Bank of Xi'an SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Our SWOT snapshot of Bank of Xi'an highlights resilient regional market strength, growing digital adoption, margin pressure from competition, and regulatory sensitivity. The analysis pinpoints strategic opportunities in SME lending and fintech partnerships while flagging capital and asset-quality risks. Discover the complete picture behind the bank’s market position with our full SWOT analysis. Purchase the report for a ready-to-use, editable investor brief and Excel matrix.

Strengths

Strong regional franchise

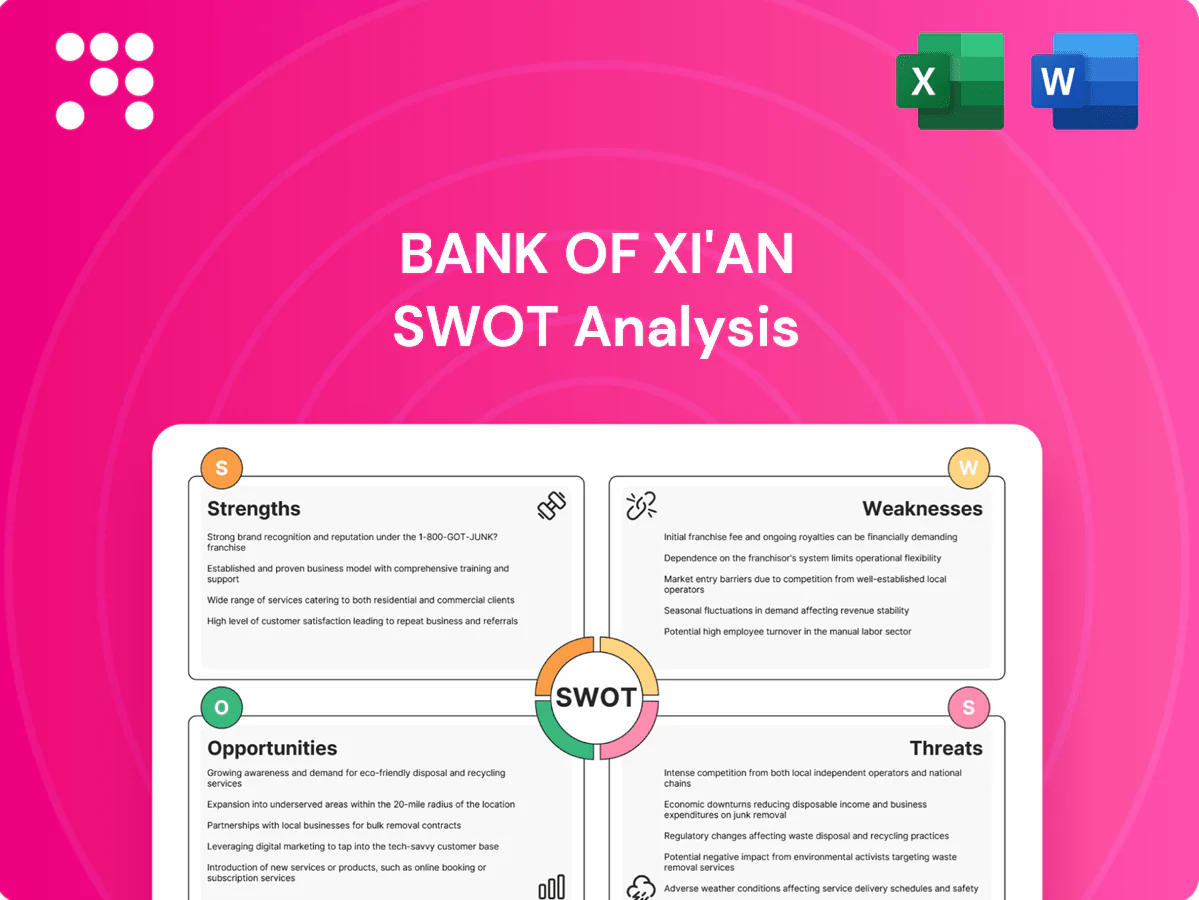

Headquartered in Xi'an with roots dating to 1997, the bank benefits from strong brand recognition and trust across Shaanxi (population 38.64 million per 2020 census). Dense local branch coverage and long-standing client ties lower customer acquisition costs. Proximity to corporates and households enables faster credit decisions and tailored solutions. That embeddedness translates into relatively stable local deposit inflows.

Diversified product suite

Bank of Xi'an offers deposits, loans and payment/settlement services to retail and corporate clients, supporting daily banking and credit needs and boosting wallet share; total assets reached about RMB 1.12 trillion by end-2023. Multiple revenue streams—interest income plus fee income—reduce reliance on any single product, with net interest margin stabilization in recent quarters. Cross-selling across segments enhances customer lifetime value and retention.

SME and local insight

Bank of Xi'an's deep local and SME focus leverages intimate knowledge of regional industries to improve underwriting outcomes; Chinese SMEs contribute over 60% of GDP and about 80% of urban employment (recent official figures). Relationship managers capture soft information beyond financials, enabling faster turnarounds that boost customer stickiness, while niche SME expertise differentiates the bank from larger national competitors.

Stable core deposits

Bank of Xi'an's stable core deposits, anchored in a strong regional retail base in Shaanxi, supply low-cost funding that supports lending growth. Sticky transaction accounts enhance liquidity management and reduce reliance on wholesale markets. Lower funding costs help protect net interest margin and the deposit base boosts resilience during stress periods.

- Regional retail base: supports low-cost funding

- Sticky transaction accounts: steady liquidity

- Lower funding costs: protect NIM

- Deposit resilience: cushions stress

Government and SOE ties

Government and SOE linkages secure steady business flows for Bank of Xi'an, feeding project lending and transactional volumes; participation in regional infrastructure programs expands loan pipelines and fee income. Public-sector payments and payroll contracts help stabilize deposit bases, while alignment with local policy priorities can dampen credit volatility in targeted segments.

- ticker 601128 — strong municipal SOE ties

- regional projects → expanded lending

- public payrolls anchor deposits

- policy alignment reduces segment volatility

Xi'an-headquartered bank since 1997 with RMB 1.12T assets and sticky retail deposits

Headquartered in Xi'an since 1997, strong brand in Shaanxi (pop 38.64M) and dense branches yield stable retail deposits and low acquisition costs.

Total assets ~RMB 1.12 trillion (end-2023), diversified interest and fee income and resilient NIM from low funding costs.

Deep SME and SOE ties (ticker 601128) drive project lending, transactional volumes and sticky deposit flows.

| Metric | Value |

|---|---|

| Founded | 1997 |

| Total assets | RMB 1.12 trillion (end-2023) |

| Shaanxi population | 38.64 million (2020) |

| Ticker | 601128 |

What is included in the product

Provides a concise SWOT analysis of Bank of Xi'an, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic position and future growth prospects.

Provides a concise Bank of Xi'an SWOT matrix that highlights key risks and opportunities for rapid pain-point mitigation, enabling executives to prioritize strategic fixes quickly.

Weaknesses

Geographic concentration

Headquartered in Xi'an with core operations concentrated in Shaanxi, Bank of Xi'an faces heightened exposure to local shocks; regional economic downturns or sector slumps tend to transmit rapidly to its asset quality. Limited cross‑province diversification constrains risk spreading and makes loan book performance closely tied to Shaanxi’s economic trajectory. Growth prospects are therefore heavily dependent on the province’s macro cycle.

Scale disadvantage

Bank of Xi'an's sub-1 trillion RMB asset base leaves it far smaller than national banks that manage assets in the tens of trillions RMB, constraining pricing power on loans and deposits. Higher unit costs raise cost-to-income pressures relative to larger peers, squeezing efficiency ratios. Access to capital markets tends to be costlier and episodic, raising funding volatility. Marketing reach and talent attraction remain comparatively limited outside its regional footprint.

Technology gaps

Bank of Xi'an (SSE: 601128) trails leading fintechs and mega-banks in digital capabilities, with uneven user experience and limited depth in data analytics relative to mobile-first rivals. Slower innovation cycles increase risk of customer churn as younger users favor agile apps. IT modernization will require sizable, sustained investment to catch up and retain deposits and fee income.

Concentrated loan book

Concentrated loan book: Bank of Xi'an’s regional corporate and SME lending often clusters in sectors such as local real estate and infrastructure, increasing cyclical sensitivity and borrower reliance on municipal demand, while collateral values move together within the region, amplifying correlation and systemic credit risk.

- Regional sector clustering

- Overweight real estate/infrastructure

- High local demand dependence

- Regionally correlated collateral

Limited fee income

Reliance on interest income exposes earnings to NIM pressure; Bank of Xi'an’s non‑interest income was only about 19% of operating income in 2023, limiting buffer against margin compression.

Underdeveloped wealth, insurance and advisory fees cap ROE upside, while volatile trading and investment gains cannot reliably replace fee income, reducing overall resilience.

- Low non‑interest income ~19% (2023)

- High interest income dependence

- Weak wealth/insurance fees

- Volatile trading gains

Xi'an regional bank ≈0.97T RMB, 19% non‑interest income

Headquartered in Xi'an with core operations concentrated in Shaanxi, Bank of Xi'an (SSE:601128) has limited geographic diversification, a sub‑1 trillion RMB asset base and weaker digital/fee franchises, leaving earnings and asset quality highly tied to regional cycles; non‑interest income was about 19% of operating income in 2023.

| Metric | Value |

|---|---|

| Total assets (2023) | ≈0.97 trillion RMB |

| Non‑interest income (2023) | ≈19% |

Preview the Actual Deliverable

Bank of Xi'an SWOT Analysis

This is the actual Bank of Xi'an SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report; buy to unlock the entire, editable version. The file is structured, actionable and ready for immediate use.

Go Beyond the Preview—Access the Full Strategic Report

Our SWOT snapshot of Bank of Xi'an highlights resilient regional market strength, growing digital adoption, margin pressure from competition, and regulatory sensitivity. The analysis pinpoints strategic opportunities in SME lending and fintech partnerships while flagging capital and asset-quality risks. Discover the complete picture behind the bank’s market position with our full SWOT analysis. Purchase the report for a ready-to-use, editable investor brief and Excel matrix.

Strengths

Strong regional franchise

Headquartered in Xi'an with roots dating to 1997, the bank benefits from strong brand recognition and trust across Shaanxi (population 38.64 million per 2020 census). Dense local branch coverage and long-standing client ties lower customer acquisition costs. Proximity to corporates and households enables faster credit decisions and tailored solutions. That embeddedness translates into relatively stable local deposit inflows.

Diversified product suite

Bank of Xi'an offers deposits, loans and payment/settlement services to retail and corporate clients, supporting daily banking and credit needs and boosting wallet share; total assets reached about RMB 1.12 trillion by end-2023. Multiple revenue streams—interest income plus fee income—reduce reliance on any single product, with net interest margin stabilization in recent quarters. Cross-selling across segments enhances customer lifetime value and retention.

SME and local insight

Bank of Xi'an's deep local and SME focus leverages intimate knowledge of regional industries to improve underwriting outcomes; Chinese SMEs contribute over 60% of GDP and about 80% of urban employment (recent official figures). Relationship managers capture soft information beyond financials, enabling faster turnarounds that boost customer stickiness, while niche SME expertise differentiates the bank from larger national competitors.

Stable core deposits

Bank of Xi'an's stable core deposits, anchored in a strong regional retail base in Shaanxi, supply low-cost funding that supports lending growth. Sticky transaction accounts enhance liquidity management and reduce reliance on wholesale markets. Lower funding costs help protect net interest margin and the deposit base boosts resilience during stress periods.

- Regional retail base: supports low-cost funding

- Sticky transaction accounts: steady liquidity

- Lower funding costs: protect NIM

- Deposit resilience: cushions stress

Government and SOE ties

Government and SOE linkages secure steady business flows for Bank of Xi'an, feeding project lending and transactional volumes; participation in regional infrastructure programs expands loan pipelines and fee income. Public-sector payments and payroll contracts help stabilize deposit bases, while alignment with local policy priorities can dampen credit volatility in targeted segments.

- ticker 601128 — strong municipal SOE ties

- regional projects → expanded lending

- public payrolls anchor deposits

- policy alignment reduces segment volatility

Xi'an-headquartered bank since 1997 with RMB 1.12T assets and sticky retail deposits

Headquartered in Xi'an since 1997, strong brand in Shaanxi (pop 38.64M) and dense branches yield stable retail deposits and low acquisition costs.

Total assets ~RMB 1.12 trillion (end-2023), diversified interest and fee income and resilient NIM from low funding costs.

Deep SME and SOE ties (ticker 601128) drive project lending, transactional volumes and sticky deposit flows.

| Metric | Value |

|---|---|

| Founded | 1997 |

| Total assets | RMB 1.12 trillion (end-2023) |

| Shaanxi population | 38.64 million (2020) |

| Ticker | 601128 |

What is included in the product

Provides a concise SWOT analysis of Bank of Xi'an, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic position and future growth prospects.

Provides a concise Bank of Xi'an SWOT matrix that highlights key risks and opportunities for rapid pain-point mitigation, enabling executives to prioritize strategic fixes quickly.

Weaknesses

Geographic concentration

Headquartered in Xi'an with core operations concentrated in Shaanxi, Bank of Xi'an faces heightened exposure to local shocks; regional economic downturns or sector slumps tend to transmit rapidly to its asset quality. Limited cross‑province diversification constrains risk spreading and makes loan book performance closely tied to Shaanxi’s economic trajectory. Growth prospects are therefore heavily dependent on the province’s macro cycle.

Scale disadvantage

Bank of Xi'an's sub-1 trillion RMB asset base leaves it far smaller than national banks that manage assets in the tens of trillions RMB, constraining pricing power on loans and deposits. Higher unit costs raise cost-to-income pressures relative to larger peers, squeezing efficiency ratios. Access to capital markets tends to be costlier and episodic, raising funding volatility. Marketing reach and talent attraction remain comparatively limited outside its regional footprint.

Technology gaps

Bank of Xi'an (SSE: 601128) trails leading fintechs and mega-banks in digital capabilities, with uneven user experience and limited depth in data analytics relative to mobile-first rivals. Slower innovation cycles increase risk of customer churn as younger users favor agile apps. IT modernization will require sizable, sustained investment to catch up and retain deposits and fee income.

Concentrated loan book

Concentrated loan book: Bank of Xi'an’s regional corporate and SME lending often clusters in sectors such as local real estate and infrastructure, increasing cyclical sensitivity and borrower reliance on municipal demand, while collateral values move together within the region, amplifying correlation and systemic credit risk.

- Regional sector clustering

- Overweight real estate/infrastructure

- High local demand dependence

- Regionally correlated collateral

Limited fee income

Reliance on interest income exposes earnings to NIM pressure; Bank of Xi'an’s non‑interest income was only about 19% of operating income in 2023, limiting buffer against margin compression.

Underdeveloped wealth, insurance and advisory fees cap ROE upside, while volatile trading and investment gains cannot reliably replace fee income, reducing overall resilience.

- Low non‑interest income ~19% (2023)

- High interest income dependence

- Weak wealth/insurance fees

- Volatile trading gains

Xi'an regional bank ≈0.97T RMB, 19% non‑interest income

Headquartered in Xi'an with core operations concentrated in Shaanxi, Bank of Xi'an (SSE:601128) has limited geographic diversification, a sub‑1 trillion RMB asset base and weaker digital/fee franchises, leaving earnings and asset quality highly tied to regional cycles; non‑interest income was about 19% of operating income in 2023.

| Metric | Value |

|---|---|

| Total assets (2023) | ≈0.97 trillion RMB |

| Non‑interest income (2023) | ≈19% |

Preview the Actual Deliverable

Bank of Xi'an SWOT Analysis

This is the actual Bank of Xi'an SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report; buy to unlock the entire, editable version. The file is structured, actionable and ready for immediate use.

Description

Go Beyond the Preview—Access the Full Strategic Report

Our SWOT snapshot of Bank of Xi'an highlights resilient regional market strength, growing digital adoption, margin pressure from competition, and regulatory sensitivity. The analysis pinpoints strategic opportunities in SME lending and fintech partnerships while flagging capital and asset-quality risks. Discover the complete picture behind the bank’s market position with our full SWOT analysis. Purchase the report for a ready-to-use, editable investor brief and Excel matrix.

Strengths

Strong regional franchise

Headquartered in Xi'an with roots dating to 1997, the bank benefits from strong brand recognition and trust across Shaanxi (population 38.64 million per 2020 census). Dense local branch coverage and long-standing client ties lower customer acquisition costs. Proximity to corporates and households enables faster credit decisions and tailored solutions. That embeddedness translates into relatively stable local deposit inflows.

Diversified product suite

Bank of Xi'an offers deposits, loans and payment/settlement services to retail and corporate clients, supporting daily banking and credit needs and boosting wallet share; total assets reached about RMB 1.12 trillion by end-2023. Multiple revenue streams—interest income plus fee income—reduce reliance on any single product, with net interest margin stabilization in recent quarters. Cross-selling across segments enhances customer lifetime value and retention.

SME and local insight

Bank of Xi'an's deep local and SME focus leverages intimate knowledge of regional industries to improve underwriting outcomes; Chinese SMEs contribute over 60% of GDP and about 80% of urban employment (recent official figures). Relationship managers capture soft information beyond financials, enabling faster turnarounds that boost customer stickiness, while niche SME expertise differentiates the bank from larger national competitors.

Stable core deposits

Bank of Xi'an's stable core deposits, anchored in a strong regional retail base in Shaanxi, supply low-cost funding that supports lending growth. Sticky transaction accounts enhance liquidity management and reduce reliance on wholesale markets. Lower funding costs help protect net interest margin and the deposit base boosts resilience during stress periods.

- Regional retail base: supports low-cost funding

- Sticky transaction accounts: steady liquidity

- Lower funding costs: protect NIM

- Deposit resilience: cushions stress

Government and SOE ties

Government and SOE linkages secure steady business flows for Bank of Xi'an, feeding project lending and transactional volumes; participation in regional infrastructure programs expands loan pipelines and fee income. Public-sector payments and payroll contracts help stabilize deposit bases, while alignment with local policy priorities can dampen credit volatility in targeted segments.

- ticker 601128 — strong municipal SOE ties

- regional projects → expanded lending

- public payrolls anchor deposits

- policy alignment reduces segment volatility

Xi'an-headquartered bank since 1997 with RMB 1.12T assets and sticky retail deposits

Headquartered in Xi'an since 1997, strong brand in Shaanxi (pop 38.64M) and dense branches yield stable retail deposits and low acquisition costs.

Total assets ~RMB 1.12 trillion (end-2023), diversified interest and fee income and resilient NIM from low funding costs.

Deep SME and SOE ties (ticker 601128) drive project lending, transactional volumes and sticky deposit flows.

| Metric | Value |

|---|---|

| Founded | 1997 |

| Total assets | RMB 1.12 trillion (end-2023) |

| Shaanxi population | 38.64 million (2020) |

| Ticker | 601128 |

What is included in the product

Provides a concise SWOT analysis of Bank of Xi'an, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess strategic position and future growth prospects.

Provides a concise Bank of Xi'an SWOT matrix that highlights key risks and opportunities for rapid pain-point mitigation, enabling executives to prioritize strategic fixes quickly.

Weaknesses

Geographic concentration

Headquartered in Xi'an with core operations concentrated in Shaanxi, Bank of Xi'an faces heightened exposure to local shocks; regional economic downturns or sector slumps tend to transmit rapidly to its asset quality. Limited cross‑province diversification constrains risk spreading and makes loan book performance closely tied to Shaanxi’s economic trajectory. Growth prospects are therefore heavily dependent on the province’s macro cycle.

Scale disadvantage

Bank of Xi'an's sub-1 trillion RMB asset base leaves it far smaller than national banks that manage assets in the tens of trillions RMB, constraining pricing power on loans and deposits. Higher unit costs raise cost-to-income pressures relative to larger peers, squeezing efficiency ratios. Access to capital markets tends to be costlier and episodic, raising funding volatility. Marketing reach and talent attraction remain comparatively limited outside its regional footprint.

Technology gaps

Bank of Xi'an (SSE: 601128) trails leading fintechs and mega-banks in digital capabilities, with uneven user experience and limited depth in data analytics relative to mobile-first rivals. Slower innovation cycles increase risk of customer churn as younger users favor agile apps. IT modernization will require sizable, sustained investment to catch up and retain deposits and fee income.

Concentrated loan book

Concentrated loan book: Bank of Xi'an’s regional corporate and SME lending often clusters in sectors such as local real estate and infrastructure, increasing cyclical sensitivity and borrower reliance on municipal demand, while collateral values move together within the region, amplifying correlation and systemic credit risk.

- Regional sector clustering

- Overweight real estate/infrastructure

- High local demand dependence

- Regionally correlated collateral

Limited fee income

Reliance on interest income exposes earnings to NIM pressure; Bank of Xi'an’s non‑interest income was only about 19% of operating income in 2023, limiting buffer against margin compression.

Underdeveloped wealth, insurance and advisory fees cap ROE upside, while volatile trading and investment gains cannot reliably replace fee income, reducing overall resilience.

- Low non‑interest income ~19% (2023)

- High interest income dependence

- Weak wealth/insurance fees

- Volatile trading gains

Xi'an regional bank ≈0.97T RMB, 19% non‑interest income

Headquartered in Xi'an with core operations concentrated in Shaanxi, Bank of Xi'an (SSE:601128) has limited geographic diversification, a sub‑1 trillion RMB asset base and weaker digital/fee franchises, leaving earnings and asset quality highly tied to regional cycles; non‑interest income was about 19% of operating income in 2023.

| Metric | Value |

|---|---|

| Total assets (2023) | ≈0.97 trillion RMB |

| Non‑interest income (2023) | ≈19% |

Preview the Actual Deliverable

Bank of Xi'an SWOT Analysis

This is the actual Bank of Xi'an SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report; buy to unlock the entire, editable version. The file is structured, actionable and ready for immediate use.