Bank Of Ireland Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

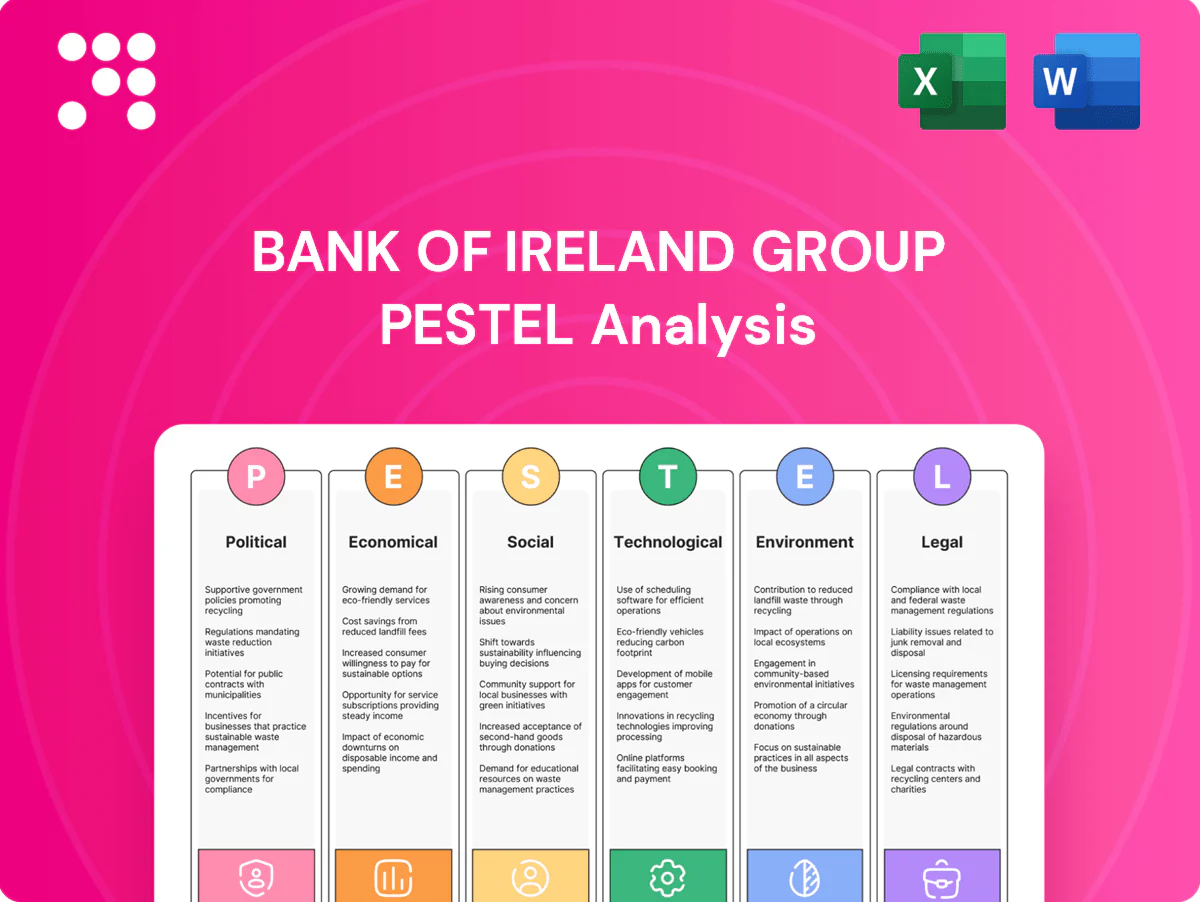

Sharpen your strategy with our PESTLE Analysis of Bank of Ireland Group—concise, current, and focused on political, economic, social, technological, legal and environmental drivers shaping performance. Ideal for investors and strategists, it highlights risks and growth levers. Buy the full report for detailed insights and actionable recommendations.

Political factors

EU and Irish policy direction

Bank of Ireland operates within Ireland’s pro-EU policy framework and the EU Banking Union, with the SSM supervising significant banks that represent roughly 80% of euro-area banking assets, raising coordinated capital and liquidity expectations. EU and Irish policy emphasis on financial stability can tighten capital buffers and liquidity rules, while supportive measures—including Ireland’s housing drive (target ~300,000 homes by 2030) and SME initiatives—can boost loan demand. Shifts in EU leadership or fiscal rules could change macro tailwinds and funding costs rapidly.

UK political and regulatory landscape

Post-Brexit PRA/FCA divergence and ring-fencing rules (implemented 2019) complicate UK retail operations and compliance costs; PRA guidance continues to diverge on liquidity and recovery planning. Election cycles (general election 2024) and fiscal shifts drive mortgage demand and consumer confidence. The Windsor Framework (Feb 2023) eased some NI trade frictions but Northern Ireland remains politically sensitive; political stability feeds sterling volatility and cross-border risk management.

Housing and affordability agenda

Irish government target of c.33,000 homes pa under Housing for All and ongoing planning reforms and subsidy schemes shape mortgage growth and credit mix by shifting demand toward new-build lending and construction finance. Political pressure to boost supply supports developer exposure while tighter rental rules and landlord incentives compress buy-to-let returns. Macroprudential measures remain politically salient amid affordability concerns; abrupt policy shocks could quickly reprice mortgage risk.

Geopolitical risk and sanctions

EU/UK/US sanctions on Russia and other jurisdictions have expanded since 2022, increasing counterparty screening and cross-border compliance complexity for Bank of Ireland; geopolitical tensions have driven market volatility (VIX spiking above 30 in 2022), pressuring treasury income and widening funding spreads. Energy-security policies contributed to euro-area inflation peaking at 10.6% in Oct 2022, altering rate expectations. The bank must maintain strict multi-jurisdictional sanctions adherence to avoid regulatory penalties.

- Sanctions expansion since 2022: higher screening workload

- Market volatility: VIX >30 in 2022, impacts treasury income

- Inflation shock: euro-area 10.6% Oct 2022, shifts rate path

- Regulatory risk: penalties for non-compliance

Public sentiment and scrutiny of banks

Public sentiment and political narratives on bank profitability, fees, and support for vulnerable customers drive heightened oversight of Bank of Ireland, pressuring pricing and disclosure decisions; debates over windfall taxes often resurface when margins widen. Expectations for pass-through of rate cuts or targeted forbearance constrain short-term margin management. Proactive stakeholder engagement reduces regulatory and reputational risk.

- Political scrutiny: fees & profitability

- Windfall-tax risk if margins expand

- Pass-through expectations affect pricing

- Stakeholder engagement mitigates reputational risk

Irish banks confront tighter SSM capital rules, housing-fueled loan growth and margin strain

Bank of Ireland faces tighter capital/liquidity expectations under the SSM (covers ~80% of euro-area banking assets) while Ireland’s housing drive (c.300,000 homes by 2030; ~33,000 pa target) and SME supports lift loan demand. Post-2022 sanctions expansion and elevated market volatility (VIX >30 in 2022) increase compliance and funding-cost risk. Political scrutiny on fees, windfall-tax talk and pass-through expectations constrain margin strategy.

| Metric | Value |

|---|---|

| SSM coverage | ~80% |

| Housing target | ~300,000 by 2030 (~33,000 pa) |

| VIX peak 2022 | >30 |

| Euro-area inflation peak | 10.6% Oct 2022 |

What is included in the product

Explores how macro-environmental forces uniquely affect Bank of Ireland Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed to help executives and investors identify risks, opportunities and forward-looking scenarios for strategic planning.

A compact PESTLE snapshot of Bank of Ireland Group highlighting regulatory, economic, technological and geopolitical impacts for quick risk assessment, slide-ready use and easy team alignment during planning sessions.

Economic factors

Interest rate cycle and margins

ECB deposit rate ~4.00% and BoE bank rate ~5.25% (H1 2025) drive Bank of Ireland Group NIM via deposit betas and asset repricing; higher policy rates boosted NIM in 2023–24 but cuts/easing risk compressing margins while supporting credit quality and loan volumes. Sensitivity hinges on fixed vs variable mortgage mix (Ireland retail book ~60% variable), with treasury hedging and a diversified funding mix (wholesale vs deposits) as key levers.

Irish and UK macro growth

Irish GDP remains volatile due to MNE activity while domestic demand, employment (unemployment around 4–5% in 2024) and wage growth (nominal pay rising mid-single digits) more directly drive household spending and SME credit demand. Domestic indicators such as employment and retail sales therefore matter more for Bank of Ireland credit risk than headline GDP. UK consumer sentiment and retail spending weakness have translated into higher Retail UK impairments and softer card volumes. Divergent Ireland/UK growth can prompt reallocations of capital and risk-weighted exposure across divisions.

Housing market dynamics

Supply shortages in Ireland (target c.33,000 new homes p.a. vs completions ~30,000 in 2024) support prices but strain affordability and tighten LTV/LTI use; UK regional variation—higher arrears risk in weaker northern regions—shapes refinancing behaviour. Construction cost inflation (peaked earlier in decade, still ~4–6% in 2024) raises development lending risk, while policy demand schemes can amplify cycles.

Credit quality and impairment cycles

Stage migration for Bank of Ireland hinges on unemployment (Ireland ~4.7% in 2024) and CPI easing to ~2.6% in 2024, which eases arrears but rate resets (about 45% of mortgages on variable/trackers) remain a watchpoint.

Concentrated exposures in hospitality and SMEs require granular monitoring; supply-chain shocks or local downturns could accelerate stage movement.

Provision overlays (previously rebuilt during 2020–22) may be unwound if macro improves or rebuilt quickly if unemployment or real incomes deteriorate.

- unemployment: 4.7% (2024)

- inflation: 2.6% (2024)

- variable mortgage share: ~45%

- watch: hospitality, SMEs, provision overlays

Funding costs and liquidity

Wholesale spreads, covered bond markets and deposit mix remain key drivers of Bank of Ireland Group cost of funds; ECB deposit rate 4.00% (Jul 2024) tightened market funding dynamics. Legacy TLTRO repayments and the MREL issuance calendar shape near-term liquidity strategy and capital planning. Sterling funding for UK operations adds FX basis and hedging costs while stable retail deposits provide a competitive funding advantage in market stress.

- Wholesale spreads pressure funding margins

- Covered bond market access critical for term funding

- TLTRO legacy and MREL calendar inform liquidity timing

- Sterling funding and stable retail deposits affect FX and resilience

Irish banks confront tighter SSM capital rules, housing-fueled loan growth and margin strain

ECB deposit rate ~4.00% and BoE rate ~5.25% (H1 2025) lift NIM but cuts could compress margins; unemployment Ireland 4.7% (2024) and CPI 2.6% (2024) support credit quality while housing shortfall sustains mortgage demand; variable mortgage share ~60% amplifies rate sensitivity; wholesale spreads, TLTRO repayments and MREL shape funding costs.

| Metric | Value |

|---|---|

| ECB deposit rate | 4.00% (Jul 2024) |

| BoE bank rate | 5.25% (H1 2025) |

| Ireland unemployment | 4.7% (2024) |

| Inflation (CPI) | 2.6% (2024) |

| Variable mortgages | ~60% (Ireland) |

Preview the Actual Deliverable

Bank Of Ireland Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Bank of Ireland Group PESTLE Analysis is the final file you’ll download after payment. No placeholders, no surprises.

Plan Smarter. Present Sharper. Compete Stronger.

Sharpen your strategy with our PESTLE Analysis of Bank of Ireland Group—concise, current, and focused on political, economic, social, technological, legal and environmental drivers shaping performance. Ideal for investors and strategists, it highlights risks and growth levers. Buy the full report for detailed insights and actionable recommendations.

Political factors

EU and Irish policy direction

Bank of Ireland operates within Ireland’s pro-EU policy framework and the EU Banking Union, with the SSM supervising significant banks that represent roughly 80% of euro-area banking assets, raising coordinated capital and liquidity expectations. EU and Irish policy emphasis on financial stability can tighten capital buffers and liquidity rules, while supportive measures—including Ireland’s housing drive (target ~300,000 homes by 2030) and SME initiatives—can boost loan demand. Shifts in EU leadership or fiscal rules could change macro tailwinds and funding costs rapidly.

UK political and regulatory landscape

Post-Brexit PRA/FCA divergence and ring-fencing rules (implemented 2019) complicate UK retail operations and compliance costs; PRA guidance continues to diverge on liquidity and recovery planning. Election cycles (general election 2024) and fiscal shifts drive mortgage demand and consumer confidence. The Windsor Framework (Feb 2023) eased some NI trade frictions but Northern Ireland remains politically sensitive; political stability feeds sterling volatility and cross-border risk management.

Housing and affordability agenda

Irish government target of c.33,000 homes pa under Housing for All and ongoing planning reforms and subsidy schemes shape mortgage growth and credit mix by shifting demand toward new-build lending and construction finance. Political pressure to boost supply supports developer exposure while tighter rental rules and landlord incentives compress buy-to-let returns. Macroprudential measures remain politically salient amid affordability concerns; abrupt policy shocks could quickly reprice mortgage risk.

Geopolitical risk and sanctions

EU/UK/US sanctions on Russia and other jurisdictions have expanded since 2022, increasing counterparty screening and cross-border compliance complexity for Bank of Ireland; geopolitical tensions have driven market volatility (VIX spiking above 30 in 2022), pressuring treasury income and widening funding spreads. Energy-security policies contributed to euro-area inflation peaking at 10.6% in Oct 2022, altering rate expectations. The bank must maintain strict multi-jurisdictional sanctions adherence to avoid regulatory penalties.

- Sanctions expansion since 2022: higher screening workload

- Market volatility: VIX >30 in 2022, impacts treasury income

- Inflation shock: euro-area 10.6% Oct 2022, shifts rate path

- Regulatory risk: penalties for non-compliance

Public sentiment and scrutiny of banks

Public sentiment and political narratives on bank profitability, fees, and support for vulnerable customers drive heightened oversight of Bank of Ireland, pressuring pricing and disclosure decisions; debates over windfall taxes often resurface when margins widen. Expectations for pass-through of rate cuts or targeted forbearance constrain short-term margin management. Proactive stakeholder engagement reduces regulatory and reputational risk.

- Political scrutiny: fees & profitability

- Windfall-tax risk if margins expand

- Pass-through expectations affect pricing

- Stakeholder engagement mitigates reputational risk

Irish banks confront tighter SSM capital rules, housing-fueled loan growth and margin strain

Bank of Ireland faces tighter capital/liquidity expectations under the SSM (covers ~80% of euro-area banking assets) while Ireland’s housing drive (c.300,000 homes by 2030; ~33,000 pa target) and SME supports lift loan demand. Post-2022 sanctions expansion and elevated market volatility (VIX >30 in 2022) increase compliance and funding-cost risk. Political scrutiny on fees, windfall-tax talk and pass-through expectations constrain margin strategy.

| Metric | Value |

|---|---|

| SSM coverage | ~80% |

| Housing target | ~300,000 by 2030 (~33,000 pa) |

| VIX peak 2022 | >30 |

| Euro-area inflation peak | 10.6% Oct 2022 |

What is included in the product

Explores how macro-environmental forces uniquely affect Bank of Ireland Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed to help executives and investors identify risks, opportunities and forward-looking scenarios for strategic planning.

A compact PESTLE snapshot of Bank of Ireland Group highlighting regulatory, economic, technological and geopolitical impacts for quick risk assessment, slide-ready use and easy team alignment during planning sessions.

Economic factors

Interest rate cycle and margins

ECB deposit rate ~4.00% and BoE bank rate ~5.25% (H1 2025) drive Bank of Ireland Group NIM via deposit betas and asset repricing; higher policy rates boosted NIM in 2023–24 but cuts/easing risk compressing margins while supporting credit quality and loan volumes. Sensitivity hinges on fixed vs variable mortgage mix (Ireland retail book ~60% variable), with treasury hedging and a diversified funding mix (wholesale vs deposits) as key levers.

Irish and UK macro growth

Irish GDP remains volatile due to MNE activity while domestic demand, employment (unemployment around 4–5% in 2024) and wage growth (nominal pay rising mid-single digits) more directly drive household spending and SME credit demand. Domestic indicators such as employment and retail sales therefore matter more for Bank of Ireland credit risk than headline GDP. UK consumer sentiment and retail spending weakness have translated into higher Retail UK impairments and softer card volumes. Divergent Ireland/UK growth can prompt reallocations of capital and risk-weighted exposure across divisions.

Housing market dynamics

Supply shortages in Ireland (target c.33,000 new homes p.a. vs completions ~30,000 in 2024) support prices but strain affordability and tighten LTV/LTI use; UK regional variation—higher arrears risk in weaker northern regions—shapes refinancing behaviour. Construction cost inflation (peaked earlier in decade, still ~4–6% in 2024) raises development lending risk, while policy demand schemes can amplify cycles.

Credit quality and impairment cycles

Stage migration for Bank of Ireland hinges on unemployment (Ireland ~4.7% in 2024) and CPI easing to ~2.6% in 2024, which eases arrears but rate resets (about 45% of mortgages on variable/trackers) remain a watchpoint.

Concentrated exposures in hospitality and SMEs require granular monitoring; supply-chain shocks or local downturns could accelerate stage movement.

Provision overlays (previously rebuilt during 2020–22) may be unwound if macro improves or rebuilt quickly if unemployment or real incomes deteriorate.

- unemployment: 4.7% (2024)

- inflation: 2.6% (2024)

- variable mortgage share: ~45%

- watch: hospitality, SMEs, provision overlays

Funding costs and liquidity

Wholesale spreads, covered bond markets and deposit mix remain key drivers of Bank of Ireland Group cost of funds; ECB deposit rate 4.00% (Jul 2024) tightened market funding dynamics. Legacy TLTRO repayments and the MREL issuance calendar shape near-term liquidity strategy and capital planning. Sterling funding for UK operations adds FX basis and hedging costs while stable retail deposits provide a competitive funding advantage in market stress.

- Wholesale spreads pressure funding margins

- Covered bond market access critical for term funding

- TLTRO legacy and MREL calendar inform liquidity timing

- Sterling funding and stable retail deposits affect FX and resilience

Irish banks confront tighter SSM capital rules, housing-fueled loan growth and margin strain

ECB deposit rate ~4.00% and BoE rate ~5.25% (H1 2025) lift NIM but cuts could compress margins; unemployment Ireland 4.7% (2024) and CPI 2.6% (2024) support credit quality while housing shortfall sustains mortgage demand; variable mortgage share ~60% amplifies rate sensitivity; wholesale spreads, TLTRO repayments and MREL shape funding costs.

| Metric | Value |

|---|---|

| ECB deposit rate | 4.00% (Jul 2024) |

| BoE bank rate | 5.25% (H1 2025) |

| Ireland unemployment | 4.7% (2024) |

| Inflation (CPI) | 2.6% (2024) |

| Variable mortgages | ~60% (Ireland) |

Preview the Actual Deliverable

Bank Of Ireland Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Bank of Ireland Group PESTLE Analysis is the final file you’ll download after payment. No placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Sharpen your strategy with our PESTLE Analysis of Bank of Ireland Group—concise, current, and focused on political, economic, social, technological, legal and environmental drivers shaping performance. Ideal for investors and strategists, it highlights risks and growth levers. Buy the full report for detailed insights and actionable recommendations.

Political factors

EU and Irish policy direction

Bank of Ireland operates within Ireland’s pro-EU policy framework and the EU Banking Union, with the SSM supervising significant banks that represent roughly 80% of euro-area banking assets, raising coordinated capital and liquidity expectations. EU and Irish policy emphasis on financial stability can tighten capital buffers and liquidity rules, while supportive measures—including Ireland’s housing drive (target ~300,000 homes by 2030) and SME initiatives—can boost loan demand. Shifts in EU leadership or fiscal rules could change macro tailwinds and funding costs rapidly.

UK political and regulatory landscape

Post-Brexit PRA/FCA divergence and ring-fencing rules (implemented 2019) complicate UK retail operations and compliance costs; PRA guidance continues to diverge on liquidity and recovery planning. Election cycles (general election 2024) and fiscal shifts drive mortgage demand and consumer confidence. The Windsor Framework (Feb 2023) eased some NI trade frictions but Northern Ireland remains politically sensitive; political stability feeds sterling volatility and cross-border risk management.

Housing and affordability agenda

Irish government target of c.33,000 homes pa under Housing for All and ongoing planning reforms and subsidy schemes shape mortgage growth and credit mix by shifting demand toward new-build lending and construction finance. Political pressure to boost supply supports developer exposure while tighter rental rules and landlord incentives compress buy-to-let returns. Macroprudential measures remain politically salient amid affordability concerns; abrupt policy shocks could quickly reprice mortgage risk.

Geopolitical risk and sanctions

EU/UK/US sanctions on Russia and other jurisdictions have expanded since 2022, increasing counterparty screening and cross-border compliance complexity for Bank of Ireland; geopolitical tensions have driven market volatility (VIX spiking above 30 in 2022), pressuring treasury income and widening funding spreads. Energy-security policies contributed to euro-area inflation peaking at 10.6% in Oct 2022, altering rate expectations. The bank must maintain strict multi-jurisdictional sanctions adherence to avoid regulatory penalties.

- Sanctions expansion since 2022: higher screening workload

- Market volatility: VIX >30 in 2022, impacts treasury income

- Inflation shock: euro-area 10.6% Oct 2022, shifts rate path

- Regulatory risk: penalties for non-compliance

Public sentiment and scrutiny of banks

Public sentiment and political narratives on bank profitability, fees, and support for vulnerable customers drive heightened oversight of Bank of Ireland, pressuring pricing and disclosure decisions; debates over windfall taxes often resurface when margins widen. Expectations for pass-through of rate cuts or targeted forbearance constrain short-term margin management. Proactive stakeholder engagement reduces regulatory and reputational risk.

- Political scrutiny: fees & profitability

- Windfall-tax risk if margins expand

- Pass-through expectations affect pricing

- Stakeholder engagement mitigates reputational risk

Irish banks confront tighter SSM capital rules, housing-fueled loan growth and margin strain

Bank of Ireland faces tighter capital/liquidity expectations under the SSM (covers ~80% of euro-area banking assets) while Ireland’s housing drive (c.300,000 homes by 2030; ~33,000 pa target) and SME supports lift loan demand. Post-2022 sanctions expansion and elevated market volatility (VIX >30 in 2022) increase compliance and funding-cost risk. Political scrutiny on fees, windfall-tax talk and pass-through expectations constrain margin strategy.

| Metric | Value |

|---|---|

| SSM coverage | ~80% |

| Housing target | ~300,000 by 2030 (~33,000 pa) |

| VIX peak 2022 | >30 |

| Euro-area inflation peak | 10.6% Oct 2022 |

What is included in the product

Explores how macro-environmental forces uniquely affect Bank of Ireland Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed to help executives and investors identify risks, opportunities and forward-looking scenarios for strategic planning.

A compact PESTLE snapshot of Bank of Ireland Group highlighting regulatory, economic, technological and geopolitical impacts for quick risk assessment, slide-ready use and easy team alignment during planning sessions.

Economic factors

Interest rate cycle and margins

ECB deposit rate ~4.00% and BoE bank rate ~5.25% (H1 2025) drive Bank of Ireland Group NIM via deposit betas and asset repricing; higher policy rates boosted NIM in 2023–24 but cuts/easing risk compressing margins while supporting credit quality and loan volumes. Sensitivity hinges on fixed vs variable mortgage mix (Ireland retail book ~60% variable), with treasury hedging and a diversified funding mix (wholesale vs deposits) as key levers.

Irish and UK macro growth

Irish GDP remains volatile due to MNE activity while domestic demand, employment (unemployment around 4–5% in 2024) and wage growth (nominal pay rising mid-single digits) more directly drive household spending and SME credit demand. Domestic indicators such as employment and retail sales therefore matter more for Bank of Ireland credit risk than headline GDP. UK consumer sentiment and retail spending weakness have translated into higher Retail UK impairments and softer card volumes. Divergent Ireland/UK growth can prompt reallocations of capital and risk-weighted exposure across divisions.

Housing market dynamics

Supply shortages in Ireland (target c.33,000 new homes p.a. vs completions ~30,000 in 2024) support prices but strain affordability and tighten LTV/LTI use; UK regional variation—higher arrears risk in weaker northern regions—shapes refinancing behaviour. Construction cost inflation (peaked earlier in decade, still ~4–6% in 2024) raises development lending risk, while policy demand schemes can amplify cycles.

Credit quality and impairment cycles

Stage migration for Bank of Ireland hinges on unemployment (Ireland ~4.7% in 2024) and CPI easing to ~2.6% in 2024, which eases arrears but rate resets (about 45% of mortgages on variable/trackers) remain a watchpoint.

Concentrated exposures in hospitality and SMEs require granular monitoring; supply-chain shocks or local downturns could accelerate stage movement.

Provision overlays (previously rebuilt during 2020–22) may be unwound if macro improves or rebuilt quickly if unemployment or real incomes deteriorate.

- unemployment: 4.7% (2024)

- inflation: 2.6% (2024)

- variable mortgage share: ~45%

- watch: hospitality, SMEs, provision overlays

Funding costs and liquidity

Wholesale spreads, covered bond markets and deposit mix remain key drivers of Bank of Ireland Group cost of funds; ECB deposit rate 4.00% (Jul 2024) tightened market funding dynamics. Legacy TLTRO repayments and the MREL issuance calendar shape near-term liquidity strategy and capital planning. Sterling funding for UK operations adds FX basis and hedging costs while stable retail deposits provide a competitive funding advantage in market stress.

- Wholesale spreads pressure funding margins

- Covered bond market access critical for term funding

- TLTRO legacy and MREL calendar inform liquidity timing

- Sterling funding and stable retail deposits affect FX and resilience

Irish banks confront tighter SSM capital rules, housing-fueled loan growth and margin strain

ECB deposit rate ~4.00% and BoE rate ~5.25% (H1 2025) lift NIM but cuts could compress margins; unemployment Ireland 4.7% (2024) and CPI 2.6% (2024) support credit quality while housing shortfall sustains mortgage demand; variable mortgage share ~60% amplifies rate sensitivity; wholesale spreads, TLTRO repayments and MREL shape funding costs.

| Metric | Value |

|---|---|

| ECB deposit rate | 4.00% (Jul 2024) |

| BoE bank rate | 5.25% (H1 2025) |

| Ireland unemployment | 4.7% (2024) |

| Inflation (CPI) | 2.6% (2024) |

| Variable mortgages | ~60% (Ireland) |

Preview the Actual Deliverable

Bank Of Ireland Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Bank of Ireland Group PESTLE Analysis is the final file you’ll download after payment. No placeholders, no surprises.