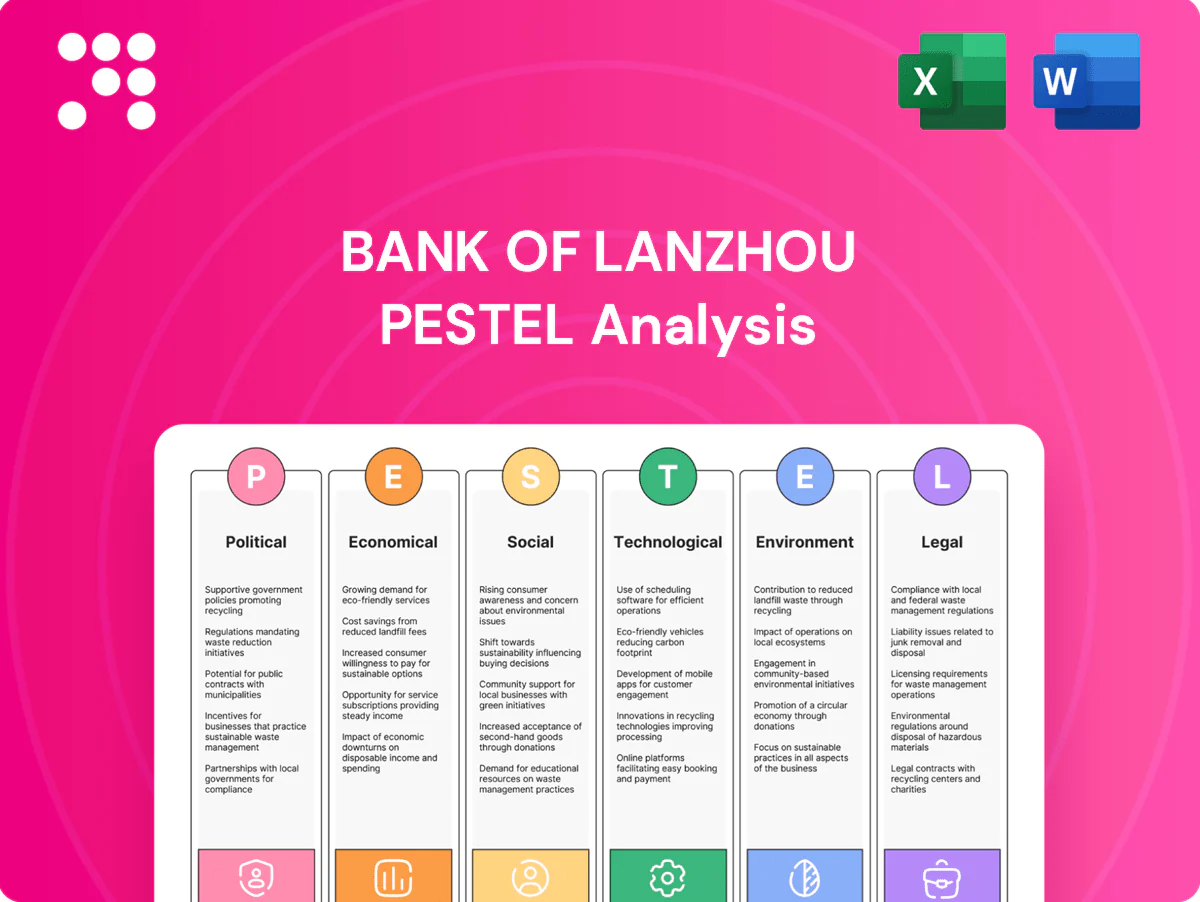

Bank of Lanzhou PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, social changes, technological advances, legal reforms, and environmental risks are reshaping Bank of Lanzhou’s strategic landscape. This concise PESTLE highlights key external drivers and vulnerabilities. Purchase the full analysis to access detailed insights and actionable recommendations for investors and strategists.

Political factors

Central policy steering

As a regional lender Bank of Lanzhou closely follows PBOC/NFRA credit guidance, directing funds to SMEs, agriculture and infrastructure in Gansu in line with Beijing’s 2024 GDP growth target of about 5%. Such policy steering compresses net interest margins but opens policy support, relending windows and targeted RRR relief; sensitivity to window guidance and targeted tools materially shapes short-term loan growth and risk-control metrics.

Local government nexus

Bank of Lanzhou's close alignment with Gansu provincial and municipal priorities channels lending into local development projects, reinforcing its role in regional infrastructure and urbanization efforts. Exposure to LGFVs is material given China's LGFV stock estimated at over RMB 60 trillion by 2024, elevating concentration and rollover risk during fiscal stress. Strong government relationships support deposits and visibility but increase political lending pressures, so balanced governance and strict credit discipline are essential.

Regional development agendas

Western Development and Belt-and-Road initiatives position Lanzhou—a city of about 4.37 million (2020 census)—as a regional logistics and industrial node; China has signed BRI cooperation documents with 149 countries and 32 organizations. Policy projects expand demand for project finance and trade services, but execution hinges on central budget flows and approvals; delays or reprioritization can constrain loan growth and fee income.

Party governance and compliance

Embedded party committees and internal discipline campaigns shape Bank of Lanzhou’s strategic decisions and personnel moves, while anti-corruption drives tighten vendor selection and internal controls; this raises governance standards but adds procedural steps and longer approval timelines. A strong compliance culture has become a competitive necessity for market access and counterparty trust.

- Party oversight influences strategy

- Anti-corruption tightens vendor controls

- More procedures, longer timelines

- Compliance = competitive requirement

Geopolitical spillovers

Geopolitical spillovers: escalating US–China technology controls since 2022 disrupt supply chains and raise default risk for manufacturing and tech borrowers; China–US goods trade was $540.7 billion in 2023, amplifying exposure for export-linked clients. Sanctions risk remains indirect but can strain correspondent banking and FX corridors amid China’s $3.07 trillion FX reserves (end‑2023). Diversifying trade finance counterparties reduces tariff and market-volatility impacts.

- US–China tech controls: supply‑chain disruption

- 2023 China–US goods trade: $540.7B

- Correspondent banking/FX exposure vs sanctions

- Diversify trade‑finance counterparties to mitigate

SME, ag & Gansu infra push for ~5%; LGFV > RMB60 tn

Bank of Lanzhou follows PBOC/NFRA guidance, prioritizing SME, agriculture and Gansu infrastructure to meet Beijing’s ~5% 2024 growth target, compressing NIMs but unlocking relending, RRR relief and targeted support. Heavy LGFV exposure (China LGFV stock >RMB60tn by 2024) raises concentration and rollover risk; strong party oversight and anti-corruption measures lengthen approvals but bolster governance.

| Metric | Value |

|---|---|

| Beijing 2024 GDP target | ~5% |

| China LGFV stock (2024) | >RMB60 tn |

| Lanzhou population (2020) | 4.37M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Bank of Lanzhou, with data-driven trends, region-specific examples and forward-looking insights to help executives and investors identify risks, opportunities and strategic responses.

A concise, PESTLE‑segmented summary of external factors affecting Bank of Lanzhou that can be dropped into presentations, edited with regional or business‑line notes, and easily shared for quick team alignment—ideal for planners and consultants needing clear input on regulatory, economic and market risks.

Economic factors

Gansu macro fundamentals

Gansu's GDP per capita was about 45,000 RMB in 2023, roughly 50% of the national ~90,000 RMB average, constraining household purchasing power and shaping lower-quality credit demand.

SMEs and agriculture drive lending—SME loan exposure exceeds 60%—and carry higher default sensitivity from commodity and seasonal shocks.

Slower income growth limits fee-based wealth revenues; counter-cyclical provisioning and risk-based pricing are essential for Bank of Lanzhou.

Property sector headwinds

National real estate correction—sector historically contributing roughly 25% of GDP when including related industries—depresses collateral values and weakens mortgage appetite. Developer and upstream supplier stress has amplified local credit strains, raising area-specific NPL pressures. Conservative loan-to-value caps (commonly 60–80%) and strict project pre-sale controls are critical. Diversifying toward manufacturing, logistics and services stabilizes asset mix and income streams.

Local government debt risk

LGFV refinancing pressure—amid China's RMB 28 trillion local government special bond stock (end‑2023) and estimated RMB 60 trillion implicit local debt (2024)—raises credit risk and deposit volatility for Bank of Lanzhou as ~20% of LGFV notes face near‑term rollovers. Policy‑led swaps and restructurings can shave near‑term cliffs but lengthen maturities; stricter due diligence on implicit guarantees is required, while exposure caps and annual stress tests protect capital.

Monetary policy and margins

LPR cuts (1Y LPR 3.45% through 2024) and ample liquidity have aided borrowers but compressed Bank of Lanzhou’s net interest margin to roughly 1.8–1.9% in 2024; stronger deposit competition lifted time-deposit funding costs. A strategic shift toward fee income and transaction banking, plus active asset–liability duration management, has helped stabilize NIM.

- LPR 1Y: 3.45% (2024)

- Estimated NIM: 1.8–1.9% (2024)

- Higher time-deposit costs

- Fee income/transaction banking offset

Industrial transition

Gansu’s shift from heavy industry toward renewables, new materials and logistics opens new lending lanes for Bank of Lanzhou as installed wind and solar capacity surpassed 40 GW by 2024, driving project and equipment finance demand. Legacy coal and steel firms face decline and stranded-asset risk, requiring credit re-underwriting to limit losses. Targeted green and supply-chain finance can capture regional growth and support orderly transition.

- renewables: >40 GW capacity (2024)

- risks: stranded assets in coal/steel

- opps: green loans, supply-chain finance

- action: credit re-underwriting

SME, ag & Gansu infra push for ~5%; LGFV > RMB60 tn

Gansu GDP per capita ~45,000 RMB (2023) vs national ~90,000, constraining household demand. SME/agriculture loans >60% exposure, higher default sensitivity. NIM compressed to ~1.8–1.9% (2024) after LPR cuts; fee income and ALM mitigate. Renewables >40 GW (2024) offer new lending; LGFV near‑term rollovers ≈20% raise credit risk.

| Metric | Value |

|---|---|

| Gansu GDP per capita (2023) | 45,000 RMB |

| National avg (2023) | ~90,000 RMB |

| SME loan share | >60% |

| NIM (2024) | 1.8–1.9% |

| Renewables capacity (2024) | >40 GW |

| LGFV near-term rollovers | ~20% |

Same Document Delivered

Bank of Lanzhou PESTLE Analysis

The Bank of Lanzhou PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the final file available for download. No placeholders or teasers—this is the real, professionally structured report you’ll own upon checkout.

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, social changes, technological advances, legal reforms, and environmental risks are reshaping Bank of Lanzhou’s strategic landscape. This concise PESTLE highlights key external drivers and vulnerabilities. Purchase the full analysis to access detailed insights and actionable recommendations for investors and strategists.

Political factors

Central policy steering

As a regional lender Bank of Lanzhou closely follows PBOC/NFRA credit guidance, directing funds to SMEs, agriculture and infrastructure in Gansu in line with Beijing’s 2024 GDP growth target of about 5%. Such policy steering compresses net interest margins but opens policy support, relending windows and targeted RRR relief; sensitivity to window guidance and targeted tools materially shapes short-term loan growth and risk-control metrics.

Local government nexus

Bank of Lanzhou's close alignment with Gansu provincial and municipal priorities channels lending into local development projects, reinforcing its role in regional infrastructure and urbanization efforts. Exposure to LGFVs is material given China's LGFV stock estimated at over RMB 60 trillion by 2024, elevating concentration and rollover risk during fiscal stress. Strong government relationships support deposits and visibility but increase political lending pressures, so balanced governance and strict credit discipline are essential.

Regional development agendas

Western Development and Belt-and-Road initiatives position Lanzhou—a city of about 4.37 million (2020 census)—as a regional logistics and industrial node; China has signed BRI cooperation documents with 149 countries and 32 organizations. Policy projects expand demand for project finance and trade services, but execution hinges on central budget flows and approvals; delays or reprioritization can constrain loan growth and fee income.

Party governance and compliance

Embedded party committees and internal discipline campaigns shape Bank of Lanzhou’s strategic decisions and personnel moves, while anti-corruption drives tighten vendor selection and internal controls; this raises governance standards but adds procedural steps and longer approval timelines. A strong compliance culture has become a competitive necessity for market access and counterparty trust.

- Party oversight influences strategy

- Anti-corruption tightens vendor controls

- More procedures, longer timelines

- Compliance = competitive requirement

Geopolitical spillovers

Geopolitical spillovers: escalating US–China technology controls since 2022 disrupt supply chains and raise default risk for manufacturing and tech borrowers; China–US goods trade was $540.7 billion in 2023, amplifying exposure for export-linked clients. Sanctions risk remains indirect but can strain correspondent banking and FX corridors amid China’s $3.07 trillion FX reserves (end‑2023). Diversifying trade finance counterparties reduces tariff and market-volatility impacts.

- US–China tech controls: supply‑chain disruption

- 2023 China–US goods trade: $540.7B

- Correspondent banking/FX exposure vs sanctions

- Diversify trade‑finance counterparties to mitigate

SME, ag & Gansu infra push for ~5%; LGFV > RMB60 tn

Bank of Lanzhou follows PBOC/NFRA guidance, prioritizing SME, agriculture and Gansu infrastructure to meet Beijing’s ~5% 2024 growth target, compressing NIMs but unlocking relending, RRR relief and targeted support. Heavy LGFV exposure (China LGFV stock >RMB60tn by 2024) raises concentration and rollover risk; strong party oversight and anti-corruption measures lengthen approvals but bolster governance.

| Metric | Value |

|---|---|

| Beijing 2024 GDP target | ~5% |

| China LGFV stock (2024) | >RMB60 tn |

| Lanzhou population (2020) | 4.37M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Bank of Lanzhou, with data-driven trends, region-specific examples and forward-looking insights to help executives and investors identify risks, opportunities and strategic responses.

A concise, PESTLE‑segmented summary of external factors affecting Bank of Lanzhou that can be dropped into presentations, edited with regional or business‑line notes, and easily shared for quick team alignment—ideal for planners and consultants needing clear input on regulatory, economic and market risks.

Economic factors

Gansu macro fundamentals

Gansu's GDP per capita was about 45,000 RMB in 2023, roughly 50% of the national ~90,000 RMB average, constraining household purchasing power and shaping lower-quality credit demand.

SMEs and agriculture drive lending—SME loan exposure exceeds 60%—and carry higher default sensitivity from commodity and seasonal shocks.

Slower income growth limits fee-based wealth revenues; counter-cyclical provisioning and risk-based pricing are essential for Bank of Lanzhou.

Property sector headwinds

National real estate correction—sector historically contributing roughly 25% of GDP when including related industries—depresses collateral values and weakens mortgage appetite. Developer and upstream supplier stress has amplified local credit strains, raising area-specific NPL pressures. Conservative loan-to-value caps (commonly 60–80%) and strict project pre-sale controls are critical. Diversifying toward manufacturing, logistics and services stabilizes asset mix and income streams.

Local government debt risk

LGFV refinancing pressure—amid China's RMB 28 trillion local government special bond stock (end‑2023) and estimated RMB 60 trillion implicit local debt (2024)—raises credit risk and deposit volatility for Bank of Lanzhou as ~20% of LGFV notes face near‑term rollovers. Policy‑led swaps and restructurings can shave near‑term cliffs but lengthen maturities; stricter due diligence on implicit guarantees is required, while exposure caps and annual stress tests protect capital.

Monetary policy and margins

LPR cuts (1Y LPR 3.45% through 2024) and ample liquidity have aided borrowers but compressed Bank of Lanzhou’s net interest margin to roughly 1.8–1.9% in 2024; stronger deposit competition lifted time-deposit funding costs. A strategic shift toward fee income and transaction banking, plus active asset–liability duration management, has helped stabilize NIM.

- LPR 1Y: 3.45% (2024)

- Estimated NIM: 1.8–1.9% (2024)

- Higher time-deposit costs

- Fee income/transaction banking offset

Industrial transition

Gansu’s shift from heavy industry toward renewables, new materials and logistics opens new lending lanes for Bank of Lanzhou as installed wind and solar capacity surpassed 40 GW by 2024, driving project and equipment finance demand. Legacy coal and steel firms face decline and stranded-asset risk, requiring credit re-underwriting to limit losses. Targeted green and supply-chain finance can capture regional growth and support orderly transition.

- renewables: >40 GW capacity (2024)

- risks: stranded assets in coal/steel

- opps: green loans, supply-chain finance

- action: credit re-underwriting

SME, ag & Gansu infra push for ~5%; LGFV > RMB60 tn

Gansu GDP per capita ~45,000 RMB (2023) vs national ~90,000, constraining household demand. SME/agriculture loans >60% exposure, higher default sensitivity. NIM compressed to ~1.8–1.9% (2024) after LPR cuts; fee income and ALM mitigate. Renewables >40 GW (2024) offer new lending; LGFV near‑term rollovers ≈20% raise credit risk.

| Metric | Value |

|---|---|

| Gansu GDP per capita (2023) | 45,000 RMB |

| National avg (2023) | ~90,000 RMB |

| SME loan share | >60% |

| NIM (2024) | 1.8–1.9% |

| Renewables capacity (2024) | >40 GW |

| LGFV near-term rollovers | ~20% |

Same Document Delivered

Bank of Lanzhou PESTLE Analysis

The Bank of Lanzhou PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the final file available for download. No placeholders or teasers—this is the real, professionally structured report you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic trends, social changes, technological advances, legal reforms, and environmental risks are reshaping Bank of Lanzhou’s strategic landscape. This concise PESTLE highlights key external drivers and vulnerabilities. Purchase the full analysis to access detailed insights and actionable recommendations for investors and strategists.

Political factors

Central policy steering

As a regional lender Bank of Lanzhou closely follows PBOC/NFRA credit guidance, directing funds to SMEs, agriculture and infrastructure in Gansu in line with Beijing’s 2024 GDP growth target of about 5%. Such policy steering compresses net interest margins but opens policy support, relending windows and targeted RRR relief; sensitivity to window guidance and targeted tools materially shapes short-term loan growth and risk-control metrics.

Local government nexus

Bank of Lanzhou's close alignment with Gansu provincial and municipal priorities channels lending into local development projects, reinforcing its role in regional infrastructure and urbanization efforts. Exposure to LGFVs is material given China's LGFV stock estimated at over RMB 60 trillion by 2024, elevating concentration and rollover risk during fiscal stress. Strong government relationships support deposits and visibility but increase political lending pressures, so balanced governance and strict credit discipline are essential.

Regional development agendas

Western Development and Belt-and-Road initiatives position Lanzhou—a city of about 4.37 million (2020 census)—as a regional logistics and industrial node; China has signed BRI cooperation documents with 149 countries and 32 organizations. Policy projects expand demand for project finance and trade services, but execution hinges on central budget flows and approvals; delays or reprioritization can constrain loan growth and fee income.

Party governance and compliance

Embedded party committees and internal discipline campaigns shape Bank of Lanzhou’s strategic decisions and personnel moves, while anti-corruption drives tighten vendor selection and internal controls; this raises governance standards but adds procedural steps and longer approval timelines. A strong compliance culture has become a competitive necessity for market access and counterparty trust.

- Party oversight influences strategy

- Anti-corruption tightens vendor controls

- More procedures, longer timelines

- Compliance = competitive requirement

Geopolitical spillovers

Geopolitical spillovers: escalating US–China technology controls since 2022 disrupt supply chains and raise default risk for manufacturing and tech borrowers; China–US goods trade was $540.7 billion in 2023, amplifying exposure for export-linked clients. Sanctions risk remains indirect but can strain correspondent banking and FX corridors amid China’s $3.07 trillion FX reserves (end‑2023). Diversifying trade finance counterparties reduces tariff and market-volatility impacts.

- US–China tech controls: supply‑chain disruption

- 2023 China–US goods trade: $540.7B

- Correspondent banking/FX exposure vs sanctions

- Diversify trade‑finance counterparties to mitigate

SME, ag & Gansu infra push for ~5%; LGFV > RMB60 tn

Bank of Lanzhou follows PBOC/NFRA guidance, prioritizing SME, agriculture and Gansu infrastructure to meet Beijing’s ~5% 2024 growth target, compressing NIMs but unlocking relending, RRR relief and targeted support. Heavy LGFV exposure (China LGFV stock >RMB60tn by 2024) raises concentration and rollover risk; strong party oversight and anti-corruption measures lengthen approvals but bolster governance.

| Metric | Value |

|---|---|

| Beijing 2024 GDP target | ~5% |

| China LGFV stock (2024) | >RMB60 tn |

| Lanzhou population (2020) | 4.37M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Bank of Lanzhou, with data-driven trends, region-specific examples and forward-looking insights to help executives and investors identify risks, opportunities and strategic responses.

A concise, PESTLE‑segmented summary of external factors affecting Bank of Lanzhou that can be dropped into presentations, edited with regional or business‑line notes, and easily shared for quick team alignment—ideal for planners and consultants needing clear input on regulatory, economic and market risks.

Economic factors

Gansu macro fundamentals

Gansu's GDP per capita was about 45,000 RMB in 2023, roughly 50% of the national ~90,000 RMB average, constraining household purchasing power and shaping lower-quality credit demand.

SMEs and agriculture drive lending—SME loan exposure exceeds 60%—and carry higher default sensitivity from commodity and seasonal shocks.

Slower income growth limits fee-based wealth revenues; counter-cyclical provisioning and risk-based pricing are essential for Bank of Lanzhou.

Property sector headwinds

National real estate correction—sector historically contributing roughly 25% of GDP when including related industries—depresses collateral values and weakens mortgage appetite. Developer and upstream supplier stress has amplified local credit strains, raising area-specific NPL pressures. Conservative loan-to-value caps (commonly 60–80%) and strict project pre-sale controls are critical. Diversifying toward manufacturing, logistics and services stabilizes asset mix and income streams.

Local government debt risk

LGFV refinancing pressure—amid China's RMB 28 trillion local government special bond stock (end‑2023) and estimated RMB 60 trillion implicit local debt (2024)—raises credit risk and deposit volatility for Bank of Lanzhou as ~20% of LGFV notes face near‑term rollovers. Policy‑led swaps and restructurings can shave near‑term cliffs but lengthen maturities; stricter due diligence on implicit guarantees is required, while exposure caps and annual stress tests protect capital.

Monetary policy and margins

LPR cuts (1Y LPR 3.45% through 2024) and ample liquidity have aided borrowers but compressed Bank of Lanzhou’s net interest margin to roughly 1.8–1.9% in 2024; stronger deposit competition lifted time-deposit funding costs. A strategic shift toward fee income and transaction banking, plus active asset–liability duration management, has helped stabilize NIM.

- LPR 1Y: 3.45% (2024)

- Estimated NIM: 1.8–1.9% (2024)

- Higher time-deposit costs

- Fee income/transaction banking offset

Industrial transition

Gansu’s shift from heavy industry toward renewables, new materials and logistics opens new lending lanes for Bank of Lanzhou as installed wind and solar capacity surpassed 40 GW by 2024, driving project and equipment finance demand. Legacy coal and steel firms face decline and stranded-asset risk, requiring credit re-underwriting to limit losses. Targeted green and supply-chain finance can capture regional growth and support orderly transition.

- renewables: >40 GW capacity (2024)

- risks: stranded assets in coal/steel

- opps: green loans, supply-chain finance

- action: credit re-underwriting

SME, ag & Gansu infra push for ~5%; LGFV > RMB60 tn

Gansu GDP per capita ~45,000 RMB (2023) vs national ~90,000, constraining household demand. SME/agriculture loans >60% exposure, higher default sensitivity. NIM compressed to ~1.8–1.9% (2024) after LPR cuts; fee income and ALM mitigate. Renewables >40 GW (2024) offer new lending; LGFV near‑term rollovers ≈20% raise credit risk.

| Metric | Value |

|---|---|

| Gansu GDP per capita (2023) | 45,000 RMB |

| National avg (2023) | ~90,000 RMB |

| SME loan share | >60% |

| NIM (2024) | 1.8–1.9% |

| Renewables capacity (2024) | >40 GW |

| LGFV near-term rollovers | ~20% |

Same Document Delivered

Bank of Lanzhou PESTLE Analysis

The Bank of Lanzhou PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the final file available for download. No placeholders or teasers—this is the real, professionally structured report you’ll own upon checkout.