Baoshan Iron & Steel SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

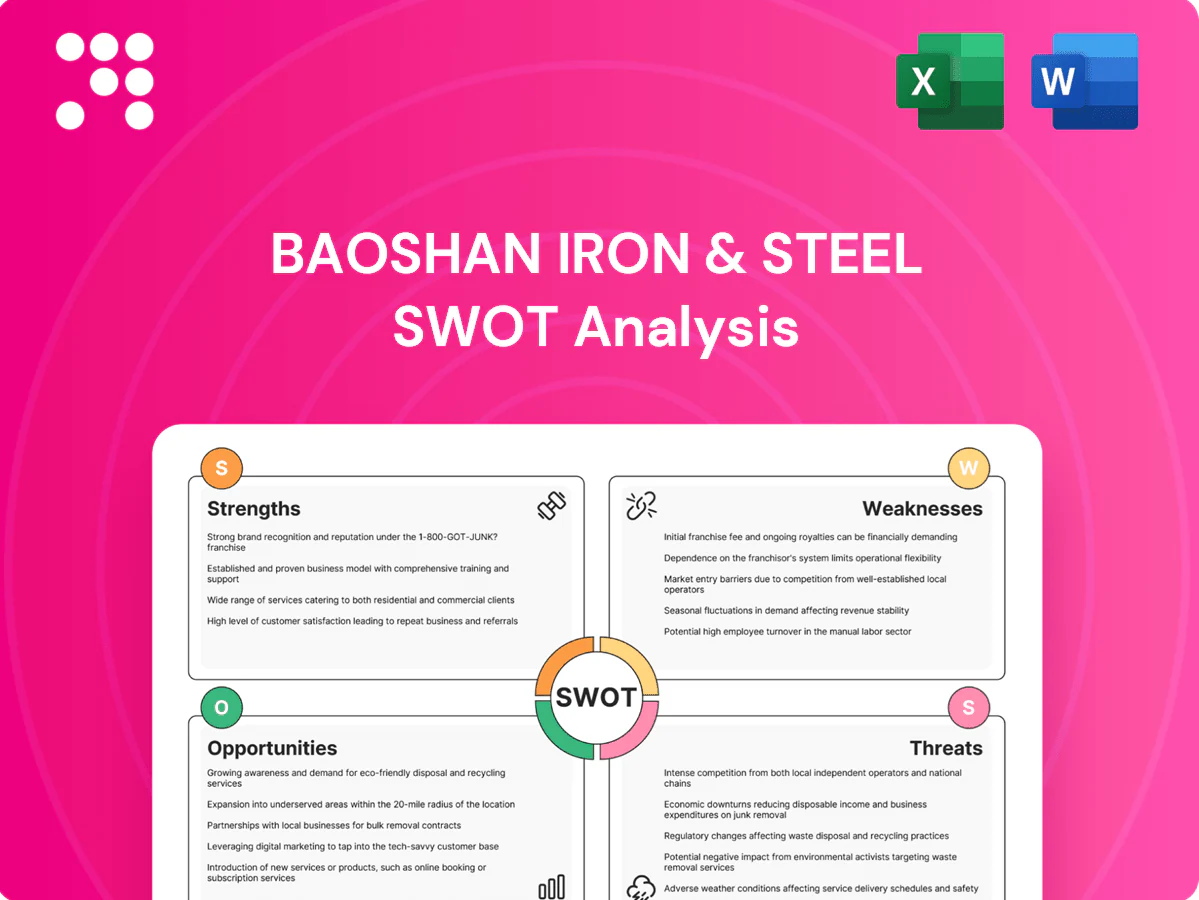

Baoshan Iron & Steel’s SWOT highlights its scale, integrated supply chain, and advancing low‑carbon tech as core strengths, offset by cyclicality, legacy assets, and leverage; opportunities include domestic infrastructure demand and green steel adoption, while competition, raw material volatility, and policy risks are key threats. Want the complete, editable SWOT with financial context and strategic takeaways? Purchase the full report to inform investment or strategy decisions.

Strengths

Scale and product breadth

Baoshan’s large-scale operations (annual crude steel capacity exceeding 40 million tonnes) drive procurement, production and distribution economies; its portfolio across carbon, stainless and special steels lets it serve automotive, construction and energy end-markets; this breadth helped Baoshan limit revenue swings in 2024 as cross‑selling raised customer retention and balanced cyclical segments.

Advanced manufacturing capabilities

Baoshan Iron & Steel leverages advanced manufacturing and stringent quality control to produce automotive-grade and specialty steels, enabling tighter tolerances and consistent performance that distinguish it from commodity-focused peers. Its focus on high-end processes supports premium pricing in niches such as automotive and aerospace, contributing to improved margins; Baoshan reported RMB 148.2 billion revenue from high-value steel products in 2024. This capability underpins long-term contract wins and higher ASPs per ton.

Strong end-market exposure

Baoshan serves automotive, construction, appliances and machinery, giving multiple demand pillars that reduce reliance on any single sector. Automotive and machinery demand higher-spec steels—supporting better margins—while construction and infrastructure deliver volume stability. As part of China Baowu (around 126 million tonnes crude steel in 2023), Baoshan benefits from scale and diversified end-market exposure.

R&D and innovation focus

Baoshan Iron & Steel’s focused R&D — backed by a reported R&D outlay of about RMB 1.15 billion in 2024 — accelerates development of high-strength, corrosion-resistant and specialty steels, enabling faster OEM customization and supporting moves into higher value-added segments; high-strength steel sales rose ~14% YoY in 2024.

- R&D spend: RMB 1.15bn (2024)

- High-strength sales growth: ~14% YoY (2024)

- Faster OEM customization

- Pathway to higher value-added segments

Global reach and customer relationships

Baoshan Iron & Steel (600019.SH), part of China Baowu, supplies both domestic and international customers, widening market access and reducing regional demand swings; its status within the world’s largest steelmaker group strengthens cross-border channels. Long-term contracts with industrial clients improve demand visibility and planning. Integrated technical services and after-sales support raise switching costs and help optimize capacity utilization across global channels.

- Global footprint via China Baowu affiliation

- Long-term industrial contracts boost demand visibility

- Technical service integration increases switching costs

- Global channels improve capacity utilization

Scale >40Mt underpins premium steels; RMB148.2bn high-value revenue (2024)

Baoshan’s scale (crude steel capacity >40Mt) delivers procurement and distribution economies and cross‑selling across carbon, stainless and special steels, stabilizing 2024 revenues. Advanced manufacturing and QA support premium automotive/aerospace ASPs; high‑value product revenue RMB148.2bn (2024). R&D RMB1.15bn (2024) fuels high‑strength sales +14% YoY, backed by China Baowu group scale.

| Metric | 2023/2024 |

|---|---|

| Crude capacity | >40 Mt |

| High‑value revenue | RMB148.2bn (2024) |

| R&D spend | RMB1.15bn (2024) |

| High‑strength sales growth | +14% YoY (2024) |

| China Baowu group capacity | ~126 Mt (2023) |

What is included in the product

Provides a concise SWOT analysis of Baoshan Iron & Steel, highlighting its scale, integrated production capabilities and strong domestic market position as strengths; exposure to commodity cycles, high leverage and regulatory/environmental pressures as weaknesses; opportunities from green steel transition, infrastructure demand and export growth; and threats from global competition, demand cyclicality and policy shifts.

Provides a concise, Baoshan Iron & Steel–specific SWOT matrix for fast strategic alignment and stakeholder-ready summaries, easing decision-making under market and regulatory pressures.

Weaknesses

High capital intensity and fixed costs

Integrated steelmaking at Baoshan requires substantial ongoing capex and maintenance, leaving high fixed costs that magnify profit swings in downturns. Large-scale, integrated facilities are less flexible to rapid demand changes, so utilization dips rapidly compress margins. China accounted for 1,013 Mt crude steel in 2023, underscoring scale-driven exposure in domestic cyclicality.

Exposure to raw material volatility

Exposure to raw material volatility hits Baoshan as swings in iron ore, coking coal and energy directly lift input costs; China produced about 1.05 billion tonnes of crude steel in 2024, keeping raw-material demand tight. Passing price spikes to customers lags and erodes margins during downturns. Hedging reduces but cannot eliminate basis and timing risk, and procurement concentration raises supply-disruption vulnerability.

Cyclical demand sensitivity

Steel consumption is highly correlated with construction, infrastructure and manufacturing cycles, with construction accounting for roughly 50% of global steel use, leaving Baoshan volumes exposed to property and industrial slowdowns. China rebar and hot-rolled coil prices swung more than 15% during 2023–24 amid inventory destocking, intensifying volume and margin volatility. Forecasting errors can force suboptimal production runs and costly restarts.

Environmental and energy intensity

Baoshan relies heavily on traditional blast-furnace BOF routes, which remain carbon- and energy-intensive (steel sector average ~2.1 tCO2/t crude steel per World Steel Association). Meeting tightening emissions and efficiency standards raises operating and compliance costs; decarbonization demands multibillion-yuan capex and new technologies. Delays risk license-to-operate issues and losing customers shifting to low-carbon steel.

- High carbon intensity ~2.1 tCO2/t

- Multibillion-yuan decarbonization capex

- Rising compliance costs

- Risk to market access and customer preference

Product and operational complexity

Serving many grades and sectors forces Baoshan Iron & Steel into tighter scheduling and heavier quality-control protocols, increasing lead-time variability and inspection workloads. Complex product mixes raise working capital tied up in inventories and semi-finished goods, and they elevate risks of yield loss and rework during production. Coordination across dispersed supply-chain nodes becomes more challenging, stressing logistics and supplier alignment.

- Higher scheduling and QC burden

- Increased inventory and working capital requirements

- Greater yield loss and rework risk

- Harder cross‑node supply chain coordination

China 2024 steel: 1.05bn t output, >15% price swings squeeze margins; decarbonization costs rise

High fixed costs from integrated BOF/DRI operations amplify downturn losses; China produced ~1.05 billion t crude steel in 2024, keeping market cyclicality acute. Input-cost exposure (iron ore, coking coal, energy) and >15% domestic price swings in 2023–24 compress margins. Carbon intensity ~2.1 tCO2/t forces multibillion-yuan decarbonization capex and rising compliance costs, risking market access shift to low‑carbon steel.

| Metric | 2023–24 / 2024 |

|---|---|

| China crude steel | ~1.05 billion t (2024) |

| Price swings | >15% (2023–24) |

| Carbon intensity | ~2.1 tCO2/t |

Same Document Delivered

Baoshan Iron & Steel SWOT Analysis

This is a real excerpt from the Baoshan Iron & Steel SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects its structure and depth. Buy now to unlock the complete, editable SWOT file.

Go Beyond the Preview—Access the Full Strategic Report

Baoshan Iron & Steel’s SWOT highlights its scale, integrated supply chain, and advancing low‑carbon tech as core strengths, offset by cyclicality, legacy assets, and leverage; opportunities include domestic infrastructure demand and green steel adoption, while competition, raw material volatility, and policy risks are key threats. Want the complete, editable SWOT with financial context and strategic takeaways? Purchase the full report to inform investment or strategy decisions.

Strengths

Scale and product breadth

Baoshan’s large-scale operations (annual crude steel capacity exceeding 40 million tonnes) drive procurement, production and distribution economies; its portfolio across carbon, stainless and special steels lets it serve automotive, construction and energy end-markets; this breadth helped Baoshan limit revenue swings in 2024 as cross‑selling raised customer retention and balanced cyclical segments.

Advanced manufacturing capabilities

Baoshan Iron & Steel leverages advanced manufacturing and stringent quality control to produce automotive-grade and specialty steels, enabling tighter tolerances and consistent performance that distinguish it from commodity-focused peers. Its focus on high-end processes supports premium pricing in niches such as automotive and aerospace, contributing to improved margins; Baoshan reported RMB 148.2 billion revenue from high-value steel products in 2024. This capability underpins long-term contract wins and higher ASPs per ton.

Strong end-market exposure

Baoshan serves automotive, construction, appliances and machinery, giving multiple demand pillars that reduce reliance on any single sector. Automotive and machinery demand higher-spec steels—supporting better margins—while construction and infrastructure deliver volume stability. As part of China Baowu (around 126 million tonnes crude steel in 2023), Baoshan benefits from scale and diversified end-market exposure.

R&D and innovation focus

Baoshan Iron & Steel’s focused R&D — backed by a reported R&D outlay of about RMB 1.15 billion in 2024 — accelerates development of high-strength, corrosion-resistant and specialty steels, enabling faster OEM customization and supporting moves into higher value-added segments; high-strength steel sales rose ~14% YoY in 2024.

- R&D spend: RMB 1.15bn (2024)

- High-strength sales growth: ~14% YoY (2024)

- Faster OEM customization

- Pathway to higher value-added segments

Global reach and customer relationships

Baoshan Iron & Steel (600019.SH), part of China Baowu, supplies both domestic and international customers, widening market access and reducing regional demand swings; its status within the world’s largest steelmaker group strengthens cross-border channels. Long-term contracts with industrial clients improve demand visibility and planning. Integrated technical services and after-sales support raise switching costs and help optimize capacity utilization across global channels.

- Global footprint via China Baowu affiliation

- Long-term industrial contracts boost demand visibility

- Technical service integration increases switching costs

- Global channels improve capacity utilization

Scale >40Mt underpins premium steels; RMB148.2bn high-value revenue (2024)

Baoshan’s scale (crude steel capacity >40Mt) delivers procurement and distribution economies and cross‑selling across carbon, stainless and special steels, stabilizing 2024 revenues. Advanced manufacturing and QA support premium automotive/aerospace ASPs; high‑value product revenue RMB148.2bn (2024). R&D RMB1.15bn (2024) fuels high‑strength sales +14% YoY, backed by China Baowu group scale.

| Metric | 2023/2024 |

|---|---|

| Crude capacity | >40 Mt |

| High‑value revenue | RMB148.2bn (2024) |

| R&D spend | RMB1.15bn (2024) |

| High‑strength sales growth | +14% YoY (2024) |

| China Baowu group capacity | ~126 Mt (2023) |

What is included in the product

Provides a concise SWOT analysis of Baoshan Iron & Steel, highlighting its scale, integrated production capabilities and strong domestic market position as strengths; exposure to commodity cycles, high leverage and regulatory/environmental pressures as weaknesses; opportunities from green steel transition, infrastructure demand and export growth; and threats from global competition, demand cyclicality and policy shifts.

Provides a concise, Baoshan Iron & Steel–specific SWOT matrix for fast strategic alignment and stakeholder-ready summaries, easing decision-making under market and regulatory pressures.

Weaknesses

High capital intensity and fixed costs

Integrated steelmaking at Baoshan requires substantial ongoing capex and maintenance, leaving high fixed costs that magnify profit swings in downturns. Large-scale, integrated facilities are less flexible to rapid demand changes, so utilization dips rapidly compress margins. China accounted for 1,013 Mt crude steel in 2023, underscoring scale-driven exposure in domestic cyclicality.

Exposure to raw material volatility

Exposure to raw material volatility hits Baoshan as swings in iron ore, coking coal and energy directly lift input costs; China produced about 1.05 billion tonnes of crude steel in 2024, keeping raw-material demand tight. Passing price spikes to customers lags and erodes margins during downturns. Hedging reduces but cannot eliminate basis and timing risk, and procurement concentration raises supply-disruption vulnerability.

Cyclical demand sensitivity

Steel consumption is highly correlated with construction, infrastructure and manufacturing cycles, with construction accounting for roughly 50% of global steel use, leaving Baoshan volumes exposed to property and industrial slowdowns. China rebar and hot-rolled coil prices swung more than 15% during 2023–24 amid inventory destocking, intensifying volume and margin volatility. Forecasting errors can force suboptimal production runs and costly restarts.

Environmental and energy intensity

Baoshan relies heavily on traditional blast-furnace BOF routes, which remain carbon- and energy-intensive (steel sector average ~2.1 tCO2/t crude steel per World Steel Association). Meeting tightening emissions and efficiency standards raises operating and compliance costs; decarbonization demands multibillion-yuan capex and new technologies. Delays risk license-to-operate issues and losing customers shifting to low-carbon steel.

- High carbon intensity ~2.1 tCO2/t

- Multibillion-yuan decarbonization capex

- Rising compliance costs

- Risk to market access and customer preference

Product and operational complexity

Serving many grades and sectors forces Baoshan Iron & Steel into tighter scheduling and heavier quality-control protocols, increasing lead-time variability and inspection workloads. Complex product mixes raise working capital tied up in inventories and semi-finished goods, and they elevate risks of yield loss and rework during production. Coordination across dispersed supply-chain nodes becomes more challenging, stressing logistics and supplier alignment.

- Higher scheduling and QC burden

- Increased inventory and working capital requirements

- Greater yield loss and rework risk

- Harder cross‑node supply chain coordination

China 2024 steel: 1.05bn t output, >15% price swings squeeze margins; decarbonization costs rise

High fixed costs from integrated BOF/DRI operations amplify downturn losses; China produced ~1.05 billion t crude steel in 2024, keeping market cyclicality acute. Input-cost exposure (iron ore, coking coal, energy) and >15% domestic price swings in 2023–24 compress margins. Carbon intensity ~2.1 tCO2/t forces multibillion-yuan decarbonization capex and rising compliance costs, risking market access shift to low‑carbon steel.

| Metric | 2023–24 / 2024 |

|---|---|

| China crude steel | ~1.05 billion t (2024) |

| Price swings | >15% (2023–24) |

| Carbon intensity | ~2.1 tCO2/t |

Same Document Delivered

Baoshan Iron & Steel SWOT Analysis

This is a real excerpt from the Baoshan Iron & Steel SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects its structure and depth. Buy now to unlock the complete, editable SWOT file.

Description

Go Beyond the Preview—Access the Full Strategic Report

Baoshan Iron & Steel’s SWOT highlights its scale, integrated supply chain, and advancing low‑carbon tech as core strengths, offset by cyclicality, legacy assets, and leverage; opportunities include domestic infrastructure demand and green steel adoption, while competition, raw material volatility, and policy risks are key threats. Want the complete, editable SWOT with financial context and strategic takeaways? Purchase the full report to inform investment or strategy decisions.

Strengths

Scale and product breadth

Baoshan’s large-scale operations (annual crude steel capacity exceeding 40 million tonnes) drive procurement, production and distribution economies; its portfolio across carbon, stainless and special steels lets it serve automotive, construction and energy end-markets; this breadth helped Baoshan limit revenue swings in 2024 as cross‑selling raised customer retention and balanced cyclical segments.

Advanced manufacturing capabilities

Baoshan Iron & Steel leverages advanced manufacturing and stringent quality control to produce automotive-grade and specialty steels, enabling tighter tolerances and consistent performance that distinguish it from commodity-focused peers. Its focus on high-end processes supports premium pricing in niches such as automotive and aerospace, contributing to improved margins; Baoshan reported RMB 148.2 billion revenue from high-value steel products in 2024. This capability underpins long-term contract wins and higher ASPs per ton.

Strong end-market exposure

Baoshan serves automotive, construction, appliances and machinery, giving multiple demand pillars that reduce reliance on any single sector. Automotive and machinery demand higher-spec steels—supporting better margins—while construction and infrastructure deliver volume stability. As part of China Baowu (around 126 million tonnes crude steel in 2023), Baoshan benefits from scale and diversified end-market exposure.

R&D and innovation focus

Baoshan Iron & Steel’s focused R&D — backed by a reported R&D outlay of about RMB 1.15 billion in 2024 — accelerates development of high-strength, corrosion-resistant and specialty steels, enabling faster OEM customization and supporting moves into higher value-added segments; high-strength steel sales rose ~14% YoY in 2024.

- R&D spend: RMB 1.15bn (2024)

- High-strength sales growth: ~14% YoY (2024)

- Faster OEM customization

- Pathway to higher value-added segments

Global reach and customer relationships

Baoshan Iron & Steel (600019.SH), part of China Baowu, supplies both domestic and international customers, widening market access and reducing regional demand swings; its status within the world’s largest steelmaker group strengthens cross-border channels. Long-term contracts with industrial clients improve demand visibility and planning. Integrated technical services and after-sales support raise switching costs and help optimize capacity utilization across global channels.

- Global footprint via China Baowu affiliation

- Long-term industrial contracts boost demand visibility

- Technical service integration increases switching costs

- Global channels improve capacity utilization

Scale >40Mt underpins premium steels; RMB148.2bn high-value revenue (2024)

Baoshan’s scale (crude steel capacity >40Mt) delivers procurement and distribution economies and cross‑selling across carbon, stainless and special steels, stabilizing 2024 revenues. Advanced manufacturing and QA support premium automotive/aerospace ASPs; high‑value product revenue RMB148.2bn (2024). R&D RMB1.15bn (2024) fuels high‑strength sales +14% YoY, backed by China Baowu group scale.

| Metric | 2023/2024 |

|---|---|

| Crude capacity | >40 Mt |

| High‑value revenue | RMB148.2bn (2024) |

| R&D spend | RMB1.15bn (2024) |

| High‑strength sales growth | +14% YoY (2024) |

| China Baowu group capacity | ~126 Mt (2023) |

What is included in the product

Provides a concise SWOT analysis of Baoshan Iron & Steel, highlighting its scale, integrated production capabilities and strong domestic market position as strengths; exposure to commodity cycles, high leverage and regulatory/environmental pressures as weaknesses; opportunities from green steel transition, infrastructure demand and export growth; and threats from global competition, demand cyclicality and policy shifts.

Provides a concise, Baoshan Iron & Steel–specific SWOT matrix for fast strategic alignment and stakeholder-ready summaries, easing decision-making under market and regulatory pressures.

Weaknesses

High capital intensity and fixed costs

Integrated steelmaking at Baoshan requires substantial ongoing capex and maintenance, leaving high fixed costs that magnify profit swings in downturns. Large-scale, integrated facilities are less flexible to rapid demand changes, so utilization dips rapidly compress margins. China accounted for 1,013 Mt crude steel in 2023, underscoring scale-driven exposure in domestic cyclicality.

Exposure to raw material volatility

Exposure to raw material volatility hits Baoshan as swings in iron ore, coking coal and energy directly lift input costs; China produced about 1.05 billion tonnes of crude steel in 2024, keeping raw-material demand tight. Passing price spikes to customers lags and erodes margins during downturns. Hedging reduces but cannot eliminate basis and timing risk, and procurement concentration raises supply-disruption vulnerability.

Cyclical demand sensitivity

Steel consumption is highly correlated with construction, infrastructure and manufacturing cycles, with construction accounting for roughly 50% of global steel use, leaving Baoshan volumes exposed to property and industrial slowdowns. China rebar and hot-rolled coil prices swung more than 15% during 2023–24 amid inventory destocking, intensifying volume and margin volatility. Forecasting errors can force suboptimal production runs and costly restarts.

Environmental and energy intensity

Baoshan relies heavily on traditional blast-furnace BOF routes, which remain carbon- and energy-intensive (steel sector average ~2.1 tCO2/t crude steel per World Steel Association). Meeting tightening emissions and efficiency standards raises operating and compliance costs; decarbonization demands multibillion-yuan capex and new technologies. Delays risk license-to-operate issues and losing customers shifting to low-carbon steel.

- High carbon intensity ~2.1 tCO2/t

- Multibillion-yuan decarbonization capex

- Rising compliance costs

- Risk to market access and customer preference

Product and operational complexity

Serving many grades and sectors forces Baoshan Iron & Steel into tighter scheduling and heavier quality-control protocols, increasing lead-time variability and inspection workloads. Complex product mixes raise working capital tied up in inventories and semi-finished goods, and they elevate risks of yield loss and rework during production. Coordination across dispersed supply-chain nodes becomes more challenging, stressing logistics and supplier alignment.

- Higher scheduling and QC burden

- Increased inventory and working capital requirements

- Greater yield loss and rework risk

- Harder cross‑node supply chain coordination

China 2024 steel: 1.05bn t output, >15% price swings squeeze margins; decarbonization costs rise

High fixed costs from integrated BOF/DRI operations amplify downturn losses; China produced ~1.05 billion t crude steel in 2024, keeping market cyclicality acute. Input-cost exposure (iron ore, coking coal, energy) and >15% domestic price swings in 2023–24 compress margins. Carbon intensity ~2.1 tCO2/t forces multibillion-yuan decarbonization capex and rising compliance costs, risking market access shift to low‑carbon steel.

| Metric | 2023–24 / 2024 |

|---|---|

| China crude steel | ~1.05 billion t (2024) |

| Price swings | >15% (2023–24) |

| Carbon intensity | ~2.1 tCO2/t |

Same Document Delivered

Baoshan Iron & Steel SWOT Analysis

This is a real excerpt from the Baoshan Iron & Steel SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects its structure and depth. Buy now to unlock the complete, editable SWOT file.