Barings PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, and regulatory changes are shaping Barings’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and growth levers you can act on today. Ideal for investors and strategists—buy the full PESTLE for the complete, ready-to-use briefing and data-rich insights.

Political factors

Geopolitical tensions and sanctions exposure

Heightened geopolitical frictions can disrupt cross-border capital flows, raise volatility and compress valuations across fixed income, equities and real assets, forcing mark-to-market effects within days. Sanctions regimes constrain investable universes and OFAC/EU lists are updated weekly, requiring rapid portfolio rebalancing often within 48–72 hours. Barings must keep country, sector and counterparty risk frameworks aligned to evolving lists. Proactive scenario planning preserves client outcomes during policy shocks.

Election cycles and policy uncertainty

Major elections, including the US vote on Nov 5, 2024, can pivot fiscal, tax and regulatory agendas and reprice sectors and risk premia across markets.

Policy shifts feed directly into rates and credit spreads (global policy rates peaked near 5%+ in 2024–25), altering real estate demand drivers and valuation assumptions.

Barings must maintain agile macro positioning, proactive client communications, and use hedging plus diversification to reduce policy-path dependence and manage drawdown risk.

Trade policy and market access

Tariffs, capital controls and foreign ownership rules constrain global diversification and liquidity, with the WTO reporting a 2023 global average applied MFN tariff of 2.9% that raises trading costs and can deter flows. Market access constraints can reshape index eligibility and allocations, forcing reweighting and tracking error. Barings must leverage local partnerships and legal structures to maintain exposure, and continuous monitoring mitigates execution and repatriation risks.

Public investment priorities

Government spending in infrastructure, defense, healthcare and green transitions reorients opportunity sets: US Bipartisan Infrastructure Law totals roughly 1.2 trillion USD and the EU NextGenerationEU package is about 800 billion EUR, directing capital into projects that expand private credit pipelines and lift real-asset yields. Barings can originate thematic strategies tied to these public funding streams and engage stakeholders to support prudent deployment.

- Policy tailwinds: public funding -> private credit growth

- Thematic origination: infrastructure, green, healthcare, defense

- Engagement: coordinate with sponsors, sovereigns, communities

Central bank independence and coordination

Shifts in central bank credibility and coordination materially alter risk pricing and have driven recent FX and rate volatility; policy divergence between major central banks increased cross-asset dispersion in 2022–25. Barings, with a multi-region rates team and over $300bn AUM (2025), leverages that expertise to exploit dispersion while active liquidity management buffers sudden regime changes.

- Policy divergence → FX/rate volatility

- Barings >$300bn AUM, multi-region rates edge

- Liquidity buffers reduce regime-change risk

Geopolitical shocks, US election & 5% rate peak force rapid asset rebalancing

Heightened geopolitical friction and weekly sanctions updates force rapid rebalancing and can compress valuations; major elections (US 5 Nov 2024) and tariff regimes (WTO MFN 2.9% in 2023) reprice sectors. Policy-driven rate peaks near 5% (2024–25) shift real‑asset demand. Public funding (US ~$1.2tn, EU ~€800bn) creates private credit pipelines. Barings >$300bn AUM requires agile hedging and local partnerships.

| Tag | Value |

|---|---|

| Elections | US 5 Nov 2024 |

| Policy rates | ~5% peak (2024–25) |

| AUM | >$300bn (2025) |

What is included in the product

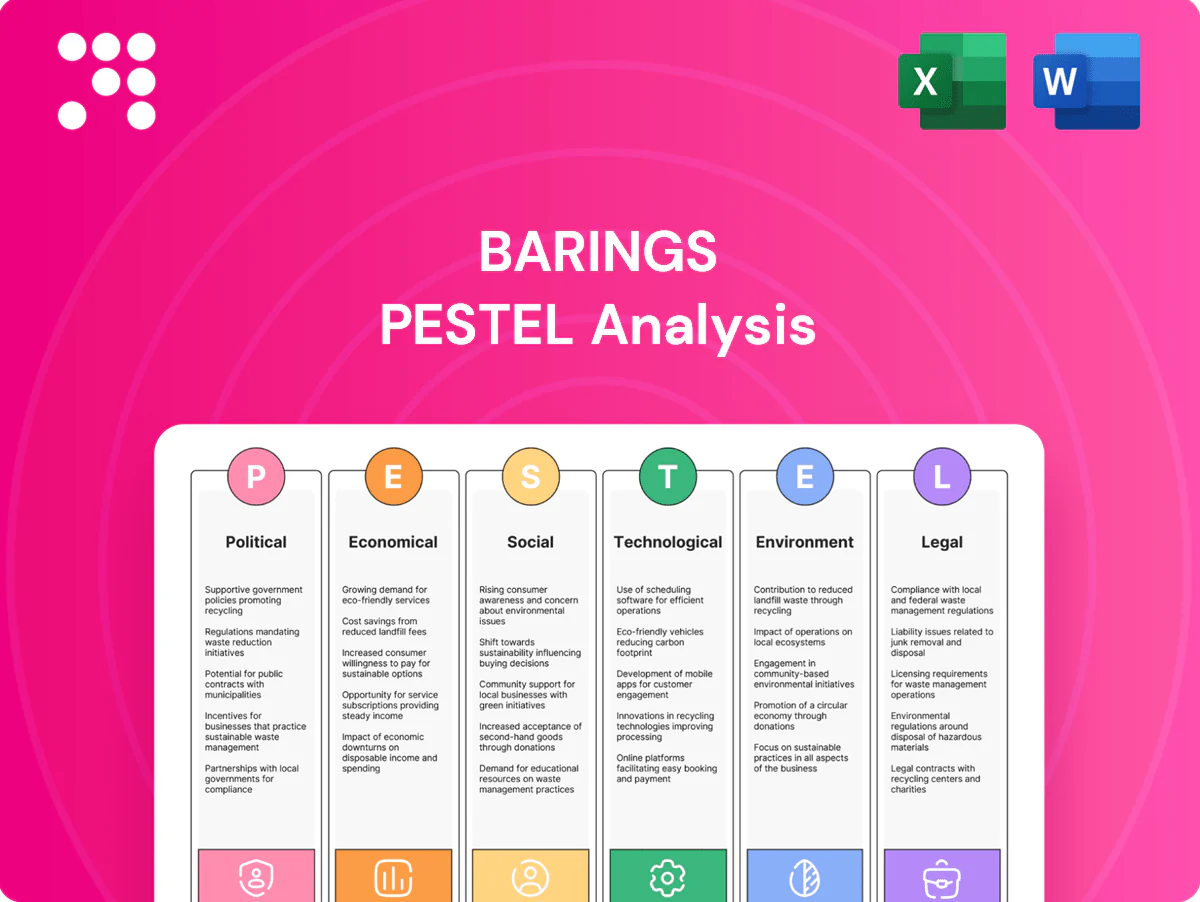

Explores how external macro-environmental factors uniquely affect Barings across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven, forward-looking insights and actionable implications to help executives, investors and strategists identify risks and opportunities.

Barings PESTLE Analysis delivers a clean, visually segmented summary for quick reference in meetings or presentations, easily editable for regional or business-line notes and shareable across teams to streamline external risk discussion and strategic alignment.

Economic factors

Interest rate cycles and yield curves

Interest-rate paths set funding costs, discount rates and credit performance—US policy rate ~5.25% (mid‑2025) and the 10‑yr Treasury ~4.2% (H1 2025) materially raise discount rates and borrowing spreads. Yield-curve shape changes relative value across short/long buckets and alters mortgage/ABS convexity. Barings can tactically shift duration and rotate sectors. Dynamic liability-aware strategies align with pension and insurer funding targets.

Inflation dynamics and real returns

Sticky or receding inflation shapes central bank stances and squeezes real incomes; policy rates remain elevated (Federal Reserve 5.25–5.50% mid‑2025) as core inflation in major economies hovers around 3–4%. Real assets and floating‑rate credit can hedge purchasing‑power erosion, while Barings can blend TIPS, inflation‑linked real assets and floating‑rate credit with active security selection. Robust research is needed to separate cyclical shocks from structural inflation pressures and target real returns.

Credit cycle and default rates

Earnings pressure and looming refinancing walls drove downgrade/default risk through 2023–24, with US speculative-grade default rates peaking near 3% in 2023 before falling toward ~1.5–2.0% in 2024; spread dispersion of 100–300 bps across sectors created alpha opportunities in private and public credit. Barings, with roughly $345bn AUM (2024), applies rigorous underwriting and covenant analysis, while deep workout teams and sector expertise support stronger recovery outcomes.

Global growth divergence and FX

Asynchronous growth across regions is driving cross-currency return dispersion; IMF projects global growth around 3% in 2025 with US ~2%, China ~4.5% and a subdued Euro area. FX volatility raises risk to unhedged returns and funding costs. Barings can deploy selective hedging, currency overlays and use macro insights to guide regional allocation and liquidity planning.

- Selective hedging to protect unhedged exposures

- Currency overlays for tactical alpha and risk control

- Macro-led regional allocation and liquidity buffers

Asset flows and fee compression

Industry flows toward passive and low-fee products (global ETF/ETP assets ~$11.5tn end-2023; passive >50% of US equity AUM in 2024) pressure margins, even as demand for private markets rises (private capital AUM ~$11.6tn in 2023). Barings can differentiate through active alpha, direct origination and bespoke mandates while operational efficiency sustains scalable client value.

- Passive share >50% US equity (2024)

- ETF/ETP assets ~$11.5tn (end-2023)

- Private capital AUM ~$11.6tn (2023)

- Differentiators: alpha, origination, customized mandates

- Focus: operational efficiency for scalability

Geopolitical shocks, US election & 5% rate peak force rapid asset rebalancing

Higher rates (Fed 5.25–5.50% mid‑2025; 10y ~4.2% H1‑25) raise discounting and funding costs; Barings ($345bn AUM 2024) can shift duration and use liability‑aware strategies. Sticky core inflation (3–4%) boosts demand for TIPS, real assets and floating‑rate credit. Regional growth divergence (IMF global ~3% 2025; US ~2%; China ~4.5%) drives FX and allocation risk.

| Metric | Value |

|---|---|

| AUM (Barings) | $345bn (2024) |

| Fed policy | 5.25–5.50% (mid‑2025) |

| 10‑yr | ~4.2% (H1‑25) |

| Global growth | ~3% (IMF 2025) |

Same Document Delivered

Barings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers a concise PESTLE analysis of Barings covering political, economic, social, technological, legal, and environmental factors. The report highlights key risks, trends, and strategic implications. Insights are actionable for investors and strategists assessing opportunities and threats.

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, and regulatory changes are shaping Barings’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and growth levers you can act on today. Ideal for investors and strategists—buy the full PESTLE for the complete, ready-to-use briefing and data-rich insights.

Political factors

Geopolitical tensions and sanctions exposure

Heightened geopolitical frictions can disrupt cross-border capital flows, raise volatility and compress valuations across fixed income, equities and real assets, forcing mark-to-market effects within days. Sanctions regimes constrain investable universes and OFAC/EU lists are updated weekly, requiring rapid portfolio rebalancing often within 48–72 hours. Barings must keep country, sector and counterparty risk frameworks aligned to evolving lists. Proactive scenario planning preserves client outcomes during policy shocks.

Election cycles and policy uncertainty

Major elections, including the US vote on Nov 5, 2024, can pivot fiscal, tax and regulatory agendas and reprice sectors and risk premia across markets.

Policy shifts feed directly into rates and credit spreads (global policy rates peaked near 5%+ in 2024–25), altering real estate demand drivers and valuation assumptions.

Barings must maintain agile macro positioning, proactive client communications, and use hedging plus diversification to reduce policy-path dependence and manage drawdown risk.

Trade policy and market access

Tariffs, capital controls and foreign ownership rules constrain global diversification and liquidity, with the WTO reporting a 2023 global average applied MFN tariff of 2.9% that raises trading costs and can deter flows. Market access constraints can reshape index eligibility and allocations, forcing reweighting and tracking error. Barings must leverage local partnerships and legal structures to maintain exposure, and continuous monitoring mitigates execution and repatriation risks.

Public investment priorities

Government spending in infrastructure, defense, healthcare and green transitions reorients opportunity sets: US Bipartisan Infrastructure Law totals roughly 1.2 trillion USD and the EU NextGenerationEU package is about 800 billion EUR, directing capital into projects that expand private credit pipelines and lift real-asset yields. Barings can originate thematic strategies tied to these public funding streams and engage stakeholders to support prudent deployment.

- Policy tailwinds: public funding -> private credit growth

- Thematic origination: infrastructure, green, healthcare, defense

- Engagement: coordinate with sponsors, sovereigns, communities

Central bank independence and coordination

Shifts in central bank credibility and coordination materially alter risk pricing and have driven recent FX and rate volatility; policy divergence between major central banks increased cross-asset dispersion in 2022–25. Barings, with a multi-region rates team and over $300bn AUM (2025), leverages that expertise to exploit dispersion while active liquidity management buffers sudden regime changes.

- Policy divergence → FX/rate volatility

- Barings >$300bn AUM, multi-region rates edge

- Liquidity buffers reduce regime-change risk

Geopolitical shocks, US election & 5% rate peak force rapid asset rebalancing

Heightened geopolitical friction and weekly sanctions updates force rapid rebalancing and can compress valuations; major elections (US 5 Nov 2024) and tariff regimes (WTO MFN 2.9% in 2023) reprice sectors. Policy-driven rate peaks near 5% (2024–25) shift real‑asset demand. Public funding (US ~$1.2tn, EU ~€800bn) creates private credit pipelines. Barings >$300bn AUM requires agile hedging and local partnerships.

| Tag | Value |

|---|---|

| Elections | US 5 Nov 2024 |

| Policy rates | ~5% peak (2024–25) |

| AUM | >$300bn (2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Barings across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven, forward-looking insights and actionable implications to help executives, investors and strategists identify risks and opportunities.

Barings PESTLE Analysis delivers a clean, visually segmented summary for quick reference in meetings or presentations, easily editable for regional or business-line notes and shareable across teams to streamline external risk discussion and strategic alignment.

Economic factors

Interest rate cycles and yield curves

Interest-rate paths set funding costs, discount rates and credit performance—US policy rate ~5.25% (mid‑2025) and the 10‑yr Treasury ~4.2% (H1 2025) materially raise discount rates and borrowing spreads. Yield-curve shape changes relative value across short/long buckets and alters mortgage/ABS convexity. Barings can tactically shift duration and rotate sectors. Dynamic liability-aware strategies align with pension and insurer funding targets.

Inflation dynamics and real returns

Sticky or receding inflation shapes central bank stances and squeezes real incomes; policy rates remain elevated (Federal Reserve 5.25–5.50% mid‑2025) as core inflation in major economies hovers around 3–4%. Real assets and floating‑rate credit can hedge purchasing‑power erosion, while Barings can blend TIPS, inflation‑linked real assets and floating‑rate credit with active security selection. Robust research is needed to separate cyclical shocks from structural inflation pressures and target real returns.

Credit cycle and default rates

Earnings pressure and looming refinancing walls drove downgrade/default risk through 2023–24, with US speculative-grade default rates peaking near 3% in 2023 before falling toward ~1.5–2.0% in 2024; spread dispersion of 100–300 bps across sectors created alpha opportunities in private and public credit. Barings, with roughly $345bn AUM (2024), applies rigorous underwriting and covenant analysis, while deep workout teams and sector expertise support stronger recovery outcomes.

Global growth divergence and FX

Asynchronous growth across regions is driving cross-currency return dispersion; IMF projects global growth around 3% in 2025 with US ~2%, China ~4.5% and a subdued Euro area. FX volatility raises risk to unhedged returns and funding costs. Barings can deploy selective hedging, currency overlays and use macro insights to guide regional allocation and liquidity planning.

- Selective hedging to protect unhedged exposures

- Currency overlays for tactical alpha and risk control

- Macro-led regional allocation and liquidity buffers

Asset flows and fee compression

Industry flows toward passive and low-fee products (global ETF/ETP assets ~$11.5tn end-2023; passive >50% of US equity AUM in 2024) pressure margins, even as demand for private markets rises (private capital AUM ~$11.6tn in 2023). Barings can differentiate through active alpha, direct origination and bespoke mandates while operational efficiency sustains scalable client value.

- Passive share >50% US equity (2024)

- ETF/ETP assets ~$11.5tn (end-2023)

- Private capital AUM ~$11.6tn (2023)

- Differentiators: alpha, origination, customized mandates

- Focus: operational efficiency for scalability

Geopolitical shocks, US election & 5% rate peak force rapid asset rebalancing

Higher rates (Fed 5.25–5.50% mid‑2025; 10y ~4.2% H1‑25) raise discounting and funding costs; Barings ($345bn AUM 2024) can shift duration and use liability‑aware strategies. Sticky core inflation (3–4%) boosts demand for TIPS, real assets and floating‑rate credit. Regional growth divergence (IMF global ~3% 2025; US ~2%; China ~4.5%) drives FX and allocation risk.

| Metric | Value |

|---|---|

| AUM (Barings) | $345bn (2024) |

| Fed policy | 5.25–5.50% (mid‑2025) |

| 10‑yr | ~4.2% (H1‑25) |

| Global growth | ~3% (IMF 2025) |

Same Document Delivered

Barings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers a concise PESTLE analysis of Barings covering political, economic, social, technological, legal, and environmental factors. The report highlights key risks, trends, and strategic implications. Insights are actionable for investors and strategists assessing opportunities and threats.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, and regulatory changes are shaping Barings’s strategic outlook in our concise PESTLE snapshot. This analysis highlights risks and growth levers you can act on today. Ideal for investors and strategists—buy the full PESTLE for the complete, ready-to-use briefing and data-rich insights.

Political factors

Geopolitical tensions and sanctions exposure

Heightened geopolitical frictions can disrupt cross-border capital flows, raise volatility and compress valuations across fixed income, equities and real assets, forcing mark-to-market effects within days. Sanctions regimes constrain investable universes and OFAC/EU lists are updated weekly, requiring rapid portfolio rebalancing often within 48–72 hours. Barings must keep country, sector and counterparty risk frameworks aligned to evolving lists. Proactive scenario planning preserves client outcomes during policy shocks.

Election cycles and policy uncertainty

Major elections, including the US vote on Nov 5, 2024, can pivot fiscal, tax and regulatory agendas and reprice sectors and risk premia across markets.

Policy shifts feed directly into rates and credit spreads (global policy rates peaked near 5%+ in 2024–25), altering real estate demand drivers and valuation assumptions.

Barings must maintain agile macro positioning, proactive client communications, and use hedging plus diversification to reduce policy-path dependence and manage drawdown risk.

Trade policy and market access

Tariffs, capital controls and foreign ownership rules constrain global diversification and liquidity, with the WTO reporting a 2023 global average applied MFN tariff of 2.9% that raises trading costs and can deter flows. Market access constraints can reshape index eligibility and allocations, forcing reweighting and tracking error. Barings must leverage local partnerships and legal structures to maintain exposure, and continuous monitoring mitigates execution and repatriation risks.

Public investment priorities

Government spending in infrastructure, defense, healthcare and green transitions reorients opportunity sets: US Bipartisan Infrastructure Law totals roughly 1.2 trillion USD and the EU NextGenerationEU package is about 800 billion EUR, directing capital into projects that expand private credit pipelines and lift real-asset yields. Barings can originate thematic strategies tied to these public funding streams and engage stakeholders to support prudent deployment.

- Policy tailwinds: public funding -> private credit growth

- Thematic origination: infrastructure, green, healthcare, defense

- Engagement: coordinate with sponsors, sovereigns, communities

Central bank independence and coordination

Shifts in central bank credibility and coordination materially alter risk pricing and have driven recent FX and rate volatility; policy divergence between major central banks increased cross-asset dispersion in 2022–25. Barings, with a multi-region rates team and over $300bn AUM (2025), leverages that expertise to exploit dispersion while active liquidity management buffers sudden regime changes.

- Policy divergence → FX/rate volatility

- Barings >$300bn AUM, multi-region rates edge

- Liquidity buffers reduce regime-change risk

Geopolitical shocks, US election & 5% rate peak force rapid asset rebalancing

Heightened geopolitical friction and weekly sanctions updates force rapid rebalancing and can compress valuations; major elections (US 5 Nov 2024) and tariff regimes (WTO MFN 2.9% in 2023) reprice sectors. Policy-driven rate peaks near 5% (2024–25) shift real‑asset demand. Public funding (US ~$1.2tn, EU ~€800bn) creates private credit pipelines. Barings >$300bn AUM requires agile hedging and local partnerships.

| Tag | Value |

|---|---|

| Elections | US 5 Nov 2024 |

| Policy rates | ~5% peak (2024–25) |

| AUM | >$300bn (2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Barings across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven, forward-looking insights and actionable implications to help executives, investors and strategists identify risks and opportunities.

Barings PESTLE Analysis delivers a clean, visually segmented summary for quick reference in meetings or presentations, easily editable for regional or business-line notes and shareable across teams to streamline external risk discussion and strategic alignment.

Economic factors

Interest rate cycles and yield curves

Interest-rate paths set funding costs, discount rates and credit performance—US policy rate ~5.25% (mid‑2025) and the 10‑yr Treasury ~4.2% (H1 2025) materially raise discount rates and borrowing spreads. Yield-curve shape changes relative value across short/long buckets and alters mortgage/ABS convexity. Barings can tactically shift duration and rotate sectors. Dynamic liability-aware strategies align with pension and insurer funding targets.

Inflation dynamics and real returns

Sticky or receding inflation shapes central bank stances and squeezes real incomes; policy rates remain elevated (Federal Reserve 5.25–5.50% mid‑2025) as core inflation in major economies hovers around 3–4%. Real assets and floating‑rate credit can hedge purchasing‑power erosion, while Barings can blend TIPS, inflation‑linked real assets and floating‑rate credit with active security selection. Robust research is needed to separate cyclical shocks from structural inflation pressures and target real returns.

Credit cycle and default rates

Earnings pressure and looming refinancing walls drove downgrade/default risk through 2023–24, with US speculative-grade default rates peaking near 3% in 2023 before falling toward ~1.5–2.0% in 2024; spread dispersion of 100–300 bps across sectors created alpha opportunities in private and public credit. Barings, with roughly $345bn AUM (2024), applies rigorous underwriting and covenant analysis, while deep workout teams and sector expertise support stronger recovery outcomes.

Global growth divergence and FX

Asynchronous growth across regions is driving cross-currency return dispersion; IMF projects global growth around 3% in 2025 with US ~2%, China ~4.5% and a subdued Euro area. FX volatility raises risk to unhedged returns and funding costs. Barings can deploy selective hedging, currency overlays and use macro insights to guide regional allocation and liquidity planning.

- Selective hedging to protect unhedged exposures

- Currency overlays for tactical alpha and risk control

- Macro-led regional allocation and liquidity buffers

Asset flows and fee compression

Industry flows toward passive and low-fee products (global ETF/ETP assets ~$11.5tn end-2023; passive >50% of US equity AUM in 2024) pressure margins, even as demand for private markets rises (private capital AUM ~$11.6tn in 2023). Barings can differentiate through active alpha, direct origination and bespoke mandates while operational efficiency sustains scalable client value.

- Passive share >50% US equity (2024)

- ETF/ETP assets ~$11.5tn (end-2023)

- Private capital AUM ~$11.6tn (2023)

- Differentiators: alpha, origination, customized mandates

- Focus: operational efficiency for scalability

Geopolitical shocks, US election & 5% rate peak force rapid asset rebalancing

Higher rates (Fed 5.25–5.50% mid‑2025; 10y ~4.2% H1‑25) raise discounting and funding costs; Barings ($345bn AUM 2024) can shift duration and use liability‑aware strategies. Sticky core inflation (3–4%) boosts demand for TIPS, real assets and floating‑rate credit. Regional growth divergence (IMF global ~3% 2025; US ~2%; China ~4.5%) drives FX and allocation risk.

| Metric | Value |

|---|---|

| AUM (Barings) | $345bn (2024) |

| Fed policy | 5.25–5.50% (mid‑2025) |

| 10‑yr | ~4.2% (H1‑25) |

| Global growth | ~3% (IMF 2025) |

Same Document Delivered

Barings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It delivers a concise PESTLE analysis of Barings covering political, economic, social, technological, legal, and environmental factors. The report highlights key risks, trends, and strategic implications. Insights are actionable for investors and strategists assessing opportunities and threats.