Bank of Jiujiang Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

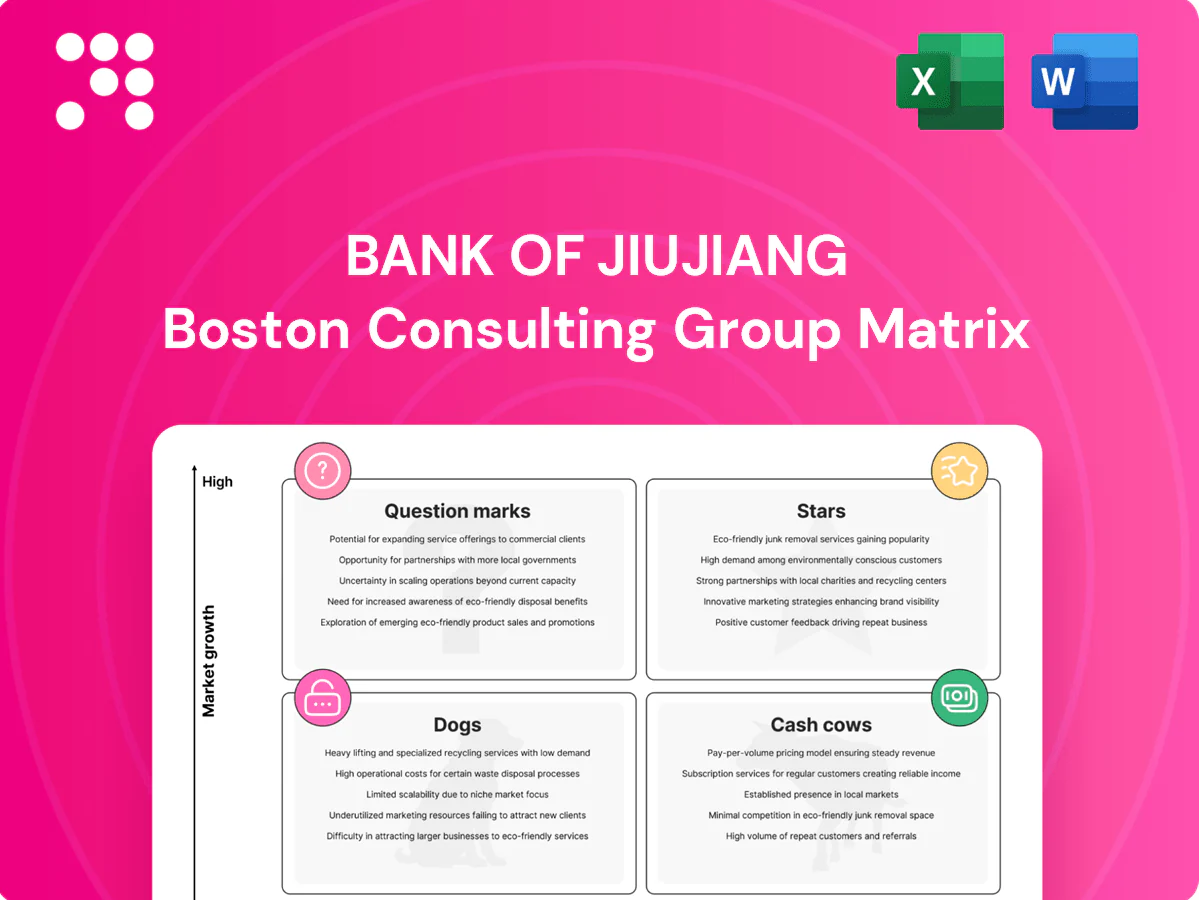

Curious where Bank of Jiujiang’s products sit—Stars, Cash Cows, Dogs or Question Marks? This preview scratches the surface; buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a clear roadmap for reallocating capital and prioritizing growth. Purchase now for a ready-to-use Word report plus an Excel summary that lets your team act fast.

Stars

Local SME lending engine

Local SME lending engine holds a dominant hometown share with demand steady-to-surging as Jiangxi industrial parks scale and provincial industrial output grew about 6% year-on-year in 2024. Continued expansion means loans can compound, but sustaining growth requires continual credit talent and advanced risk tools. Management should keep investing in underwriting and relationship managers to preserve and deepen share. Hold share now to let it mature into a compounding profit base.

Digital payments and settlement in Jiangxi

Digital payments and settlement in Jiangxi have become the de facto rail for many local businesses, showing strong daily usage and rising merchant adoption in 2024 as network effects accelerate. The product attracts scale but burns cash on tech, incentives, and uptime, pressuring margins. Prioritize reliability investments and deeper merchant integrations now. Win the platform game today to mint cash tomorrow.

Government and public-sector banking

Deep ties with local governments and SOE-linked entities give Bank of Jiujiang scale and client stickiness, anchoring core deposit and fee income streams. Transaction volumes rise with regional infrastructure projects and public-services digitization, expanding cash-management and fintech touchpoints. Maintain high service levels and disciplined pricing to protect margins against competitive pressure. A steady government pipeline feeds cross-sell opportunities across the franchise.

Mobile retail banking adoption

Mobile retail banking shows strong traction: monthly active users up ~30% YoY and payment/light-wealth transactions rising ~42% through 2024, but unit economics remain negative as acquisition and feature costs keep CAC above LTV in early cohorts.

Focus on active-user KPIs and structured cross-sell journeys; improving 90-day retention will translate into higher deposits and fee spread over 12–24 months.

- MAU growth ~30% YoY (2024)

- Payments/light-wealth txns +42% (2024)

- High CAC; near-term profitability weak

- Priority: active-user KPIs, cross-sell, retention→deposits/NIM

Supply-chain finance for anchor industries

Supply-chain finance for anchor industries is a Star for Bank of Jiujiang as local manufacturing and logistics anchors deliver steadily growing receivables and predictable cash conversion cycles; high invoice digitalization and platform data give visibility that compresses credit loss experience as volumes ramp. Prioritize investing in onboarding, anchor coverage teams and scalable platforms to capture market share and lock the ecosystem around the bank.

- Anchor-driven receivables: predictable flows

- High data visibility: lower risk, faster underwriting

- Invest: platforms, anchor coverage, fast onboarding

- Scale now: ecosystem lock-in and share gains

Back SME growth: scale underwriting, reliable payments & anchor-led supply-chain profits

SME lending, digital payments and supply-chain finance are Stars: SME loans leverage hometown dominance as Jiangxi industrial output +6% YoY (2024); mobile MAU +30% and payments +42% (2024); supply-chain shows lower loss ratios with rising invoice digitalization. Invest in underwriting, reliability, platforms and anchor coverage to convert share into compounding profits.

| Business | 2024 metric | Priority |

|---|---|---|

| SME lending | Regional demand; Jiangxi industrial output +6% YoY | Underwriting & RM hires |

| Digital payments | MAU +30% YoY; txns +42% | Reliability & merchant integrations |

| Supply-chain finance | Higher volumes; lower credit loss | Platform & anchor coverage |

What is included in the product

In-depth BCG review of Bank of Jiujiang: quadrant-by-quadrant strategic moves—invest, hold or divest—plus trend-driven risks/opps.

One-page BCG snapshot for Bank of Jiujiang—clarifies portfolio, cuts meeting time and decision friction.

Cash Cows

Core retail and SME deposits

Core retail and SME deposits form the bank’s primary cash cow, comprising roughly 68% of total deposits with 3.5% YoY growth in 2024, reflecting a large, sticky base amid modest market expansion. Low-cost funding has helped sustain NIM near 2.45% and cushions earnings through rate cycles. Maintain service quality and pricing discipline while optimizing analytics to deepen balances without heavy promotional spending.

Payroll and transaction accounts for local corporates

Payroll and transaction accounts for local corporates are mature, high-share relationships with low churn, forming a stable cash cow in 2024. Fee income is predictable and operational costs remain controlled, supporting steady contribution to core revenues. Keep integrations tight and SLAs crisp to protect share; incremental automation completed in 2024 lifts margins further and reduces processing time and error rates.

Prime residential mortgages in established districts

Prime residential mortgages in established districts form a stable book for Bank of Jiujiang, showing low delinquency around 0.5% in 2024 and only modest market growth. Once seasoned they are capital-light and deliver dependable interest income, supporting ROA resilience. Focus on retention at refinance and reducing cost-to-serve; avoid chasing volume and instead milk efficiency gains.

Standard wealth management products

Standard wealth management products are plain-vanilla offerings serving a loyal local client base with moderate growth; distribution is cheap via branch and mobile channels, while tight risk controls and transparent fees sustain high trust. Management should harvest fees, rationalize the product shelf, and avoid bloat to protect margins and client retention.

- Low-cost distribution

- High client loyalty

- Tight compliance

- Fee harvesting

- Product rationalization

Settlement and remittance fees

Settlement and remittance fees are steady cash cows for Bank of Jiujiang, driven by everyday payments with low marginal cost at scale; in China non-cash transaction value topped an estimated 400 trillion yuan in 2024, keeping volumes resilient. Guarded pricing and high reliability sustain margins while incremental UX tweaks (faster confirmations, batch routing) lift usage without big spend. Incremental fee uplift of even 1–2% on core flows materially boosts annual fee income given scale.

- Low marginal cost

- High volume (China non-cash ~400T yuan, 2024)

- Pricing + reliability = margin protection

- Small UX changes → higher engagement

Core deposits and payroll: harvest fees, boost retention, automate UX to lift NIM

Core retail/SME deposits (68% of deposits, +3.5% YoY, NIM ~2.45%), payroll/transaction accounts (low churn), seasoned prime mortgages (delinq ~0.5%), settlement/remittance (China non-cash ~400T yuan) form Bank of Jiujiang’s cash cows; focus on fee harvest, retention, cost-to-serve and minor UX/automation to lift margins.

| Metric | 2024 |

|---|---|

| Core deposits share | 68% |

| Deposit YoY | +3.5% |

| NIM | 2.45% |

| Mortgage delinq | 0.5% |

| Non-cash value (China) | ~400T CNY |

Delivered as Shown

Bank of Jiujiang BCG Matrix

The file you're previewing is the final Bank of Jiujiang BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, ready-to-use strategy report. It reflects precise market analysis and is immediately downloadable post-purchase. Edit, print, or present it with confidence.

Visual. Strategic. Downloadable.

Curious where Bank of Jiujiang’s products sit—Stars, Cash Cows, Dogs or Question Marks? This preview scratches the surface; buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a clear roadmap for reallocating capital and prioritizing growth. Purchase now for a ready-to-use Word report plus an Excel summary that lets your team act fast.

Stars

Local SME lending engine

Local SME lending engine holds a dominant hometown share with demand steady-to-surging as Jiangxi industrial parks scale and provincial industrial output grew about 6% year-on-year in 2024. Continued expansion means loans can compound, but sustaining growth requires continual credit talent and advanced risk tools. Management should keep investing in underwriting and relationship managers to preserve and deepen share. Hold share now to let it mature into a compounding profit base.

Digital payments and settlement in Jiangxi

Digital payments and settlement in Jiangxi have become the de facto rail for many local businesses, showing strong daily usage and rising merchant adoption in 2024 as network effects accelerate. The product attracts scale but burns cash on tech, incentives, and uptime, pressuring margins. Prioritize reliability investments and deeper merchant integrations now. Win the platform game today to mint cash tomorrow.

Government and public-sector banking

Deep ties with local governments and SOE-linked entities give Bank of Jiujiang scale and client stickiness, anchoring core deposit and fee income streams. Transaction volumes rise with regional infrastructure projects and public-services digitization, expanding cash-management and fintech touchpoints. Maintain high service levels and disciplined pricing to protect margins against competitive pressure. A steady government pipeline feeds cross-sell opportunities across the franchise.

Mobile retail banking adoption

Mobile retail banking shows strong traction: monthly active users up ~30% YoY and payment/light-wealth transactions rising ~42% through 2024, but unit economics remain negative as acquisition and feature costs keep CAC above LTV in early cohorts.

Focus on active-user KPIs and structured cross-sell journeys; improving 90-day retention will translate into higher deposits and fee spread over 12–24 months.

- MAU growth ~30% YoY (2024)

- Payments/light-wealth txns +42% (2024)

- High CAC; near-term profitability weak

- Priority: active-user KPIs, cross-sell, retention→deposits/NIM

Supply-chain finance for anchor industries

Supply-chain finance for anchor industries is a Star for Bank of Jiujiang as local manufacturing and logistics anchors deliver steadily growing receivables and predictable cash conversion cycles; high invoice digitalization and platform data give visibility that compresses credit loss experience as volumes ramp. Prioritize investing in onboarding, anchor coverage teams and scalable platforms to capture market share and lock the ecosystem around the bank.

- Anchor-driven receivables: predictable flows

- High data visibility: lower risk, faster underwriting

- Invest: platforms, anchor coverage, fast onboarding

- Scale now: ecosystem lock-in and share gains

Back SME growth: scale underwriting, reliable payments & anchor-led supply-chain profits

SME lending, digital payments and supply-chain finance are Stars: SME loans leverage hometown dominance as Jiangxi industrial output +6% YoY (2024); mobile MAU +30% and payments +42% (2024); supply-chain shows lower loss ratios with rising invoice digitalization. Invest in underwriting, reliability, platforms and anchor coverage to convert share into compounding profits.

| Business | 2024 metric | Priority |

|---|---|---|

| SME lending | Regional demand; Jiangxi industrial output +6% YoY | Underwriting & RM hires |

| Digital payments | MAU +30% YoY; txns +42% | Reliability & merchant integrations |

| Supply-chain finance | Higher volumes; lower credit loss | Platform & anchor coverage |

What is included in the product

In-depth BCG review of Bank of Jiujiang: quadrant-by-quadrant strategic moves—invest, hold or divest—plus trend-driven risks/opps.

One-page BCG snapshot for Bank of Jiujiang—clarifies portfolio, cuts meeting time and decision friction.

Cash Cows

Core retail and SME deposits

Core retail and SME deposits form the bank’s primary cash cow, comprising roughly 68% of total deposits with 3.5% YoY growth in 2024, reflecting a large, sticky base amid modest market expansion. Low-cost funding has helped sustain NIM near 2.45% and cushions earnings through rate cycles. Maintain service quality and pricing discipline while optimizing analytics to deepen balances without heavy promotional spending.

Payroll and transaction accounts for local corporates

Payroll and transaction accounts for local corporates are mature, high-share relationships with low churn, forming a stable cash cow in 2024. Fee income is predictable and operational costs remain controlled, supporting steady contribution to core revenues. Keep integrations tight and SLAs crisp to protect share; incremental automation completed in 2024 lifts margins further and reduces processing time and error rates.

Prime residential mortgages in established districts

Prime residential mortgages in established districts form a stable book for Bank of Jiujiang, showing low delinquency around 0.5% in 2024 and only modest market growth. Once seasoned they are capital-light and deliver dependable interest income, supporting ROA resilience. Focus on retention at refinance and reducing cost-to-serve; avoid chasing volume and instead milk efficiency gains.

Standard wealth management products

Standard wealth management products are plain-vanilla offerings serving a loyal local client base with moderate growth; distribution is cheap via branch and mobile channels, while tight risk controls and transparent fees sustain high trust. Management should harvest fees, rationalize the product shelf, and avoid bloat to protect margins and client retention.

- Low-cost distribution

- High client loyalty

- Tight compliance

- Fee harvesting

- Product rationalization

Settlement and remittance fees

Settlement and remittance fees are steady cash cows for Bank of Jiujiang, driven by everyday payments with low marginal cost at scale; in China non-cash transaction value topped an estimated 400 trillion yuan in 2024, keeping volumes resilient. Guarded pricing and high reliability sustain margins while incremental UX tweaks (faster confirmations, batch routing) lift usage without big spend. Incremental fee uplift of even 1–2% on core flows materially boosts annual fee income given scale.

- Low marginal cost

- High volume (China non-cash ~400T yuan, 2024)

- Pricing + reliability = margin protection

- Small UX changes → higher engagement

Core deposits and payroll: harvest fees, boost retention, automate UX to lift NIM

Core retail/SME deposits (68% of deposits, +3.5% YoY, NIM ~2.45%), payroll/transaction accounts (low churn), seasoned prime mortgages (delinq ~0.5%), settlement/remittance (China non-cash ~400T yuan) form Bank of Jiujiang’s cash cows; focus on fee harvest, retention, cost-to-serve and minor UX/automation to lift margins.

| Metric | 2024 |

|---|---|

| Core deposits share | 68% |

| Deposit YoY | +3.5% |

| NIM | 2.45% |

| Mortgage delinq | 0.5% |

| Non-cash value (China) | ~400T CNY |

Delivered as Shown

Bank of Jiujiang BCG Matrix

The file you're previewing is the final Bank of Jiujiang BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, ready-to-use strategy report. It reflects precise market analysis and is immediately downloadable post-purchase. Edit, print, or present it with confidence.

Description

Visual. Strategic. Downloadable.

Curious where Bank of Jiujiang’s products sit—Stars, Cash Cows, Dogs or Question Marks? This preview scratches the surface; buy the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and a clear roadmap for reallocating capital and prioritizing growth. Purchase now for a ready-to-use Word report plus an Excel summary that lets your team act fast.

Stars

Local SME lending engine

Local SME lending engine holds a dominant hometown share with demand steady-to-surging as Jiangxi industrial parks scale and provincial industrial output grew about 6% year-on-year in 2024. Continued expansion means loans can compound, but sustaining growth requires continual credit talent and advanced risk tools. Management should keep investing in underwriting and relationship managers to preserve and deepen share. Hold share now to let it mature into a compounding profit base.

Digital payments and settlement in Jiangxi

Digital payments and settlement in Jiangxi have become the de facto rail for many local businesses, showing strong daily usage and rising merchant adoption in 2024 as network effects accelerate. The product attracts scale but burns cash on tech, incentives, and uptime, pressuring margins. Prioritize reliability investments and deeper merchant integrations now. Win the platform game today to mint cash tomorrow.

Government and public-sector banking

Deep ties with local governments and SOE-linked entities give Bank of Jiujiang scale and client stickiness, anchoring core deposit and fee income streams. Transaction volumes rise with regional infrastructure projects and public-services digitization, expanding cash-management and fintech touchpoints. Maintain high service levels and disciplined pricing to protect margins against competitive pressure. A steady government pipeline feeds cross-sell opportunities across the franchise.

Mobile retail banking adoption

Mobile retail banking shows strong traction: monthly active users up ~30% YoY and payment/light-wealth transactions rising ~42% through 2024, but unit economics remain negative as acquisition and feature costs keep CAC above LTV in early cohorts.

Focus on active-user KPIs and structured cross-sell journeys; improving 90-day retention will translate into higher deposits and fee spread over 12–24 months.

- MAU growth ~30% YoY (2024)

- Payments/light-wealth txns +42% (2024)

- High CAC; near-term profitability weak

- Priority: active-user KPIs, cross-sell, retention→deposits/NIM

Supply-chain finance for anchor industries

Supply-chain finance for anchor industries is a Star for Bank of Jiujiang as local manufacturing and logistics anchors deliver steadily growing receivables and predictable cash conversion cycles; high invoice digitalization and platform data give visibility that compresses credit loss experience as volumes ramp. Prioritize investing in onboarding, anchor coverage teams and scalable platforms to capture market share and lock the ecosystem around the bank.

- Anchor-driven receivables: predictable flows

- High data visibility: lower risk, faster underwriting

- Invest: platforms, anchor coverage, fast onboarding

- Scale now: ecosystem lock-in and share gains

Back SME growth: scale underwriting, reliable payments & anchor-led supply-chain profits

SME lending, digital payments and supply-chain finance are Stars: SME loans leverage hometown dominance as Jiangxi industrial output +6% YoY (2024); mobile MAU +30% and payments +42% (2024); supply-chain shows lower loss ratios with rising invoice digitalization. Invest in underwriting, reliability, platforms and anchor coverage to convert share into compounding profits.

| Business | 2024 metric | Priority |

|---|---|---|

| SME lending | Regional demand; Jiangxi industrial output +6% YoY | Underwriting & RM hires |

| Digital payments | MAU +30% YoY; txns +42% | Reliability & merchant integrations |

| Supply-chain finance | Higher volumes; lower credit loss | Platform & anchor coverage |

What is included in the product

In-depth BCG review of Bank of Jiujiang: quadrant-by-quadrant strategic moves—invest, hold or divest—plus trend-driven risks/opps.

One-page BCG snapshot for Bank of Jiujiang—clarifies portfolio, cuts meeting time and decision friction.

Cash Cows

Core retail and SME deposits

Core retail and SME deposits form the bank’s primary cash cow, comprising roughly 68% of total deposits with 3.5% YoY growth in 2024, reflecting a large, sticky base amid modest market expansion. Low-cost funding has helped sustain NIM near 2.45% and cushions earnings through rate cycles. Maintain service quality and pricing discipline while optimizing analytics to deepen balances without heavy promotional spending.

Payroll and transaction accounts for local corporates

Payroll and transaction accounts for local corporates are mature, high-share relationships with low churn, forming a stable cash cow in 2024. Fee income is predictable and operational costs remain controlled, supporting steady contribution to core revenues. Keep integrations tight and SLAs crisp to protect share; incremental automation completed in 2024 lifts margins further and reduces processing time and error rates.

Prime residential mortgages in established districts

Prime residential mortgages in established districts form a stable book for Bank of Jiujiang, showing low delinquency around 0.5% in 2024 and only modest market growth. Once seasoned they are capital-light and deliver dependable interest income, supporting ROA resilience. Focus on retention at refinance and reducing cost-to-serve; avoid chasing volume and instead milk efficiency gains.

Standard wealth management products

Standard wealth management products are plain-vanilla offerings serving a loyal local client base with moderate growth; distribution is cheap via branch and mobile channels, while tight risk controls and transparent fees sustain high trust. Management should harvest fees, rationalize the product shelf, and avoid bloat to protect margins and client retention.

- Low-cost distribution

- High client loyalty

- Tight compliance

- Fee harvesting

- Product rationalization

Settlement and remittance fees

Settlement and remittance fees are steady cash cows for Bank of Jiujiang, driven by everyday payments with low marginal cost at scale; in China non-cash transaction value topped an estimated 400 trillion yuan in 2024, keeping volumes resilient. Guarded pricing and high reliability sustain margins while incremental UX tweaks (faster confirmations, batch routing) lift usage without big spend. Incremental fee uplift of even 1–2% on core flows materially boosts annual fee income given scale.

- Low marginal cost

- High volume (China non-cash ~400T yuan, 2024)

- Pricing + reliability = margin protection

- Small UX changes → higher engagement

Core deposits and payroll: harvest fees, boost retention, automate UX to lift NIM

Core retail/SME deposits (68% of deposits, +3.5% YoY, NIM ~2.45%), payroll/transaction accounts (low churn), seasoned prime mortgages (delinq ~0.5%), settlement/remittance (China non-cash ~400T yuan) form Bank of Jiujiang’s cash cows; focus on fee harvest, retention, cost-to-serve and minor UX/automation to lift margins.

| Metric | 2024 |

|---|---|

| Core deposits share | 68% |

| Deposit YoY | +3.5% |

| NIM | 2.45% |

| Mortgage delinq | 0.5% |

| Non-cash value (China) | ~400T CNY |

Delivered as Shown

Bank of Jiujiang BCG Matrix

The file you're previewing is the final Bank of Jiujiang BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just the fully formatted, ready-to-use strategy report. It reflects precise market analysis and is immediately downloadable post-purchase. Edit, print, or present it with confidence.