Bank of Maharashtra Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Bank of Maharashtra faces moderate buyer power, intense regulatory scrutiny, and rising fintech substitution, while its branch network and PSU backing bolster barriers to entry. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force ratings, visuals, and actionable strategy tailored to Bank of Maharashtra. Purchase now for a consultant‑grade report.

Suppliers Bargaining Power

Low-cost depositors as capital suppliers

Bank of Maharashtra relies heavily on CASA depositors, which provided around 40% of deposits in 2024, supplying low-cost funding that supports net interest margins. Individually their bargaining power is low, but collectively they can reallocate balances toward higher rates or superior digital platforms. Sensitivity rises with tightening liquidity and rising rate cycles. Strong branch network and trust moderate this supplier power.

Government ownership and policy influence

As a majority government‑owned public sector bank, Bank of Maharashtra benefits from sovereign backing that stabilizes funding and lowers perceived risk, reducing supplier leverage. However, government mandates like priority sector lending (40% of adjusted net bank credit, 8% for small/marginal farmers) constrain commercial flexibility, creating a dual dynamic of lower supplier power but added policy-driven constraints.

Wholesale funding and interbank markets

Access to bonds, CDs and interbank lines gives Bank of Maharashtra scale but increases supplier power in tight markets; India’s 10-year G-sec averaged about 7.2% in 2024 and repo was 6.5%, sharpening funding costs with sentiment shifts. Pricing is highly sensitive to credit ratings and macro risk. RBI LAF/OMO operations cushion spikes but do not remove volatility. Diversifying tenors and instruments reduces dependence.

Technology vendors and core platforms

Reliance on core banking suites, cybersecurity providers and payment rails concentrates supplier power in a handful of vendors, and switching costs, integration complexity and regulatory uptime mandates amplify vendor leverage. Long-term contracts and certification requirements deepen dependence, while multi-vendor strategies and open APIs reduce lock-in and improve negotiating leverage.

- Concentration: few core vendors

- Leverage: high switching costs

- Risk: regulatory uptime & certifications

- Mitigation: multi-vendor + open APIs

Skilled talent and compliance expertise

Experienced bankers, risk managers and tech talent remain scarce for Bank of Maharashtra, with industry reports in 2024 showing talent shortages pushing salary premiums of roughly 20–30% at private banks and fintechs vs PSBs; this elevates supplier power of labor. PSB pay structures and rigid scales limit rapid matching of market offers, though targeted retention bonuses and internal mobility partially mitigate churn. Ongoing training pipelines and accelerated upskilling programs reduce reliance on external hires over the medium term.

- 2024 salary premium: 20–30% at private banks/fintechs

- PSB flexibility: constrained by standardized pay scales

- Mitigants: internal mobility, training pipelines, targeted bonuses

Moderate supplier power — CASA ~40%, higher rates and salary premiums increase leverage

Suppliers' bargaining power is moderate: CASA (~40% of deposits in 2024) supplies low-cost funds but can shift to better rates or platforms. Market funding sensitivity increased as 10y G-sec averaged 7.2% and repo was 6.5% in 2024. Vendor concentration, high switching costs and 20–30% private-bank salary premiums raise supplier leverage, offset by PSU backing and multi-vendor strategies.

| Metric | 2024 Value |

|---|---|

| CASA share | ~40% |

| 10y G-sec | 7.2% |

| Repo rate | 6.5% |

| Salary premium | 20–30% |

What is included in the product

Porter’s Five Forces analysis for Bank of Maharashtra uncovers competitive drivers, customer bargaining power, supplier influence, threat of new entrants and substitutes, and regulatory pressures shaping profitability. It highlights emerging digital disruptors and market dynamics that constrain pricing, protect incumbency, and guide strategic responses.

One-sheet Porter's Five Forces for Bank of Maharashtra—clarifies competitive pressures, lets you customize intensity by scenario, and includes a ready-to-use radar chart and clean layout for swift boardroom decisions and regulatory planning.

Customers Bargaining Power

Rate-sensitive retail depositors

Individual rate-sensitive retail depositors compare BoM rates and digital service quality across banks, with UPI-enabled switching and digital onboarding (UPI crossed ~100 billion annual transactions by 2023 per NPCI) raising buyer power when rates diverge. Trust and public-sector ownership of Bank of Maharashtra (majority government-held as of 2024) still anchor many balances. Loyalty programs, branch convenience and safety can offset pure price sensitivity.

SME borrowers with multiple options

SME borrowers can choose among 12 public sector banks, private banks, NBFCs and government schemes such as CGTMSE and MUDRA, strengthening their bargaining power. They routinely negotiate interest rates, collateral requirements and turnaround time, pressing lenders on pricing and service. Digital lending platforms have raised price transparency and choice, while Bank of Maharashtra’s relationship banking and bundled cash‑management and trade services help retain SMEs and temper their bargaining leverage.

Large corporates and institutional clients

Large corporates and institutional clients wield strong leverage over Bank of Maharashtra as contested treasury mandates and large loans drive pressure for thin spreads, fee waivers, and tailored cash-management solutions. Syndication of big-ticket loans reduces single-bank dependence, further strengthening buyer power. Deep cross-sell relationships and public-sector comfort—BoM had about 1,810 branches in 2024—help retain portions of this business.

Digital-first customers demanding UX

Digital-first customers benchmark Bank of Maharashtra against top apps; UPI speed and >99% success rates in 2024 set baseline expectations. Poor UX or reliability triggers rapid switching or multi-banking, amplified by social media feedback loops and reviews. Continuous feature upgrades and 24x7 support materially reduce buyer leverage.

- Benchmarks: app performance, UPI latency

- 2024: >99% UPI success; ~80% retail interactions digital

- Response: continuous upgrades, 24x7 support

Rural and priority sector segments

Rural and priority customers for Bank of Maharashtra are semi-captive due to regulatory priority sector targets (40% of adjusted net bank credit), but ticket sizes remain small so pricing sensitivity is limited. Physical reach via 2,000+ branches/BC network often trumps interest-rate competition; co-ops, MFIs and SFBs increase choice modestly. Strong DBT and scheme linkages (subsidies, crop loans) stabilize tenure and cross-sell.

Digital-first retail vs branch stickiness: UPI >99%, digital ~80%

Customers exert moderate-to-high bargaining power: rate-sensitive retail depositors compare UPI-enabled offers (>99% UPI success in 2024) and ~80% retail interactions digital, while public-ownership (majority govt-held in 2024) and branch reach (≈1,810 branches) retain stickiness. SMEs and corporates have stronger leverage via NBFCs/alternate lenders and syndication; priority‑sector clients are semi-captive (40% PSL).

| Metric | 2024 |

|---|---|

| UPI success | >99% |

| Retail digital interactions | ~80% |

| Branches | ≈1,810 |

| Priority sector target | 40% PSL |

Full Version Awaits

Bank of Maharashtra Porter's Five Forces Analysis

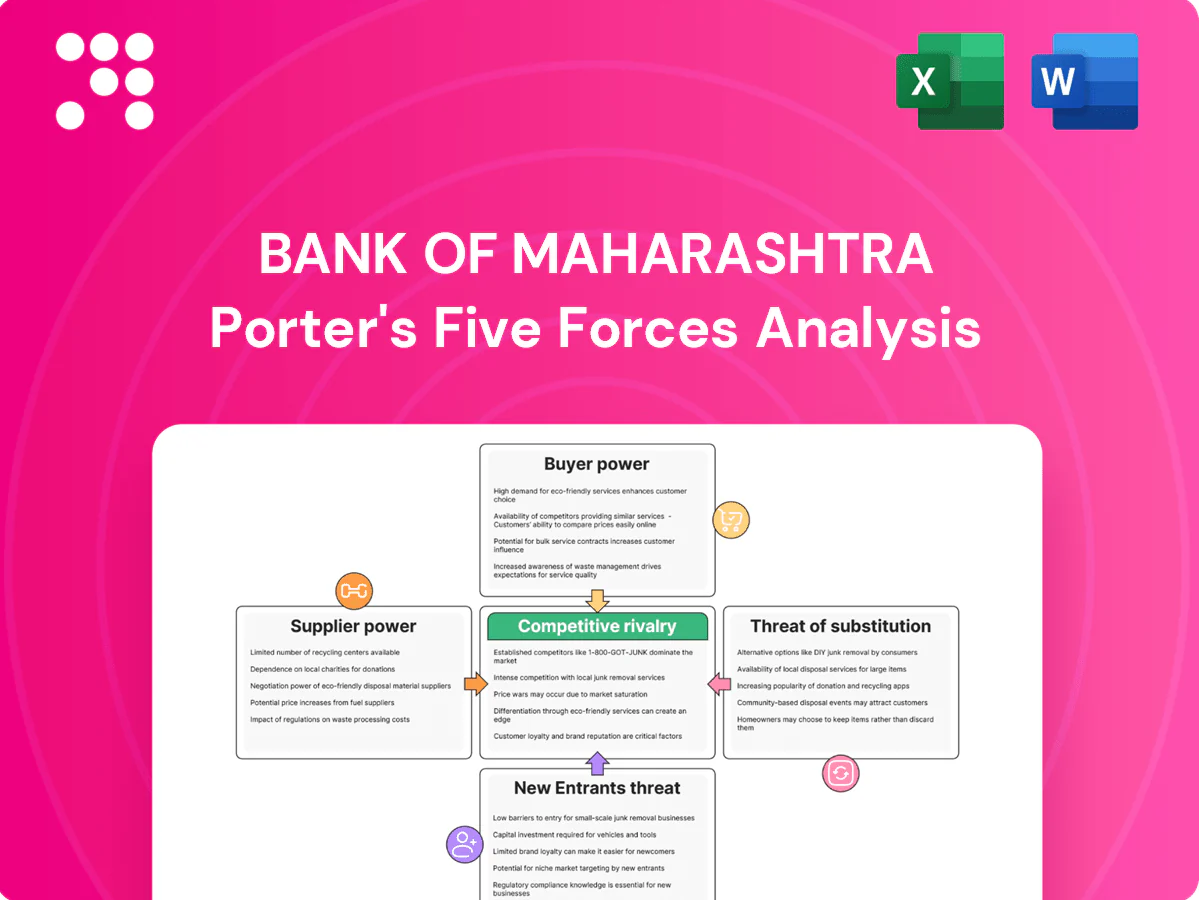

This preview shows the exact Bank of Maharashtra Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The document covers buyer power, supplier power, competitive rivalry, threat of substitutes and barriers to entry with clear conclusions and implications. It's fully formatted and ready to download instantly. Use it immediately in reports or presentations.

Go Beyond the Preview—Access the Full Strategic Report

Bank of Maharashtra faces moderate buyer power, intense regulatory scrutiny, and rising fintech substitution, while its branch network and PSU backing bolster barriers to entry. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force ratings, visuals, and actionable strategy tailored to Bank of Maharashtra. Purchase now for a consultant‑grade report.

Suppliers Bargaining Power

Low-cost depositors as capital suppliers

Bank of Maharashtra relies heavily on CASA depositors, which provided around 40% of deposits in 2024, supplying low-cost funding that supports net interest margins. Individually their bargaining power is low, but collectively they can reallocate balances toward higher rates or superior digital platforms. Sensitivity rises with tightening liquidity and rising rate cycles. Strong branch network and trust moderate this supplier power.

Government ownership and policy influence

As a majority government‑owned public sector bank, Bank of Maharashtra benefits from sovereign backing that stabilizes funding and lowers perceived risk, reducing supplier leverage. However, government mandates like priority sector lending (40% of adjusted net bank credit, 8% for small/marginal farmers) constrain commercial flexibility, creating a dual dynamic of lower supplier power but added policy-driven constraints.

Wholesale funding and interbank markets

Access to bonds, CDs and interbank lines gives Bank of Maharashtra scale but increases supplier power in tight markets; India’s 10-year G-sec averaged about 7.2% in 2024 and repo was 6.5%, sharpening funding costs with sentiment shifts. Pricing is highly sensitive to credit ratings and macro risk. RBI LAF/OMO operations cushion spikes but do not remove volatility. Diversifying tenors and instruments reduces dependence.

Technology vendors and core platforms

Reliance on core banking suites, cybersecurity providers and payment rails concentrates supplier power in a handful of vendors, and switching costs, integration complexity and regulatory uptime mandates amplify vendor leverage. Long-term contracts and certification requirements deepen dependence, while multi-vendor strategies and open APIs reduce lock-in and improve negotiating leverage.

- Concentration: few core vendors

- Leverage: high switching costs

- Risk: regulatory uptime & certifications

- Mitigation: multi-vendor + open APIs

Skilled talent and compliance expertise

Experienced bankers, risk managers and tech talent remain scarce for Bank of Maharashtra, with industry reports in 2024 showing talent shortages pushing salary premiums of roughly 20–30% at private banks and fintechs vs PSBs; this elevates supplier power of labor. PSB pay structures and rigid scales limit rapid matching of market offers, though targeted retention bonuses and internal mobility partially mitigate churn. Ongoing training pipelines and accelerated upskilling programs reduce reliance on external hires over the medium term.

- 2024 salary premium: 20–30% at private banks/fintechs

- PSB flexibility: constrained by standardized pay scales

- Mitigants: internal mobility, training pipelines, targeted bonuses

Moderate supplier power — CASA ~40%, higher rates and salary premiums increase leverage

Suppliers' bargaining power is moderate: CASA (~40% of deposits in 2024) supplies low-cost funds but can shift to better rates or platforms. Market funding sensitivity increased as 10y G-sec averaged 7.2% and repo was 6.5% in 2024. Vendor concentration, high switching costs and 20–30% private-bank salary premiums raise supplier leverage, offset by PSU backing and multi-vendor strategies.

| Metric | 2024 Value |

|---|---|

| CASA share | ~40% |

| 10y G-sec | 7.2% |

| Repo rate | 6.5% |

| Salary premium | 20–30% |

What is included in the product

Porter’s Five Forces analysis for Bank of Maharashtra uncovers competitive drivers, customer bargaining power, supplier influence, threat of new entrants and substitutes, and regulatory pressures shaping profitability. It highlights emerging digital disruptors and market dynamics that constrain pricing, protect incumbency, and guide strategic responses.

One-sheet Porter's Five Forces for Bank of Maharashtra—clarifies competitive pressures, lets you customize intensity by scenario, and includes a ready-to-use radar chart and clean layout for swift boardroom decisions and regulatory planning.

Customers Bargaining Power

Rate-sensitive retail depositors

Individual rate-sensitive retail depositors compare BoM rates and digital service quality across banks, with UPI-enabled switching and digital onboarding (UPI crossed ~100 billion annual transactions by 2023 per NPCI) raising buyer power when rates diverge. Trust and public-sector ownership of Bank of Maharashtra (majority government-held as of 2024) still anchor many balances. Loyalty programs, branch convenience and safety can offset pure price sensitivity.

SME borrowers with multiple options

SME borrowers can choose among 12 public sector banks, private banks, NBFCs and government schemes such as CGTMSE and MUDRA, strengthening their bargaining power. They routinely negotiate interest rates, collateral requirements and turnaround time, pressing lenders on pricing and service. Digital lending platforms have raised price transparency and choice, while Bank of Maharashtra’s relationship banking and bundled cash‑management and trade services help retain SMEs and temper their bargaining leverage.

Large corporates and institutional clients

Large corporates and institutional clients wield strong leverage over Bank of Maharashtra as contested treasury mandates and large loans drive pressure for thin spreads, fee waivers, and tailored cash-management solutions. Syndication of big-ticket loans reduces single-bank dependence, further strengthening buyer power. Deep cross-sell relationships and public-sector comfort—BoM had about 1,810 branches in 2024—help retain portions of this business.

Digital-first customers demanding UX

Digital-first customers benchmark Bank of Maharashtra against top apps; UPI speed and >99% success rates in 2024 set baseline expectations. Poor UX or reliability triggers rapid switching or multi-banking, amplified by social media feedback loops and reviews. Continuous feature upgrades and 24x7 support materially reduce buyer leverage.

- Benchmarks: app performance, UPI latency

- 2024: >99% UPI success; ~80% retail interactions digital

- Response: continuous upgrades, 24x7 support

Rural and priority sector segments

Rural and priority customers for Bank of Maharashtra are semi-captive due to regulatory priority sector targets (40% of adjusted net bank credit), but ticket sizes remain small so pricing sensitivity is limited. Physical reach via 2,000+ branches/BC network often trumps interest-rate competition; co-ops, MFIs and SFBs increase choice modestly. Strong DBT and scheme linkages (subsidies, crop loans) stabilize tenure and cross-sell.

Digital-first retail vs branch stickiness: UPI >99%, digital ~80%

Customers exert moderate-to-high bargaining power: rate-sensitive retail depositors compare UPI-enabled offers (>99% UPI success in 2024) and ~80% retail interactions digital, while public-ownership (majority govt-held in 2024) and branch reach (≈1,810 branches) retain stickiness. SMEs and corporates have stronger leverage via NBFCs/alternate lenders and syndication; priority‑sector clients are semi-captive (40% PSL).

| Metric | 2024 |

|---|---|

| UPI success | >99% |

| Retail digital interactions | ~80% |

| Branches | ≈1,810 |

| Priority sector target | 40% PSL |

Full Version Awaits

Bank of Maharashtra Porter's Five Forces Analysis

This preview shows the exact Bank of Maharashtra Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The document covers buyer power, supplier power, competitive rivalry, threat of substitutes and barriers to entry with clear conclusions and implications. It's fully formatted and ready to download instantly. Use it immediately in reports or presentations.

Description

Go Beyond the Preview—Access the Full Strategic Report

Bank of Maharashtra faces moderate buyer power, intense regulatory scrutiny, and rising fintech substitution, while its branch network and PSU backing bolster barriers to entry. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force ratings, visuals, and actionable strategy tailored to Bank of Maharashtra. Purchase now for a consultant‑grade report.

Suppliers Bargaining Power

Low-cost depositors as capital suppliers

Bank of Maharashtra relies heavily on CASA depositors, which provided around 40% of deposits in 2024, supplying low-cost funding that supports net interest margins. Individually their bargaining power is low, but collectively they can reallocate balances toward higher rates or superior digital platforms. Sensitivity rises with tightening liquidity and rising rate cycles. Strong branch network and trust moderate this supplier power.

Government ownership and policy influence

As a majority government‑owned public sector bank, Bank of Maharashtra benefits from sovereign backing that stabilizes funding and lowers perceived risk, reducing supplier leverage. However, government mandates like priority sector lending (40% of adjusted net bank credit, 8% for small/marginal farmers) constrain commercial flexibility, creating a dual dynamic of lower supplier power but added policy-driven constraints.

Wholesale funding and interbank markets

Access to bonds, CDs and interbank lines gives Bank of Maharashtra scale but increases supplier power in tight markets; India’s 10-year G-sec averaged about 7.2% in 2024 and repo was 6.5%, sharpening funding costs with sentiment shifts. Pricing is highly sensitive to credit ratings and macro risk. RBI LAF/OMO operations cushion spikes but do not remove volatility. Diversifying tenors and instruments reduces dependence.

Technology vendors and core platforms

Reliance on core banking suites, cybersecurity providers and payment rails concentrates supplier power in a handful of vendors, and switching costs, integration complexity and regulatory uptime mandates amplify vendor leverage. Long-term contracts and certification requirements deepen dependence, while multi-vendor strategies and open APIs reduce lock-in and improve negotiating leverage.

- Concentration: few core vendors

- Leverage: high switching costs

- Risk: regulatory uptime & certifications

- Mitigation: multi-vendor + open APIs

Skilled talent and compliance expertise

Experienced bankers, risk managers and tech talent remain scarce for Bank of Maharashtra, with industry reports in 2024 showing talent shortages pushing salary premiums of roughly 20–30% at private banks and fintechs vs PSBs; this elevates supplier power of labor. PSB pay structures and rigid scales limit rapid matching of market offers, though targeted retention bonuses and internal mobility partially mitigate churn. Ongoing training pipelines and accelerated upskilling programs reduce reliance on external hires over the medium term.

- 2024 salary premium: 20–30% at private banks/fintechs

- PSB flexibility: constrained by standardized pay scales

- Mitigants: internal mobility, training pipelines, targeted bonuses

Moderate supplier power — CASA ~40%, higher rates and salary premiums increase leverage

Suppliers' bargaining power is moderate: CASA (~40% of deposits in 2024) supplies low-cost funds but can shift to better rates or platforms. Market funding sensitivity increased as 10y G-sec averaged 7.2% and repo was 6.5% in 2024. Vendor concentration, high switching costs and 20–30% private-bank salary premiums raise supplier leverage, offset by PSU backing and multi-vendor strategies.

| Metric | 2024 Value |

|---|---|

| CASA share | ~40% |

| 10y G-sec | 7.2% |

| Repo rate | 6.5% |

| Salary premium | 20–30% |

What is included in the product

Porter’s Five Forces analysis for Bank of Maharashtra uncovers competitive drivers, customer bargaining power, supplier influence, threat of new entrants and substitutes, and regulatory pressures shaping profitability. It highlights emerging digital disruptors and market dynamics that constrain pricing, protect incumbency, and guide strategic responses.

One-sheet Porter's Five Forces for Bank of Maharashtra—clarifies competitive pressures, lets you customize intensity by scenario, and includes a ready-to-use radar chart and clean layout for swift boardroom decisions and regulatory planning.

Customers Bargaining Power

Rate-sensitive retail depositors

Individual rate-sensitive retail depositors compare BoM rates and digital service quality across banks, with UPI-enabled switching and digital onboarding (UPI crossed ~100 billion annual transactions by 2023 per NPCI) raising buyer power when rates diverge. Trust and public-sector ownership of Bank of Maharashtra (majority government-held as of 2024) still anchor many balances. Loyalty programs, branch convenience and safety can offset pure price sensitivity.

SME borrowers with multiple options

SME borrowers can choose among 12 public sector banks, private banks, NBFCs and government schemes such as CGTMSE and MUDRA, strengthening their bargaining power. They routinely negotiate interest rates, collateral requirements and turnaround time, pressing lenders on pricing and service. Digital lending platforms have raised price transparency and choice, while Bank of Maharashtra’s relationship banking and bundled cash‑management and trade services help retain SMEs and temper their bargaining leverage.

Large corporates and institutional clients

Large corporates and institutional clients wield strong leverage over Bank of Maharashtra as contested treasury mandates and large loans drive pressure for thin spreads, fee waivers, and tailored cash-management solutions. Syndication of big-ticket loans reduces single-bank dependence, further strengthening buyer power. Deep cross-sell relationships and public-sector comfort—BoM had about 1,810 branches in 2024—help retain portions of this business.

Digital-first customers demanding UX

Digital-first customers benchmark Bank of Maharashtra against top apps; UPI speed and >99% success rates in 2024 set baseline expectations. Poor UX or reliability triggers rapid switching or multi-banking, amplified by social media feedback loops and reviews. Continuous feature upgrades and 24x7 support materially reduce buyer leverage.

- Benchmarks: app performance, UPI latency

- 2024: >99% UPI success; ~80% retail interactions digital

- Response: continuous upgrades, 24x7 support

Rural and priority sector segments

Rural and priority customers for Bank of Maharashtra are semi-captive due to regulatory priority sector targets (40% of adjusted net bank credit), but ticket sizes remain small so pricing sensitivity is limited. Physical reach via 2,000+ branches/BC network often trumps interest-rate competition; co-ops, MFIs and SFBs increase choice modestly. Strong DBT and scheme linkages (subsidies, crop loans) stabilize tenure and cross-sell.

Digital-first retail vs branch stickiness: UPI >99%, digital ~80%

Customers exert moderate-to-high bargaining power: rate-sensitive retail depositors compare UPI-enabled offers (>99% UPI success in 2024) and ~80% retail interactions digital, while public-ownership (majority govt-held in 2024) and branch reach (≈1,810 branches) retain stickiness. SMEs and corporates have stronger leverage via NBFCs/alternate lenders and syndication; priority‑sector clients are semi-captive (40% PSL).

| Metric | 2024 |

|---|---|

| UPI success | >99% |

| Retail digital interactions | ~80% |

| Branches | ≈1,810 |

| Priority sector target | 40% PSL |

Full Version Awaits

Bank of Maharashtra Porter's Five Forces Analysis

This preview shows the exact Bank of Maharashtra Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. The document covers buyer power, supplier power, competitive rivalry, threat of substitutes and barriers to entry with clear conclusions and implications. It's fully formatted and ready to download instantly. Use it immediately in reports or presentations.