Bank of India Business Model Canvas

Banking Business Model Canvas: Retail & Corporate Blueprint for Scalability

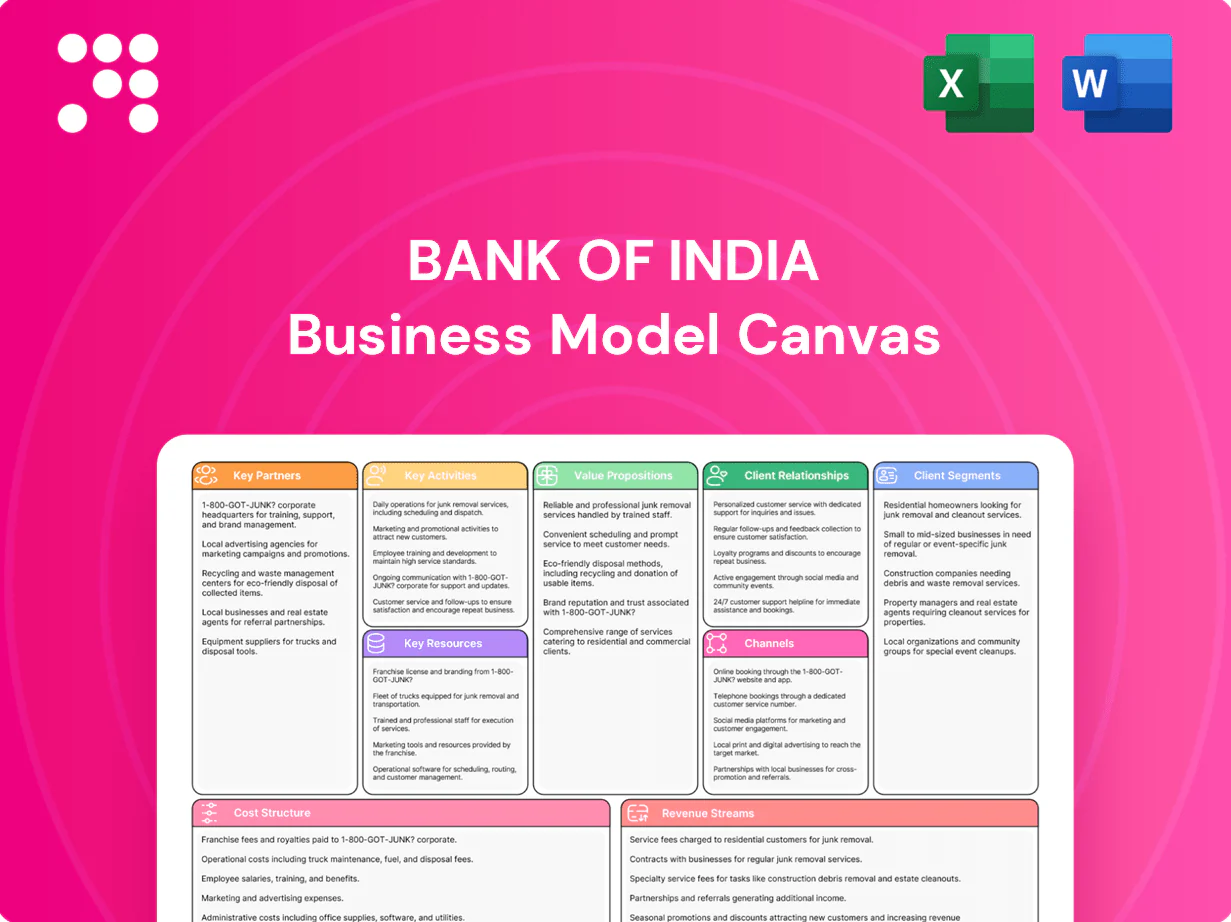

Unlock the full strategic blueprint behind Bank of India's business model. This concise Business Model Canvas maps customer segments, value propositions, channels, revenue streams and cost structure, showing how BOI scales retail and corporate banking across India. Download the full, editable Canvas in Word & Excel to benchmark, plan or pitch with confidence.

Partnerships

Government and Regulators

Partnerships with the RBI, Ministry of Finance and other regulators secure Bank of India’s licensing, access to liquidity windows (LAF, SDF) and policy alignment, with the RBI repo at ~6.50% in 2024. These ties enable participation in 40% priority sector targets and financial inclusion schemes (PMJDY ~460 million accounts by Dec 2024). Regular engagement ensures compliance, risk oversight and access to refinance/guarantee programs (NABARD, SIDBI).

Fintech and Technology Vendors

Alliances with core-banking vendors, cloud and cybersecurity firms and fintechs accelerate Bank of India’s digital roadmap, enabling UPI, eKYC, analytics and AI-driven services; NPCI processed about 104 billion UPI transactions in FY2023-24, underscoring scale. Such partnerships cut time-to-market and boost operational resilience through shared SLAs and cloud failover. Co-creation with fintechs expands customer-centric features cost-effectively while lowering development CAPEX.

Payment Networks and Card Schemes

Bank of India’s partnerships with RuPay, Visa, Mastercard and NPCI enable card issuance and digital payments, with RuPay holding ~60% domestic card market share in 2024 and Visa/Mastercard extending international acceptance. These ties boost security and value-added features like tokenisation and EMV, scale merchant acquiring and QR acceptance across 50+ million merchants, and use shared risk frameworks to cut fraud exposure and improve chargeback controls.

Correspondent and Foreign Banks

Global correspondents support Bank of India’s cross-border payments, trade finance and treasury operations, extending reach in NRI and exporter corridors; India received about 120 billion USD in remittances in 2024 (World Bank), highlighting corridor value. Access to global liquidity and FX products broadens services, while joint due diligence strengthens compliance standards and KYC controls.

- Cross-border payments: expanded corridor coverage

- Trade finance: correspondent-backed instruments

- FX & liquidity: wider product suite

- Compliance: joint due diligence, enhanced KYC

Insurance and Investment Partners

Bancassurance and mutual fund tie-ups expand Bank of India fee income, with bancassurance contributing about 25% of non-interest fees in 2024; customers receive integrated protection, savings and investment solutions that simplify lifecycle planning. Cross-sell lifts wallet share and retention, while shared distribution cuts acquisition cost and boosts economics for both partners.

- 25%: bancassurance share of 2024 fee income

- Integrated protection + investment: one-stop customer offering

- Higher retention via cross-sell

- Shared distribution lowers acquisition costs

Regulatory, UPI and bancassurance ties drive liquidity, scale and fees in 2024

Regulatory ties (RBI repo ~6.50% in 2024) secure licensing, liquidity and priority-sector support (PMJDY ~460M accounts by Dec 2024). Tech and fintech alliances drive UPI/eKYC scale (NPCI ~104B UPI txns FY2023-24) and cloud resilience. Card, correspondent and bancassurance partners (RuPay ~60% card share; remittances ~$120B in 2024; bancassurance ~25% of fee income) expand services and fee pools.

| Partner | Metric (2024) | Impact |

|---|---|---|

| RBI/Finance | Repo ~6.50% | Liquidity & compliance |

| NPCI/UPI | 104B txns FY23-24 | Scale digital payments |

| RuPay | ~60% card share | Domestic acceptance |

| Bancassurance | ~25% fee income | Fee diversification |

What is included in the product

A comprehensive Business Model Canvas for Bank of India detailing all nine blocks—customer segments, value propositions, channels, revenue streams, key resources, activities, partners, cost structure and customer relationships—aligned with real-world banking operations and strategy. Ideal for presentations and investor discussions, it includes competitive advantage analysis and linked SWOT insights to support decision-making and validation.

High-level snapshot that streamlines Bank of India's customer segments, channels, and revenue streams into editable cells to eliminate lengthy structuring—ideal for fast strategy workshops and board reviews.

Activities

Deposit Mobilization

Acquire and manage CASA and term deposits to fund lending, with CASA share around 38% in FY2024 and term-deposit pricing roughly 6.5–7.5% in 2024. Pricing and product design balance growth and cost of funds to protect margins. Relationship programs drive stickiness and higher average balances. Robust liquidity buffers and active ALM ensure stability across cycles.

Lending and Credit Underwriting

Originate retail, MSME, agri and corporate loans across Bank of India’s book (advances ~INR 3.0 lakh crore in FY2024) with robust appraisal including cash-flow underwriting and sector stress tests. Use scorecards, collateral and covenants to price and mitigate risk, keeping GNPA near mid-single digits. Ongoing monitoring, collections and recovery teams sustain asset quality while portfolio analytics and vintage analysis refine credit strategy and provisioning.

Risk, Compliance, and Governance

Bank of India enforces RBI/LCR and Basel-aligned prudential norms and FATF 40-recommendation AML/CFT standards to detect and prevent financial crime. Enterprise risk frameworks cover credit, market and operational risk with ICAAP-driven capital planning informed by stress testing. Quarterly stress tests and ICAAP outcomes guide buffer calibration; continuous internal audit and control uplift enhance resilience.

Digital Banking and Platform Operations

Bank of India builds and operates mobile, internet, UPI and API ecosystems to deliver seamless banking; as of 2024 NPCI reports billions of UPI transactions monthly, underscoring scale. Continuous UX, uptime and cybersecurity improvements reduce friction and breaches; data-driven personalization and machine-learning fraud detection improve conversion and loss prevention. Rapid partner integration via open APIs expands services and time-to-market.

- Build: mobile, internet, UPI, API ecosystems

- Ops: UX, uptime, cybersecurity

- Data: personalization, fraud prevention

- Partners: API-led rapid integration

Treasury, FX, and Trade Services

Treasury, FX, and Trade Services manage liquidity, investments and interest-rate risk across treasury books while offering hedging, remittance and trade-finance solutions to corporates; India merchandise exports were USD 447.46bn in FY2023–24, driving trade volumes and FX flows. The bank optimizes SLR/HTM portfolios within the 18% SLR framework for yield and safety and provides end-to-end support to exporters/importers from pre-shipment finance to post-shipment settlement.

- Liquidity management

- FX hedging & remittance

- Trade finance (pre/post-shipment)

- SLR/HTM optimization (18% SLR)

CASA ≈38% and term deposits 6.5–7.5% to protect margins

Fund retail, MSME, agri and corporate lending via CASA (≈38% in FY2024) and term deposits (pricing ~6.5–7.5% in 2024) to protect margins.

Originate and manage advances (~INR 3.0 lakh crore in FY2024) with scorecards, collateral and collections to keep GNPA around mid-single digits.

Operate digital channels (mobile, internet, UPI) and APIs; NPCI reports billions of UPI transactions monthly in 2024.

Treasury optimizes liquidity, SLR (18%) and FX/trade solutions; India exports USD 447.46bn in FY2023–24.

| Metric | 2024 |

|---|---|

| CASA share | ≈38% |

| Advances | INR 3.0L cr |

| Term-deposit pricing | 6.5–7.5% |

| UPI volume | Billions/mo |

| SLR | 18% |

| India exports | USD 447.46bn |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of India Business Model Canvas you’ll receive after purchase. It’s not a mockup or sample; this preview is a direct snapshot of the final, editable file. Upon payment you’ll instantly download the same complete document formatted and ready to use.

Banking Business Model Canvas: Retail & Corporate Blueprint for Scalability

Unlock the full strategic blueprint behind Bank of India's business model. This concise Business Model Canvas maps customer segments, value propositions, channels, revenue streams and cost structure, showing how BOI scales retail and corporate banking across India. Download the full, editable Canvas in Word & Excel to benchmark, plan or pitch with confidence.

Partnerships

Government and Regulators

Partnerships with the RBI, Ministry of Finance and other regulators secure Bank of India’s licensing, access to liquidity windows (LAF, SDF) and policy alignment, with the RBI repo at ~6.50% in 2024. These ties enable participation in 40% priority sector targets and financial inclusion schemes (PMJDY ~460 million accounts by Dec 2024). Regular engagement ensures compliance, risk oversight and access to refinance/guarantee programs (NABARD, SIDBI).

Fintech and Technology Vendors

Alliances with core-banking vendors, cloud and cybersecurity firms and fintechs accelerate Bank of India’s digital roadmap, enabling UPI, eKYC, analytics and AI-driven services; NPCI processed about 104 billion UPI transactions in FY2023-24, underscoring scale. Such partnerships cut time-to-market and boost operational resilience through shared SLAs and cloud failover. Co-creation with fintechs expands customer-centric features cost-effectively while lowering development CAPEX.

Payment Networks and Card Schemes

Bank of India’s partnerships with RuPay, Visa, Mastercard and NPCI enable card issuance and digital payments, with RuPay holding ~60% domestic card market share in 2024 and Visa/Mastercard extending international acceptance. These ties boost security and value-added features like tokenisation and EMV, scale merchant acquiring and QR acceptance across 50+ million merchants, and use shared risk frameworks to cut fraud exposure and improve chargeback controls.

Correspondent and Foreign Banks

Global correspondents support Bank of India’s cross-border payments, trade finance and treasury operations, extending reach in NRI and exporter corridors; India received about 120 billion USD in remittances in 2024 (World Bank), highlighting corridor value. Access to global liquidity and FX products broadens services, while joint due diligence strengthens compliance standards and KYC controls.

- Cross-border payments: expanded corridor coverage

- Trade finance: correspondent-backed instruments

- FX & liquidity: wider product suite

- Compliance: joint due diligence, enhanced KYC

Insurance and Investment Partners

Bancassurance and mutual fund tie-ups expand Bank of India fee income, with bancassurance contributing about 25% of non-interest fees in 2024; customers receive integrated protection, savings and investment solutions that simplify lifecycle planning. Cross-sell lifts wallet share and retention, while shared distribution cuts acquisition cost and boosts economics for both partners.

- 25%: bancassurance share of 2024 fee income

- Integrated protection + investment: one-stop customer offering

- Higher retention via cross-sell

- Shared distribution lowers acquisition costs

Regulatory, UPI and bancassurance ties drive liquidity, scale and fees in 2024

Regulatory ties (RBI repo ~6.50% in 2024) secure licensing, liquidity and priority-sector support (PMJDY ~460M accounts by Dec 2024). Tech and fintech alliances drive UPI/eKYC scale (NPCI ~104B UPI txns FY2023-24) and cloud resilience. Card, correspondent and bancassurance partners (RuPay ~60% card share; remittances ~$120B in 2024; bancassurance ~25% of fee income) expand services and fee pools.

| Partner | Metric (2024) | Impact |

|---|---|---|

| RBI/Finance | Repo ~6.50% | Liquidity & compliance |

| NPCI/UPI | 104B txns FY23-24 | Scale digital payments |

| RuPay | ~60% card share | Domestic acceptance |

| Bancassurance | ~25% fee income | Fee diversification |

What is included in the product

A comprehensive Business Model Canvas for Bank of India detailing all nine blocks—customer segments, value propositions, channels, revenue streams, key resources, activities, partners, cost structure and customer relationships—aligned with real-world banking operations and strategy. Ideal for presentations and investor discussions, it includes competitive advantage analysis and linked SWOT insights to support decision-making and validation.

High-level snapshot that streamlines Bank of India's customer segments, channels, and revenue streams into editable cells to eliminate lengthy structuring—ideal for fast strategy workshops and board reviews.

Activities

Deposit Mobilization

Acquire and manage CASA and term deposits to fund lending, with CASA share around 38% in FY2024 and term-deposit pricing roughly 6.5–7.5% in 2024. Pricing and product design balance growth and cost of funds to protect margins. Relationship programs drive stickiness and higher average balances. Robust liquidity buffers and active ALM ensure stability across cycles.

Lending and Credit Underwriting

Originate retail, MSME, agri and corporate loans across Bank of India’s book (advances ~INR 3.0 lakh crore in FY2024) with robust appraisal including cash-flow underwriting and sector stress tests. Use scorecards, collateral and covenants to price and mitigate risk, keeping GNPA near mid-single digits. Ongoing monitoring, collections and recovery teams sustain asset quality while portfolio analytics and vintage analysis refine credit strategy and provisioning.

Risk, Compliance, and Governance

Bank of India enforces RBI/LCR and Basel-aligned prudential norms and FATF 40-recommendation AML/CFT standards to detect and prevent financial crime. Enterprise risk frameworks cover credit, market and operational risk with ICAAP-driven capital planning informed by stress testing. Quarterly stress tests and ICAAP outcomes guide buffer calibration; continuous internal audit and control uplift enhance resilience.

Digital Banking and Platform Operations

Bank of India builds and operates mobile, internet, UPI and API ecosystems to deliver seamless banking; as of 2024 NPCI reports billions of UPI transactions monthly, underscoring scale. Continuous UX, uptime and cybersecurity improvements reduce friction and breaches; data-driven personalization and machine-learning fraud detection improve conversion and loss prevention. Rapid partner integration via open APIs expands services and time-to-market.

- Build: mobile, internet, UPI, API ecosystems

- Ops: UX, uptime, cybersecurity

- Data: personalization, fraud prevention

- Partners: API-led rapid integration

Treasury, FX, and Trade Services

Treasury, FX, and Trade Services manage liquidity, investments and interest-rate risk across treasury books while offering hedging, remittance and trade-finance solutions to corporates; India merchandise exports were USD 447.46bn in FY2023–24, driving trade volumes and FX flows. The bank optimizes SLR/HTM portfolios within the 18% SLR framework for yield and safety and provides end-to-end support to exporters/importers from pre-shipment finance to post-shipment settlement.

- Liquidity management

- FX hedging & remittance

- Trade finance (pre/post-shipment)

- SLR/HTM optimization (18% SLR)

CASA ≈38% and term deposits 6.5–7.5% to protect margins

Fund retail, MSME, agri and corporate lending via CASA (≈38% in FY2024) and term deposits (pricing ~6.5–7.5% in 2024) to protect margins.

Originate and manage advances (~INR 3.0 lakh crore in FY2024) with scorecards, collateral and collections to keep GNPA around mid-single digits.

Operate digital channels (mobile, internet, UPI) and APIs; NPCI reports billions of UPI transactions monthly in 2024.

Treasury optimizes liquidity, SLR (18%) and FX/trade solutions; India exports USD 447.46bn in FY2023–24.

| Metric | 2024 |

|---|---|

| CASA share | ≈38% |

| Advances | INR 3.0L cr |

| Term-deposit pricing | 6.5–7.5% |

| UPI volume | Billions/mo |

| SLR | 18% |

| India exports | USD 447.46bn |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of India Business Model Canvas you’ll receive after purchase. It’s not a mockup or sample; this preview is a direct snapshot of the final, editable file. Upon payment you’ll instantly download the same complete document formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Banking Business Model Canvas: Retail & Corporate Blueprint for Scalability

Unlock the full strategic blueprint behind Bank of India's business model. This concise Business Model Canvas maps customer segments, value propositions, channels, revenue streams and cost structure, showing how BOI scales retail and corporate banking across India. Download the full, editable Canvas in Word & Excel to benchmark, plan or pitch with confidence.

Partnerships

Government and Regulators

Partnerships with the RBI, Ministry of Finance and other regulators secure Bank of India’s licensing, access to liquidity windows (LAF, SDF) and policy alignment, with the RBI repo at ~6.50% in 2024. These ties enable participation in 40% priority sector targets and financial inclusion schemes (PMJDY ~460 million accounts by Dec 2024). Regular engagement ensures compliance, risk oversight and access to refinance/guarantee programs (NABARD, SIDBI).

Fintech and Technology Vendors

Alliances with core-banking vendors, cloud and cybersecurity firms and fintechs accelerate Bank of India’s digital roadmap, enabling UPI, eKYC, analytics and AI-driven services; NPCI processed about 104 billion UPI transactions in FY2023-24, underscoring scale. Such partnerships cut time-to-market and boost operational resilience through shared SLAs and cloud failover. Co-creation with fintechs expands customer-centric features cost-effectively while lowering development CAPEX.

Payment Networks and Card Schemes

Bank of India’s partnerships with RuPay, Visa, Mastercard and NPCI enable card issuance and digital payments, with RuPay holding ~60% domestic card market share in 2024 and Visa/Mastercard extending international acceptance. These ties boost security and value-added features like tokenisation and EMV, scale merchant acquiring and QR acceptance across 50+ million merchants, and use shared risk frameworks to cut fraud exposure and improve chargeback controls.

Correspondent and Foreign Banks

Global correspondents support Bank of India’s cross-border payments, trade finance and treasury operations, extending reach in NRI and exporter corridors; India received about 120 billion USD in remittances in 2024 (World Bank), highlighting corridor value. Access to global liquidity and FX products broadens services, while joint due diligence strengthens compliance standards and KYC controls.

- Cross-border payments: expanded corridor coverage

- Trade finance: correspondent-backed instruments

- FX & liquidity: wider product suite

- Compliance: joint due diligence, enhanced KYC

Insurance and Investment Partners

Bancassurance and mutual fund tie-ups expand Bank of India fee income, with bancassurance contributing about 25% of non-interest fees in 2024; customers receive integrated protection, savings and investment solutions that simplify lifecycle planning. Cross-sell lifts wallet share and retention, while shared distribution cuts acquisition cost and boosts economics for both partners.

- 25%: bancassurance share of 2024 fee income

- Integrated protection + investment: one-stop customer offering

- Higher retention via cross-sell

- Shared distribution lowers acquisition costs

Regulatory, UPI and bancassurance ties drive liquidity, scale and fees in 2024

Regulatory ties (RBI repo ~6.50% in 2024) secure licensing, liquidity and priority-sector support (PMJDY ~460M accounts by Dec 2024). Tech and fintech alliances drive UPI/eKYC scale (NPCI ~104B UPI txns FY2023-24) and cloud resilience. Card, correspondent and bancassurance partners (RuPay ~60% card share; remittances ~$120B in 2024; bancassurance ~25% of fee income) expand services and fee pools.

| Partner | Metric (2024) | Impact |

|---|---|---|

| RBI/Finance | Repo ~6.50% | Liquidity & compliance |

| NPCI/UPI | 104B txns FY23-24 | Scale digital payments |

| RuPay | ~60% card share | Domestic acceptance |

| Bancassurance | ~25% fee income | Fee diversification |

What is included in the product

A comprehensive Business Model Canvas for Bank of India detailing all nine blocks—customer segments, value propositions, channels, revenue streams, key resources, activities, partners, cost structure and customer relationships—aligned with real-world banking operations and strategy. Ideal for presentations and investor discussions, it includes competitive advantage analysis and linked SWOT insights to support decision-making and validation.

High-level snapshot that streamlines Bank of India's customer segments, channels, and revenue streams into editable cells to eliminate lengthy structuring—ideal for fast strategy workshops and board reviews.

Activities

Deposit Mobilization

Acquire and manage CASA and term deposits to fund lending, with CASA share around 38% in FY2024 and term-deposit pricing roughly 6.5–7.5% in 2024. Pricing and product design balance growth and cost of funds to protect margins. Relationship programs drive stickiness and higher average balances. Robust liquidity buffers and active ALM ensure stability across cycles.

Lending and Credit Underwriting

Originate retail, MSME, agri and corporate loans across Bank of India’s book (advances ~INR 3.0 lakh crore in FY2024) with robust appraisal including cash-flow underwriting and sector stress tests. Use scorecards, collateral and covenants to price and mitigate risk, keeping GNPA near mid-single digits. Ongoing monitoring, collections and recovery teams sustain asset quality while portfolio analytics and vintage analysis refine credit strategy and provisioning.

Risk, Compliance, and Governance

Bank of India enforces RBI/LCR and Basel-aligned prudential norms and FATF 40-recommendation AML/CFT standards to detect and prevent financial crime. Enterprise risk frameworks cover credit, market and operational risk with ICAAP-driven capital planning informed by stress testing. Quarterly stress tests and ICAAP outcomes guide buffer calibration; continuous internal audit and control uplift enhance resilience.

Digital Banking and Platform Operations

Bank of India builds and operates mobile, internet, UPI and API ecosystems to deliver seamless banking; as of 2024 NPCI reports billions of UPI transactions monthly, underscoring scale. Continuous UX, uptime and cybersecurity improvements reduce friction and breaches; data-driven personalization and machine-learning fraud detection improve conversion and loss prevention. Rapid partner integration via open APIs expands services and time-to-market.

- Build: mobile, internet, UPI, API ecosystems

- Ops: UX, uptime, cybersecurity

- Data: personalization, fraud prevention

- Partners: API-led rapid integration

Treasury, FX, and Trade Services

Treasury, FX, and Trade Services manage liquidity, investments and interest-rate risk across treasury books while offering hedging, remittance and trade-finance solutions to corporates; India merchandise exports were USD 447.46bn in FY2023–24, driving trade volumes and FX flows. The bank optimizes SLR/HTM portfolios within the 18% SLR framework for yield and safety and provides end-to-end support to exporters/importers from pre-shipment finance to post-shipment settlement.

- Liquidity management

- FX hedging & remittance

- Trade finance (pre/post-shipment)

- SLR/HTM optimization (18% SLR)

CASA ≈38% and term deposits 6.5–7.5% to protect margins

Fund retail, MSME, agri and corporate lending via CASA (≈38% in FY2024) and term deposits (pricing ~6.5–7.5% in 2024) to protect margins.

Originate and manage advances (~INR 3.0 lakh crore in FY2024) with scorecards, collateral and collections to keep GNPA around mid-single digits.

Operate digital channels (mobile, internet, UPI) and APIs; NPCI reports billions of UPI transactions monthly in 2024.

Treasury optimizes liquidity, SLR (18%) and FX/trade solutions; India exports USD 447.46bn in FY2023–24.

| Metric | 2024 |

|---|---|

| CASA share | ≈38% |

| Advances | INR 3.0L cr |

| Term-deposit pricing | 6.5–7.5% |

| UPI volume | Billions/mo |

| SLR | 18% |

| India exports | USD 447.46bn |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Bank of India Business Model Canvas you’ll receive after purchase. It’s not a mockup or sample; this preview is a direct snapshot of the final, editable file. Upon payment you’ll instantly download the same complete document formatted and ready to use.