Bar Harbor Bankshares PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE analysis of Bar Harbor Bankshares—mapping political, economic, social, technological, legal and environmental forces shaping its outlook. Actionable insights reveal risks and growth levers for investors and managers. Ready-made and research-backed, it saves you hours. Purchase the full report to access the complete analysis now.

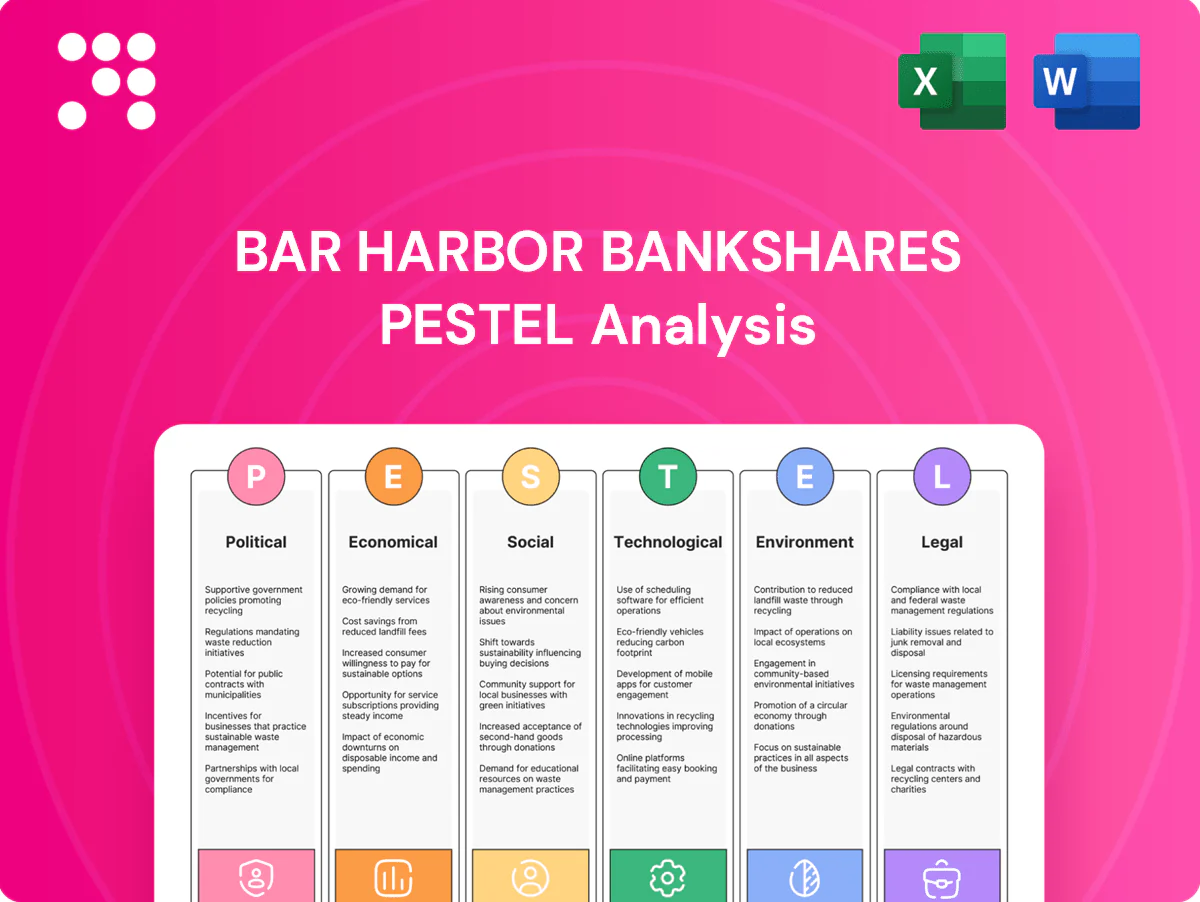

Political factors

State-level banking incentives and oversight

Operating across Maine (pop. ~1.37M), New Hampshire (1.38M) and Vermont (0.65M) exposes Bar Harbor Bankshares to three distinct state banking priorities and supervisory nuances. State programs for community development, broadband and housing—often funded via federal ARPA and state bond initiatives—can boost loan demand while directing capital to targeted sectors. Close alignment with state economic agendas enhances franchise value but demands nimble compliance and stakeholder engagement. Ongoing monitoring of legislative sessions and banking department guidance is essential for timely resource allocation.

Federal fiscal policy and infrastructure funding

Federal infrastructure programs such as the $1.2 trillion Bipartisan Infrastructure Law and $1.9 trillion American Rescue Plan drive municipal deposits, construction lending and treasury services in Northern New England, with millions flowing via formula grants and competitive awards. Timing lags between appropriations and local project starts create forecasting challenges for loan and deposit pipelines. Public‑private partnerships expand fee income opportunities in cash management. Shifts in federal budget priorities can quickly alter regional liquidity dynamics.

Community banking and rural development priorities

Bipartisan support for community banks and rural credit access has produced programs and guarantees that Bar Harbor Bankshares can tap to boost CRA-aligned lending; Bar Harbor reported about $3.2 billion in assets (2024) enabling targeted deployment. Advocacy outcomes shaping SBA and USDA guarantees—SBA 7(a) and USDA rural housing/USDA business programs—expand risk-adjusted returns while increasing inclusion. Reduced or delayed appropriations would slow targeted lending momentum and could raise funding costs.

Cross-border and regional trade exposure

Northern New England’s proximity to Canada links local businesses to cross-border tourism and trade; US–Canada goods and services trade exceeded 700 billion in 2023, making policy shifts material for gateway towns. Political frictions, tariffs or border-staffing changes can compress small-business cash flows and seasonal deposits, while a stable policy environment supports steady transaction volumes. Contingency planning for policy shocks reduces concentration risk.

- Cross-border dependence: high in coastal/gateway towns

- Macro fact: US–Canada trade >700bn in 2023

- Risk: tariffs/border staffing → seasonal deposit volatility

- Mitigation: contingency plans to manage concentration

Local taxation and municipal policy

Local property tax regimes, zoning changes, and municipal housing initiatives directly affect Bar Harbor Bankshares' collateral values and regional real estate activity, shaping loan volumes and loss assumptions. Competitive municipal cash management RFPs and deposit regulations influence access to low-cost public deposits. Policy-driven affordable housing programs create construction and permanent lending opportunities with layered credits, while rapid tax reassessments or moratoria can briefly chill lending appetite.

- Property tax & zoning: affect collateral values

- Municipal deposits: low-cost funding source

- Affordable housing: pipeline for construction/permanent loans

- Tax reassessments: temporary underwriting caution

Regional bank navigates ME/NH/VT rules, backing municipal builds with $3.2B

Bar Harbor faces multi-state regulatory nuance across ME/NH/VT, driving compliance costs but unlocking community-lending programs; assets ≈ $3.2B (2024). Federal infrastructure and ARPA funding fuel municipal deposits and construction loans; US–Canada trade >700bn (2023) affects border towns. Municipal tax/zoning shifts alter collateral values and deposit access; contingency plans reduce concentration risk.

| Metric | Value |

|---|---|

| Assets (2024) | $3.2B |

| US–Canada trade (2023) | >$700B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bar Harbor Bankshares across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by regional data and current trends. Designed for executives and investors, the analysis offers forward-looking insights, actionable risks and opportunities, and formatted content ready for plans and reports.

A concise, visually segmented PESTLE summary for Bar Harbor Bankshares that eases meeting prep and strategic reviews, easily dropped into presentations or shared for quick team alignment while allowing note additions for regional or business-line context.

Economic factors

Interest rate cycle and net interest margin

Rate volatility, with the federal funds target at 5.25–5.50% (July 2025), directly alters funding costs, loan yields and deposit betas, squeezing community bank NIMs. In competitive New England markets Bar Harbor may face faster deposit repricing, pressuring margins. Strong asset‑liability discipline stabilizes NIM across cycles. Active hedging and product‑mix shifts mitigate earnings swings.

Tourism and seasonal business dynamics

Maine draws millions of visitors annually (Maine Office of Tourism), driving pronounced seasonal deposits and credit utilization across hospitality, retail and services.

Off-season cash flow softness elevates credit-monitoring and collections needs for Bar Harbor Bankshares as operating cash and collateral values fall.

Tailored working-capital lines and treasury services smooth seasonality while weather and travel trends can materially amplify swings in fee and interest income.

Housing market and construction activity

Regional housing supply constraints and in-migration in Maine tighten mortgage and construction pipelines, pressuring affordability and origination volumes. Rising construction input costs — roughly 6% year-over-year through mid-2024 per BLS PPI — and appraisal volatility can reduce collateral coverage and slow draws. Portfolio mix between fixed and adjustable-rate loans determines sensitivity to Fed hikes, while public housing and LIHTC projects create lower-risk, lower-yield lending opportunities.

SMB health and labor market conditions

Local SMBs in Bar Harbor Bankshares markets face tight labor markets with Maine unemployment at 3.5% (June 2025) and NFIB reporting 27% of small firms with few or no qualified applicants in 2024, driving wage inflation and input cost variability. Credit performance closely tracks regional employment and consumer confidence, stressing smaller lenders during downturns. Advisory and cash management solutions can bolster client resilience while sector diversification reduces localized downturn risk.

- labor: Maine unemployment 3.5% (Jun 2025)

- labor shortage: 27% SMBs report few/no qualified applicants (NFIB 2024)

- credit link: defaults correlated with regional employment

- mitigation: advisory, cash mgmt, sector diversification

Deposit competition and liquidity

Higher market rates (federal funds 5.25–5.50% since 2023) and money-market/high-yield savings yields above 4% have intensified competition for core deposits; Bar Harbor leans on relationship banking, treasury services and wealth offerings to defend balances. Maintaining liquidity buffers and contingent funding plans is critical under stress, while pricing discipline balances deposit growth with margin protection.

- Fed funds 5.25–5.50%

- Money-market/HH savings >4%

- Focus: relationship banking, treasury, wealth

- Key: liquidity buffers, contingent funding

- Strategy: disciplined pricing vs growth

Regional bank navigates ME/NH/VT rules, backing municipal builds with $3.2B

Rate volatility (fed funds 5.25–5.50% Jul 2025) and >4% money‑market yields compress NIMs, requiring hedging and product mix shifts. Maine unemployment 3.5% (Jun 2025) and 27% SMBs reporting hiring difficulty (NFIB 2024) drive wage pressure and credit sensitivity. Tourism seasonality creates volatile deposits and loan demand; construction PPI +6% y/y mid‑2024 tightens origination economics.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Funding cost |

| Unemployment ME | 3.5% | Wage pressure |

| SMB hiring | 27% | Credit risk |

| Construction PPI | +6% y/y | Origination |

Preview Before You Purchase

Bar Harbor Bankshares PESTLE Analysis

The Bar Harbor Bankshares PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete Political, Economic, Social, Technological, Legal, and Environmental assessment as displayed. No placeholders or teasers—this is the final file you’ll download immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE analysis of Bar Harbor Bankshares—mapping political, economic, social, technological, legal and environmental forces shaping its outlook. Actionable insights reveal risks and growth levers for investors and managers. Ready-made and research-backed, it saves you hours. Purchase the full report to access the complete analysis now.

Political factors

State-level banking incentives and oversight

Operating across Maine (pop. ~1.37M), New Hampshire (1.38M) and Vermont (0.65M) exposes Bar Harbor Bankshares to three distinct state banking priorities and supervisory nuances. State programs for community development, broadband and housing—often funded via federal ARPA and state bond initiatives—can boost loan demand while directing capital to targeted sectors. Close alignment with state economic agendas enhances franchise value but demands nimble compliance and stakeholder engagement. Ongoing monitoring of legislative sessions and banking department guidance is essential for timely resource allocation.

Federal fiscal policy and infrastructure funding

Federal infrastructure programs such as the $1.2 trillion Bipartisan Infrastructure Law and $1.9 trillion American Rescue Plan drive municipal deposits, construction lending and treasury services in Northern New England, with millions flowing via formula grants and competitive awards. Timing lags between appropriations and local project starts create forecasting challenges for loan and deposit pipelines. Public‑private partnerships expand fee income opportunities in cash management. Shifts in federal budget priorities can quickly alter regional liquidity dynamics.

Community banking and rural development priorities

Bipartisan support for community banks and rural credit access has produced programs and guarantees that Bar Harbor Bankshares can tap to boost CRA-aligned lending; Bar Harbor reported about $3.2 billion in assets (2024) enabling targeted deployment. Advocacy outcomes shaping SBA and USDA guarantees—SBA 7(a) and USDA rural housing/USDA business programs—expand risk-adjusted returns while increasing inclusion. Reduced or delayed appropriations would slow targeted lending momentum and could raise funding costs.

Cross-border and regional trade exposure

Northern New England’s proximity to Canada links local businesses to cross-border tourism and trade; US–Canada goods and services trade exceeded 700 billion in 2023, making policy shifts material for gateway towns. Political frictions, tariffs or border-staffing changes can compress small-business cash flows and seasonal deposits, while a stable policy environment supports steady transaction volumes. Contingency planning for policy shocks reduces concentration risk.

- Cross-border dependence: high in coastal/gateway towns

- Macro fact: US–Canada trade >700bn in 2023

- Risk: tariffs/border staffing → seasonal deposit volatility

- Mitigation: contingency plans to manage concentration

Local taxation and municipal policy

Local property tax regimes, zoning changes, and municipal housing initiatives directly affect Bar Harbor Bankshares' collateral values and regional real estate activity, shaping loan volumes and loss assumptions. Competitive municipal cash management RFPs and deposit regulations influence access to low-cost public deposits. Policy-driven affordable housing programs create construction and permanent lending opportunities with layered credits, while rapid tax reassessments or moratoria can briefly chill lending appetite.

- Property tax & zoning: affect collateral values

- Municipal deposits: low-cost funding source

- Affordable housing: pipeline for construction/permanent loans

- Tax reassessments: temporary underwriting caution

Regional bank navigates ME/NH/VT rules, backing municipal builds with $3.2B

Bar Harbor faces multi-state regulatory nuance across ME/NH/VT, driving compliance costs but unlocking community-lending programs; assets ≈ $3.2B (2024). Federal infrastructure and ARPA funding fuel municipal deposits and construction loans; US–Canada trade >700bn (2023) affects border towns. Municipal tax/zoning shifts alter collateral values and deposit access; contingency plans reduce concentration risk.

| Metric | Value |

|---|---|

| Assets (2024) | $3.2B |

| US–Canada trade (2023) | >$700B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bar Harbor Bankshares across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by regional data and current trends. Designed for executives and investors, the analysis offers forward-looking insights, actionable risks and opportunities, and formatted content ready for plans and reports.

A concise, visually segmented PESTLE summary for Bar Harbor Bankshares that eases meeting prep and strategic reviews, easily dropped into presentations or shared for quick team alignment while allowing note additions for regional or business-line context.

Economic factors

Interest rate cycle and net interest margin

Rate volatility, with the federal funds target at 5.25–5.50% (July 2025), directly alters funding costs, loan yields and deposit betas, squeezing community bank NIMs. In competitive New England markets Bar Harbor may face faster deposit repricing, pressuring margins. Strong asset‑liability discipline stabilizes NIM across cycles. Active hedging and product‑mix shifts mitigate earnings swings.

Tourism and seasonal business dynamics

Maine draws millions of visitors annually (Maine Office of Tourism), driving pronounced seasonal deposits and credit utilization across hospitality, retail and services.

Off-season cash flow softness elevates credit-monitoring and collections needs for Bar Harbor Bankshares as operating cash and collateral values fall.

Tailored working-capital lines and treasury services smooth seasonality while weather and travel trends can materially amplify swings in fee and interest income.

Housing market and construction activity

Regional housing supply constraints and in-migration in Maine tighten mortgage and construction pipelines, pressuring affordability and origination volumes. Rising construction input costs — roughly 6% year-over-year through mid-2024 per BLS PPI — and appraisal volatility can reduce collateral coverage and slow draws. Portfolio mix between fixed and adjustable-rate loans determines sensitivity to Fed hikes, while public housing and LIHTC projects create lower-risk, lower-yield lending opportunities.

SMB health and labor market conditions

Local SMBs in Bar Harbor Bankshares markets face tight labor markets with Maine unemployment at 3.5% (June 2025) and NFIB reporting 27% of small firms with few or no qualified applicants in 2024, driving wage inflation and input cost variability. Credit performance closely tracks regional employment and consumer confidence, stressing smaller lenders during downturns. Advisory and cash management solutions can bolster client resilience while sector diversification reduces localized downturn risk.

- labor: Maine unemployment 3.5% (Jun 2025)

- labor shortage: 27% SMBs report few/no qualified applicants (NFIB 2024)

- credit link: defaults correlated with regional employment

- mitigation: advisory, cash mgmt, sector diversification

Deposit competition and liquidity

Higher market rates (federal funds 5.25–5.50% since 2023) and money-market/high-yield savings yields above 4% have intensified competition for core deposits; Bar Harbor leans on relationship banking, treasury services and wealth offerings to defend balances. Maintaining liquidity buffers and contingent funding plans is critical under stress, while pricing discipline balances deposit growth with margin protection.

- Fed funds 5.25–5.50%

- Money-market/HH savings >4%

- Focus: relationship banking, treasury, wealth

- Key: liquidity buffers, contingent funding

- Strategy: disciplined pricing vs growth

Regional bank navigates ME/NH/VT rules, backing municipal builds with $3.2B

Rate volatility (fed funds 5.25–5.50% Jul 2025) and >4% money‑market yields compress NIMs, requiring hedging and product mix shifts. Maine unemployment 3.5% (Jun 2025) and 27% SMBs reporting hiring difficulty (NFIB 2024) drive wage pressure and credit sensitivity. Tourism seasonality creates volatile deposits and loan demand; construction PPI +6% y/y mid‑2024 tightens origination economics.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Funding cost |

| Unemployment ME | 3.5% | Wage pressure |

| SMB hiring | 27% | Credit risk |

| Construction PPI | +6% y/y | Origination |

Preview Before You Purchase

Bar Harbor Bankshares PESTLE Analysis

The Bar Harbor Bankshares PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete Political, Economic, Social, Technological, Legal, and Environmental assessment as displayed. No placeholders or teasers—this is the final file you’ll download immediately after checkout.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE analysis of Bar Harbor Bankshares—mapping political, economic, social, technological, legal and environmental forces shaping its outlook. Actionable insights reveal risks and growth levers for investors and managers. Ready-made and research-backed, it saves you hours. Purchase the full report to access the complete analysis now.

Political factors

State-level banking incentives and oversight

Operating across Maine (pop. ~1.37M), New Hampshire (1.38M) and Vermont (0.65M) exposes Bar Harbor Bankshares to three distinct state banking priorities and supervisory nuances. State programs for community development, broadband and housing—often funded via federal ARPA and state bond initiatives—can boost loan demand while directing capital to targeted sectors. Close alignment with state economic agendas enhances franchise value but demands nimble compliance and stakeholder engagement. Ongoing monitoring of legislative sessions and banking department guidance is essential for timely resource allocation.

Federal fiscal policy and infrastructure funding

Federal infrastructure programs such as the $1.2 trillion Bipartisan Infrastructure Law and $1.9 trillion American Rescue Plan drive municipal deposits, construction lending and treasury services in Northern New England, with millions flowing via formula grants and competitive awards. Timing lags between appropriations and local project starts create forecasting challenges for loan and deposit pipelines. Public‑private partnerships expand fee income opportunities in cash management. Shifts in federal budget priorities can quickly alter regional liquidity dynamics.

Community banking and rural development priorities

Bipartisan support for community banks and rural credit access has produced programs and guarantees that Bar Harbor Bankshares can tap to boost CRA-aligned lending; Bar Harbor reported about $3.2 billion in assets (2024) enabling targeted deployment. Advocacy outcomes shaping SBA and USDA guarantees—SBA 7(a) and USDA rural housing/USDA business programs—expand risk-adjusted returns while increasing inclusion. Reduced or delayed appropriations would slow targeted lending momentum and could raise funding costs.

Cross-border and regional trade exposure

Northern New England’s proximity to Canada links local businesses to cross-border tourism and trade; US–Canada goods and services trade exceeded 700 billion in 2023, making policy shifts material for gateway towns. Political frictions, tariffs or border-staffing changes can compress small-business cash flows and seasonal deposits, while a stable policy environment supports steady transaction volumes. Contingency planning for policy shocks reduces concentration risk.

- Cross-border dependence: high in coastal/gateway towns

- Macro fact: US–Canada trade >700bn in 2023

- Risk: tariffs/border staffing → seasonal deposit volatility

- Mitigation: contingency plans to manage concentration

Local taxation and municipal policy

Local property tax regimes, zoning changes, and municipal housing initiatives directly affect Bar Harbor Bankshares' collateral values and regional real estate activity, shaping loan volumes and loss assumptions. Competitive municipal cash management RFPs and deposit regulations influence access to low-cost public deposits. Policy-driven affordable housing programs create construction and permanent lending opportunities with layered credits, while rapid tax reassessments or moratoria can briefly chill lending appetite.

- Property tax & zoning: affect collateral values

- Municipal deposits: low-cost funding source

- Affordable housing: pipeline for construction/permanent loans

- Tax reassessments: temporary underwriting caution

Regional bank navigates ME/NH/VT rules, backing municipal builds with $3.2B

Bar Harbor faces multi-state regulatory nuance across ME/NH/VT, driving compliance costs but unlocking community-lending programs; assets ≈ $3.2B (2024). Federal infrastructure and ARPA funding fuel municipal deposits and construction loans; US–Canada trade >700bn (2023) affects border towns. Municipal tax/zoning shifts alter collateral values and deposit access; contingency plans reduce concentration risk.

| Metric | Value |

|---|---|

| Assets (2024) | $3.2B |

| US–Canada trade (2023) | >$700B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bar Harbor Bankshares across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by regional data and current trends. Designed for executives and investors, the analysis offers forward-looking insights, actionable risks and opportunities, and formatted content ready for plans and reports.

A concise, visually segmented PESTLE summary for Bar Harbor Bankshares that eases meeting prep and strategic reviews, easily dropped into presentations or shared for quick team alignment while allowing note additions for regional or business-line context.

Economic factors

Interest rate cycle and net interest margin

Rate volatility, with the federal funds target at 5.25–5.50% (July 2025), directly alters funding costs, loan yields and deposit betas, squeezing community bank NIMs. In competitive New England markets Bar Harbor may face faster deposit repricing, pressuring margins. Strong asset‑liability discipline stabilizes NIM across cycles. Active hedging and product‑mix shifts mitigate earnings swings.

Tourism and seasonal business dynamics

Maine draws millions of visitors annually (Maine Office of Tourism), driving pronounced seasonal deposits and credit utilization across hospitality, retail and services.

Off-season cash flow softness elevates credit-monitoring and collections needs for Bar Harbor Bankshares as operating cash and collateral values fall.

Tailored working-capital lines and treasury services smooth seasonality while weather and travel trends can materially amplify swings in fee and interest income.

Housing market and construction activity

Regional housing supply constraints and in-migration in Maine tighten mortgage and construction pipelines, pressuring affordability and origination volumes. Rising construction input costs — roughly 6% year-over-year through mid-2024 per BLS PPI — and appraisal volatility can reduce collateral coverage and slow draws. Portfolio mix between fixed and adjustable-rate loans determines sensitivity to Fed hikes, while public housing and LIHTC projects create lower-risk, lower-yield lending opportunities.

SMB health and labor market conditions

Local SMBs in Bar Harbor Bankshares markets face tight labor markets with Maine unemployment at 3.5% (June 2025) and NFIB reporting 27% of small firms with few or no qualified applicants in 2024, driving wage inflation and input cost variability. Credit performance closely tracks regional employment and consumer confidence, stressing smaller lenders during downturns. Advisory and cash management solutions can bolster client resilience while sector diversification reduces localized downturn risk.

- labor: Maine unemployment 3.5% (Jun 2025)

- labor shortage: 27% SMBs report few/no qualified applicants (NFIB 2024)

- credit link: defaults correlated with regional employment

- mitigation: advisory, cash mgmt, sector diversification

Deposit competition and liquidity

Higher market rates (federal funds 5.25–5.50% since 2023) and money-market/high-yield savings yields above 4% have intensified competition for core deposits; Bar Harbor leans on relationship banking, treasury services and wealth offerings to defend balances. Maintaining liquidity buffers and contingent funding plans is critical under stress, while pricing discipline balances deposit growth with margin protection.

- Fed funds 5.25–5.50%

- Money-market/HH savings >4%

- Focus: relationship banking, treasury, wealth

- Key: liquidity buffers, contingent funding

- Strategy: disciplined pricing vs growth

Regional bank navigates ME/NH/VT rules, backing municipal builds with $3.2B

Rate volatility (fed funds 5.25–5.50% Jul 2025) and >4% money‑market yields compress NIMs, requiring hedging and product mix shifts. Maine unemployment 3.5% (Jun 2025) and 27% SMBs reporting hiring difficulty (NFIB 2024) drive wage pressure and credit sensitivity. Tourism seasonality creates volatile deposits and loan demand; construction PPI +6% y/y mid‑2024 tightens origination economics.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Funding cost |

| Unemployment ME | 3.5% | Wage pressure |

| SMB hiring | 27% | Credit risk |

| Construction PPI | +6% y/y | Origination |

Preview Before You Purchase

Bar Harbor Bankshares PESTLE Analysis

The Bar Harbor Bankshares PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete Political, Economic, Social, Technological, Legal, and Environmental assessment as displayed. No placeholders or teasers—this is the final file you’ll download immediately after checkout.