Bank of Maharashtra Boston Consulting Group Matrix

Download Your Competitive Advantage

Curious how Bank of Maharashtra’s businesses stack up—market leaders, cash generators, or underperformers? This snapshot highlights the shifts but the full BCG Matrix gives quadrant-level clarity, data-backed moves, and practical steps to reallocate capital or double down. Buy the complete report for a ready-to-use Word analysis plus an Excel summary you can present to your board. Get it now and turn ambiguity into a clear, actionable strategy.

Stars

Digital payments & UPI lanes

Fast-growing volumes and strong adoption in UPI—handling tens of billions of transactions annually as of 2024—give Bank of Maharashtra real momentum in digital payments and UPI lanes.

The bank leverages public-sector scale and branch reach to gain market share and daily usage advantages in low-cost payment rails.

Promotion and uptime investments remain critical to defend share; sustained capex and marketing can convert this growth engine into a reliable fee-income stream.

Retail deposits (CASA-led)

Sticky low-cost deposits drive a high share in a growing pool: Bank of Maharashtra reported CASA at 45.4% in FY24 with retail deposits up 18% YoY, and widening digital onboarding boosts scale. CASA growth underpins pricing power across loans and fee products, improving NIM resilience. Continuous UX improvements and branch-led activation are required to maintain momentum; holding this lead compounds into a durable competitive advantage.

MSME lending franchise

MSME lending is a Star for Bank of Maharashtra as credit demand in India’s MSME segment is expanding and the bank leverages its nationwide network of over 2,000 branches and deep ties across small-business ecosystems to capture growth.

Its reach, risk know-how, and linkage to government schemes like CGTMSE help gain share, though the portfolio remains capital-intensive and needs sharper underwriting technology.

Priority: invest in digital underwriting and scaling while the MSME market is running to convert reach into profitable share gains.

Home loans in core markets

Home loans in core markets remain a Star as urban and semi-urban housing demand keeps climbing; housing credit grew about 12% YoY in FY2024 (RBI), lifting volumes for lenders including Bank of Maharashtra. Brand trust and PSU credibility drive primaries and balance-transfer wins, while TAT and digital journeys need continued investment. Keep the taps open — current growth is funding the expansion.

- Demand: urban + semi-urban housing up, housing credit ~12% YoY (FY2024)

- Strength: PSU trust wins primaries and transfers

- Weakness: TAT & digital UX require capex

- Strategy: sustain funding — growth self-financing

Government ecosystem flows

Government ecosystem flows — salaries, pensions and collections — are Stars for Bank of Maharashtra as digitization of state services drives large recurring throughput; in 2024 UPI and government e-payments volumes remained buoyant, supporting scale and share. These flows demand continuous integrations and strict SLAs to maintain uptime and reconciliation. Competitors actively target these margins, so BoM must defend relationships and platform reliability.

UPI scale, 45.4% CASA and +18% retail inflows fuel low-cost funding

Bank of Maharashtra’s Stars: UPI/ payments scale (tens of billions TXns in 2024) and CASA strength (45.4% FY24) fuel low-cost funding; retail deposits +18% YoY (FY24). MSME and home loans grow strongly (housing credit ~12% YoY FY24), leveraging 2,000+ branches and CGTMSE linkages; invest in digital underwriting, UX and SLAs to defend share.

| Metric | Value (2024) |

|---|---|

| UPI volumes | tens of billions TXns |

| CASA | 45.4% (FY24) |

| Retail deposits | +18% YoY (FY24) |

| Branches | 2,000+ |

| Housing credit growth | ~12% YoY (FY24) |

What is included in the product

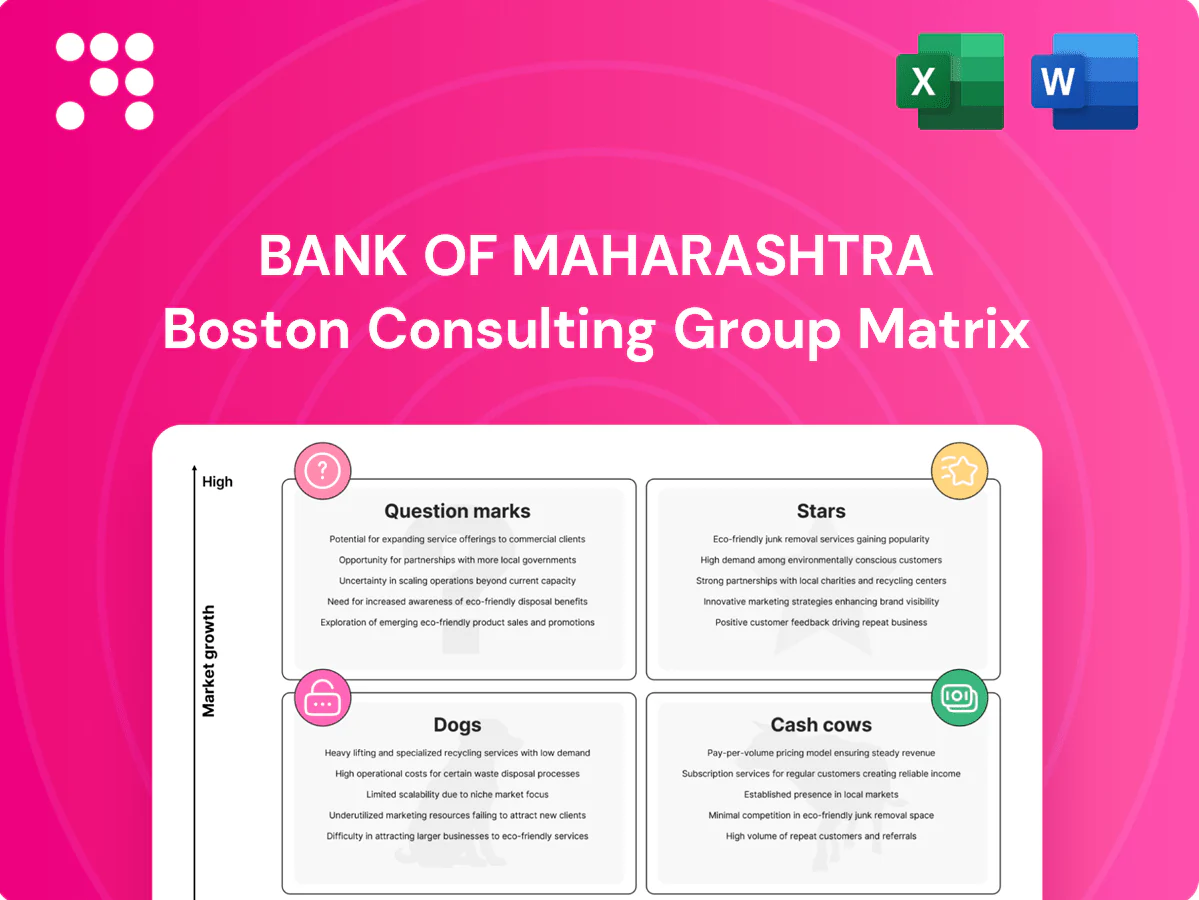

Comprehensive BCG Matrix review of Bank of Maharashtra's business units, with quadrant strategies, investment priorities and competitive risks.

One-page BCG Matrix for Bank of Maharashtra mapping units to ease strategic decisions and resource allocation

Cash Cows

Corporate transaction banking

Corporate transaction banking is a cash cow for Bank of Maharashtra with high share and mature usage, delivering predictable fee streams and stable contribution to non-interest income in FY24. Growth is low but services are sticky once embedded in client operations, reducing churn. Incremental tech upgrades in FY24 improved yields without major capex, so strategy is to milk relationships and quietly upgrade rails to protect margins.

Treasury & SLR book

Core interest income from a seasoned Treasury & SLR book provides stable cash flow for Bank of Maharashtra, anchored by SLR holdings (statutory limit 18% of NDTL) in a stable rate regime. Not flashy, it throws off cash through disciplined duration management amid a 6.5% RBI repo backdrop and 10yr G‑sec near 7.2%. Systems upgrades are squeezing basis points; maintain prudence and harvest steady spread.

Trade finance & guarantees

Trade finance & guarantees sit as a cash cow with established corridors and high repeat-client rates, benefiting from process familiarity across import/export lanes; global trade finance gap stood at about $1.7 trillion in 2023 (ICC), highlighting persistent demand. Growth is moderate, margins decent and risks well-known. Digitization can trim cost-to-serve by roughly 30% (McKinsey 2024). Keep service tight and fees flowing.

Classic savings & term deposits

Classic savings and term deposits form Bank of Maharashtra’s cash cow: with over INR 2 lakh crore in deposits as of March 2024 they deliver predictable, low-churn customer behavior, requiring minimal promotional spend versus acquisition channels; targeted nudges and cross-sells lift lifetime value and allow the deposit base to fund higher-risk growth bets.

- Large base: >INR 2 lakh crore deposits (Mar 2024)

- Low churn: stable retail behavior

- Promo-light: acquisition cost savings

- Growth lever: nudges & cross-sell raise LTV

ATM/branch fee income

ATM/branch fee income for Bank of Maharashtra remains a dependable cash cow: usage is flat to modest but steady, with the bank operating roughly 1,800 branches and about 1,700 ATMs as of March 2024, making network costs largely sunk; small yield tweaks (fee tiers, interchange optimization) raise ROI while digital growth scales core margins.

- Dependable low-volatility income

- Sunk network capex — marginal gains matter

- Keep uptime >99% and fees competitive

- Supports operating costs during digital transition

Large deposit base (>INR 2L cr), trade fees and Treasury yield steady — network keeps margins

Bank of Maharashtra cash cows: deposits (>INR 2 lakh crore, Mar 2024), corporate transaction banking and trade finance deliver stable fees, and Treasury/SLR holdings provide predictable interest cash flow amid a 6.5% repo and 10yr G‑sec ~7.2% (FY24). Network fees (1,800 branches; 1,700 ATMs) and digital nudges sustain margins with low churn and modest growth.

| Metric | Value |

|---|---|

| Total deposits | >INR 2 lakh crore (Mar 2024) |

| Branches / ATMs | 1,800 / 1,700 (Mar 2024) |

| RBI repo / 10yr G‑sec | 6.5% / ~7.2% (FY24) |

| Trade finance context | Global gap ~$1.7tn (2023) |

What You See Is What You Get

Bank of Maharashtra BCG Matrix

The file you're previewing is the exact Bank of Maharashtra BCG Matrix report you'll receive after purchase. No watermarks, no placeholders — just the finalized, fully formatted analysis ready for presentation. Built by strategy professionals with clear visuals and actionable insights, it's downloadable immediately to your inbox. Use it as-is for planning, pitching, or sharing with stakeholders.

Download Your Competitive Advantage

Curious how Bank of Maharashtra’s businesses stack up—market leaders, cash generators, or underperformers? This snapshot highlights the shifts but the full BCG Matrix gives quadrant-level clarity, data-backed moves, and practical steps to reallocate capital or double down. Buy the complete report for a ready-to-use Word analysis plus an Excel summary you can present to your board. Get it now and turn ambiguity into a clear, actionable strategy.

Stars

Digital payments & UPI lanes

Fast-growing volumes and strong adoption in UPI—handling tens of billions of transactions annually as of 2024—give Bank of Maharashtra real momentum in digital payments and UPI lanes.

The bank leverages public-sector scale and branch reach to gain market share and daily usage advantages in low-cost payment rails.

Promotion and uptime investments remain critical to defend share; sustained capex and marketing can convert this growth engine into a reliable fee-income stream.

Retail deposits (CASA-led)

Sticky low-cost deposits drive a high share in a growing pool: Bank of Maharashtra reported CASA at 45.4% in FY24 with retail deposits up 18% YoY, and widening digital onboarding boosts scale. CASA growth underpins pricing power across loans and fee products, improving NIM resilience. Continuous UX improvements and branch-led activation are required to maintain momentum; holding this lead compounds into a durable competitive advantage.

MSME lending franchise

MSME lending is a Star for Bank of Maharashtra as credit demand in India’s MSME segment is expanding and the bank leverages its nationwide network of over 2,000 branches and deep ties across small-business ecosystems to capture growth.

Its reach, risk know-how, and linkage to government schemes like CGTMSE help gain share, though the portfolio remains capital-intensive and needs sharper underwriting technology.

Priority: invest in digital underwriting and scaling while the MSME market is running to convert reach into profitable share gains.

Home loans in core markets

Home loans in core markets remain a Star as urban and semi-urban housing demand keeps climbing; housing credit grew about 12% YoY in FY2024 (RBI), lifting volumes for lenders including Bank of Maharashtra. Brand trust and PSU credibility drive primaries and balance-transfer wins, while TAT and digital journeys need continued investment. Keep the taps open — current growth is funding the expansion.

- Demand: urban + semi-urban housing up, housing credit ~12% YoY (FY2024)

- Strength: PSU trust wins primaries and transfers

- Weakness: TAT & digital UX require capex

- Strategy: sustain funding — growth self-financing

Government ecosystem flows

Government ecosystem flows — salaries, pensions and collections — are Stars for Bank of Maharashtra as digitization of state services drives large recurring throughput; in 2024 UPI and government e-payments volumes remained buoyant, supporting scale and share. These flows demand continuous integrations and strict SLAs to maintain uptime and reconciliation. Competitors actively target these margins, so BoM must defend relationships and platform reliability.

UPI scale, 45.4% CASA and +18% retail inflows fuel low-cost funding

Bank of Maharashtra’s Stars: UPI/ payments scale (tens of billions TXns in 2024) and CASA strength (45.4% FY24) fuel low-cost funding; retail deposits +18% YoY (FY24). MSME and home loans grow strongly (housing credit ~12% YoY FY24), leveraging 2,000+ branches and CGTMSE linkages; invest in digital underwriting, UX and SLAs to defend share.

| Metric | Value (2024) |

|---|---|

| UPI volumes | tens of billions TXns |

| CASA | 45.4% (FY24) |

| Retail deposits | +18% YoY (FY24) |

| Branches | 2,000+ |

| Housing credit growth | ~12% YoY (FY24) |

What is included in the product

Comprehensive BCG Matrix review of Bank of Maharashtra's business units, with quadrant strategies, investment priorities and competitive risks.

One-page BCG Matrix for Bank of Maharashtra mapping units to ease strategic decisions and resource allocation

Cash Cows

Corporate transaction banking

Corporate transaction banking is a cash cow for Bank of Maharashtra with high share and mature usage, delivering predictable fee streams and stable contribution to non-interest income in FY24. Growth is low but services are sticky once embedded in client operations, reducing churn. Incremental tech upgrades in FY24 improved yields without major capex, so strategy is to milk relationships and quietly upgrade rails to protect margins.

Treasury & SLR book

Core interest income from a seasoned Treasury & SLR book provides stable cash flow for Bank of Maharashtra, anchored by SLR holdings (statutory limit 18% of NDTL) in a stable rate regime. Not flashy, it throws off cash through disciplined duration management amid a 6.5% RBI repo backdrop and 10yr G‑sec near 7.2%. Systems upgrades are squeezing basis points; maintain prudence and harvest steady spread.

Trade finance & guarantees

Trade finance & guarantees sit as a cash cow with established corridors and high repeat-client rates, benefiting from process familiarity across import/export lanes; global trade finance gap stood at about $1.7 trillion in 2023 (ICC), highlighting persistent demand. Growth is moderate, margins decent and risks well-known. Digitization can trim cost-to-serve by roughly 30% (McKinsey 2024). Keep service tight and fees flowing.

Classic savings & term deposits

Classic savings and term deposits form Bank of Maharashtra’s cash cow: with over INR 2 lakh crore in deposits as of March 2024 they deliver predictable, low-churn customer behavior, requiring minimal promotional spend versus acquisition channels; targeted nudges and cross-sells lift lifetime value and allow the deposit base to fund higher-risk growth bets.

- Large base: >INR 2 lakh crore deposits (Mar 2024)

- Low churn: stable retail behavior

- Promo-light: acquisition cost savings

- Growth lever: nudges & cross-sell raise LTV

ATM/branch fee income

ATM/branch fee income for Bank of Maharashtra remains a dependable cash cow: usage is flat to modest but steady, with the bank operating roughly 1,800 branches and about 1,700 ATMs as of March 2024, making network costs largely sunk; small yield tweaks (fee tiers, interchange optimization) raise ROI while digital growth scales core margins.

- Dependable low-volatility income

- Sunk network capex — marginal gains matter

- Keep uptime >99% and fees competitive

- Supports operating costs during digital transition

Large deposit base (>INR 2L cr), trade fees and Treasury yield steady — network keeps margins

Bank of Maharashtra cash cows: deposits (>INR 2 lakh crore, Mar 2024), corporate transaction banking and trade finance deliver stable fees, and Treasury/SLR holdings provide predictable interest cash flow amid a 6.5% repo and 10yr G‑sec ~7.2% (FY24). Network fees (1,800 branches; 1,700 ATMs) and digital nudges sustain margins with low churn and modest growth.

| Metric | Value |

|---|---|

| Total deposits | >INR 2 lakh crore (Mar 2024) |

| Branches / ATMs | 1,800 / 1,700 (Mar 2024) |

| RBI repo / 10yr G‑sec | 6.5% / ~7.2% (FY24) |

| Trade finance context | Global gap ~$1.7tn (2023) |

What You See Is What You Get

Bank of Maharashtra BCG Matrix

The file you're previewing is the exact Bank of Maharashtra BCG Matrix report you'll receive after purchase. No watermarks, no placeholders — just the finalized, fully formatted analysis ready for presentation. Built by strategy professionals with clear visuals and actionable insights, it's downloadable immediately to your inbox. Use it as-is for planning, pitching, or sharing with stakeholders.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

Curious how Bank of Maharashtra’s businesses stack up—market leaders, cash generators, or underperformers? This snapshot highlights the shifts but the full BCG Matrix gives quadrant-level clarity, data-backed moves, and practical steps to reallocate capital or double down. Buy the complete report for a ready-to-use Word analysis plus an Excel summary you can present to your board. Get it now and turn ambiguity into a clear, actionable strategy.

Stars

Digital payments & UPI lanes

Fast-growing volumes and strong adoption in UPI—handling tens of billions of transactions annually as of 2024—give Bank of Maharashtra real momentum in digital payments and UPI lanes.

The bank leverages public-sector scale and branch reach to gain market share and daily usage advantages in low-cost payment rails.

Promotion and uptime investments remain critical to defend share; sustained capex and marketing can convert this growth engine into a reliable fee-income stream.

Retail deposits (CASA-led)

Sticky low-cost deposits drive a high share in a growing pool: Bank of Maharashtra reported CASA at 45.4% in FY24 with retail deposits up 18% YoY, and widening digital onboarding boosts scale. CASA growth underpins pricing power across loans and fee products, improving NIM resilience. Continuous UX improvements and branch-led activation are required to maintain momentum; holding this lead compounds into a durable competitive advantage.

MSME lending franchise

MSME lending is a Star for Bank of Maharashtra as credit demand in India’s MSME segment is expanding and the bank leverages its nationwide network of over 2,000 branches and deep ties across small-business ecosystems to capture growth.

Its reach, risk know-how, and linkage to government schemes like CGTMSE help gain share, though the portfolio remains capital-intensive and needs sharper underwriting technology.

Priority: invest in digital underwriting and scaling while the MSME market is running to convert reach into profitable share gains.

Home loans in core markets

Home loans in core markets remain a Star as urban and semi-urban housing demand keeps climbing; housing credit grew about 12% YoY in FY2024 (RBI), lifting volumes for lenders including Bank of Maharashtra. Brand trust and PSU credibility drive primaries and balance-transfer wins, while TAT and digital journeys need continued investment. Keep the taps open — current growth is funding the expansion.

- Demand: urban + semi-urban housing up, housing credit ~12% YoY (FY2024)

- Strength: PSU trust wins primaries and transfers

- Weakness: TAT & digital UX require capex

- Strategy: sustain funding — growth self-financing

Government ecosystem flows

Government ecosystem flows — salaries, pensions and collections — are Stars for Bank of Maharashtra as digitization of state services drives large recurring throughput; in 2024 UPI and government e-payments volumes remained buoyant, supporting scale and share. These flows demand continuous integrations and strict SLAs to maintain uptime and reconciliation. Competitors actively target these margins, so BoM must defend relationships and platform reliability.

UPI scale, 45.4% CASA and +18% retail inflows fuel low-cost funding

Bank of Maharashtra’s Stars: UPI/ payments scale (tens of billions TXns in 2024) and CASA strength (45.4% FY24) fuel low-cost funding; retail deposits +18% YoY (FY24). MSME and home loans grow strongly (housing credit ~12% YoY FY24), leveraging 2,000+ branches and CGTMSE linkages; invest in digital underwriting, UX and SLAs to defend share.

| Metric | Value (2024) |

|---|---|

| UPI volumes | tens of billions TXns |

| CASA | 45.4% (FY24) |

| Retail deposits | +18% YoY (FY24) |

| Branches | 2,000+ |

| Housing credit growth | ~12% YoY (FY24) |

What is included in the product

Comprehensive BCG Matrix review of Bank of Maharashtra's business units, with quadrant strategies, investment priorities and competitive risks.

One-page BCG Matrix for Bank of Maharashtra mapping units to ease strategic decisions and resource allocation

Cash Cows

Corporate transaction banking

Corporate transaction banking is a cash cow for Bank of Maharashtra with high share and mature usage, delivering predictable fee streams and stable contribution to non-interest income in FY24. Growth is low but services are sticky once embedded in client operations, reducing churn. Incremental tech upgrades in FY24 improved yields without major capex, so strategy is to milk relationships and quietly upgrade rails to protect margins.

Treasury & SLR book

Core interest income from a seasoned Treasury & SLR book provides stable cash flow for Bank of Maharashtra, anchored by SLR holdings (statutory limit 18% of NDTL) in a stable rate regime. Not flashy, it throws off cash through disciplined duration management amid a 6.5% RBI repo backdrop and 10yr G‑sec near 7.2%. Systems upgrades are squeezing basis points; maintain prudence and harvest steady spread.

Trade finance & guarantees

Trade finance & guarantees sit as a cash cow with established corridors and high repeat-client rates, benefiting from process familiarity across import/export lanes; global trade finance gap stood at about $1.7 trillion in 2023 (ICC), highlighting persistent demand. Growth is moderate, margins decent and risks well-known. Digitization can trim cost-to-serve by roughly 30% (McKinsey 2024). Keep service tight and fees flowing.

Classic savings & term deposits

Classic savings and term deposits form Bank of Maharashtra’s cash cow: with over INR 2 lakh crore in deposits as of March 2024 they deliver predictable, low-churn customer behavior, requiring minimal promotional spend versus acquisition channels; targeted nudges and cross-sells lift lifetime value and allow the deposit base to fund higher-risk growth bets.

- Large base: >INR 2 lakh crore deposits (Mar 2024)

- Low churn: stable retail behavior

- Promo-light: acquisition cost savings

- Growth lever: nudges & cross-sell raise LTV

ATM/branch fee income

ATM/branch fee income for Bank of Maharashtra remains a dependable cash cow: usage is flat to modest but steady, with the bank operating roughly 1,800 branches and about 1,700 ATMs as of March 2024, making network costs largely sunk; small yield tweaks (fee tiers, interchange optimization) raise ROI while digital growth scales core margins.

- Dependable low-volatility income

- Sunk network capex — marginal gains matter

- Keep uptime >99% and fees competitive

- Supports operating costs during digital transition

Large deposit base (>INR 2L cr), trade fees and Treasury yield steady — network keeps margins

Bank of Maharashtra cash cows: deposits (>INR 2 lakh crore, Mar 2024), corporate transaction banking and trade finance deliver stable fees, and Treasury/SLR holdings provide predictable interest cash flow amid a 6.5% repo and 10yr G‑sec ~7.2% (FY24). Network fees (1,800 branches; 1,700 ATMs) and digital nudges sustain margins with low churn and modest growth.

| Metric | Value |

|---|---|

| Total deposits | >INR 2 lakh crore (Mar 2024) |

| Branches / ATMs | 1,800 / 1,700 (Mar 2024) |

| RBI repo / 10yr G‑sec | 6.5% / ~7.2% (FY24) |

| Trade finance context | Global gap ~$1.7tn (2023) |

What You See Is What You Get

Bank of Maharashtra BCG Matrix

The file you're previewing is the exact Bank of Maharashtra BCG Matrix report you'll receive after purchase. No watermarks, no placeholders — just the finalized, fully formatted analysis ready for presentation. Built by strategy professionals with clear visuals and actionable insights, it's downloadable immediately to your inbox. Use it as-is for planning, pitching, or sharing with stakeholders.