Banorte Business Model Canvas

Unlock a Mexican bank's strategic playbook with a concise Business Model Canvas

Unlock Banorte’s strategic playbook with our concise Business Model Canvas—three to five core insights that reveal how the bank creates value, attracts customers, and sustains growth in Mexico’s financial market. Ideal for investors, consultants, and founders seeking actionable tactics. Purchase the full, editable Canvas for a complete section-by-section breakdown and ready-to-use templates.

Partnerships

Payment networks

Alliances with Visa, Mastercard and domestic card schemes enable Banorte to provide issuing and acquiring services, leveraging networks that together process over 90% of global card transactions. These partnerships expand merchant acceptance and transaction volumes domestically and cross-border. Co-branding plus EMV and PCI DSS security standards enhance consumer trust. Economics emphasize interchange optimization and joint marketing to grow card spend and fee income.

Fintech collaborators

Partnerships with fintechs accelerate digital onboarding, KYC and alternative scoring, shortening approval cycles through API-driven identity and data shares.

APIs enable embedded finance across partner ecosystems; McKinsey estimates embedded finance could represent up to 7 trillion dollars in revenues by 2030.

Joint pilots cut time-to-market for features and revenue-sharing models align incentives while distributing credit and operational risk.

Correspondent banks

Correspondent banks enable Banorte to tap global FX liquidity and trade finance markets—global FX turnover averaged about 7.5 trillion USD daily in 2022–23—supporting cross-border payments and hedging for corporate and wealth clients. Access to correspondent networks and SWIFT gpi (≈99% of tracked payments settled within 24h) improves settlement speed and lowers costs. Robust KYC/AML and sanctions compliance frameworks ensure safe international operations.

Insurance & Afore allies

Ties with insurers and Afore allies enable Banorte to expand bancassurance and retirement offerings, leveraging Afore system scale—Afores manage over 5.5 trillion MXN as of 2024—to access long-duration savings flows. Co-designing products with partners improves fit and pricing, while regulated data sharing strengthens underwriting accuracy and customer retention; distribution agreements lift fee income and cross-sell yields.

- Partners: insurers, Afores

- Scale: >5.5 trillion MXN Afore assets (2024)

- Benefits: better pricing, underwriting, retention

- Revenue: higher fee income via distribution deals

Tech & cloud vendors

Tech and cloud vendors power Banorte’s scalability by underpinning core banking, cybersecurity, and cloud infrastructure as the bank—Mexico’s largest domestically owned lender and second-largest by assets—accelerates digital services.

Joint roadmaps with vendors improve uptime and resilience while advanced analytics partners enable personalization and stronger risk controls.

Service-level agreements enforce performance, availability and regulatory compliance across mission-critical systems.

- core-banking

- cybersecurity

- cloud-scalability

- analytics-personalization

- SLAs-compliance

Cards, embedded finance & SWIFT gpi drive payments - 7T USD by 2030

Banorte partners with Visa/Mastercard and domestic schemes to drive card issuing/acquiring, optimizing interchange and joint marketing; fintechs and APIs speed KYC, onboarding and embedded finance growth (McKinsey: up to 7T USD by 2030). Correspondent banks and SWIFT gpi (≈99% within 24h) support FX/trade; Afores (≈5.5T MXN assets, 2024) and insurers enable bancassurance and long-duration funding. Tech vendors ensure cloud, security and SLA-backed resilience.

| Partner | Metric | 2024/Stat |

|---|---|---|

| Card schemes | Global share | >90% |

| Embedded finance | Revenue potential | ~7T USD by 2030 |

| Correspondent banks | FX daily turnover | ~7.5T USD |

| Afores | Assets | ≈5.5T MXN (2024) |

| SWIFT gpi | Same-day rate | ≈99% within 24h |

What is included in the product

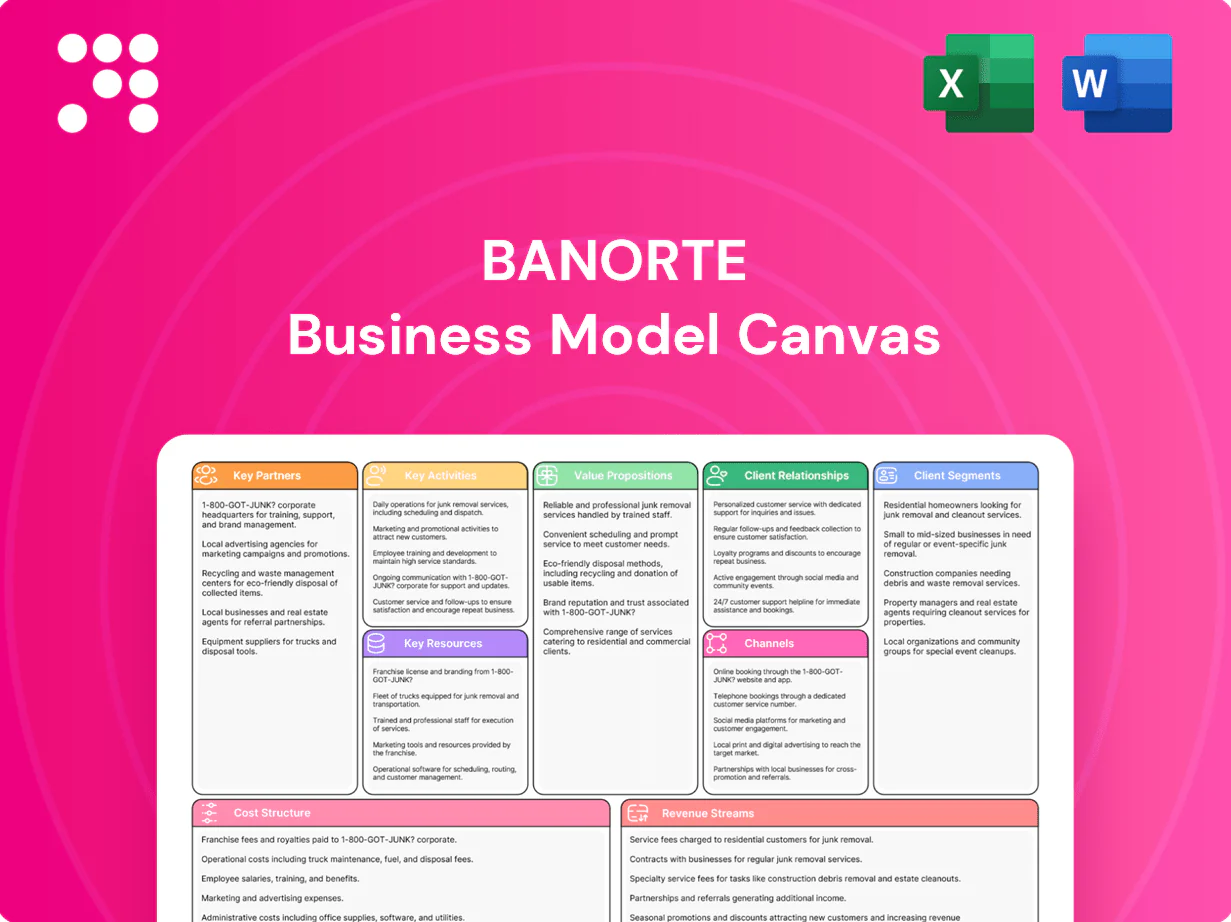

A comprehensive Business Model Canvas for Banorte detailing its customer segments, channels, value propositions and revenue streams across the 9 classic blocks, with insights on competitive advantages, linked SWOT analysis, and practical use for strategic planning, investor presentations, and decision-making.

Banorte Business Model Canvas delivers an editable one-page snapshot to quickly identify core banking components, streamline strategic planning and save hours of formatting—ideal for boardrooms, teams, teaching or comparing multiple models side-by-side.

Activities

Lending & credit

Banorte originates, underwrites and services retail, SME and corporate lending across a roughly MXN 1.1–1.3 trillion portfolio, using dynamic pricing and risk-based limits to target sustained NPLs near 1.8% (2024). Collections, early-warning and restructuring teams manage problem loans and recoveries. Continuous model monitoring, validation and governance align credit practices with CNBV and Basel III requirements.

Deposit & payments

Banorte acquires and manages low-cost deposits to fund growth, serving about 16 million customers which underpins retail funding. It operates cards, transfers and merchant acquiring at scale, processing millions of monthly transactions through Banorte Pay. Robust fraud prevention and real-time monitoring secure volumes, while active liquidity management optimizes net interest spread and funding costs.

Investment services

Banorte delivers brokerage, asset management and pension administration, with Afore XXI Banorte managing about MXN 1.3 trillion as of 2024 and a domestic banking market share near 16% in 2024. The bank manufactures and advises on products across conservative to aggressive risk profiles, provides execution, custody and consolidated reporting for institutional and retail clients, and maintains compliance and best-execution standards aligned with CNBV rules.

Digital product dev

Digital product dev focuses on designing and iterating mobile and web onboarding and servicing flows, using A/B testing and telemetry to reduce drop-off; as of 2024 Banorte doubled product release cadence to accelerate feature delivery. Data-driven personalization increases engagement and cross-sell via behavioral scoring. API management supports partnerships and open banking; UX, security, and reliability remain core.

- onboarding optimization

- personalization & cross-sell

- API & open banking

- UX, security, reliability

Risk & compliance

Risk & compliance at Banorte covers credit, market, liquidity and operational risk oversight with enterprise-wide limits, scenario and stress testing and capital planning aligned to CNBV and Basel III frameworks in 2024, maintaining capital and liquidity buffers above regulatory minima. AML/KYC, sanctions screening and data privacy controls operate across retail, corporate and digital channels with transaction monitoring and enhanced due diligence. Internal audit, business continuity and recovery testing run regularly to ensure resilience.

- Regulatory alignment: CNBV/Basel III

- Capital/liquidity: buffers above minima (2024)

- AML/KYC: enterprise transaction monitoring (2024)

- Continuity: periodic recovery & stress tests

MXN 1.1-1.3T loans, NPL ~1.8%, ~16M customers

Banorte originates, underwrites and services a MXN 1.1–1.3 trillion loan book targeting NPLs ~1.8% (2024), with collections and restructuring teams. It funds growth via low-cost deposits from ~16 million customers and operates cards, acquiring and Banorte Pay. Asset management & Afore XXI Banorte manage MXN 1.3 trillion (~16% market share, 2024). Digital product cadence doubled in 2024; API/open banking and risk/compliance per CNBV/Basel III.

| Metric | 2024 |

|---|---|

| Loan portfolio | MXN 1.1–1.3T |

| NPLs | ~1.8% |

| Customers | ~16M |

| Afore assets | MXN 1.3T |

| Market share | ~16% |

Full Version Awaits

Business Model Canvas

The Banorte Business Model Canvas preview shown here is the exact deliverable you’ll receive—no mockups or placeholders. When you purchase, you’ll get this same fully formatted document ready for editing and presentation. The content, structure, and pages match precisely what’s displayed in the preview.

Unlock a Mexican bank's strategic playbook with a concise Business Model Canvas

Unlock Banorte’s strategic playbook with our concise Business Model Canvas—three to five core insights that reveal how the bank creates value, attracts customers, and sustains growth in Mexico’s financial market. Ideal for investors, consultants, and founders seeking actionable tactics. Purchase the full, editable Canvas for a complete section-by-section breakdown and ready-to-use templates.

Partnerships

Payment networks

Alliances with Visa, Mastercard and domestic card schemes enable Banorte to provide issuing and acquiring services, leveraging networks that together process over 90% of global card transactions. These partnerships expand merchant acceptance and transaction volumes domestically and cross-border. Co-branding plus EMV and PCI DSS security standards enhance consumer trust. Economics emphasize interchange optimization and joint marketing to grow card spend and fee income.

Fintech collaborators

Partnerships with fintechs accelerate digital onboarding, KYC and alternative scoring, shortening approval cycles through API-driven identity and data shares.

APIs enable embedded finance across partner ecosystems; McKinsey estimates embedded finance could represent up to 7 trillion dollars in revenues by 2030.

Joint pilots cut time-to-market for features and revenue-sharing models align incentives while distributing credit and operational risk.

Correspondent banks

Correspondent banks enable Banorte to tap global FX liquidity and trade finance markets—global FX turnover averaged about 7.5 trillion USD daily in 2022–23—supporting cross-border payments and hedging for corporate and wealth clients. Access to correspondent networks and SWIFT gpi (≈99% of tracked payments settled within 24h) improves settlement speed and lowers costs. Robust KYC/AML and sanctions compliance frameworks ensure safe international operations.

Insurance & Afore allies

Ties with insurers and Afore allies enable Banorte to expand bancassurance and retirement offerings, leveraging Afore system scale—Afores manage over 5.5 trillion MXN as of 2024—to access long-duration savings flows. Co-designing products with partners improves fit and pricing, while regulated data sharing strengthens underwriting accuracy and customer retention; distribution agreements lift fee income and cross-sell yields.

- Partners: insurers, Afores

- Scale: >5.5 trillion MXN Afore assets (2024)

- Benefits: better pricing, underwriting, retention

- Revenue: higher fee income via distribution deals

Tech & cloud vendors

Tech and cloud vendors power Banorte’s scalability by underpinning core banking, cybersecurity, and cloud infrastructure as the bank—Mexico’s largest domestically owned lender and second-largest by assets—accelerates digital services.

Joint roadmaps with vendors improve uptime and resilience while advanced analytics partners enable personalization and stronger risk controls.

Service-level agreements enforce performance, availability and regulatory compliance across mission-critical systems.

- core-banking

- cybersecurity

- cloud-scalability

- analytics-personalization

- SLAs-compliance

Cards, embedded finance & SWIFT gpi drive payments - 7T USD by 2030

Banorte partners with Visa/Mastercard and domestic schemes to drive card issuing/acquiring, optimizing interchange and joint marketing; fintechs and APIs speed KYC, onboarding and embedded finance growth (McKinsey: up to 7T USD by 2030). Correspondent banks and SWIFT gpi (≈99% within 24h) support FX/trade; Afores (≈5.5T MXN assets, 2024) and insurers enable bancassurance and long-duration funding. Tech vendors ensure cloud, security and SLA-backed resilience.

| Partner | Metric | 2024/Stat |

|---|---|---|

| Card schemes | Global share | >90% |

| Embedded finance | Revenue potential | ~7T USD by 2030 |

| Correspondent banks | FX daily turnover | ~7.5T USD |

| Afores | Assets | ≈5.5T MXN (2024) |

| SWIFT gpi | Same-day rate | ≈99% within 24h |

What is included in the product

A comprehensive Business Model Canvas for Banorte detailing its customer segments, channels, value propositions and revenue streams across the 9 classic blocks, with insights on competitive advantages, linked SWOT analysis, and practical use for strategic planning, investor presentations, and decision-making.

Banorte Business Model Canvas delivers an editable one-page snapshot to quickly identify core banking components, streamline strategic planning and save hours of formatting—ideal for boardrooms, teams, teaching or comparing multiple models side-by-side.

Activities

Lending & credit

Banorte originates, underwrites and services retail, SME and corporate lending across a roughly MXN 1.1–1.3 trillion portfolio, using dynamic pricing and risk-based limits to target sustained NPLs near 1.8% (2024). Collections, early-warning and restructuring teams manage problem loans and recoveries. Continuous model monitoring, validation and governance align credit practices with CNBV and Basel III requirements.

Deposit & payments

Banorte acquires and manages low-cost deposits to fund growth, serving about 16 million customers which underpins retail funding. It operates cards, transfers and merchant acquiring at scale, processing millions of monthly transactions through Banorte Pay. Robust fraud prevention and real-time monitoring secure volumes, while active liquidity management optimizes net interest spread and funding costs.

Investment services

Banorte delivers brokerage, asset management and pension administration, with Afore XXI Banorte managing about MXN 1.3 trillion as of 2024 and a domestic banking market share near 16% in 2024. The bank manufactures and advises on products across conservative to aggressive risk profiles, provides execution, custody and consolidated reporting for institutional and retail clients, and maintains compliance and best-execution standards aligned with CNBV rules.

Digital product dev

Digital product dev focuses on designing and iterating mobile and web onboarding and servicing flows, using A/B testing and telemetry to reduce drop-off; as of 2024 Banorte doubled product release cadence to accelerate feature delivery. Data-driven personalization increases engagement and cross-sell via behavioral scoring. API management supports partnerships and open banking; UX, security, and reliability remain core.

- onboarding optimization

- personalization & cross-sell

- API & open banking

- UX, security, reliability

Risk & compliance

Risk & compliance at Banorte covers credit, market, liquidity and operational risk oversight with enterprise-wide limits, scenario and stress testing and capital planning aligned to CNBV and Basel III frameworks in 2024, maintaining capital and liquidity buffers above regulatory minima. AML/KYC, sanctions screening and data privacy controls operate across retail, corporate and digital channels with transaction monitoring and enhanced due diligence. Internal audit, business continuity and recovery testing run regularly to ensure resilience.

- Regulatory alignment: CNBV/Basel III

- Capital/liquidity: buffers above minima (2024)

- AML/KYC: enterprise transaction monitoring (2024)

- Continuity: periodic recovery & stress tests

MXN 1.1-1.3T loans, NPL ~1.8%, ~16M customers

Banorte originates, underwrites and services a MXN 1.1–1.3 trillion loan book targeting NPLs ~1.8% (2024), with collections and restructuring teams. It funds growth via low-cost deposits from ~16 million customers and operates cards, acquiring and Banorte Pay. Asset management & Afore XXI Banorte manage MXN 1.3 trillion (~16% market share, 2024). Digital product cadence doubled in 2024; API/open banking and risk/compliance per CNBV/Basel III.

| Metric | 2024 |

|---|---|

| Loan portfolio | MXN 1.1–1.3T |

| NPLs | ~1.8% |

| Customers | ~16M |

| Afore assets | MXN 1.3T |

| Market share | ~16% |

Full Version Awaits

Business Model Canvas

The Banorte Business Model Canvas preview shown here is the exact deliverable you’ll receive—no mockups or placeholders. When you purchase, you’ll get this same fully formatted document ready for editing and presentation. The content, structure, and pages match precisely what’s displayed in the preview.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a Mexican bank's strategic playbook with a concise Business Model Canvas

Unlock Banorte’s strategic playbook with our concise Business Model Canvas—three to five core insights that reveal how the bank creates value, attracts customers, and sustains growth in Mexico’s financial market. Ideal for investors, consultants, and founders seeking actionable tactics. Purchase the full, editable Canvas for a complete section-by-section breakdown and ready-to-use templates.

Partnerships

Payment networks

Alliances with Visa, Mastercard and domestic card schemes enable Banorte to provide issuing and acquiring services, leveraging networks that together process over 90% of global card transactions. These partnerships expand merchant acceptance and transaction volumes domestically and cross-border. Co-branding plus EMV and PCI DSS security standards enhance consumer trust. Economics emphasize interchange optimization and joint marketing to grow card spend and fee income.

Fintech collaborators

Partnerships with fintechs accelerate digital onboarding, KYC and alternative scoring, shortening approval cycles through API-driven identity and data shares.

APIs enable embedded finance across partner ecosystems; McKinsey estimates embedded finance could represent up to 7 trillion dollars in revenues by 2030.

Joint pilots cut time-to-market for features and revenue-sharing models align incentives while distributing credit and operational risk.

Correspondent banks

Correspondent banks enable Banorte to tap global FX liquidity and trade finance markets—global FX turnover averaged about 7.5 trillion USD daily in 2022–23—supporting cross-border payments and hedging for corporate and wealth clients. Access to correspondent networks and SWIFT gpi (≈99% of tracked payments settled within 24h) improves settlement speed and lowers costs. Robust KYC/AML and sanctions compliance frameworks ensure safe international operations.

Insurance & Afore allies

Ties with insurers and Afore allies enable Banorte to expand bancassurance and retirement offerings, leveraging Afore system scale—Afores manage over 5.5 trillion MXN as of 2024—to access long-duration savings flows. Co-designing products with partners improves fit and pricing, while regulated data sharing strengthens underwriting accuracy and customer retention; distribution agreements lift fee income and cross-sell yields.

- Partners: insurers, Afores

- Scale: >5.5 trillion MXN Afore assets (2024)

- Benefits: better pricing, underwriting, retention

- Revenue: higher fee income via distribution deals

Tech & cloud vendors

Tech and cloud vendors power Banorte’s scalability by underpinning core banking, cybersecurity, and cloud infrastructure as the bank—Mexico’s largest domestically owned lender and second-largest by assets—accelerates digital services.

Joint roadmaps with vendors improve uptime and resilience while advanced analytics partners enable personalization and stronger risk controls.

Service-level agreements enforce performance, availability and regulatory compliance across mission-critical systems.

- core-banking

- cybersecurity

- cloud-scalability

- analytics-personalization

- SLAs-compliance

Cards, embedded finance & SWIFT gpi drive payments - 7T USD by 2030

Banorte partners with Visa/Mastercard and domestic schemes to drive card issuing/acquiring, optimizing interchange and joint marketing; fintechs and APIs speed KYC, onboarding and embedded finance growth (McKinsey: up to 7T USD by 2030). Correspondent banks and SWIFT gpi (≈99% within 24h) support FX/trade; Afores (≈5.5T MXN assets, 2024) and insurers enable bancassurance and long-duration funding. Tech vendors ensure cloud, security and SLA-backed resilience.

| Partner | Metric | 2024/Stat |

|---|---|---|

| Card schemes | Global share | >90% |

| Embedded finance | Revenue potential | ~7T USD by 2030 |

| Correspondent banks | FX daily turnover | ~7.5T USD |

| Afores | Assets | ≈5.5T MXN (2024) |

| SWIFT gpi | Same-day rate | ≈99% within 24h |

What is included in the product

A comprehensive Business Model Canvas for Banorte detailing its customer segments, channels, value propositions and revenue streams across the 9 classic blocks, with insights on competitive advantages, linked SWOT analysis, and practical use for strategic planning, investor presentations, and decision-making.

Banorte Business Model Canvas delivers an editable one-page snapshot to quickly identify core banking components, streamline strategic planning and save hours of formatting—ideal for boardrooms, teams, teaching or comparing multiple models side-by-side.

Activities

Lending & credit

Banorte originates, underwrites and services retail, SME and corporate lending across a roughly MXN 1.1–1.3 trillion portfolio, using dynamic pricing and risk-based limits to target sustained NPLs near 1.8% (2024). Collections, early-warning and restructuring teams manage problem loans and recoveries. Continuous model monitoring, validation and governance align credit practices with CNBV and Basel III requirements.

Deposit & payments

Banorte acquires and manages low-cost deposits to fund growth, serving about 16 million customers which underpins retail funding. It operates cards, transfers and merchant acquiring at scale, processing millions of monthly transactions through Banorte Pay. Robust fraud prevention and real-time monitoring secure volumes, while active liquidity management optimizes net interest spread and funding costs.

Investment services

Banorte delivers brokerage, asset management and pension administration, with Afore XXI Banorte managing about MXN 1.3 trillion as of 2024 and a domestic banking market share near 16% in 2024. The bank manufactures and advises on products across conservative to aggressive risk profiles, provides execution, custody and consolidated reporting for institutional and retail clients, and maintains compliance and best-execution standards aligned with CNBV rules.

Digital product dev

Digital product dev focuses on designing and iterating mobile and web onboarding and servicing flows, using A/B testing and telemetry to reduce drop-off; as of 2024 Banorte doubled product release cadence to accelerate feature delivery. Data-driven personalization increases engagement and cross-sell via behavioral scoring. API management supports partnerships and open banking; UX, security, and reliability remain core.

- onboarding optimization

- personalization & cross-sell

- API & open banking

- UX, security, reliability

Risk & compliance

Risk & compliance at Banorte covers credit, market, liquidity and operational risk oversight with enterprise-wide limits, scenario and stress testing and capital planning aligned to CNBV and Basel III frameworks in 2024, maintaining capital and liquidity buffers above regulatory minima. AML/KYC, sanctions screening and data privacy controls operate across retail, corporate and digital channels with transaction monitoring and enhanced due diligence. Internal audit, business continuity and recovery testing run regularly to ensure resilience.

- Regulatory alignment: CNBV/Basel III

- Capital/liquidity: buffers above minima (2024)

- AML/KYC: enterprise transaction monitoring (2024)

- Continuity: periodic recovery & stress tests

MXN 1.1-1.3T loans, NPL ~1.8%, ~16M customers

Banorte originates, underwrites and services a MXN 1.1–1.3 trillion loan book targeting NPLs ~1.8% (2024), with collections and restructuring teams. It funds growth via low-cost deposits from ~16 million customers and operates cards, acquiring and Banorte Pay. Asset management & Afore XXI Banorte manage MXN 1.3 trillion (~16% market share, 2024). Digital product cadence doubled in 2024; API/open banking and risk/compliance per CNBV/Basel III.

| Metric | 2024 |

|---|---|

| Loan portfolio | MXN 1.1–1.3T |

| NPLs | ~1.8% |

| Customers | ~16M |

| Afore assets | MXN 1.3T |

| Market share | ~16% |

Full Version Awaits

Business Model Canvas

The Banorte Business Model Canvas preview shown here is the exact deliverable you’ll receive—no mockups or placeholders. When you purchase, you’ll get this same fully formatted document ready for editing and presentation. The content, structure, and pages match precisely what’s displayed in the preview.