Southern Bank Business Model Canvas

Unlock a bank Business Model Canvas: customers, value propositions, partners, revenue

Unlock Southern Bank’s strategic blueprint with our Business Model Canvas—detailing customer segments, value propositions, key partnerships and revenue mechanics. Perfect for investors, advisors, and founders seeking actionable insights. Purchase the full, editable Word/Excel canvas to benchmark and plan.

Partnerships

Fintech vendors

Partnerships with core banking, digital onboarding, and fraud-prevention vendors let Southern Bank scale features fast as mobile banking adoption hit 78% in 2024; vendors deliver mobile UI, instant payments rails and analytics without heavy in-house build. Integrations cut time-to-market an estimated 30–50% while preserving compliance. SLAs and roadmap alignment target 99.9% uptime and future-proofing.

Payment networks

Alliances with Visa and Mastercard and processors enable debit, credit and ACH services, securing settlements and standardized chargeback handling via network rules; Visa and Mastercard together account for roughly 75–80% of global card volume in 2024. Co-branded cards deepen loyalty and commonly lift interchange revenue 20–30% and cardholder spend by ~15%. Access to tokenization and expanding real-time rails (RTP/ISO 20022 adoption) accelerates instant, secure payments and improves UX.

Correspondent banks

Correspondent banks provide liquidity, cash management and specialty services, supporting wire clearing, FX and participation loans that help Southern Bank manage balance-sheet risks and scale operations. In 2024 global syndicated loan volume was about $1.03 trillion, enabling access to larger syndicated credits for clients. These ties reduce funding volatility and expand product reach.

Realtors & brokers

Local real estate agents and mortgage brokers feed qualified home-loan referrals, with NAR 2024 reporting about 89% of buyers use an agent, boosting purchase-originations into Southern Bank’s pipeline; joint education events and co-branded seminars build brand trust and lift referral conversion. Streamlined referral workflows shorten approval-to-closing times, increasing cross-sell into deposits and insurance-like protections and improving LTV retention.

- Referral volume: agent-sourced mortgages

- Trust: joint education events

- Speed: streamlined workflows

- Revenue: cross-sell into deposits & insurance

Community groups

Community groups such as chambers, nonprofits, and schools expand Southern Bank’s reach and credibility across local networks; there are over 7,000 chambers of commerce in the US, and community banks supply roughly 45% of small-business loans under $1M (ICBA 2024). Financial literacy programs build goodwill and a future customer pipeline, while sponsorships and local events provide warm introductions that reinforce the bank’s community-first positioning.

- Chambers: local networks, 7,000+ US chambers

- Small-business lending: ~45% of loans under $1M (ICBA 2024)

- Financial literacy: goodwill + pipeline

- Sponsorships/events: warm referrals, community-first brand

US mobile banking 78%; vendors cut time-to-market 30-50%

Vendors accelerate mobile features as US mobile banking adoption hit 78% in 2024; integrations cut time-to-market ~30–50% with 99.9% SLA targets. Card networks (Visa/Mastercard ~75–80% share) boost interchange +20–30% and card spend ~15%. Correspondent banks underpin liquidity (global syndicated loans $1.03T in 2024). Agents drive originations (89% buyers use agents); community banks fund ~45% of small loans under $1M (ICBA 2024).

| Partner | Benefit | 2024 metric |

|---|---|---|

| Vendors | Faster features, uptime | 78% mobile adoption; 30–50% faster |

| Card Networks | Revenue & UX | 75–80% share; +20–30% interchange |

| Correspondents | Liquidity | $1.03T syndicated loans |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Southern Bank’s strategy, organized into the nine classic BMC blocks with full narrative and insights. It covers customer segments, channels, value propositions, revenue and cost structures, includes competitive advantages, SWOT-linked analysis, and is ideal for presentations, funding discussions, and strategic decision-making.

High-level, editable Business Model Canvas that quickly relieves pain by consolidating Southern Bank’s lending products, customer segments, and compliance needs into a single, shareable page for faster decision-making and team alignment.

Activities

Deposit gathering

Design checking, savings and CDs to attract stable, low-cost funding by tiered relationship pricing and term CD promotions aligned with 1-year Treasury yields near 4.5% in 2024 and FDIC insurance limits of 250,000. Run targeted digital campaigns and branch outreach to grow core balances, using segment pricing to increase sticky deposits. Manage rates and product features to retain customers and maintain ALM liquidity buffers in compliance with regulatory guidance.

Loan origination

Marketing, underwriting and closing for mortgages, consumer and commercial loans combine streamlined policy-based credit scoring with manual judgment on complex files to maintain speed and accuracy; community banks in 2024 continued to prioritize local decisioning to preserve relationships.

Fast, local decisions—often within 48–72 hours for standard files—differentiate service and support conversion in competitive markets.

Ongoing portfolio monitoring and stress-testing kept asset quality a focus in 2024, with community-bank nonperforming loan ratios targeted below 1% through proactive workout and surveillance.

Risk management

Southern Bank's credit, market, liquidity and operational risk frameworks maintain capital and liquidity targets (CET1 >10.5%, LCR >100%) and limit concentrations. Compliance programs cover BSA/AML, KYC and fair lending with quarterly SAR review; bank runs quarterly stress tests and annual loan reviews, with monthly monitoring of high‑risk credits. Cybersecurity spending reflects industry norms given average breach cost $4.45M (2024) and targets 99.9% uptime.

Relationship banking

Relationship banking drives proactive outreach to individuals and businesses to uncover needs, increasing cross-sell across deposits, loans and wealth solutions and leveraging Southern Bank’s community branches where community banks originated roughly half of US small-business loans in 2024 (FDIC).

- Proactive outreach

- Cross-sell: deposits, loans, wealth

- Community presence = referrals

- Service recovery → loyalty

Wealth advisory

- Goal-based advice

- Integrated banking and portfolios

- Fiduciary oversight, transparent fees

- Ongoing reviews

Price deposits to 1-yr Treasury 4.5%, grow deposits, CET1>10.5%, NPLs<1%

Design and price deposits to secure low-cost funding (1-yr Treasury ~4.5% in 2024; FDIC cap 250,000), grow core balances via digital+branch campaigns, manage ALM/liquidity buffers. Originate mortgages, consumer and commercial loans with 48–72h decisions, maintain NPLs <1% through monitoring. Maintain CET1 >10.5%, LCR >100%, robust BSA/AML and cybersecurity (avg breach cost 4.45M).

| Metric | 2024 |

|---|---|

| 1-yr Treasury | ~4.5% |

| FDIC limit | $250,000 |

| NPL target | <1% |

| CET1 | >10.5% |

| Wealth AUM | $32T |

Delivered as Displayed

Business Model Canvas

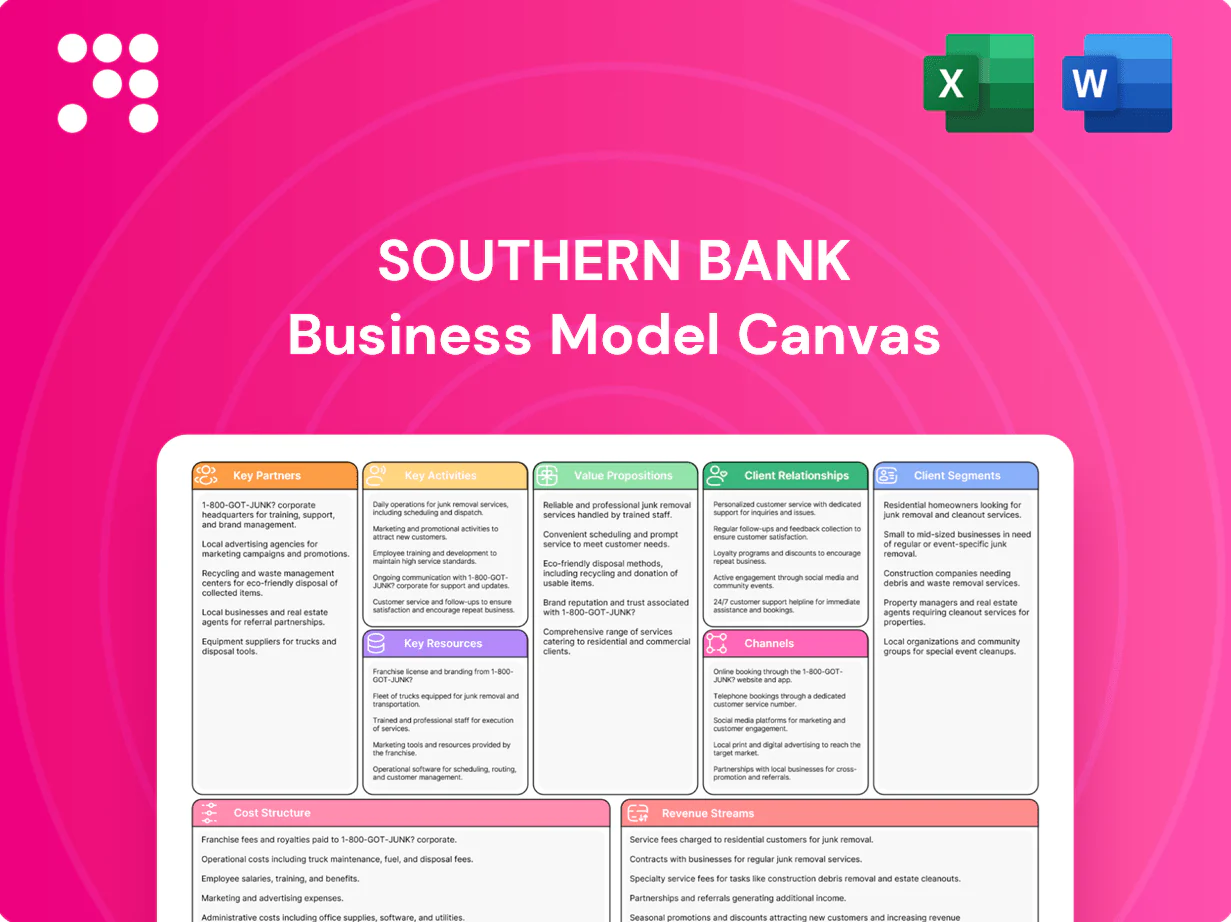

The Southern Bank Business Model Canvas shown here is the exact file you’ll receive after purchase, not a mockup or sample. This preview reflects the full deliverable—formatted, editable, and ready-to-use. Upon checkout you’ll instantly download the same complete document in Word and Excel formats. No surprises.

Unlock a bank Business Model Canvas: customers, value propositions, partners, revenue

Unlock Southern Bank’s strategic blueprint with our Business Model Canvas—detailing customer segments, value propositions, key partnerships and revenue mechanics. Perfect for investors, advisors, and founders seeking actionable insights. Purchase the full, editable Word/Excel canvas to benchmark and plan.

Partnerships

Fintech vendors

Partnerships with core banking, digital onboarding, and fraud-prevention vendors let Southern Bank scale features fast as mobile banking adoption hit 78% in 2024; vendors deliver mobile UI, instant payments rails and analytics without heavy in-house build. Integrations cut time-to-market an estimated 30–50% while preserving compliance. SLAs and roadmap alignment target 99.9% uptime and future-proofing.

Payment networks

Alliances with Visa and Mastercard and processors enable debit, credit and ACH services, securing settlements and standardized chargeback handling via network rules; Visa and Mastercard together account for roughly 75–80% of global card volume in 2024. Co-branded cards deepen loyalty and commonly lift interchange revenue 20–30% and cardholder spend by ~15%. Access to tokenization and expanding real-time rails (RTP/ISO 20022 adoption) accelerates instant, secure payments and improves UX.

Correspondent banks

Correspondent banks provide liquidity, cash management and specialty services, supporting wire clearing, FX and participation loans that help Southern Bank manage balance-sheet risks and scale operations. In 2024 global syndicated loan volume was about $1.03 trillion, enabling access to larger syndicated credits for clients. These ties reduce funding volatility and expand product reach.

Realtors & brokers

Local real estate agents and mortgage brokers feed qualified home-loan referrals, with NAR 2024 reporting about 89% of buyers use an agent, boosting purchase-originations into Southern Bank’s pipeline; joint education events and co-branded seminars build brand trust and lift referral conversion. Streamlined referral workflows shorten approval-to-closing times, increasing cross-sell into deposits and insurance-like protections and improving LTV retention.

- Referral volume: agent-sourced mortgages

- Trust: joint education events

- Speed: streamlined workflows

- Revenue: cross-sell into deposits & insurance

Community groups

Community groups such as chambers, nonprofits, and schools expand Southern Bank’s reach and credibility across local networks; there are over 7,000 chambers of commerce in the US, and community banks supply roughly 45% of small-business loans under $1M (ICBA 2024). Financial literacy programs build goodwill and a future customer pipeline, while sponsorships and local events provide warm introductions that reinforce the bank’s community-first positioning.

- Chambers: local networks, 7,000+ US chambers

- Small-business lending: ~45% of loans under $1M (ICBA 2024)

- Financial literacy: goodwill + pipeline

- Sponsorships/events: warm referrals, community-first brand

US mobile banking 78%; vendors cut time-to-market 30-50%

Vendors accelerate mobile features as US mobile banking adoption hit 78% in 2024; integrations cut time-to-market ~30–50% with 99.9% SLA targets. Card networks (Visa/Mastercard ~75–80% share) boost interchange +20–30% and card spend ~15%. Correspondent banks underpin liquidity (global syndicated loans $1.03T in 2024). Agents drive originations (89% buyers use agents); community banks fund ~45% of small loans under $1M (ICBA 2024).

| Partner | Benefit | 2024 metric |

|---|---|---|

| Vendors | Faster features, uptime | 78% mobile adoption; 30–50% faster |

| Card Networks | Revenue & UX | 75–80% share; +20–30% interchange |

| Correspondents | Liquidity | $1.03T syndicated loans |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Southern Bank’s strategy, organized into the nine classic BMC blocks with full narrative and insights. It covers customer segments, channels, value propositions, revenue and cost structures, includes competitive advantages, SWOT-linked analysis, and is ideal for presentations, funding discussions, and strategic decision-making.

High-level, editable Business Model Canvas that quickly relieves pain by consolidating Southern Bank’s lending products, customer segments, and compliance needs into a single, shareable page for faster decision-making and team alignment.

Activities

Deposit gathering

Design checking, savings and CDs to attract stable, low-cost funding by tiered relationship pricing and term CD promotions aligned with 1-year Treasury yields near 4.5% in 2024 and FDIC insurance limits of 250,000. Run targeted digital campaigns and branch outreach to grow core balances, using segment pricing to increase sticky deposits. Manage rates and product features to retain customers and maintain ALM liquidity buffers in compliance with regulatory guidance.

Loan origination

Marketing, underwriting and closing for mortgages, consumer and commercial loans combine streamlined policy-based credit scoring with manual judgment on complex files to maintain speed and accuracy; community banks in 2024 continued to prioritize local decisioning to preserve relationships.

Fast, local decisions—often within 48–72 hours for standard files—differentiate service and support conversion in competitive markets.

Ongoing portfolio monitoring and stress-testing kept asset quality a focus in 2024, with community-bank nonperforming loan ratios targeted below 1% through proactive workout and surveillance.

Risk management

Southern Bank's credit, market, liquidity and operational risk frameworks maintain capital and liquidity targets (CET1 >10.5%, LCR >100%) and limit concentrations. Compliance programs cover BSA/AML, KYC and fair lending with quarterly SAR review; bank runs quarterly stress tests and annual loan reviews, with monthly monitoring of high‑risk credits. Cybersecurity spending reflects industry norms given average breach cost $4.45M (2024) and targets 99.9% uptime.

Relationship banking

Relationship banking drives proactive outreach to individuals and businesses to uncover needs, increasing cross-sell across deposits, loans and wealth solutions and leveraging Southern Bank’s community branches where community banks originated roughly half of US small-business loans in 2024 (FDIC).

- Proactive outreach

- Cross-sell: deposits, loans, wealth

- Community presence = referrals

- Service recovery → loyalty

Wealth advisory

- Goal-based advice

- Integrated banking and portfolios

- Fiduciary oversight, transparent fees

- Ongoing reviews

Price deposits to 1-yr Treasury 4.5%, grow deposits, CET1>10.5%, NPLs<1%

Design and price deposits to secure low-cost funding (1-yr Treasury ~4.5% in 2024; FDIC cap 250,000), grow core balances via digital+branch campaigns, manage ALM/liquidity buffers. Originate mortgages, consumer and commercial loans with 48–72h decisions, maintain NPLs <1% through monitoring. Maintain CET1 >10.5%, LCR >100%, robust BSA/AML and cybersecurity (avg breach cost 4.45M).

| Metric | 2024 |

|---|---|

| 1-yr Treasury | ~4.5% |

| FDIC limit | $250,000 |

| NPL target | <1% |

| CET1 | >10.5% |

| Wealth AUM | $32T |

Delivered as Displayed

Business Model Canvas

The Southern Bank Business Model Canvas shown here is the exact file you’ll receive after purchase, not a mockup or sample. This preview reflects the full deliverable—formatted, editable, and ready-to-use. Upon checkout you’ll instantly download the same complete document in Word and Excel formats. No surprises.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a bank Business Model Canvas: customers, value propositions, partners, revenue

Unlock Southern Bank’s strategic blueprint with our Business Model Canvas—detailing customer segments, value propositions, key partnerships and revenue mechanics. Perfect for investors, advisors, and founders seeking actionable insights. Purchase the full, editable Word/Excel canvas to benchmark and plan.

Partnerships

Fintech vendors

Partnerships with core banking, digital onboarding, and fraud-prevention vendors let Southern Bank scale features fast as mobile banking adoption hit 78% in 2024; vendors deliver mobile UI, instant payments rails and analytics without heavy in-house build. Integrations cut time-to-market an estimated 30–50% while preserving compliance. SLAs and roadmap alignment target 99.9% uptime and future-proofing.

Payment networks

Alliances with Visa and Mastercard and processors enable debit, credit and ACH services, securing settlements and standardized chargeback handling via network rules; Visa and Mastercard together account for roughly 75–80% of global card volume in 2024. Co-branded cards deepen loyalty and commonly lift interchange revenue 20–30% and cardholder spend by ~15%. Access to tokenization and expanding real-time rails (RTP/ISO 20022 adoption) accelerates instant, secure payments and improves UX.

Correspondent banks

Correspondent banks provide liquidity, cash management and specialty services, supporting wire clearing, FX and participation loans that help Southern Bank manage balance-sheet risks and scale operations. In 2024 global syndicated loan volume was about $1.03 trillion, enabling access to larger syndicated credits for clients. These ties reduce funding volatility and expand product reach.

Realtors & brokers

Local real estate agents and mortgage brokers feed qualified home-loan referrals, with NAR 2024 reporting about 89% of buyers use an agent, boosting purchase-originations into Southern Bank’s pipeline; joint education events and co-branded seminars build brand trust and lift referral conversion. Streamlined referral workflows shorten approval-to-closing times, increasing cross-sell into deposits and insurance-like protections and improving LTV retention.

- Referral volume: agent-sourced mortgages

- Trust: joint education events

- Speed: streamlined workflows

- Revenue: cross-sell into deposits & insurance

Community groups

Community groups such as chambers, nonprofits, and schools expand Southern Bank’s reach and credibility across local networks; there are over 7,000 chambers of commerce in the US, and community banks supply roughly 45% of small-business loans under $1M (ICBA 2024). Financial literacy programs build goodwill and a future customer pipeline, while sponsorships and local events provide warm introductions that reinforce the bank’s community-first positioning.

- Chambers: local networks, 7,000+ US chambers

- Small-business lending: ~45% of loans under $1M (ICBA 2024)

- Financial literacy: goodwill + pipeline

- Sponsorships/events: warm referrals, community-first brand

US mobile banking 78%; vendors cut time-to-market 30-50%

Vendors accelerate mobile features as US mobile banking adoption hit 78% in 2024; integrations cut time-to-market ~30–50% with 99.9% SLA targets. Card networks (Visa/Mastercard ~75–80% share) boost interchange +20–30% and card spend ~15%. Correspondent banks underpin liquidity (global syndicated loans $1.03T in 2024). Agents drive originations (89% buyers use agents); community banks fund ~45% of small loans under $1M (ICBA 2024).

| Partner | Benefit | 2024 metric |

|---|---|---|

| Vendors | Faster features, uptime | 78% mobile adoption; 30–50% faster |

| Card Networks | Revenue & UX | 75–80% share; +20–30% interchange |

| Correspondents | Liquidity | $1.03T syndicated loans |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Southern Bank’s strategy, organized into the nine classic BMC blocks with full narrative and insights. It covers customer segments, channels, value propositions, revenue and cost structures, includes competitive advantages, SWOT-linked analysis, and is ideal for presentations, funding discussions, and strategic decision-making.

High-level, editable Business Model Canvas that quickly relieves pain by consolidating Southern Bank’s lending products, customer segments, and compliance needs into a single, shareable page for faster decision-making and team alignment.

Activities

Deposit gathering

Design checking, savings and CDs to attract stable, low-cost funding by tiered relationship pricing and term CD promotions aligned with 1-year Treasury yields near 4.5% in 2024 and FDIC insurance limits of 250,000. Run targeted digital campaigns and branch outreach to grow core balances, using segment pricing to increase sticky deposits. Manage rates and product features to retain customers and maintain ALM liquidity buffers in compliance with regulatory guidance.

Loan origination

Marketing, underwriting and closing for mortgages, consumer and commercial loans combine streamlined policy-based credit scoring with manual judgment on complex files to maintain speed and accuracy; community banks in 2024 continued to prioritize local decisioning to preserve relationships.

Fast, local decisions—often within 48–72 hours for standard files—differentiate service and support conversion in competitive markets.

Ongoing portfolio monitoring and stress-testing kept asset quality a focus in 2024, with community-bank nonperforming loan ratios targeted below 1% through proactive workout and surveillance.

Risk management

Southern Bank's credit, market, liquidity and operational risk frameworks maintain capital and liquidity targets (CET1 >10.5%, LCR >100%) and limit concentrations. Compliance programs cover BSA/AML, KYC and fair lending with quarterly SAR review; bank runs quarterly stress tests and annual loan reviews, with monthly monitoring of high‑risk credits. Cybersecurity spending reflects industry norms given average breach cost $4.45M (2024) and targets 99.9% uptime.

Relationship banking

Relationship banking drives proactive outreach to individuals and businesses to uncover needs, increasing cross-sell across deposits, loans and wealth solutions and leveraging Southern Bank’s community branches where community banks originated roughly half of US small-business loans in 2024 (FDIC).

- Proactive outreach

- Cross-sell: deposits, loans, wealth

- Community presence = referrals

- Service recovery → loyalty

Wealth advisory

- Goal-based advice

- Integrated banking and portfolios

- Fiduciary oversight, transparent fees

- Ongoing reviews

Price deposits to 1-yr Treasury 4.5%, grow deposits, CET1>10.5%, NPLs<1%

Design and price deposits to secure low-cost funding (1-yr Treasury ~4.5% in 2024; FDIC cap 250,000), grow core balances via digital+branch campaigns, manage ALM/liquidity buffers. Originate mortgages, consumer and commercial loans with 48–72h decisions, maintain NPLs <1% through monitoring. Maintain CET1 >10.5%, LCR >100%, robust BSA/AML and cybersecurity (avg breach cost 4.45M).

| Metric | 2024 |

|---|---|

| 1-yr Treasury | ~4.5% |

| FDIC limit | $250,000 |

| NPL target | <1% |

| CET1 | >10.5% |

| Wealth AUM | $32T |

Delivered as Displayed

Business Model Canvas

The Southern Bank Business Model Canvas shown here is the exact file you’ll receive after purchase, not a mockup or sample. This preview reflects the full deliverable—formatted, editable, and ready-to-use. Upon checkout you’ll instantly download the same complete document in Word and Excel formats. No surprises.