Southern Bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

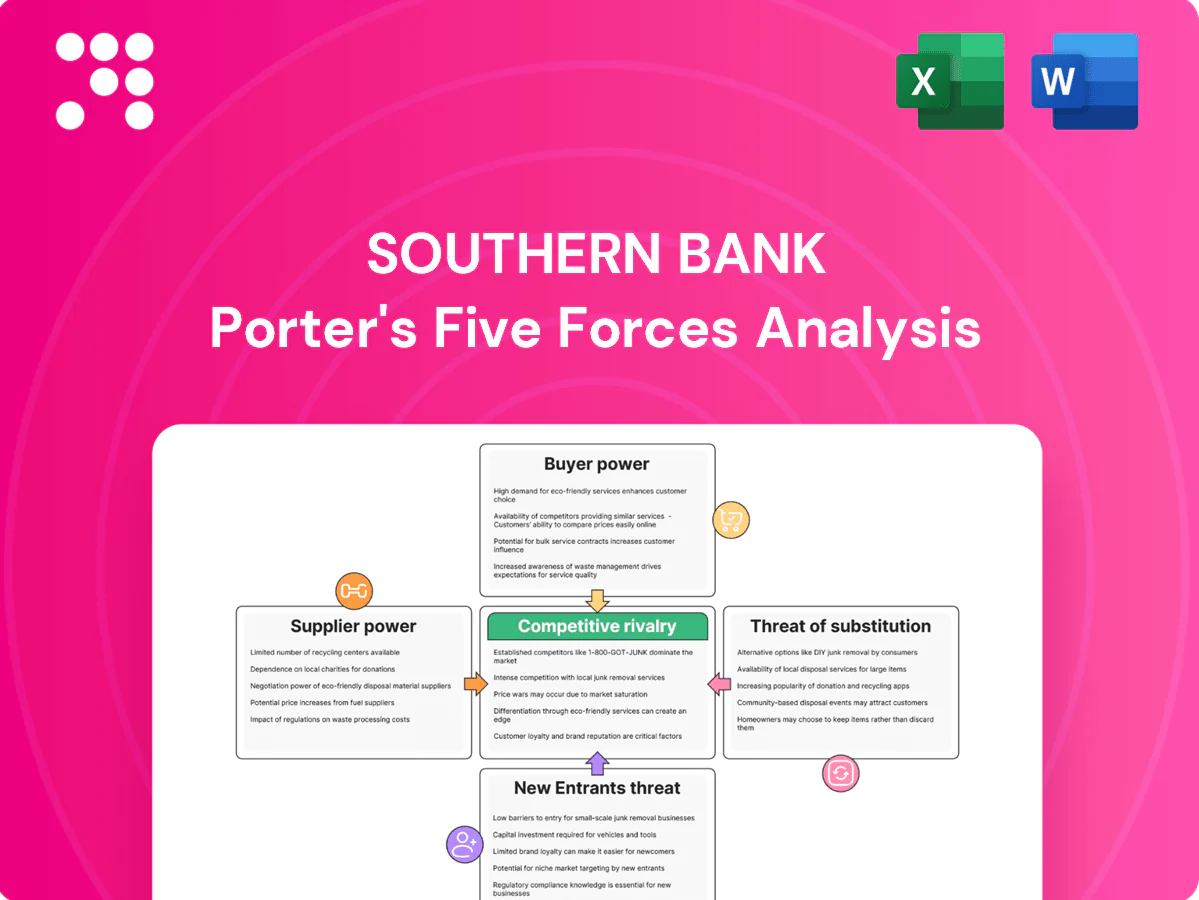

Southern Bank’s Porter's Five Forces snapshot highlights competitive pressures across buyer power, supplier influence, substitutes and entry threats, plus rivalry intensity. It reveals where margins and growth are most at risk. This brief teases strategic implications and gaps. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Concentrated core banking vendors

Core processors FIS, Fiserv and Jack Henry remain the dominant US providers in 2024, collectively accounting for the majority of bank core relationships, giving them pricing and contract leverage; vendor switching is costly, risky and operationally disruptive, often taking months and millions in migration costs, and Southern Bank’s dependence on these platforms heightens supplier power while its smaller scale limits bargaining for favorable SLAs.

Funding suppliers and wholesale lines

Funding suppliers — depositors, FHLB advances and brokered CDs — supplied a material share of Southern Bank’s balance-sheet funding in 2024, with non-core sources estimated near 18–22% of liabilities, elevating supplier leverage. In tight liquidity cycles 2024 wholesale rates rose sharply and FHLB covenants tightened, boosting supplier power and cost of funds volatility. Strong local deposit franchises mitigated but did not eliminate this exposure.

Payment networks and card schemes

Visa and Mastercard control over 80% of U.S. card volume in 2024 and, together with ACH rules, set interchange and network fees that Southern Bank has little leverage to change. Interchange typically runs 1.5–2.5% for credit plus assessments of $0.02–$0.30 per txn, largely non‑negotiable for small banks. Scale advantages accrue to the largest issuers (top 10 hold ~60% of accounts), forcing Southern to accept standardized economics to remain interoperable.

Talent and specialized services

Credit underwriters, commercial lenders and compliance officers are scarce locally, raising supplier power as banks compete; BLS 2024 data shows average hourly earnings up about 4.1% YoY, fueling wage inflation and poaching by larger banks. Outsourced compliance, cybersecurity and audit firms command premium rates, and retention and signing bonuses (often 10–25% of base pay) partially mitigate turnover but raise cost per hire.

- Talent scarcity: higher bargaining power

- Wage inflation: BLS 2024 avg +4.1% YoY

- Outsourced services: premium fees

- Retention programs: costly (10–25% bonuses)

Data, cloud, and fintech partners

APIs, analytics, and cloud services are central to Southern Bank’s digital customer experience, but major cloud providers and leading fintechs—which held roughly two-thirds of global cloud market share in 2024—can impose standardized pricing and terms that squeeze margins. Deep integration dependencies create switching frictions and potential vendor lock-in. Co-innovation exists but typically skews value capture toward the platform owner.

- APIs: dependency and lock-in

- Cloud: ~two-thirds market share (2024)

- Fintechs: standardized commercial terms

- Co-innovation: platform owner advantage

Core processors, >80% card share, 18-22% non-core debt

Core processors (FIS, Fiserv, Jack Henry) dominate US cores in 2024, creating high switching costs and contract leverage for suppliers. Non‑core funding (FHLB, brokered CDs) comprised ~18–22% of liabilities in 2024, raising funding supplier power. Visa/Mastercard control >80% of US card volume and cloud providers held ~66% market share in 2024; BLS wage inflation +4.1% YoY.

| Supplier | 2024 metric |

|---|---|

| Core processors | Majority market share |

| Non-core funding | 18–22% liabilities |

| Card networks | >80% U.S. volume |

| Cloud providers | ~66% market share |

| Wage inflation | +4.1% YoY |

What is included in the product

Tailored Porter's Five Forces analysis for Southern Bank, uncovering key competitive drivers, customer and supplier influence on pricing, and market entry barriers that protect incumbents. Identifies disruptive threats, substitutes, and strategic levers Southern Bank can use to defend or grow its market position.

A concise one-sheet Porter's Five Forces for Southern Bank that visualizes strategic pressure with a spider chart, lets you customize force levels by new data or scenarios, and plugs directly into decks or Excel dashboards—no macros or finance jargon required.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors now use comparison apps and marketplaces that make yields fully transparent; with the fed funds rate at roughly 5.25–5.50% in 2023–24, deposit betas historically span about 20–60%, rising in tightening cycles and shifting mix toward higher-cost retail deposits. Southern must price competitively to avoid outflows, since relationship bundles can dampen but not eliminate sensitivity.

SMB borrowers with alternatives

As of 2024 small businesses regularly choose among credit unions, regional banks and online lenders for term loans and lines of credit. Competing term sheets put pressure on pricing, fees and covenant structures, forcing tighter spreads and fee waivers. Speed of decisioning is often the decisive procurement factor for SMBs. Southern’s deep local knowledge remains a differentiator but must be paired with faster turnaround to retain deals.

Low switching costs for basic products

Low switching costs: digital account openings accounted for over 50% of new checking/savings accounts in 2024, making basic account switches easy. Persistent friction from bill-pay setup and redirecting direct deposits creates inertia for many customers. Acquisition bonuses—often $200–$600 in 2024 campaigns—boost buyer power during onboarding. Banks must differentiate beyond commodity rates via services and UX.

Wealth clients demand advisory value

Service quality as leverage

Community bank clients expect high-touch support and quick resolutions, and J.D. Power 2024 shows community banks lead in customer satisfaction, making service the primary bargaining lever. Local social reviews and reputation amplify dissatisfaction, turning individual complaints into broader negotiating power. Buyers increasingly cite service expectations to extract fee concessions, while consistent in-branch and digital experiences blunt that leverage.

- High-touch expectations

- Social reviews amplify risk

- Service used to negotiate

- Omnichannel consistency reduces leverage

Customers pressure price and service with fed funds at 5.25–5.50% and digital >50%

Customers exert strong price and service pressure: with fed funds ~5.25–5.50% (2023–24) and deposit betas 20–60%, digital account openings >50% (2024) and acquisition bonuses $200–$600 raise switching risk; SMBs push on price and speed; robo AUM >1T (2024) heightens fee sensitivity; J.D. Power 2024 shows community banks lead in satisfaction, making service a decisive bargaining lever.

| Metric | 2024 Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Deposit beta | 20–60% |

| Digital openings | >50% |

| Robo AUM | >$1T |

| Acq bonus | $200–$600 |

Full Version Awaits

Southern Bank Porter's Five Forces Analysis

This preview shows the exact Southern Bank Porter’s Five Forces Analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. No samples or placeholders—instant access to the final deliverable.

A Must-Have Tool for Decision-Makers

Southern Bank’s Porter's Five Forces snapshot highlights competitive pressures across buyer power, supplier influence, substitutes and entry threats, plus rivalry intensity. It reveals where margins and growth are most at risk. This brief teases strategic implications and gaps. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Concentrated core banking vendors

Core processors FIS, Fiserv and Jack Henry remain the dominant US providers in 2024, collectively accounting for the majority of bank core relationships, giving them pricing and contract leverage; vendor switching is costly, risky and operationally disruptive, often taking months and millions in migration costs, and Southern Bank’s dependence on these platforms heightens supplier power while its smaller scale limits bargaining for favorable SLAs.

Funding suppliers and wholesale lines

Funding suppliers — depositors, FHLB advances and brokered CDs — supplied a material share of Southern Bank’s balance-sheet funding in 2024, with non-core sources estimated near 18–22% of liabilities, elevating supplier leverage. In tight liquidity cycles 2024 wholesale rates rose sharply and FHLB covenants tightened, boosting supplier power and cost of funds volatility. Strong local deposit franchises mitigated but did not eliminate this exposure.

Payment networks and card schemes

Visa and Mastercard control over 80% of U.S. card volume in 2024 and, together with ACH rules, set interchange and network fees that Southern Bank has little leverage to change. Interchange typically runs 1.5–2.5% for credit plus assessments of $0.02–$0.30 per txn, largely non‑negotiable for small banks. Scale advantages accrue to the largest issuers (top 10 hold ~60% of accounts), forcing Southern to accept standardized economics to remain interoperable.

Talent and specialized services

Credit underwriters, commercial lenders and compliance officers are scarce locally, raising supplier power as banks compete; BLS 2024 data shows average hourly earnings up about 4.1% YoY, fueling wage inflation and poaching by larger banks. Outsourced compliance, cybersecurity and audit firms command premium rates, and retention and signing bonuses (often 10–25% of base pay) partially mitigate turnover but raise cost per hire.

- Talent scarcity: higher bargaining power

- Wage inflation: BLS 2024 avg +4.1% YoY

- Outsourced services: premium fees

- Retention programs: costly (10–25% bonuses)

Data, cloud, and fintech partners

APIs, analytics, and cloud services are central to Southern Bank’s digital customer experience, but major cloud providers and leading fintechs—which held roughly two-thirds of global cloud market share in 2024—can impose standardized pricing and terms that squeeze margins. Deep integration dependencies create switching frictions and potential vendor lock-in. Co-innovation exists but typically skews value capture toward the platform owner.

- APIs: dependency and lock-in

- Cloud: ~two-thirds market share (2024)

- Fintechs: standardized commercial terms

- Co-innovation: platform owner advantage

Core processors, >80% card share, 18-22% non-core debt

Core processors (FIS, Fiserv, Jack Henry) dominate US cores in 2024, creating high switching costs and contract leverage for suppliers. Non‑core funding (FHLB, brokered CDs) comprised ~18–22% of liabilities in 2024, raising funding supplier power. Visa/Mastercard control >80% of US card volume and cloud providers held ~66% market share in 2024; BLS wage inflation +4.1% YoY.

| Supplier | 2024 metric |

|---|---|

| Core processors | Majority market share |

| Non-core funding | 18–22% liabilities |

| Card networks | >80% U.S. volume |

| Cloud providers | ~66% market share |

| Wage inflation | +4.1% YoY |

What is included in the product

Tailored Porter's Five Forces analysis for Southern Bank, uncovering key competitive drivers, customer and supplier influence on pricing, and market entry barriers that protect incumbents. Identifies disruptive threats, substitutes, and strategic levers Southern Bank can use to defend or grow its market position.

A concise one-sheet Porter's Five Forces for Southern Bank that visualizes strategic pressure with a spider chart, lets you customize force levels by new data or scenarios, and plugs directly into decks or Excel dashboards—no macros or finance jargon required.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors now use comparison apps and marketplaces that make yields fully transparent; with the fed funds rate at roughly 5.25–5.50% in 2023–24, deposit betas historically span about 20–60%, rising in tightening cycles and shifting mix toward higher-cost retail deposits. Southern must price competitively to avoid outflows, since relationship bundles can dampen but not eliminate sensitivity.

SMB borrowers with alternatives

As of 2024 small businesses regularly choose among credit unions, regional banks and online lenders for term loans and lines of credit. Competing term sheets put pressure on pricing, fees and covenant structures, forcing tighter spreads and fee waivers. Speed of decisioning is often the decisive procurement factor for SMBs. Southern’s deep local knowledge remains a differentiator but must be paired with faster turnaround to retain deals.

Low switching costs for basic products

Low switching costs: digital account openings accounted for over 50% of new checking/savings accounts in 2024, making basic account switches easy. Persistent friction from bill-pay setup and redirecting direct deposits creates inertia for many customers. Acquisition bonuses—often $200–$600 in 2024 campaigns—boost buyer power during onboarding. Banks must differentiate beyond commodity rates via services and UX.

Wealth clients demand advisory value

Service quality as leverage

Community bank clients expect high-touch support and quick resolutions, and J.D. Power 2024 shows community banks lead in customer satisfaction, making service the primary bargaining lever. Local social reviews and reputation amplify dissatisfaction, turning individual complaints into broader negotiating power. Buyers increasingly cite service expectations to extract fee concessions, while consistent in-branch and digital experiences blunt that leverage.

- High-touch expectations

- Social reviews amplify risk

- Service used to negotiate

- Omnichannel consistency reduces leverage

Customers pressure price and service with fed funds at 5.25–5.50% and digital >50%

Customers exert strong price and service pressure: with fed funds ~5.25–5.50% (2023–24) and deposit betas 20–60%, digital account openings >50% (2024) and acquisition bonuses $200–$600 raise switching risk; SMBs push on price and speed; robo AUM >1T (2024) heightens fee sensitivity; J.D. Power 2024 shows community banks lead in satisfaction, making service a decisive bargaining lever.

| Metric | 2024 Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Deposit beta | 20–60% |

| Digital openings | >50% |

| Robo AUM | >$1T |

| Acq bonus | $200–$600 |

Full Version Awaits

Southern Bank Porter's Five Forces Analysis

This preview shows the exact Southern Bank Porter’s Five Forces Analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. No samples or placeholders—instant access to the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Southern Bank’s Porter's Five Forces snapshot highlights competitive pressures across buyer power, supplier influence, substitutes and entry threats, plus rivalry intensity. It reveals where margins and growth are most at risk. This brief teases strategic implications and gaps. Unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Concentrated core banking vendors

Core processors FIS, Fiserv and Jack Henry remain the dominant US providers in 2024, collectively accounting for the majority of bank core relationships, giving them pricing and contract leverage; vendor switching is costly, risky and operationally disruptive, often taking months and millions in migration costs, and Southern Bank’s dependence on these platforms heightens supplier power while its smaller scale limits bargaining for favorable SLAs.

Funding suppliers and wholesale lines

Funding suppliers — depositors, FHLB advances and brokered CDs — supplied a material share of Southern Bank’s balance-sheet funding in 2024, with non-core sources estimated near 18–22% of liabilities, elevating supplier leverage. In tight liquidity cycles 2024 wholesale rates rose sharply and FHLB covenants tightened, boosting supplier power and cost of funds volatility. Strong local deposit franchises mitigated but did not eliminate this exposure.

Payment networks and card schemes

Visa and Mastercard control over 80% of U.S. card volume in 2024 and, together with ACH rules, set interchange and network fees that Southern Bank has little leverage to change. Interchange typically runs 1.5–2.5% for credit plus assessments of $0.02–$0.30 per txn, largely non‑negotiable for small banks. Scale advantages accrue to the largest issuers (top 10 hold ~60% of accounts), forcing Southern to accept standardized economics to remain interoperable.

Talent and specialized services

Credit underwriters, commercial lenders and compliance officers are scarce locally, raising supplier power as banks compete; BLS 2024 data shows average hourly earnings up about 4.1% YoY, fueling wage inflation and poaching by larger banks. Outsourced compliance, cybersecurity and audit firms command premium rates, and retention and signing bonuses (often 10–25% of base pay) partially mitigate turnover but raise cost per hire.

- Talent scarcity: higher bargaining power

- Wage inflation: BLS 2024 avg +4.1% YoY

- Outsourced services: premium fees

- Retention programs: costly (10–25% bonuses)

Data, cloud, and fintech partners

APIs, analytics, and cloud services are central to Southern Bank’s digital customer experience, but major cloud providers and leading fintechs—which held roughly two-thirds of global cloud market share in 2024—can impose standardized pricing and terms that squeeze margins. Deep integration dependencies create switching frictions and potential vendor lock-in. Co-innovation exists but typically skews value capture toward the platform owner.

- APIs: dependency and lock-in

- Cloud: ~two-thirds market share (2024)

- Fintechs: standardized commercial terms

- Co-innovation: platform owner advantage

Core processors, >80% card share, 18-22% non-core debt

Core processors (FIS, Fiserv, Jack Henry) dominate US cores in 2024, creating high switching costs and contract leverage for suppliers. Non‑core funding (FHLB, brokered CDs) comprised ~18–22% of liabilities in 2024, raising funding supplier power. Visa/Mastercard control >80% of US card volume and cloud providers held ~66% market share in 2024; BLS wage inflation +4.1% YoY.

| Supplier | 2024 metric |

|---|---|

| Core processors | Majority market share |

| Non-core funding | 18–22% liabilities |

| Card networks | >80% U.S. volume |

| Cloud providers | ~66% market share |

| Wage inflation | +4.1% YoY |

What is included in the product

Tailored Porter's Five Forces analysis for Southern Bank, uncovering key competitive drivers, customer and supplier influence on pricing, and market entry barriers that protect incumbents. Identifies disruptive threats, substitutes, and strategic levers Southern Bank can use to defend or grow its market position.

A concise one-sheet Porter's Five Forces for Southern Bank that visualizes strategic pressure with a spider chart, lets you customize force levels by new data or scenarios, and plugs directly into decks or Excel dashboards—no macros or finance jargon required.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors now use comparison apps and marketplaces that make yields fully transparent; with the fed funds rate at roughly 5.25–5.50% in 2023–24, deposit betas historically span about 20–60%, rising in tightening cycles and shifting mix toward higher-cost retail deposits. Southern must price competitively to avoid outflows, since relationship bundles can dampen but not eliminate sensitivity.

SMB borrowers with alternatives

As of 2024 small businesses regularly choose among credit unions, regional banks and online lenders for term loans and lines of credit. Competing term sheets put pressure on pricing, fees and covenant structures, forcing tighter spreads and fee waivers. Speed of decisioning is often the decisive procurement factor for SMBs. Southern’s deep local knowledge remains a differentiator but must be paired with faster turnaround to retain deals.

Low switching costs for basic products

Low switching costs: digital account openings accounted for over 50% of new checking/savings accounts in 2024, making basic account switches easy. Persistent friction from bill-pay setup and redirecting direct deposits creates inertia for many customers. Acquisition bonuses—often $200–$600 in 2024 campaigns—boost buyer power during onboarding. Banks must differentiate beyond commodity rates via services and UX.

Wealth clients demand advisory value

Service quality as leverage

Community bank clients expect high-touch support and quick resolutions, and J.D. Power 2024 shows community banks lead in customer satisfaction, making service the primary bargaining lever. Local social reviews and reputation amplify dissatisfaction, turning individual complaints into broader negotiating power. Buyers increasingly cite service expectations to extract fee concessions, while consistent in-branch and digital experiences blunt that leverage.

- High-touch expectations

- Social reviews amplify risk

- Service used to negotiate

- Omnichannel consistency reduces leverage

Customers pressure price and service with fed funds at 5.25–5.50% and digital >50%

Customers exert strong price and service pressure: with fed funds ~5.25–5.50% (2023–24) and deposit betas 20–60%, digital account openings >50% (2024) and acquisition bonuses $200–$600 raise switching risk; SMBs push on price and speed; robo AUM >1T (2024) heightens fee sensitivity; J.D. Power 2024 shows community banks lead in satisfaction, making service a decisive bargaining lever.

| Metric | 2024 Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Deposit beta | 20–60% |

| Digital openings | >50% |

| Robo AUM | >$1T |

| Acq bonus | $200–$600 |

Full Version Awaits

Southern Bank Porter's Five Forces Analysis

This preview shows the exact Southern Bank Porter’s Five Forces Analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. No samples or placeholders—instant access to the final deliverable.