — not a mockup or teaser. Upon purchase you'll download this same fully formatted, editable file ready for presentation and analysis. No changes, no omissions, just the full deliverable.