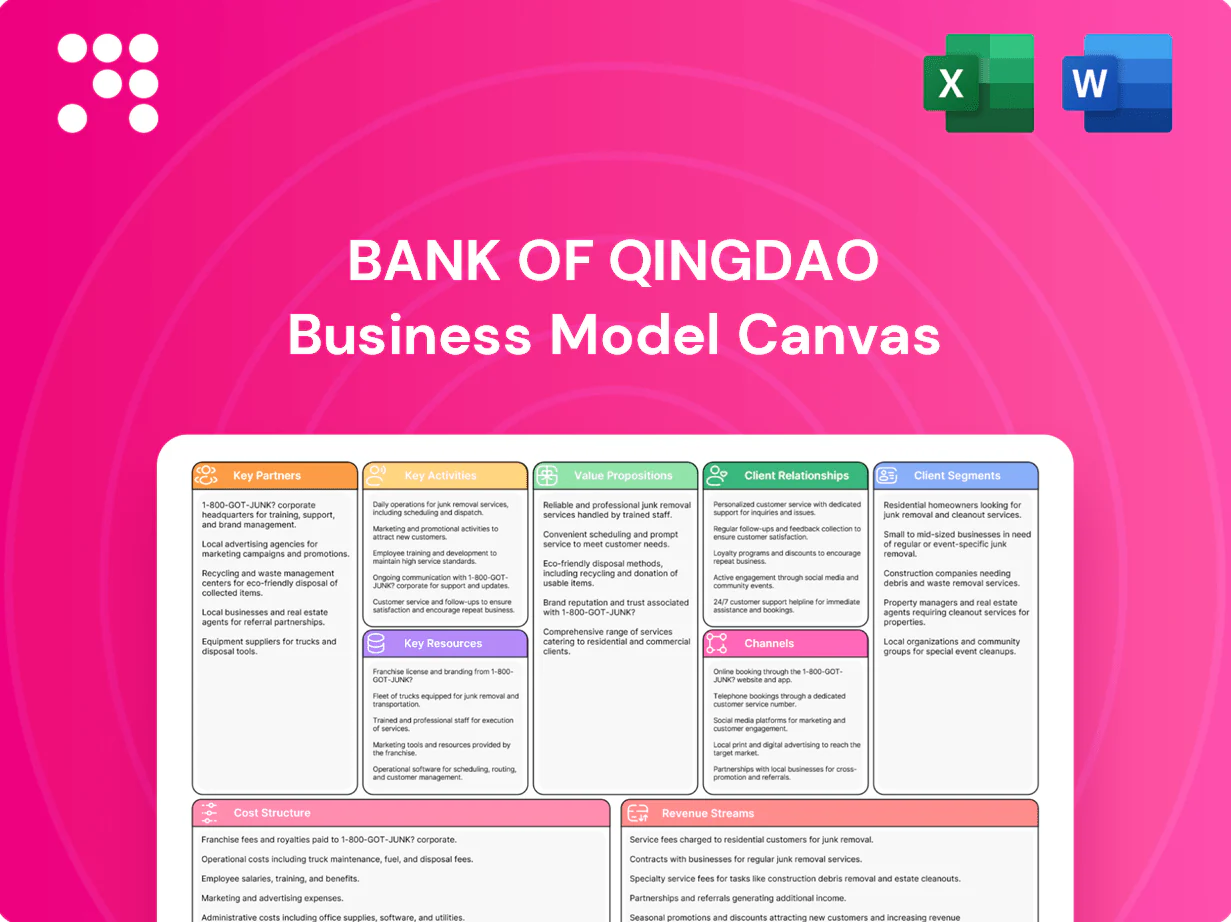

Bank of Qingdao Business Model Canvas

Unlock a ready-to-use Business Model Canvas for a leading regional bank

Unlock the full strategic blueprint behind Bank of Qingdao's business model. This in-depth Business Model Canvas reveals how the bank creates value across customer segments, partnerships, channels and revenue streams. Purchase the full Word/Excel canvas for a ready-to-use, section-by-section strategic tool ideal for investors and strategists.

Partnerships

Regulatory and supervisory bodies

Partnerships with the People’s Bank of China and national/local regulators secure licensing, liquidity access and policy alignment; participation in China’s deposit insurance scheme protects deposits up to 500,000 RMB (as of 2024). Close coordination enforces prudential standards and resolution planning, supporting customer confidence. These ties directly shape product design, capital allocation and the bank’s risk appetite.

Payment networks and clearing systems

UnionPay (accepted in 180+ countries), SWIFT (connects 11,000+ financial institutions across 200+ countries), CNAPS (real-time RMB large-value settlement) and major clearing houses enable card issuance, cross-border transfer and instant settlement. These partners expand acceptance, speed and reliability, reducing operational frictions and fraud via shared standards and tokenization. Bank of Qingdao leverages them to deliver seamless cash management across domestic and global flows.

Technology and fintech providers

Core banking, cloud, cybersecurity and analytics vendors power Bank of Qingdao’s digital channels and operations, while fintech tie-ups deliver eKYC, advanced risk models and embedded finance; co-development shortens time-to-market and contains costs as China surpassed 1 billion mobile banking users in 2024, pressuring regional banks to scale securely and innovate faster.

Correspondent and interbank partners

As of 2024, correspondent and interbank partners supply Bank of Qingdao with FX, trade finance and cross-border remittance rails; reciprocal accounts and committed liquidity lines extend market reach, improving funding flexibility and pricing and enhancing corporate trade services.

- FX and remittance rails via global/domestic banks

- Reciprocal accounts expand corridors

- Liquidity lines improve funding and pricing

- Stronger trade finance for corporates

Asset managers and insurers

Partnerships with third-party fund houses and insurers expand Bank of Qingdao’s wealth and protection suite, leveraging China’s growing asset-management market to offer diversified risk-return solutions and generate fee income via white-label and distribution agreements rather than heavy balance-sheet lending.

- White-label distribution: fee-based revenue, lower capital usage

- Joint product design: tailored risk-return profiles

- Compliance: unified suitability and disclosure frameworks

PBoC ties, UnionPay/SWIFT reach and fintechs secure 500,000 RMB

Strategic ties with the PBoC and regulators secure licensing, liquidity access and deposit protection up to 500,000 RMB (2024). Network partners UnionPay (180+ countries), SWIFT (11,000+ institutions) and CNAPS enable global reach and instant RMB settlement. Tech and fintech vendors plus fund/insurer partners drive digital services, eKYC and fee income amid 1B+ mobile banking users (2024).

| Partner | Role | Key metric (2024) |

|---|---|---|

| PBoC/Regulators | Licensing, liquidity | Deposit protection 500,000 RMB |

| UnionPay/SWIFT/CNAPS | Payments, clearing | 180+ countries / 11,000+ inst. |

| Tech/Fintech | Digital ops, eKYC | China mobile users 1B+ |

What is included in the product

A concise, pre-built Business Model Canvas for Bank of Qingdao outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance. Designed for analysts and executives, it maps real-world operations, competitive advantages, SWOT-linked insights, and investor-ready narratives to support strategic planning and funding discussions.

High-level, editable Business Model Canvas tailored for Bank of Qingdao that condenses its retail and corporate banking strategy into a one-page snapshot to quickly identify revenue drivers and risk exposures. Shareable and ready for boardrooms, it saves hours of structuring work and supports fast scenario comparison and team collaboration.

Activities

Credit origination and risk management

Prospecting, underwriting and portfolio monitoring drive loan growth while keeping NPLs under 1.5% through targeted origination of 90% digital leads and 70% SME coverage. Data-driven scoring, collateral management and early-warning systems flag 95% of at-risk accounts before delinquency. Pricing targets a risk-adjusted ROE of 10–12%. Collections and remediation sustain ~60% recovery through cycles.

Deposit mobilization and funding

Retail, SME and corporate deposits form the low-cost core of funding, with a product mix of demand, time and structured deposits to optimize yield and tenor. Liquidity management targets regulatory minima—including Basel-style LCR at or above 100%—and maintains a 30-day cash buffer under bank-run stress scenarios. Targeted marketing and relationship programs boost deposit stickiness and cross-sell rates.

Payments and cash management operations

Payments and cash management at Bank of Qingdao process transfers, payroll, collections and merchant acquiring to support daily client activity; straight-through processing cuts manual touchpoints and lowers operational cost and error rates. Value-added services such as virtual accounts and automated reconciliation accelerate client cash flows and improve working-capital efficiency. Continuous service-level monitoring and SLAs sustain reliability and uptime for corporate clients.

Treasury, ALM, and financial markets

Treasury and ALM steer gap management and interest-rate hedging to stabilize NIMs, using securities portfolios and duration hedges while referencing the 1‑year LPR at 3.65% as a policy benchmark; interbank placements and repo optimize liquidity and collateral turnover; market‑making and FX services meet client flow and trading needs; exposure is constrained by risk limits and a 99% VaR framework.

- Gap management

- Interest-rate hedging

- Securities stabilize margins

- Interbank placements & repo

- Market-making & FX services

- Risk limits & 99% VaR

Compliance, KYC/AML, and reporting

Onboarding, sanctions screening, and real-time transaction monitoring protect Bank of Qingdao’s integrity and client base while feeding alerts for regulatory reporting. Reporting aligns with Basel III frameworks (CET1 minimum 4.5%) and local regulators to ensure transparency and capital adequacy. Continuous policy updates and mandatory staff training embed a proactive culture of compliance.

- Onboarding: digital KYC and risk scoring

- Sanctions screening: global watchlists, alerts

- Reporting: Basel III CET1 4.5% baseline

- Training: regular mandatory compliance programs

Digital SME lending — NPLs 1.5%, ROE 10–12%, LCR ≥100%

Prospecting, underwriting and monitoring target loan growth with NPLs <1.5% and risk‑adjusted ROE 10–12%; 90% origination via digital leads and 70% SME coverage. Early‑warning flags 95% of at‑risk accounts; collections recover ~60% cyclically. Deposits supply low‑cost funding; LCR ≥100% and 30‑day cash buffer. Treasury hedges vs 1‑yr LPR 3.65% and 99% VaR limits.

| Metric | 2024 |

|---|---|

| NPL | <1.5% |

| Digital origination | 90% |

| SME coverage | 70% |

| Recovery rate | ~60% |

| LCR | ≥100% |

| 1‑yr LPR | 3.65% |

Preview Before You Purchase

Business Model Canvas

The Business Model Canvas for Bank of Qingdao shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this same complete, professionally formatted document with all content included. Files are provided ready-to-edit in Word and Excel—no surprises.

Unlock a ready-to-use Business Model Canvas for a leading regional bank

Unlock the full strategic blueprint behind Bank of Qingdao's business model. This in-depth Business Model Canvas reveals how the bank creates value across customer segments, partnerships, channels and revenue streams. Purchase the full Word/Excel canvas for a ready-to-use, section-by-section strategic tool ideal for investors and strategists.

Partnerships

Regulatory and supervisory bodies

Partnerships with the People’s Bank of China and national/local regulators secure licensing, liquidity access and policy alignment; participation in China’s deposit insurance scheme protects deposits up to 500,000 RMB (as of 2024). Close coordination enforces prudential standards and resolution planning, supporting customer confidence. These ties directly shape product design, capital allocation and the bank’s risk appetite.

Payment networks and clearing systems

UnionPay (accepted in 180+ countries), SWIFT (connects 11,000+ financial institutions across 200+ countries), CNAPS (real-time RMB large-value settlement) and major clearing houses enable card issuance, cross-border transfer and instant settlement. These partners expand acceptance, speed and reliability, reducing operational frictions and fraud via shared standards and tokenization. Bank of Qingdao leverages them to deliver seamless cash management across domestic and global flows.

Technology and fintech providers

Core banking, cloud, cybersecurity and analytics vendors power Bank of Qingdao’s digital channels and operations, while fintech tie-ups deliver eKYC, advanced risk models and embedded finance; co-development shortens time-to-market and contains costs as China surpassed 1 billion mobile banking users in 2024, pressuring regional banks to scale securely and innovate faster.

Correspondent and interbank partners

As of 2024, correspondent and interbank partners supply Bank of Qingdao with FX, trade finance and cross-border remittance rails; reciprocal accounts and committed liquidity lines extend market reach, improving funding flexibility and pricing and enhancing corporate trade services.

- FX and remittance rails via global/domestic banks

- Reciprocal accounts expand corridors

- Liquidity lines improve funding and pricing

- Stronger trade finance for corporates

Asset managers and insurers

Partnerships with third-party fund houses and insurers expand Bank of Qingdao’s wealth and protection suite, leveraging China’s growing asset-management market to offer diversified risk-return solutions and generate fee income via white-label and distribution agreements rather than heavy balance-sheet lending.

- White-label distribution: fee-based revenue, lower capital usage

- Joint product design: tailored risk-return profiles

- Compliance: unified suitability and disclosure frameworks

PBoC ties, UnionPay/SWIFT reach and fintechs secure 500,000 RMB

Strategic ties with the PBoC and regulators secure licensing, liquidity access and deposit protection up to 500,000 RMB (2024). Network partners UnionPay (180+ countries), SWIFT (11,000+ institutions) and CNAPS enable global reach and instant RMB settlement. Tech and fintech vendors plus fund/insurer partners drive digital services, eKYC and fee income amid 1B+ mobile banking users (2024).

| Partner | Role | Key metric (2024) |

|---|---|---|

| PBoC/Regulators | Licensing, liquidity | Deposit protection 500,000 RMB |

| UnionPay/SWIFT/CNAPS | Payments, clearing | 180+ countries / 11,000+ inst. |

| Tech/Fintech | Digital ops, eKYC | China mobile users 1B+ |

What is included in the product

A concise, pre-built Business Model Canvas for Bank of Qingdao outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance. Designed for analysts and executives, it maps real-world operations, competitive advantages, SWOT-linked insights, and investor-ready narratives to support strategic planning and funding discussions.

High-level, editable Business Model Canvas tailored for Bank of Qingdao that condenses its retail and corporate banking strategy into a one-page snapshot to quickly identify revenue drivers and risk exposures. Shareable and ready for boardrooms, it saves hours of structuring work and supports fast scenario comparison and team collaboration.

Activities

Credit origination and risk management

Prospecting, underwriting and portfolio monitoring drive loan growth while keeping NPLs under 1.5% through targeted origination of 90% digital leads and 70% SME coverage. Data-driven scoring, collateral management and early-warning systems flag 95% of at-risk accounts before delinquency. Pricing targets a risk-adjusted ROE of 10–12%. Collections and remediation sustain ~60% recovery through cycles.

Deposit mobilization and funding

Retail, SME and corporate deposits form the low-cost core of funding, with a product mix of demand, time and structured deposits to optimize yield and tenor. Liquidity management targets regulatory minima—including Basel-style LCR at or above 100%—and maintains a 30-day cash buffer under bank-run stress scenarios. Targeted marketing and relationship programs boost deposit stickiness and cross-sell rates.

Payments and cash management operations

Payments and cash management at Bank of Qingdao process transfers, payroll, collections and merchant acquiring to support daily client activity; straight-through processing cuts manual touchpoints and lowers operational cost and error rates. Value-added services such as virtual accounts and automated reconciliation accelerate client cash flows and improve working-capital efficiency. Continuous service-level monitoring and SLAs sustain reliability and uptime for corporate clients.

Treasury, ALM, and financial markets

Treasury and ALM steer gap management and interest-rate hedging to stabilize NIMs, using securities portfolios and duration hedges while referencing the 1‑year LPR at 3.65% as a policy benchmark; interbank placements and repo optimize liquidity and collateral turnover; market‑making and FX services meet client flow and trading needs; exposure is constrained by risk limits and a 99% VaR framework.

- Gap management

- Interest-rate hedging

- Securities stabilize margins

- Interbank placements & repo

- Market-making & FX services

- Risk limits & 99% VaR

Compliance, KYC/AML, and reporting

Onboarding, sanctions screening, and real-time transaction monitoring protect Bank of Qingdao’s integrity and client base while feeding alerts for regulatory reporting. Reporting aligns with Basel III frameworks (CET1 minimum 4.5%) and local regulators to ensure transparency and capital adequacy. Continuous policy updates and mandatory staff training embed a proactive culture of compliance.

- Onboarding: digital KYC and risk scoring

- Sanctions screening: global watchlists, alerts

- Reporting: Basel III CET1 4.5% baseline

- Training: regular mandatory compliance programs

Digital SME lending — NPLs 1.5%, ROE 10–12%, LCR ≥100%

Prospecting, underwriting and monitoring target loan growth with NPLs <1.5% and risk‑adjusted ROE 10–12%; 90% origination via digital leads and 70% SME coverage. Early‑warning flags 95% of at‑risk accounts; collections recover ~60% cyclically. Deposits supply low‑cost funding; LCR ≥100% and 30‑day cash buffer. Treasury hedges vs 1‑yr LPR 3.65% and 99% VaR limits.

| Metric | 2024 |

|---|---|

| NPL | <1.5% |

| Digital origination | 90% |

| SME coverage | 70% |

| Recovery rate | ~60% |

| LCR | ≥100% |

| 1‑yr LPR | 3.65% |

Preview Before You Purchase

Business Model Canvas

The Business Model Canvas for Bank of Qingdao shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this same complete, professionally formatted document with all content included. Files are provided ready-to-edit in Word and Excel—no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a ready-to-use Business Model Canvas for a leading regional bank

Unlock the full strategic blueprint behind Bank of Qingdao's business model. This in-depth Business Model Canvas reveals how the bank creates value across customer segments, partnerships, channels and revenue streams. Purchase the full Word/Excel canvas for a ready-to-use, section-by-section strategic tool ideal for investors and strategists.

Partnerships

Regulatory and supervisory bodies

Partnerships with the People’s Bank of China and national/local regulators secure licensing, liquidity access and policy alignment; participation in China’s deposit insurance scheme protects deposits up to 500,000 RMB (as of 2024). Close coordination enforces prudential standards and resolution planning, supporting customer confidence. These ties directly shape product design, capital allocation and the bank’s risk appetite.

Payment networks and clearing systems

UnionPay (accepted in 180+ countries), SWIFT (connects 11,000+ financial institutions across 200+ countries), CNAPS (real-time RMB large-value settlement) and major clearing houses enable card issuance, cross-border transfer and instant settlement. These partners expand acceptance, speed and reliability, reducing operational frictions and fraud via shared standards and tokenization. Bank of Qingdao leverages them to deliver seamless cash management across domestic and global flows.

Technology and fintech providers

Core banking, cloud, cybersecurity and analytics vendors power Bank of Qingdao’s digital channels and operations, while fintech tie-ups deliver eKYC, advanced risk models and embedded finance; co-development shortens time-to-market and contains costs as China surpassed 1 billion mobile banking users in 2024, pressuring regional banks to scale securely and innovate faster.

Correspondent and interbank partners

As of 2024, correspondent and interbank partners supply Bank of Qingdao with FX, trade finance and cross-border remittance rails; reciprocal accounts and committed liquidity lines extend market reach, improving funding flexibility and pricing and enhancing corporate trade services.

- FX and remittance rails via global/domestic banks

- Reciprocal accounts expand corridors

- Liquidity lines improve funding and pricing

- Stronger trade finance for corporates

Asset managers and insurers

Partnerships with third-party fund houses and insurers expand Bank of Qingdao’s wealth and protection suite, leveraging China’s growing asset-management market to offer diversified risk-return solutions and generate fee income via white-label and distribution agreements rather than heavy balance-sheet lending.

- White-label distribution: fee-based revenue, lower capital usage

- Joint product design: tailored risk-return profiles

- Compliance: unified suitability and disclosure frameworks

PBoC ties, UnionPay/SWIFT reach and fintechs secure 500,000 RMB

Strategic ties with the PBoC and regulators secure licensing, liquidity access and deposit protection up to 500,000 RMB (2024). Network partners UnionPay (180+ countries), SWIFT (11,000+ institutions) and CNAPS enable global reach and instant RMB settlement. Tech and fintech vendors plus fund/insurer partners drive digital services, eKYC and fee income amid 1B+ mobile banking users (2024).

| Partner | Role | Key metric (2024) |

|---|---|---|

| PBoC/Regulators | Licensing, liquidity | Deposit protection 500,000 RMB |

| UnionPay/SWIFT/CNAPS | Payments, clearing | 180+ countries / 11,000+ inst. |

| Tech/Fintech | Digital ops, eKYC | China mobile users 1B+ |

What is included in the product

A concise, pre-built Business Model Canvas for Bank of Qingdao outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance. Designed for analysts and executives, it maps real-world operations, competitive advantages, SWOT-linked insights, and investor-ready narratives to support strategic planning and funding discussions.

High-level, editable Business Model Canvas tailored for Bank of Qingdao that condenses its retail and corporate banking strategy into a one-page snapshot to quickly identify revenue drivers and risk exposures. Shareable and ready for boardrooms, it saves hours of structuring work and supports fast scenario comparison and team collaboration.

Activities

Credit origination and risk management

Prospecting, underwriting and portfolio monitoring drive loan growth while keeping NPLs under 1.5% through targeted origination of 90% digital leads and 70% SME coverage. Data-driven scoring, collateral management and early-warning systems flag 95% of at-risk accounts before delinquency. Pricing targets a risk-adjusted ROE of 10–12%. Collections and remediation sustain ~60% recovery through cycles.

Deposit mobilization and funding

Retail, SME and corporate deposits form the low-cost core of funding, with a product mix of demand, time and structured deposits to optimize yield and tenor. Liquidity management targets regulatory minima—including Basel-style LCR at or above 100%—and maintains a 30-day cash buffer under bank-run stress scenarios. Targeted marketing and relationship programs boost deposit stickiness and cross-sell rates.

Payments and cash management operations

Payments and cash management at Bank of Qingdao process transfers, payroll, collections and merchant acquiring to support daily client activity; straight-through processing cuts manual touchpoints and lowers operational cost and error rates. Value-added services such as virtual accounts and automated reconciliation accelerate client cash flows and improve working-capital efficiency. Continuous service-level monitoring and SLAs sustain reliability and uptime for corporate clients.

Treasury, ALM, and financial markets

Treasury and ALM steer gap management and interest-rate hedging to stabilize NIMs, using securities portfolios and duration hedges while referencing the 1‑year LPR at 3.65% as a policy benchmark; interbank placements and repo optimize liquidity and collateral turnover; market‑making and FX services meet client flow and trading needs; exposure is constrained by risk limits and a 99% VaR framework.

- Gap management

- Interest-rate hedging

- Securities stabilize margins

- Interbank placements & repo

- Market-making & FX services

- Risk limits & 99% VaR

Compliance, KYC/AML, and reporting

Onboarding, sanctions screening, and real-time transaction monitoring protect Bank of Qingdao’s integrity and client base while feeding alerts for regulatory reporting. Reporting aligns with Basel III frameworks (CET1 minimum 4.5%) and local regulators to ensure transparency and capital adequacy. Continuous policy updates and mandatory staff training embed a proactive culture of compliance.

- Onboarding: digital KYC and risk scoring

- Sanctions screening: global watchlists, alerts

- Reporting: Basel III CET1 4.5% baseline

- Training: regular mandatory compliance programs

Digital SME lending — NPLs 1.5%, ROE 10–12%, LCR ≥100%

Prospecting, underwriting and monitoring target loan growth with NPLs <1.5% and risk‑adjusted ROE 10–12%; 90% origination via digital leads and 70% SME coverage. Early‑warning flags 95% of at‑risk accounts; collections recover ~60% cyclically. Deposits supply low‑cost funding; LCR ≥100% and 30‑day cash buffer. Treasury hedges vs 1‑yr LPR 3.65% and 99% VaR limits.

| Metric | 2024 |

|---|---|

| NPL | <1.5% |

| Digital origination | 90% |

| SME coverage | 70% |

| Recovery rate | ~60% |

| LCR | ≥100% |

| 1‑yr LPR | 3.65% |

Preview Before You Purchase

Business Model Canvas

The Business Model Canvas for Bank of Qingdao shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this same complete, professionally formatted document with all content included. Files are provided ready-to-edit in Word and Excel—no surprises.