Banorte Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

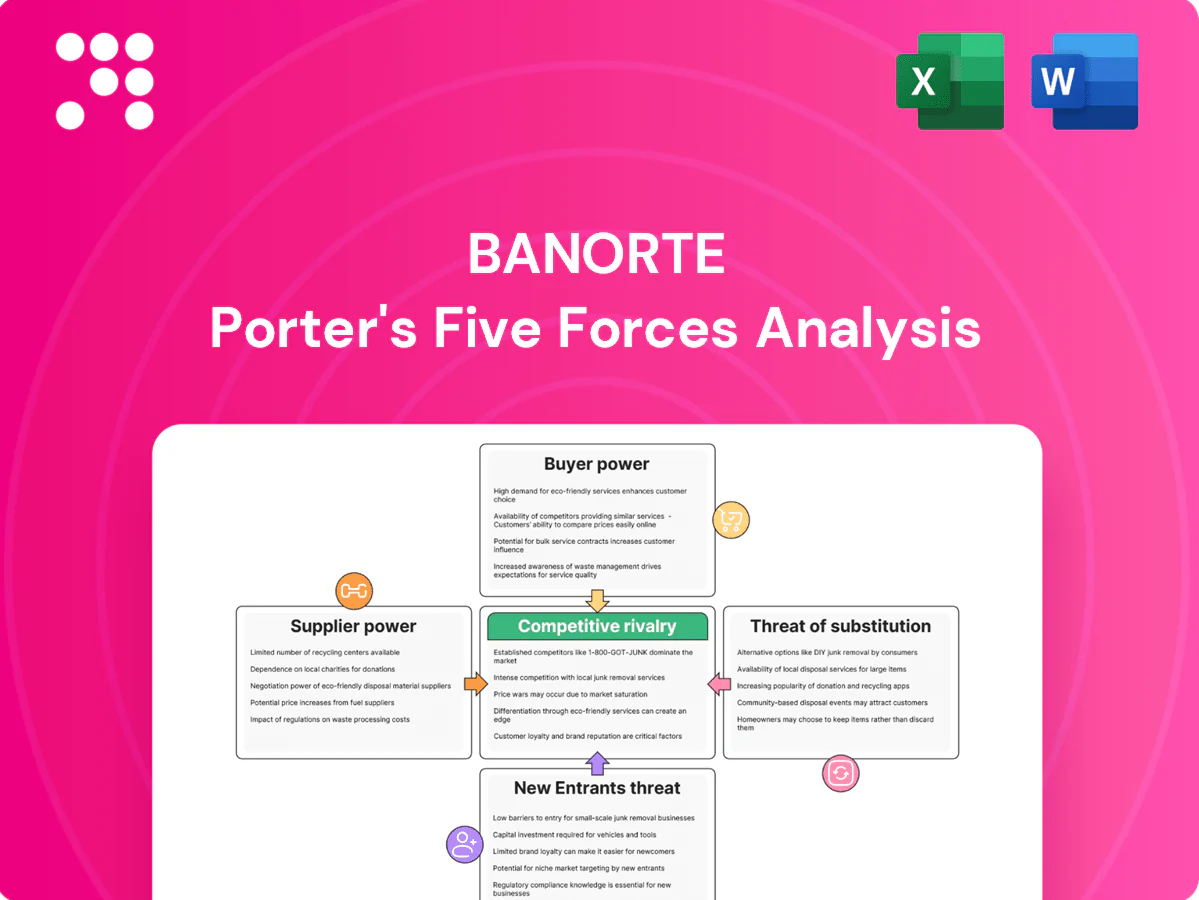

Banorte faces moderate buyer power, significant rival intensity from national banks, manageable supplier influence, limited substitute threats, and barriers that deter many new entrants; these dynamics shape pricing and growth potential. This snapshot hints at strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Banorte.

Suppliers Bargaining Power

Concentrated tech vendors

Banorte relies on a limited set of core-banking, cloud and payments vendors, concentrating negotiation leverage with incumbents and exposing the bank to supplier power. Vendor switching is costly, risky and time-consuming due to complex integrations and regulatory re‑certifications, often embedded in multi-year (typically 3–5 year) contracts that entrench suppliers. Multi-vendor strategies and selective in‑house development mitigate but do not eliminate this supplier bargaining power.

Payment networks and processors

Visa and Mastercard together account for over 80% of global card transaction volume, setting fees and technical standards that shape card economics; network rules and interchange frameworks cap Banorte’s unilateral pricing flexibility. Banorte, with roughly 16% of Mexican banking assets in 2024, gains negotiating leverage from scale but cannot fully offset network power. Merchant fees in Mexico average about 2%–2.5%, and alternative rails like CoDi remain low single-digit share of electronic payments in 2024.

Wholesale and institutional funding

Access to interbank markets, bond investors and institutional depositors drives Banorte’s funding costs; in tight liquidity cycles these suppliers can demand wider spreads and pressure net interest margins. Banorte’s retail deposit franchise—about 17% domestic market share and ~MXN 1.9 trillion in deposits in 2024—reduces wholesale reliance. Diversified maturities and covered issuances (around USD 1.0 billion program) help balance supplier influence.

Data and credit infrastructure

Specialized talent and outsourcing

Cybersecurity, AI/ML and risk specialists remain scarce—ISC2 estimates a 3.5 million global cyber workforce gap in 2024—giving talent and niche outsourcers pricing leverage; US AI engineer median base pay ~180,000 in 2024 (Glassdoor), raising acquisition costs amid Big Tech competition; Banorte can dilute supplier power via internal academies and knowledge transfer and stabilize capacity/pricing through strategic nearshoring partnerships.

- Scarcity: ISC2 3.5M gap (2024)

- Cost pressure: AI median pay ~180k (Glassdoor 2024)

- Mitigation: internal academies, nearshoring

Regional bank faces concentrated vendor power, card networks >80% and tech talent squeeze

Banorte faces concentrated supplier power from core-banking, cloud and payments vendors, with vendor switching costly and contracts typically 3–5 years. Visa/Mastercard >80% global volume, limiting card pricing; Banorte ~16% banking assets and MXN1.9tn deposits (2024) provide scale but not full leverage. Credit bureaus (2), ISC2 cyber gap 3.5M and US AI median pay ~180,000 (2024) tighten specialist supply.

| Metric | 2024 Value |

|---|---|

| Visa/Mastercard share | >80% |

| Banorte assets share | ~16% |

| Deposits | MXN 1.9tn |

| Credit bureaus | 2 |

| Cyber workforce gap | 3.5M |

| AI engineer median pay (US) | ~180,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Banorte that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with strategic insights to inform pricing and market defense.

A concise one-sheet Porter's Five Forces for Banorte that highlights competitive pressures, regulatory risks and supplier/customer dynamics for quick decisions; editable radar chart and scenario tabs let teams update pressure levels and integrate into decks or Excel without complex tools.

Customers Bargaining Power

Multi-banked corporates

Multi-banked large enterprises and government entities drive price competition in credit and cash management; Banorte, with ≈18% share of Mexican banking assets in 2024, faces pressure to lower rates and fees on high-volume accounts. Volumes give clients leverage to demand spreads, RFP-driven procurement increases transparency and switching, often compressing margins by tens of basis points. Deep relationships and tailored solutions remain key defenses.

Price-sensitive retail customers

Price-sensitive retail customers increasingly compare fees, rates and UX across apps—Mexico's smartphone penetration (~79% in 2024) accelerates this transparency and raises customer bargaining power. Fintech wallets and retailers now offer cheaper payment rails and installment options, eroding fees on transactional products where switching is easiest. Customers switch less for credit and pensions, but loyalty programs and bundled services materially curb churn.

Digital service expectations

Customers now demand instant onboarding, 24/7 reliability and rich feature sets, and Banorte, as one of Mexico’s largest banks by assets, faces rapid churn when outages or friction occur. App store ratings and social media amplify buyer influence, turning single incidents into broad reputational risk. Continuous release cycles and CX analytics are essential defenses to retain digitally-savvy clients.

SMEs’ credit access

SMEs in Mexico represent 99.8% of firms and contribute roughly 52% of GDP (INEGI, 2024), giving them substantial bargaining power over credit terms as they prioritize speed and flexibility and use aggregation platforms to compare offers. Alternative lenders and fintechs, often delivering underwriting and funding within hours to a day, have reset SME expectations on turnaround times. SMEs routinely negotiate collateral, covenants and pricing, while embedded finance partnerships (e.g., POS and ERP integrations) help rival banks retain SME flows.

- SME market share: 99.8% of firms (INEGI, 2024)

- Key demand: speed, flexibility, multi-offer platforms

- Negotiation levers: collateral, covenants, pricing

- Retention tool: embedded finance via POS/ERP partnerships

Regulatory transparency empowering buyers

Regulatory transparency in 2024—with Banorte holding about MXN 4.2 trillion in assets and roughly 17% market share—boosts product comparability through mandatory disclosure and consumer protection rules, reducing information asymmetry and strengthening buyer decisions. Robust complaint mechanisms create pricing and practice pressure, while clear value propositions and financial education blunt purely price-driven switching.

- Disclosure: standardized facts increase comparability

- Asymmetry: clearer data strengthens buyer choice

- Complaints: regulatory channels pressure pricing

- Offset: education and value propositions reduce churn

Corporate RFPs compress spreads; mobile retail and SMEs strengthen bargaining power

Large corporates and government clients wield pricing leverage—Banorte holds ~18% market share (~MXN 4.2T assets in 2024) so high-volume RFPs compress spreads. Retail customers (smartphone penetration ~79% in 2024) and fintechs raise fee transparency and switching. SMEs (99.8% of firms; ~52% GDP) demand speed and flexibility, strengthening bargaining power.

| Metric | 2024 |

|---|---|

| Banorte market share | ~18% (MXN 4.2T) |

| Smartphone penetration | ~79% |

| SMEs share of firms | 99.8% |

| SMEs contribution to GDP | ~52% |

Same Document Delivered

Banorte Porter's Five Forces Analysis

This preview shows the exact Banorte Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted and ready for download and use the moment you buy. No mockups; this is the final deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Banorte faces moderate buyer power, significant rival intensity from national banks, manageable supplier influence, limited substitute threats, and barriers that deter many new entrants; these dynamics shape pricing and growth potential. This snapshot hints at strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Banorte.

Suppliers Bargaining Power

Concentrated tech vendors

Banorte relies on a limited set of core-banking, cloud and payments vendors, concentrating negotiation leverage with incumbents and exposing the bank to supplier power. Vendor switching is costly, risky and time-consuming due to complex integrations and regulatory re‑certifications, often embedded in multi-year (typically 3–5 year) contracts that entrench suppliers. Multi-vendor strategies and selective in‑house development mitigate but do not eliminate this supplier bargaining power.

Payment networks and processors

Visa and Mastercard together account for over 80% of global card transaction volume, setting fees and technical standards that shape card economics; network rules and interchange frameworks cap Banorte’s unilateral pricing flexibility. Banorte, with roughly 16% of Mexican banking assets in 2024, gains negotiating leverage from scale but cannot fully offset network power. Merchant fees in Mexico average about 2%–2.5%, and alternative rails like CoDi remain low single-digit share of electronic payments in 2024.

Wholesale and institutional funding

Access to interbank markets, bond investors and institutional depositors drives Banorte’s funding costs; in tight liquidity cycles these suppliers can demand wider spreads and pressure net interest margins. Banorte’s retail deposit franchise—about 17% domestic market share and ~MXN 1.9 trillion in deposits in 2024—reduces wholesale reliance. Diversified maturities and covered issuances (around USD 1.0 billion program) help balance supplier influence.

Data and credit infrastructure

Specialized talent and outsourcing

Cybersecurity, AI/ML and risk specialists remain scarce—ISC2 estimates a 3.5 million global cyber workforce gap in 2024—giving talent and niche outsourcers pricing leverage; US AI engineer median base pay ~180,000 in 2024 (Glassdoor), raising acquisition costs amid Big Tech competition; Banorte can dilute supplier power via internal academies and knowledge transfer and stabilize capacity/pricing through strategic nearshoring partnerships.

- Scarcity: ISC2 3.5M gap (2024)

- Cost pressure: AI median pay ~180k (Glassdoor 2024)

- Mitigation: internal academies, nearshoring

Regional bank faces concentrated vendor power, card networks >80% and tech talent squeeze

Banorte faces concentrated supplier power from core-banking, cloud and payments vendors, with vendor switching costly and contracts typically 3–5 years. Visa/Mastercard >80% global volume, limiting card pricing; Banorte ~16% banking assets and MXN1.9tn deposits (2024) provide scale but not full leverage. Credit bureaus (2), ISC2 cyber gap 3.5M and US AI median pay ~180,000 (2024) tighten specialist supply.

| Metric | 2024 Value |

|---|---|

| Visa/Mastercard share | >80% |

| Banorte assets share | ~16% |

| Deposits | MXN 1.9tn |

| Credit bureaus | 2 |

| Cyber workforce gap | 3.5M |

| AI engineer median pay (US) | ~180,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Banorte that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with strategic insights to inform pricing and market defense.

A concise one-sheet Porter's Five Forces for Banorte that highlights competitive pressures, regulatory risks and supplier/customer dynamics for quick decisions; editable radar chart and scenario tabs let teams update pressure levels and integrate into decks or Excel without complex tools.

Customers Bargaining Power

Multi-banked corporates

Multi-banked large enterprises and government entities drive price competition in credit and cash management; Banorte, with ≈18% share of Mexican banking assets in 2024, faces pressure to lower rates and fees on high-volume accounts. Volumes give clients leverage to demand spreads, RFP-driven procurement increases transparency and switching, often compressing margins by tens of basis points. Deep relationships and tailored solutions remain key defenses.

Price-sensitive retail customers

Price-sensitive retail customers increasingly compare fees, rates and UX across apps—Mexico's smartphone penetration (~79% in 2024) accelerates this transparency and raises customer bargaining power. Fintech wallets and retailers now offer cheaper payment rails and installment options, eroding fees on transactional products where switching is easiest. Customers switch less for credit and pensions, but loyalty programs and bundled services materially curb churn.

Digital service expectations

Customers now demand instant onboarding, 24/7 reliability and rich feature sets, and Banorte, as one of Mexico’s largest banks by assets, faces rapid churn when outages or friction occur. App store ratings and social media amplify buyer influence, turning single incidents into broad reputational risk. Continuous release cycles and CX analytics are essential defenses to retain digitally-savvy clients.

SMEs’ credit access

SMEs in Mexico represent 99.8% of firms and contribute roughly 52% of GDP (INEGI, 2024), giving them substantial bargaining power over credit terms as they prioritize speed and flexibility and use aggregation platforms to compare offers. Alternative lenders and fintechs, often delivering underwriting and funding within hours to a day, have reset SME expectations on turnaround times. SMEs routinely negotiate collateral, covenants and pricing, while embedded finance partnerships (e.g., POS and ERP integrations) help rival banks retain SME flows.

- SME market share: 99.8% of firms (INEGI, 2024)

- Key demand: speed, flexibility, multi-offer platforms

- Negotiation levers: collateral, covenants, pricing

- Retention tool: embedded finance via POS/ERP partnerships

Regulatory transparency empowering buyers

Regulatory transparency in 2024—with Banorte holding about MXN 4.2 trillion in assets and roughly 17% market share—boosts product comparability through mandatory disclosure and consumer protection rules, reducing information asymmetry and strengthening buyer decisions. Robust complaint mechanisms create pricing and practice pressure, while clear value propositions and financial education blunt purely price-driven switching.

- Disclosure: standardized facts increase comparability

- Asymmetry: clearer data strengthens buyer choice

- Complaints: regulatory channels pressure pricing

- Offset: education and value propositions reduce churn

Corporate RFPs compress spreads; mobile retail and SMEs strengthen bargaining power

Large corporates and government clients wield pricing leverage—Banorte holds ~18% market share (~MXN 4.2T assets in 2024) so high-volume RFPs compress spreads. Retail customers (smartphone penetration ~79% in 2024) and fintechs raise fee transparency and switching. SMEs (99.8% of firms; ~52% GDP) demand speed and flexibility, strengthening bargaining power.

| Metric | 2024 |

|---|---|

| Banorte market share | ~18% (MXN 4.2T) |

| Smartphone penetration | ~79% |

| SMEs share of firms | 99.8% |

| SMEs contribution to GDP | ~52% |

Same Document Delivered

Banorte Porter's Five Forces Analysis

This preview shows the exact Banorte Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted and ready for download and use the moment you buy. No mockups; this is the final deliverable.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Banorte faces moderate buyer power, significant rival intensity from national banks, manageable supplier influence, limited substitute threats, and barriers that deter many new entrants; these dynamics shape pricing and growth potential. This snapshot hints at strategic risks and opportunities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Banorte.

Suppliers Bargaining Power

Concentrated tech vendors

Banorte relies on a limited set of core-banking, cloud and payments vendors, concentrating negotiation leverage with incumbents and exposing the bank to supplier power. Vendor switching is costly, risky and time-consuming due to complex integrations and regulatory re‑certifications, often embedded in multi-year (typically 3–5 year) contracts that entrench suppliers. Multi-vendor strategies and selective in‑house development mitigate but do not eliminate this supplier bargaining power.

Payment networks and processors

Visa and Mastercard together account for over 80% of global card transaction volume, setting fees and technical standards that shape card economics; network rules and interchange frameworks cap Banorte’s unilateral pricing flexibility. Banorte, with roughly 16% of Mexican banking assets in 2024, gains negotiating leverage from scale but cannot fully offset network power. Merchant fees in Mexico average about 2%–2.5%, and alternative rails like CoDi remain low single-digit share of electronic payments in 2024.

Wholesale and institutional funding

Access to interbank markets, bond investors and institutional depositors drives Banorte’s funding costs; in tight liquidity cycles these suppliers can demand wider spreads and pressure net interest margins. Banorte’s retail deposit franchise—about 17% domestic market share and ~MXN 1.9 trillion in deposits in 2024—reduces wholesale reliance. Diversified maturities and covered issuances (around USD 1.0 billion program) help balance supplier influence.

Data and credit infrastructure

Specialized talent and outsourcing

Cybersecurity, AI/ML and risk specialists remain scarce—ISC2 estimates a 3.5 million global cyber workforce gap in 2024—giving talent and niche outsourcers pricing leverage; US AI engineer median base pay ~180,000 in 2024 (Glassdoor), raising acquisition costs amid Big Tech competition; Banorte can dilute supplier power via internal academies and knowledge transfer and stabilize capacity/pricing through strategic nearshoring partnerships.

- Scarcity: ISC2 3.5M gap (2024)

- Cost pressure: AI median pay ~180k (Glassdoor 2024)

- Mitigation: internal academies, nearshoring

Regional bank faces concentrated vendor power, card networks >80% and tech talent squeeze

Banorte faces concentrated supplier power from core-banking, cloud and payments vendors, with vendor switching costly and contracts typically 3–5 years. Visa/Mastercard >80% global volume, limiting card pricing; Banorte ~16% banking assets and MXN1.9tn deposits (2024) provide scale but not full leverage. Credit bureaus (2), ISC2 cyber gap 3.5M and US AI median pay ~180,000 (2024) tighten specialist supply.

| Metric | 2024 Value |

|---|---|

| Visa/Mastercard share | >80% |

| Banorte assets share | ~16% |

| Deposits | MXN 1.9tn |

| Credit bureaus | 2 |

| Cyber workforce gap | 3.5M |

| AI engineer median pay (US) | ~180,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Banorte that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, with strategic insights to inform pricing and market defense.

A concise one-sheet Porter's Five Forces for Banorte that highlights competitive pressures, regulatory risks and supplier/customer dynamics for quick decisions; editable radar chart and scenario tabs let teams update pressure levels and integrate into decks or Excel without complex tools.

Customers Bargaining Power

Multi-banked corporates

Multi-banked large enterprises and government entities drive price competition in credit and cash management; Banorte, with ≈18% share of Mexican banking assets in 2024, faces pressure to lower rates and fees on high-volume accounts. Volumes give clients leverage to demand spreads, RFP-driven procurement increases transparency and switching, often compressing margins by tens of basis points. Deep relationships and tailored solutions remain key defenses.

Price-sensitive retail customers

Price-sensitive retail customers increasingly compare fees, rates and UX across apps—Mexico's smartphone penetration (~79% in 2024) accelerates this transparency and raises customer bargaining power. Fintech wallets and retailers now offer cheaper payment rails and installment options, eroding fees on transactional products where switching is easiest. Customers switch less for credit and pensions, but loyalty programs and bundled services materially curb churn.

Digital service expectations

Customers now demand instant onboarding, 24/7 reliability and rich feature sets, and Banorte, as one of Mexico’s largest banks by assets, faces rapid churn when outages or friction occur. App store ratings and social media amplify buyer influence, turning single incidents into broad reputational risk. Continuous release cycles and CX analytics are essential defenses to retain digitally-savvy clients.

SMEs’ credit access

SMEs in Mexico represent 99.8% of firms and contribute roughly 52% of GDP (INEGI, 2024), giving them substantial bargaining power over credit terms as they prioritize speed and flexibility and use aggregation platforms to compare offers. Alternative lenders and fintechs, often delivering underwriting and funding within hours to a day, have reset SME expectations on turnaround times. SMEs routinely negotiate collateral, covenants and pricing, while embedded finance partnerships (e.g., POS and ERP integrations) help rival banks retain SME flows.

- SME market share: 99.8% of firms (INEGI, 2024)

- Key demand: speed, flexibility, multi-offer platforms

- Negotiation levers: collateral, covenants, pricing

- Retention tool: embedded finance via POS/ERP partnerships

Regulatory transparency empowering buyers

Regulatory transparency in 2024—with Banorte holding about MXN 4.2 trillion in assets and roughly 17% market share—boosts product comparability through mandatory disclosure and consumer protection rules, reducing information asymmetry and strengthening buyer decisions. Robust complaint mechanisms create pricing and practice pressure, while clear value propositions and financial education blunt purely price-driven switching.

- Disclosure: standardized facts increase comparability

- Asymmetry: clearer data strengthens buyer choice

- Complaints: regulatory channels pressure pricing

- Offset: education and value propositions reduce churn

Corporate RFPs compress spreads; mobile retail and SMEs strengthen bargaining power

Large corporates and government clients wield pricing leverage—Banorte holds ~18% market share (~MXN 4.2T assets in 2024) so high-volume RFPs compress spreads. Retail customers (smartphone penetration ~79% in 2024) and fintechs raise fee transparency and switching. SMEs (99.8% of firms; ~52% GDP) demand speed and flexibility, strengthening bargaining power.

| Metric | 2024 |

|---|---|

| Banorte market share | ~18% (MXN 4.2T) |

| Smartphone penetration | ~79% |

| SMEs share of firms | 99.8% |

| SMEs contribution to GDP | ~52% |

Same Document Delivered

Banorte Porter's Five Forces Analysis

This preview shows the exact Banorte Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted and ready for download and use the moment you buy. No mockups; this is the final deliverable.