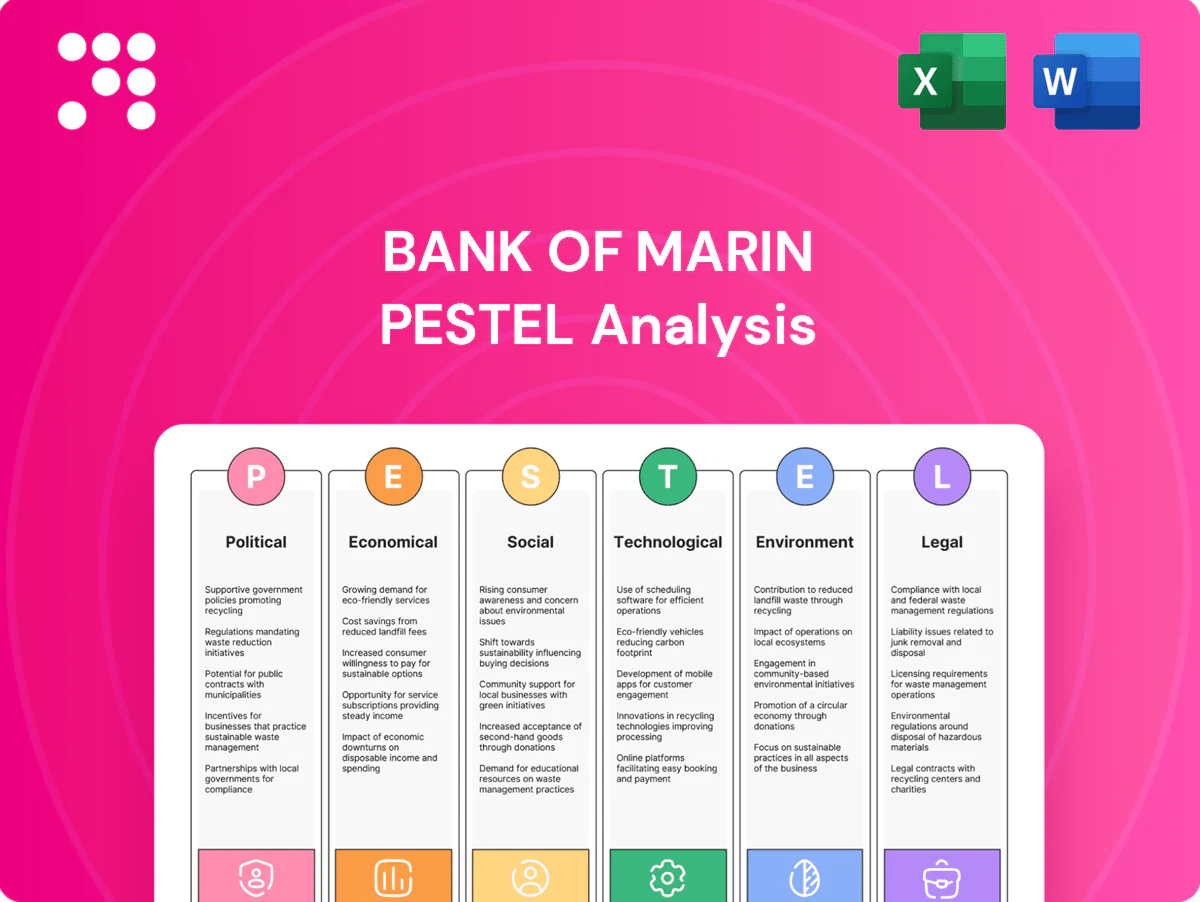

Bank of Marin PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis tailored to Bank of Marin—spot regulatory, economic, and technological forces shaping its future. This concise briefing highlights risks and opportunities you can act on immediately. Purchase the full analysis for the detailed, editable insights your decisions demand.

Political factors

Local government priorities

Marin County’s FY2024–25 budget of about $1.06 billion shapes municipal deposits and local lending capacity, while a Bay Area public-works pipeline estimated at over $2 billion through 2027 can drive credit demand for construction and municipal finance; turnover from 2024–25 local elections may reorient procurement and banking relationships across Marin and nearby cities, so active participation in civic forums helps anticipate shifts.

Housing and zoning policy

California housing laws such as SB 9 and SB 10 and the Bay Area RHNA allocation of 441,176 units for 2023–2031 directly shape mortgage volume and construction lending opportunities for Bank of Marin.

Stricter local zoning or permitting delays lengthen development timetables, slowing loan pipelines and increasing carry costs for developers.

Affordable housing mandates and density bonuses create targeted financing niches, while policy volatility demands flexible underwriting, adjustable covenants and scenario stress-testing.

Federal banking oversight

Federal, FDIC and California regulators' supervisory emphasis forces Bank of Marin to align capital planning with Basel/US minima (CET1 4.5%, total capital 8%, leverage 4%) and higher internal targets for liquidity stress testing. Recent proposals targeting community bank compliance and assessment methodologies raise projected compliance costs by mid-single-digit percentages. CRA exam focus—ratings scale from Outstanding to Substantial Noncompliance—directly affects branch and local-lending strategies, while political turnover can reprioritize rule timelines and enforcement dates.

Tax and incentives

Local and state tax credits lower SMB project costs and boost borrowing demand, while SALT deductibility remains capped at $10,000 (TCJA 2017), influencing affluent client deposit and lending behavior.

- muni-issuance: US municipal issuance ≈ $460B (2024)

- SALT-cap: $10,000

- SMB-credit: supports regional loan growth

- fiscal-shifts: public-entity deposit flows affect liquidity

Public safety and civic stability

Perceptions of safety and governance shape Bay Area business formation and commercial corridor vitality; California recorded about 171,000 people experiencing homelessness in 2023, which influences retail foot traffic and investor confidence. Political responses to homelessness and rising retail theft incidents drive policy and policing shifts that affect branch visits and small-business credit demand. Policy missteps can depress local consumer spending and loan performance.

- Safety perception: affects new business formation and branch traffic

- Homelessness (CA ~171,000 in 2023): impacts corridor vitality

- Retail theft & policy response: alters policing, insurance, lending

Marin $1.06B budget; RHNA 441,176 units expand housing demand

Marin County FY2024–25 budget ≈ $1.06B and Bay Area public-works pipeline >$2B through 2027 support municipal and construction lending; CA RHNA 441,176 units (2023–31) expands mortgage and developer demand. Federal/FDIC/CA rules require capital planning (CET1 4.5% min) and rising compliance costs; homelessness (~171,000 in CA, 2023) and retail crime affect branch traffic and small-business credit.

| Metric | Value |

|---|---|

| Marin budget FY24–25 | $1.06B |

| Bay Area muni issuance (2024) | $460B |

| RHNA 2023–31 | 441,176 units |

| CA homelessness (2023) | ~171,000 |

| SALT cap | $10,000 |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank of Marin across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific insights and forward-looking implications to help executives and advisors identify risks, opportunities and strategic actions.

A concise, visually segmented PESTLE summary for Bank of Marin that’s easy to drop into presentations and share across teams, enabling quick alignment on external risks and market positioning. Editable notes let users tailor insights to region or business line for faster decision-making in planning sessions.

Economic factors

Interest rate cycle

Net interest margin for Bank of Marin hinges on the Fed funds rate (5.25–5.50% as of July 2025) and deposit beta; higher beta erodes NIM. Rapid hiking cycles raise funding costs and force unrealized losses in securities AOCI. Easing can revive loan demand but tends to compress spreads. Active balance sheet management is therefore critical.

Bay Area growth volatility

Bay Area tech employment swings—recently reflecting a VC funding environment roughly 50% below the 2021 peak—drive deposit flows and credit demand for Bank of Marin as payroll-sensitive clients fluctuate. Office vacancy in San Francisco and Silicon Valley remains elevated, above 20%, pressuring CRE collateral values. Equity market moves materially affect high-net-worth balances and lending capacity. Broad industry diversification in the region helps mitigate cyclical exposure.

Small business health

Local SMB revenue trends directly drive Bank of Marin C&I utilization as small firms tighten working capital; new business applications stayed elevated at about 4.4 million in 2023 (U.S. Census Business Formation Statistics), supporting deposit and treasury-fee growth. Ongoing supply-chain disruptions and sustained wage inflation pressure margins and raise credit risk metrics. Relationship banking positions the bank to capture share during local dislocations.

Credit quality and delinquencies

Inflation and slower growth elevate NPA risk for Bank of Marin as borrowers face cash‑flow pressure, with commercial real estate—notably retail and office—requiring closer surveillance due to sectoral demand shifts. Prudent loan‑to‑value limits and covenant enforcement have contained losses historically, while scenario-driven stress tests direct reserve adequacy and capital planning.

- Credit risk: heightened by inflation and slower GDP

- CRE focus: retail and office higher watchlist

- Risk controls: LTV limits and covenants

- Reserves: stress tests inform provisioning

Competition and consolidation

Large banks and fintechs pushed online savings APYs into the ~4–5% range in 2024–H1 2025, bidding up deposit costs and raising customer expectations for convenience; Bank of Marin faces pressure to match rates or lean on service and niche lending. Accelerating M&A has concentrated share regionally and driven branch closures, testing pricing discipline in crowded niches while rewarding niche expertise and faster service delivery.

- Deposit APY pressure: ~4–5% (2024–H1 2025)

- M&A concentrates local market share, reduces branch density

- Pricing discipline strained in crowded niches

- Niche expertise and speed = differentiation

Marin $1.06B budget; RHNA 441,176 units expand housing demand

Fed funds 5.25–5.50% (Jul 2025) compresses NIM; deposit APYs ~4–5% (2024–H1 2025) raise funding cost. Bay Area VC funding ~50% below 2021 peak and office vacancy >20% elevate CRE and HNW volatility. New business applications 4.4M (2023) support deposits but wage inflation and slower growth heighten credit risk.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| Deposit APY | ~4–5% (2024–H1 2025) |

| Office vacancy | >20% (SF/SV) |

| VC funding | ~50% below 2021 peak |

| New business apps | 4.4M (2023) |

Preview Before You Purchase

Bank of Marin PESTLE Analysis

The preview shown here is the exact Bank of Marin PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete PESTLE assessment, analysis and conclusions with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after buying.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis tailored to Bank of Marin—spot regulatory, economic, and technological forces shaping its future. This concise briefing highlights risks and opportunities you can act on immediately. Purchase the full analysis for the detailed, editable insights your decisions demand.

Political factors

Local government priorities

Marin County’s FY2024–25 budget of about $1.06 billion shapes municipal deposits and local lending capacity, while a Bay Area public-works pipeline estimated at over $2 billion through 2027 can drive credit demand for construction and municipal finance; turnover from 2024–25 local elections may reorient procurement and banking relationships across Marin and nearby cities, so active participation in civic forums helps anticipate shifts.

Housing and zoning policy

California housing laws such as SB 9 and SB 10 and the Bay Area RHNA allocation of 441,176 units for 2023–2031 directly shape mortgage volume and construction lending opportunities for Bank of Marin.

Stricter local zoning or permitting delays lengthen development timetables, slowing loan pipelines and increasing carry costs for developers.

Affordable housing mandates and density bonuses create targeted financing niches, while policy volatility demands flexible underwriting, adjustable covenants and scenario stress-testing.

Federal banking oversight

Federal, FDIC and California regulators' supervisory emphasis forces Bank of Marin to align capital planning with Basel/US minima (CET1 4.5%, total capital 8%, leverage 4%) and higher internal targets for liquidity stress testing. Recent proposals targeting community bank compliance and assessment methodologies raise projected compliance costs by mid-single-digit percentages. CRA exam focus—ratings scale from Outstanding to Substantial Noncompliance—directly affects branch and local-lending strategies, while political turnover can reprioritize rule timelines and enforcement dates.

Tax and incentives

Local and state tax credits lower SMB project costs and boost borrowing demand, while SALT deductibility remains capped at $10,000 (TCJA 2017), influencing affluent client deposit and lending behavior.

- muni-issuance: US municipal issuance ≈ $460B (2024)

- SALT-cap: $10,000

- SMB-credit: supports regional loan growth

- fiscal-shifts: public-entity deposit flows affect liquidity

Public safety and civic stability

Perceptions of safety and governance shape Bay Area business formation and commercial corridor vitality; California recorded about 171,000 people experiencing homelessness in 2023, which influences retail foot traffic and investor confidence. Political responses to homelessness and rising retail theft incidents drive policy and policing shifts that affect branch visits and small-business credit demand. Policy missteps can depress local consumer spending and loan performance.

- Safety perception: affects new business formation and branch traffic

- Homelessness (CA ~171,000 in 2023): impacts corridor vitality

- Retail theft & policy response: alters policing, insurance, lending

Marin $1.06B budget; RHNA 441,176 units expand housing demand

Marin County FY2024–25 budget ≈ $1.06B and Bay Area public-works pipeline >$2B through 2027 support municipal and construction lending; CA RHNA 441,176 units (2023–31) expands mortgage and developer demand. Federal/FDIC/CA rules require capital planning (CET1 4.5% min) and rising compliance costs; homelessness (~171,000 in CA, 2023) and retail crime affect branch traffic and small-business credit.

| Metric | Value |

|---|---|

| Marin budget FY24–25 | $1.06B |

| Bay Area muni issuance (2024) | $460B |

| RHNA 2023–31 | 441,176 units |

| CA homelessness (2023) | ~171,000 |

| SALT cap | $10,000 |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank of Marin across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific insights and forward-looking implications to help executives and advisors identify risks, opportunities and strategic actions.

A concise, visually segmented PESTLE summary for Bank of Marin that’s easy to drop into presentations and share across teams, enabling quick alignment on external risks and market positioning. Editable notes let users tailor insights to region or business line for faster decision-making in planning sessions.

Economic factors

Interest rate cycle

Net interest margin for Bank of Marin hinges on the Fed funds rate (5.25–5.50% as of July 2025) and deposit beta; higher beta erodes NIM. Rapid hiking cycles raise funding costs and force unrealized losses in securities AOCI. Easing can revive loan demand but tends to compress spreads. Active balance sheet management is therefore critical.

Bay Area growth volatility

Bay Area tech employment swings—recently reflecting a VC funding environment roughly 50% below the 2021 peak—drive deposit flows and credit demand for Bank of Marin as payroll-sensitive clients fluctuate. Office vacancy in San Francisco and Silicon Valley remains elevated, above 20%, pressuring CRE collateral values. Equity market moves materially affect high-net-worth balances and lending capacity. Broad industry diversification in the region helps mitigate cyclical exposure.

Small business health

Local SMB revenue trends directly drive Bank of Marin C&I utilization as small firms tighten working capital; new business applications stayed elevated at about 4.4 million in 2023 (U.S. Census Business Formation Statistics), supporting deposit and treasury-fee growth. Ongoing supply-chain disruptions and sustained wage inflation pressure margins and raise credit risk metrics. Relationship banking positions the bank to capture share during local dislocations.

Credit quality and delinquencies

Inflation and slower growth elevate NPA risk for Bank of Marin as borrowers face cash‑flow pressure, with commercial real estate—notably retail and office—requiring closer surveillance due to sectoral demand shifts. Prudent loan‑to‑value limits and covenant enforcement have contained losses historically, while scenario-driven stress tests direct reserve adequacy and capital planning.

- Credit risk: heightened by inflation and slower GDP

- CRE focus: retail and office higher watchlist

- Risk controls: LTV limits and covenants

- Reserves: stress tests inform provisioning

Competition and consolidation

Large banks and fintechs pushed online savings APYs into the ~4–5% range in 2024–H1 2025, bidding up deposit costs and raising customer expectations for convenience; Bank of Marin faces pressure to match rates or lean on service and niche lending. Accelerating M&A has concentrated share regionally and driven branch closures, testing pricing discipline in crowded niches while rewarding niche expertise and faster service delivery.

- Deposit APY pressure: ~4–5% (2024–H1 2025)

- M&A concentrates local market share, reduces branch density

- Pricing discipline strained in crowded niches

- Niche expertise and speed = differentiation

Marin $1.06B budget; RHNA 441,176 units expand housing demand

Fed funds 5.25–5.50% (Jul 2025) compresses NIM; deposit APYs ~4–5% (2024–H1 2025) raise funding cost. Bay Area VC funding ~50% below 2021 peak and office vacancy >20% elevate CRE and HNW volatility. New business applications 4.4M (2023) support deposits but wage inflation and slower growth heighten credit risk.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| Deposit APY | ~4–5% (2024–H1 2025) |

| Office vacancy | >20% (SF/SV) |

| VC funding | ~50% below 2021 peak |

| New business apps | 4.4M (2023) |

Preview Before You Purchase

Bank of Marin PESTLE Analysis

The preview shown here is the exact Bank of Marin PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete PESTLE assessment, analysis and conclusions with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after buying.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis tailored to Bank of Marin—spot regulatory, economic, and technological forces shaping its future. This concise briefing highlights risks and opportunities you can act on immediately. Purchase the full analysis for the detailed, editable insights your decisions demand.

Political factors

Local government priorities

Marin County’s FY2024–25 budget of about $1.06 billion shapes municipal deposits and local lending capacity, while a Bay Area public-works pipeline estimated at over $2 billion through 2027 can drive credit demand for construction and municipal finance; turnover from 2024–25 local elections may reorient procurement and banking relationships across Marin and nearby cities, so active participation in civic forums helps anticipate shifts.

Housing and zoning policy

California housing laws such as SB 9 and SB 10 and the Bay Area RHNA allocation of 441,176 units for 2023–2031 directly shape mortgage volume and construction lending opportunities for Bank of Marin.

Stricter local zoning or permitting delays lengthen development timetables, slowing loan pipelines and increasing carry costs for developers.

Affordable housing mandates and density bonuses create targeted financing niches, while policy volatility demands flexible underwriting, adjustable covenants and scenario stress-testing.

Federal banking oversight

Federal, FDIC and California regulators' supervisory emphasis forces Bank of Marin to align capital planning with Basel/US minima (CET1 4.5%, total capital 8%, leverage 4%) and higher internal targets for liquidity stress testing. Recent proposals targeting community bank compliance and assessment methodologies raise projected compliance costs by mid-single-digit percentages. CRA exam focus—ratings scale from Outstanding to Substantial Noncompliance—directly affects branch and local-lending strategies, while political turnover can reprioritize rule timelines and enforcement dates.

Tax and incentives

Local and state tax credits lower SMB project costs and boost borrowing demand, while SALT deductibility remains capped at $10,000 (TCJA 2017), influencing affluent client deposit and lending behavior.

- muni-issuance: US municipal issuance ≈ $460B (2024)

- SALT-cap: $10,000

- SMB-credit: supports regional loan growth

- fiscal-shifts: public-entity deposit flows affect liquidity

Public safety and civic stability

Perceptions of safety and governance shape Bay Area business formation and commercial corridor vitality; California recorded about 171,000 people experiencing homelessness in 2023, which influences retail foot traffic and investor confidence. Political responses to homelessness and rising retail theft incidents drive policy and policing shifts that affect branch visits and small-business credit demand. Policy missteps can depress local consumer spending and loan performance.

- Safety perception: affects new business formation and branch traffic

- Homelessness (CA ~171,000 in 2023): impacts corridor vitality

- Retail theft & policy response: alters policing, insurance, lending

Marin $1.06B budget; RHNA 441,176 units expand housing demand

Marin County FY2024–25 budget ≈ $1.06B and Bay Area public-works pipeline >$2B through 2027 support municipal and construction lending; CA RHNA 441,176 units (2023–31) expands mortgage and developer demand. Federal/FDIC/CA rules require capital planning (CET1 4.5% min) and rising compliance costs; homelessness (~171,000 in CA, 2023) and retail crime affect branch traffic and small-business credit.

| Metric | Value |

|---|---|

| Marin budget FY24–25 | $1.06B |

| Bay Area muni issuance (2024) | $460B |

| RHNA 2023–31 | 441,176 units |

| CA homelessness (2023) | ~171,000 |

| SALT cap | $10,000 |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank of Marin across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific insights and forward-looking implications to help executives and advisors identify risks, opportunities and strategic actions.

A concise, visually segmented PESTLE summary for Bank of Marin that’s easy to drop into presentations and share across teams, enabling quick alignment on external risks and market positioning. Editable notes let users tailor insights to region or business line for faster decision-making in planning sessions.

Economic factors

Interest rate cycle

Net interest margin for Bank of Marin hinges on the Fed funds rate (5.25–5.50% as of July 2025) and deposit beta; higher beta erodes NIM. Rapid hiking cycles raise funding costs and force unrealized losses in securities AOCI. Easing can revive loan demand but tends to compress spreads. Active balance sheet management is therefore critical.

Bay Area growth volatility

Bay Area tech employment swings—recently reflecting a VC funding environment roughly 50% below the 2021 peak—drive deposit flows and credit demand for Bank of Marin as payroll-sensitive clients fluctuate. Office vacancy in San Francisco and Silicon Valley remains elevated, above 20%, pressuring CRE collateral values. Equity market moves materially affect high-net-worth balances and lending capacity. Broad industry diversification in the region helps mitigate cyclical exposure.

Small business health

Local SMB revenue trends directly drive Bank of Marin C&I utilization as small firms tighten working capital; new business applications stayed elevated at about 4.4 million in 2023 (U.S. Census Business Formation Statistics), supporting deposit and treasury-fee growth. Ongoing supply-chain disruptions and sustained wage inflation pressure margins and raise credit risk metrics. Relationship banking positions the bank to capture share during local dislocations.

Credit quality and delinquencies

Inflation and slower growth elevate NPA risk for Bank of Marin as borrowers face cash‑flow pressure, with commercial real estate—notably retail and office—requiring closer surveillance due to sectoral demand shifts. Prudent loan‑to‑value limits and covenant enforcement have contained losses historically, while scenario-driven stress tests direct reserve adequacy and capital planning.

- Credit risk: heightened by inflation and slower GDP

- CRE focus: retail and office higher watchlist

- Risk controls: LTV limits and covenants

- Reserves: stress tests inform provisioning

Competition and consolidation

Large banks and fintechs pushed online savings APYs into the ~4–5% range in 2024–H1 2025, bidding up deposit costs and raising customer expectations for convenience; Bank of Marin faces pressure to match rates or lean on service and niche lending. Accelerating M&A has concentrated share regionally and driven branch closures, testing pricing discipline in crowded niches while rewarding niche expertise and faster service delivery.

- Deposit APY pressure: ~4–5% (2024–H1 2025)

- M&A concentrates local market share, reduces branch density

- Pricing discipline strained in crowded niches

- Niche expertise and speed = differentiation

Marin $1.06B budget; RHNA 441,176 units expand housing demand

Fed funds 5.25–5.50% (Jul 2025) compresses NIM; deposit APYs ~4–5% (2024–H1 2025) raise funding cost. Bay Area VC funding ~50% below 2021 peak and office vacancy >20% elevate CRE and HNW volatility. New business applications 4.4M (2023) support deposits but wage inflation and slower growth heighten credit risk.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jul 2025) |

| Deposit APY | ~4–5% (2024–H1 2025) |

| Office vacancy | >20% (SF/SV) |

| VC funding | ~50% below 2021 peak |

| New business apps | 4.4M (2023) |

Preview Before You Purchase

Bank of Marin PESTLE Analysis

The preview shown here is the exact Bank of Marin PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete PESTLE assessment, analysis and conclusions with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after buying.