Bank of Lanzhou Boston Consulting Group Matrix

See the Bigger Picture

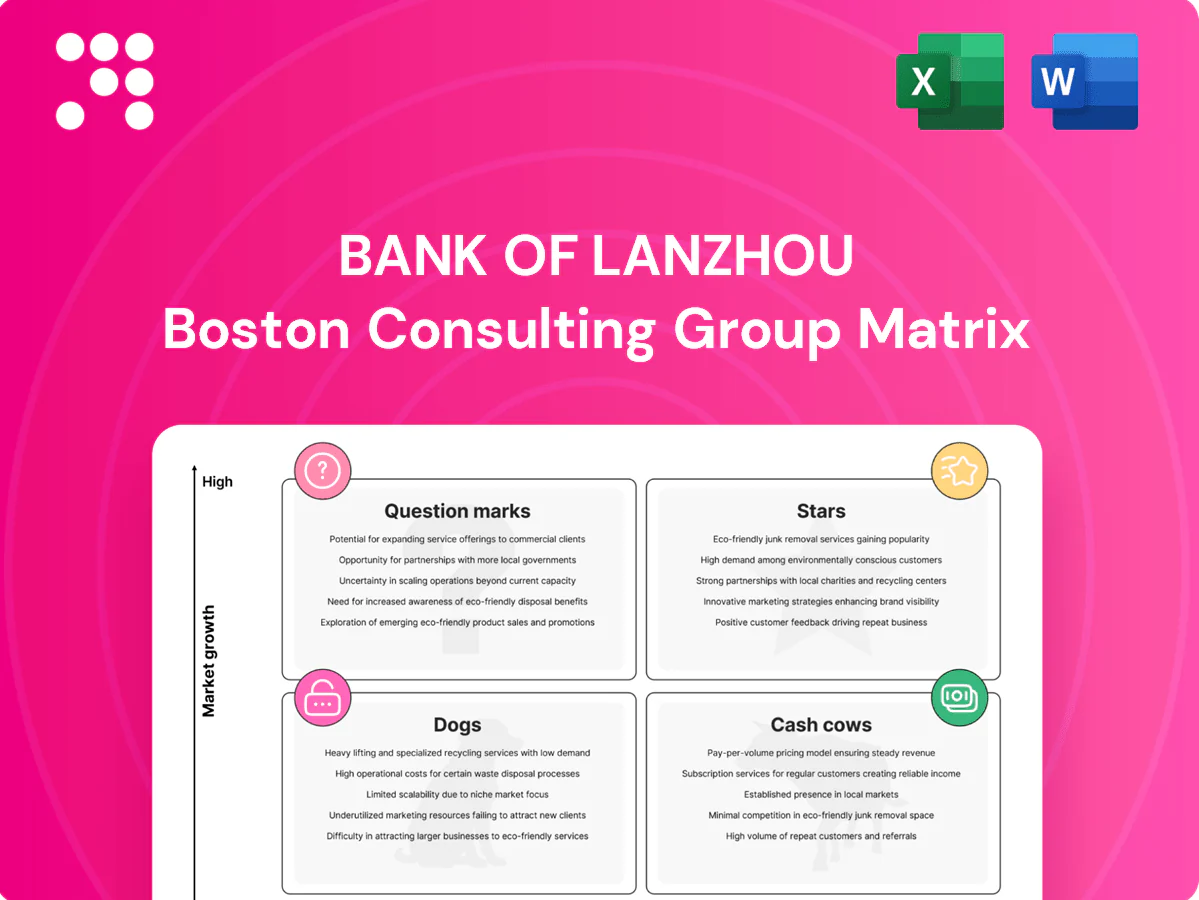

Curious where Bank of Lanzhou’s services land—Stars, Cash Cows, Dogs or Question Marks? This concise preview hints at strengths and drains, but the full BCG Matrix gives you quadrant-by-quadrant placement, data-backed recommendations and a clean roadmap for capital allocation. Buy the complete report for a ready-to-use Word analysis plus a high-level Excel summary and start making sharper product and investment decisions today.

Stars

Digital retail banking in Gansu

Mobile-first accounts, QR payments and app-based lending are grabbing share fast in Gansu as China surpassed 1 billion mobile payment users in 2024 and QR payments account for over 90% of transactions; Bank of Lanzhou’s regional brand drives trust and rising DAU. Growth is high and marketing spend is heavy, but unit economics improve with scale; keep investing in UX, data underwriting and merchant acceptance to lock the lead.

SME lending to core local industries

Serving Gansu’s traders, niche manufacturers and service SMEs is Bank of Lanzhou’s home turf: SMEs account for over 60% of China’s GDP and ~80% of urban employment, underpinning steady deal flow, solid margins and rich cross-sell (payments, payroll, FX-lite).

Portfolio growth is strong as the local economy formalizes; the bank should double down on risk analytics and sector expertise to defend and expand share in core industries.

Transaction banking for local SOEs and public entities

Transaction banking with municipal bodies and local SOEs delivers sticky cash management, collections, and settlement flows that drive high share and elevated switching costs; daily balances in 2024 continued to underpin low-cost funding, representing a substantial portion of deposit liquidity. Growth correlates with regional infrastructure pipelines and 2024 digitization mandates from regulators. Priorities: expand APIs, straight-through reconciliation, and tighten SLAs to protect volumes.

Inclusive finance and micro–small business programs

Inclusive finance and micro–small business programs are a Star for Bank of Lanzhou: in 2024 provincial policy accelerated policy-backed credit to micro and sole-proprietor clients, with government guidance and risk-sharing tools enabling rapid scale while absorbing capital and operations capacity today to build deposit and loyalty pools tomorrow.

- Scale: policy-backed credit expansion (2024)

- Governance: government guidance + risk-sharing tools

- Cost: higher capital and ops now, future deposit loyalty gains

- Action: invest in digital onboarding and alternative-data scoring

Local infrastructure and public–private project finance

Pipeline in urban renewal, transport and utilities remains active, lifting fee and interest income; the bank’s proximity to project sponsors gives clear origination and monitoring advantages. Growth is robust but capital-intensive, requiring disciplined risk limits and proactive syndication to manage sector and single-borrower concentration. Maintain strict covenant enforcement and portfolio stress-testing.

- Origination edge

- Fee & interest lift

- Capital-intensive

- Discipline & syndication

Mobile banking wins: 1B users, >90% QR power SME growth

Bank of Lanzhou is a Star: mobile-first banking captures share as China exceeded 1 billion mobile payment users in 2024 and QR payments exceed 90%, driving DAU and scale economies; SME focus taps a market where SMEs deliver >60% of GDP and ~80% of urban employment. Policy-backed microcredit expansion in 2024 boosts volumes but raises near-term capital and ops costs; invest in UX, data underwriting and APIs to lock leadership.

| Metric | 2024 |

|---|---|

| China mobile payment users | 1 billion |

| QR payments share | >90% |

| SME GDP contribution | >60% |

| SME urban employment | ~80% |

What is included in the product

Concise BCG review of Bank of Lanzhou: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment and divestment guidance.

One-page BCG matrix for Bank of Lanzhou that pinpoints portfolio pain points and guides quick resource shifts.

Cash Cows

Core retail deposits (DDAs and savings)

Core retail deposits (DDAs and savings) provide Bank of Lanzhou with stable, low-cost household funding that anchors NIM and cushions interest-rate volatility. Growth is modest but balances are durable and service costs are low, supporting profitable margin management. These deposits bankroll selective expansion into higher-yield loans and fee businesses. Keeping churn low via simple bundles and fair rates preserves cost advantage and lifetime value.

Prime residential mortgages

Prime residential mortgages form a seasoned book with predictable cash flows and low loss rates (NPL ~0.3% in 2024) concentrated in core cities, supporting stable net interest income. Market growth is muted (~1%–2% in 2024), but Bank of Lanzhou maintains solid share and efficient servicing costs (~25 bps). Strong LTV-backed collateral and minimal marketing spend reduce capital strain. Optimize pricing and prepayment management (CPR ~12% in 2024) to milk steady income.

Payment and settlement fees for SMEs

Daily payments, POS acquiring and collections deliver steady, low-touch fee income for SMEs, with merchant acquiring fees typically in the 0.2–1% range and predictable daily volumes. Volume is mature and margins are moderate, while retention is high because switching payments providers is inconvenient for clients (industry retention often above 80%). Cross-sell opportunities (cash management, lending) remain viable and can lift wallet share by double digits. Focus operationally on reliability and thin, transparent pricing to protect this cash cow.

Treasury operations for public sector payroll

Treasury operations for public sector payroll generate steady float, fee income, and highly predictable monthly volumes, with entrenched relationships limiting churn. Operating leverage is attractive as back-office systems scale, compressing unit costs and boosting margin contribution. Maintain strict compliance and continuity protocols to defend the cash-cow base and preserve service stickiness.

- Float + fees: steady revenue stream

- Predictable volumes: low volatility

- Entrenched relationships: high retention

- Operating leverage: falling unit costs

- Risks: compliance and business continuity

Anchor corporate lending to long-standing clients

Anchor corporate lending to long-standing clients: large, relationship loans with disciplined structures and collateral deliver steady cash flows; 2024 renewal rates ~75% and ROE near 9% supported by ancillary fees and low loss experience. Minimal acquisition spend (<1% of operating income) preserves margins while covenant strength and pricing grids sustain spreads (~180 bps) and returns.

- renewal rate ~75% (2024)

- roe ~9% (2024)

- acquisition spend <1% OI

- pricing/grid spread ~180 bps

Stable funding from core deposits & prime mortgages — ROE ~9%

Core deposits, prime mortgages, payments and treasury payrolls deliver stable, low-cost funding and predictable fees, anchoring NIM and cash generation. NPLs for mortgages ~0.3% (2024), CPR ~12% and mortgage servicing ~25 bps support steady interest income. Merchant retention >80% and corporate renewal ~75% keep fee and loan cash flows reliable, ROE ~9% with spreads ~180 bps.

| Metric | Value |

|---|---|

| Mortgage NPL | ~0.3% (2024) |

| CPR | ~12% (2024) |

| Servicing cost | ~25 bps |

| Merchant retention | >80% |

| Corporate renewal | ~75% |

| ROE | ~9% (2024) |

| Spread | ~180 bps |

What You See Is What You Get

Bank of Lanzhou BCG Matrix

The Bank of Lanzhou BCG Matrix you're previewing is the exact file you'll get after purchase. No watermarks, no placeholders—just the finished, professionally formatted report. It's ready to download, edit, print, or present to stakeholders. Delivered instantly and designed for strategic clarity, with no hidden changes or surprises.

See the Bigger Picture

Curious where Bank of Lanzhou’s services land—Stars, Cash Cows, Dogs or Question Marks? This concise preview hints at strengths and drains, but the full BCG Matrix gives you quadrant-by-quadrant placement, data-backed recommendations and a clean roadmap for capital allocation. Buy the complete report for a ready-to-use Word analysis plus a high-level Excel summary and start making sharper product and investment decisions today.

Stars

Digital retail banking in Gansu

Mobile-first accounts, QR payments and app-based lending are grabbing share fast in Gansu as China surpassed 1 billion mobile payment users in 2024 and QR payments account for over 90% of transactions; Bank of Lanzhou’s regional brand drives trust and rising DAU. Growth is high and marketing spend is heavy, but unit economics improve with scale; keep investing in UX, data underwriting and merchant acceptance to lock the lead.

SME lending to core local industries

Serving Gansu’s traders, niche manufacturers and service SMEs is Bank of Lanzhou’s home turf: SMEs account for over 60% of China’s GDP and ~80% of urban employment, underpinning steady deal flow, solid margins and rich cross-sell (payments, payroll, FX-lite).

Portfolio growth is strong as the local economy formalizes; the bank should double down on risk analytics and sector expertise to defend and expand share in core industries.

Transaction banking for local SOEs and public entities

Transaction banking with municipal bodies and local SOEs delivers sticky cash management, collections, and settlement flows that drive high share and elevated switching costs; daily balances in 2024 continued to underpin low-cost funding, representing a substantial portion of deposit liquidity. Growth correlates with regional infrastructure pipelines and 2024 digitization mandates from regulators. Priorities: expand APIs, straight-through reconciliation, and tighten SLAs to protect volumes.

Inclusive finance and micro–small business programs

Inclusive finance and micro–small business programs are a Star for Bank of Lanzhou: in 2024 provincial policy accelerated policy-backed credit to micro and sole-proprietor clients, with government guidance and risk-sharing tools enabling rapid scale while absorbing capital and operations capacity today to build deposit and loyalty pools tomorrow.

- Scale: policy-backed credit expansion (2024)

- Governance: government guidance + risk-sharing tools

- Cost: higher capital and ops now, future deposit loyalty gains

- Action: invest in digital onboarding and alternative-data scoring

Local infrastructure and public–private project finance

Pipeline in urban renewal, transport and utilities remains active, lifting fee and interest income; the bank’s proximity to project sponsors gives clear origination and monitoring advantages. Growth is robust but capital-intensive, requiring disciplined risk limits and proactive syndication to manage sector and single-borrower concentration. Maintain strict covenant enforcement and portfolio stress-testing.

- Origination edge

- Fee & interest lift

- Capital-intensive

- Discipline & syndication

Mobile banking wins: 1B users, >90% QR power SME growth

Bank of Lanzhou is a Star: mobile-first banking captures share as China exceeded 1 billion mobile payment users in 2024 and QR payments exceed 90%, driving DAU and scale economies; SME focus taps a market where SMEs deliver >60% of GDP and ~80% of urban employment. Policy-backed microcredit expansion in 2024 boosts volumes but raises near-term capital and ops costs; invest in UX, data underwriting and APIs to lock leadership.

| Metric | 2024 |

|---|---|

| China mobile payment users | 1 billion |

| QR payments share | >90% |

| SME GDP contribution | >60% |

| SME urban employment | ~80% |

What is included in the product

Concise BCG review of Bank of Lanzhou: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment and divestment guidance.

One-page BCG matrix for Bank of Lanzhou that pinpoints portfolio pain points and guides quick resource shifts.

Cash Cows

Core retail deposits (DDAs and savings)

Core retail deposits (DDAs and savings) provide Bank of Lanzhou with stable, low-cost household funding that anchors NIM and cushions interest-rate volatility. Growth is modest but balances are durable and service costs are low, supporting profitable margin management. These deposits bankroll selective expansion into higher-yield loans and fee businesses. Keeping churn low via simple bundles and fair rates preserves cost advantage and lifetime value.

Prime residential mortgages

Prime residential mortgages form a seasoned book with predictable cash flows and low loss rates (NPL ~0.3% in 2024) concentrated in core cities, supporting stable net interest income. Market growth is muted (~1%–2% in 2024), but Bank of Lanzhou maintains solid share and efficient servicing costs (~25 bps). Strong LTV-backed collateral and minimal marketing spend reduce capital strain. Optimize pricing and prepayment management (CPR ~12% in 2024) to milk steady income.

Payment and settlement fees for SMEs

Daily payments, POS acquiring and collections deliver steady, low-touch fee income for SMEs, with merchant acquiring fees typically in the 0.2–1% range and predictable daily volumes. Volume is mature and margins are moderate, while retention is high because switching payments providers is inconvenient for clients (industry retention often above 80%). Cross-sell opportunities (cash management, lending) remain viable and can lift wallet share by double digits. Focus operationally on reliability and thin, transparent pricing to protect this cash cow.

Treasury operations for public sector payroll

Treasury operations for public sector payroll generate steady float, fee income, and highly predictable monthly volumes, with entrenched relationships limiting churn. Operating leverage is attractive as back-office systems scale, compressing unit costs and boosting margin contribution. Maintain strict compliance and continuity protocols to defend the cash-cow base and preserve service stickiness.

- Float + fees: steady revenue stream

- Predictable volumes: low volatility

- Entrenched relationships: high retention

- Operating leverage: falling unit costs

- Risks: compliance and business continuity

Anchor corporate lending to long-standing clients

Anchor corporate lending to long-standing clients: large, relationship loans with disciplined structures and collateral deliver steady cash flows; 2024 renewal rates ~75% and ROE near 9% supported by ancillary fees and low loss experience. Minimal acquisition spend (<1% of operating income) preserves margins while covenant strength and pricing grids sustain spreads (~180 bps) and returns.

- renewal rate ~75% (2024)

- roe ~9% (2024)

- acquisition spend <1% OI

- pricing/grid spread ~180 bps

Stable funding from core deposits & prime mortgages — ROE ~9%

Core deposits, prime mortgages, payments and treasury payrolls deliver stable, low-cost funding and predictable fees, anchoring NIM and cash generation. NPLs for mortgages ~0.3% (2024), CPR ~12% and mortgage servicing ~25 bps support steady interest income. Merchant retention >80% and corporate renewal ~75% keep fee and loan cash flows reliable, ROE ~9% with spreads ~180 bps.

| Metric | Value |

|---|---|

| Mortgage NPL | ~0.3% (2024) |

| CPR | ~12% (2024) |

| Servicing cost | ~25 bps |

| Merchant retention | >80% |

| Corporate renewal | ~75% |

| ROE | ~9% (2024) |

| Spread | ~180 bps |

What You See Is What You Get

Bank of Lanzhou BCG Matrix

The Bank of Lanzhou BCG Matrix you're previewing is the exact file you'll get after purchase. No watermarks, no placeholders—just the finished, professionally formatted report. It's ready to download, edit, print, or present to stakeholders. Delivered instantly and designed for strategic clarity, with no hidden changes or surprises.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Curious where Bank of Lanzhou’s services land—Stars, Cash Cows, Dogs or Question Marks? This concise preview hints at strengths and drains, but the full BCG Matrix gives you quadrant-by-quadrant placement, data-backed recommendations and a clean roadmap for capital allocation. Buy the complete report for a ready-to-use Word analysis plus a high-level Excel summary and start making sharper product and investment decisions today.

Stars

Digital retail banking in Gansu

Mobile-first accounts, QR payments and app-based lending are grabbing share fast in Gansu as China surpassed 1 billion mobile payment users in 2024 and QR payments account for over 90% of transactions; Bank of Lanzhou’s regional brand drives trust and rising DAU. Growth is high and marketing spend is heavy, but unit economics improve with scale; keep investing in UX, data underwriting and merchant acceptance to lock the lead.

SME lending to core local industries

Serving Gansu’s traders, niche manufacturers and service SMEs is Bank of Lanzhou’s home turf: SMEs account for over 60% of China’s GDP and ~80% of urban employment, underpinning steady deal flow, solid margins and rich cross-sell (payments, payroll, FX-lite).

Portfolio growth is strong as the local economy formalizes; the bank should double down on risk analytics and sector expertise to defend and expand share in core industries.

Transaction banking for local SOEs and public entities

Transaction banking with municipal bodies and local SOEs delivers sticky cash management, collections, and settlement flows that drive high share and elevated switching costs; daily balances in 2024 continued to underpin low-cost funding, representing a substantial portion of deposit liquidity. Growth correlates with regional infrastructure pipelines and 2024 digitization mandates from regulators. Priorities: expand APIs, straight-through reconciliation, and tighten SLAs to protect volumes.

Inclusive finance and micro–small business programs

Inclusive finance and micro–small business programs are a Star for Bank of Lanzhou: in 2024 provincial policy accelerated policy-backed credit to micro and sole-proprietor clients, with government guidance and risk-sharing tools enabling rapid scale while absorbing capital and operations capacity today to build deposit and loyalty pools tomorrow.

- Scale: policy-backed credit expansion (2024)

- Governance: government guidance + risk-sharing tools

- Cost: higher capital and ops now, future deposit loyalty gains

- Action: invest in digital onboarding and alternative-data scoring

Local infrastructure and public–private project finance

Pipeline in urban renewal, transport and utilities remains active, lifting fee and interest income; the bank’s proximity to project sponsors gives clear origination and monitoring advantages. Growth is robust but capital-intensive, requiring disciplined risk limits and proactive syndication to manage sector and single-borrower concentration. Maintain strict covenant enforcement and portfolio stress-testing.

- Origination edge

- Fee & interest lift

- Capital-intensive

- Discipline & syndication

Mobile banking wins: 1B users, >90% QR power SME growth

Bank of Lanzhou is a Star: mobile-first banking captures share as China exceeded 1 billion mobile payment users in 2024 and QR payments exceed 90%, driving DAU and scale economies; SME focus taps a market where SMEs deliver >60% of GDP and ~80% of urban employment. Policy-backed microcredit expansion in 2024 boosts volumes but raises near-term capital and ops costs; invest in UX, data underwriting and APIs to lock leadership.

| Metric | 2024 |

|---|---|

| China mobile payment users | 1 billion |

| QR payments share | >90% |

| SME GDP contribution | >60% |

| SME urban employment | ~80% |

What is included in the product

Concise BCG review of Bank of Lanzhou: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment and divestment guidance.

One-page BCG matrix for Bank of Lanzhou that pinpoints portfolio pain points and guides quick resource shifts.

Cash Cows

Core retail deposits (DDAs and savings)

Core retail deposits (DDAs and savings) provide Bank of Lanzhou with stable, low-cost household funding that anchors NIM and cushions interest-rate volatility. Growth is modest but balances are durable and service costs are low, supporting profitable margin management. These deposits bankroll selective expansion into higher-yield loans and fee businesses. Keeping churn low via simple bundles and fair rates preserves cost advantage and lifetime value.

Prime residential mortgages

Prime residential mortgages form a seasoned book with predictable cash flows and low loss rates (NPL ~0.3% in 2024) concentrated in core cities, supporting stable net interest income. Market growth is muted (~1%–2% in 2024), but Bank of Lanzhou maintains solid share and efficient servicing costs (~25 bps). Strong LTV-backed collateral and minimal marketing spend reduce capital strain. Optimize pricing and prepayment management (CPR ~12% in 2024) to milk steady income.

Payment and settlement fees for SMEs

Daily payments, POS acquiring and collections deliver steady, low-touch fee income for SMEs, with merchant acquiring fees typically in the 0.2–1% range and predictable daily volumes. Volume is mature and margins are moderate, while retention is high because switching payments providers is inconvenient for clients (industry retention often above 80%). Cross-sell opportunities (cash management, lending) remain viable and can lift wallet share by double digits. Focus operationally on reliability and thin, transparent pricing to protect this cash cow.

Treasury operations for public sector payroll

Treasury operations for public sector payroll generate steady float, fee income, and highly predictable monthly volumes, with entrenched relationships limiting churn. Operating leverage is attractive as back-office systems scale, compressing unit costs and boosting margin contribution. Maintain strict compliance and continuity protocols to defend the cash-cow base and preserve service stickiness.

- Float + fees: steady revenue stream

- Predictable volumes: low volatility

- Entrenched relationships: high retention

- Operating leverage: falling unit costs

- Risks: compliance and business continuity

Anchor corporate lending to long-standing clients

Anchor corporate lending to long-standing clients: large, relationship loans with disciplined structures and collateral deliver steady cash flows; 2024 renewal rates ~75% and ROE near 9% supported by ancillary fees and low loss experience. Minimal acquisition spend (<1% of operating income) preserves margins while covenant strength and pricing grids sustain spreads (~180 bps) and returns.

- renewal rate ~75% (2024)

- roe ~9% (2024)

- acquisition spend <1% OI

- pricing/grid spread ~180 bps

Stable funding from core deposits & prime mortgages — ROE ~9%

Core deposits, prime mortgages, payments and treasury payrolls deliver stable, low-cost funding and predictable fees, anchoring NIM and cash generation. NPLs for mortgages ~0.3% (2024), CPR ~12% and mortgage servicing ~25 bps support steady interest income. Merchant retention >80% and corporate renewal ~75% keep fee and loan cash flows reliable, ROE ~9% with spreads ~180 bps.

| Metric | Value |

|---|---|

| Mortgage NPL | ~0.3% (2024) |

| CPR | ~12% (2024) |

| Servicing cost | ~25 bps |

| Merchant retention | >80% |

| Corporate renewal | ~75% |

| ROE | ~9% (2024) |

| Spread | ~180 bps |

What You See Is What You Get

Bank of Lanzhou BCG Matrix

The Bank of Lanzhou BCG Matrix you're previewing is the exact file you'll get after purchase. No watermarks, no placeholders—just the finished, professionally formatted report. It's ready to download, edit, print, or present to stakeholders. Delivered instantly and designed for strategic clarity, with no hidden changes or surprises.