Basic-Fit Porter's Five Forces Analysis

From Overview to Strategy Blueprint

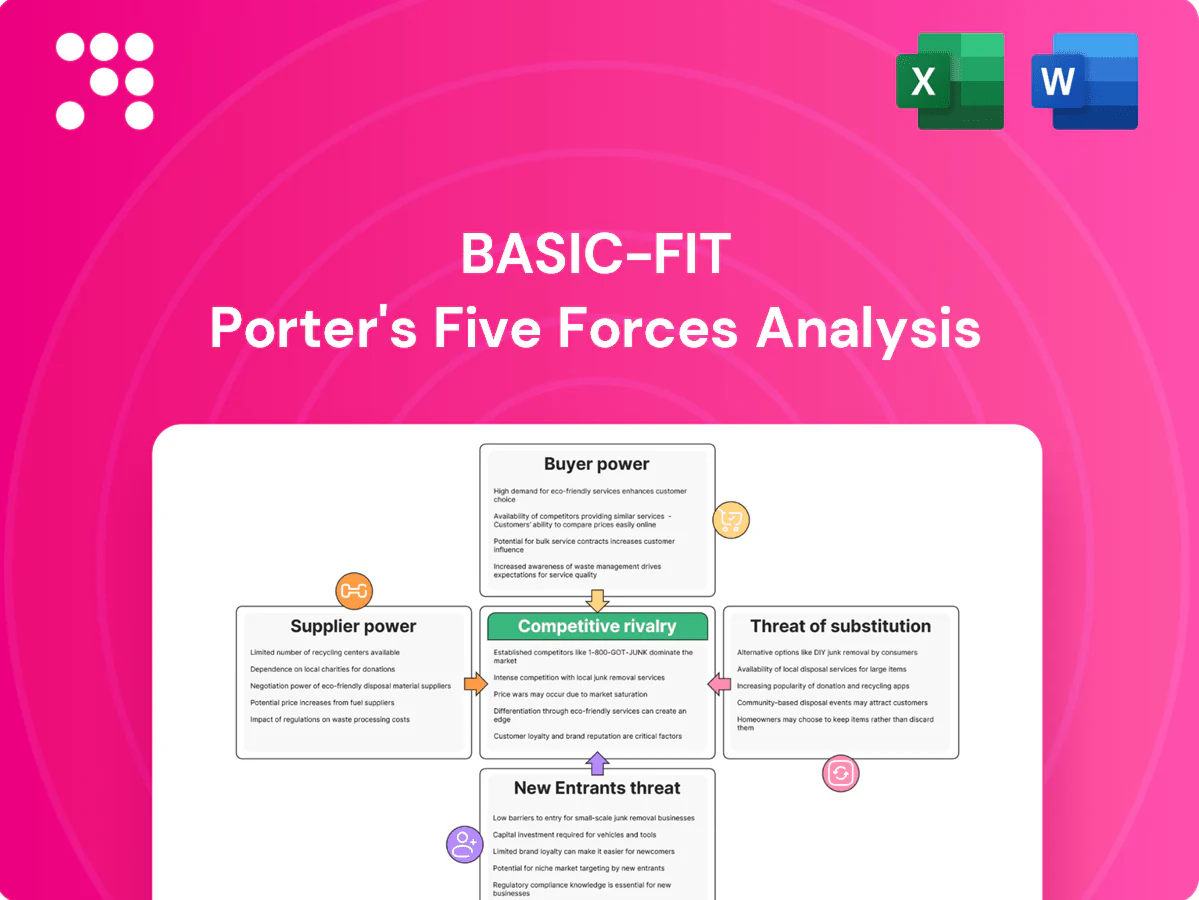

Basic-Fit’s competitive landscape shows strong buyer power, intense rivalry, and low supplier leverage, with digital services and low-cost positioning shaping substitute and entry threats. This snapshot highlights key pressures but omits force-by-force ratings and visuals. The full Porter’s Five Forces Analysis uncovers detailed strengths, risks, and strategic implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Standardized equipment market

Strength and cardio equipment are largely standardized, allowing Basic-Fit to multisource from global OEMs like Technogym and Life Fitness and reduce supplier differentiation; Basic-Fit operates over 1,500 clubs and ~3.1 million members (2024), supporting scale purchasing. Proprietary ecosystems and software locks from some suppliers can create pockets of dependency. Volume-based contracts and group purchasing drive discounts and dilute individual supplier leverage.

Scale-driven purchasing leverage

Basic-Fit's scale — c.1,400 clubs and about 3.8 million members in 2024 — delivers strong purchasing leverage, enabling bulk discounts and extended payment terms; centralized procurement and multi-year supplier contracts lower per-unit hardware costs, create high supplier incentive to keep Basic-Fit as a repeat buyer, and dampen cost volatility on core equipment.

Maintenance and service dependencies

After-sales maintenance contracts confer supplier leverage for Basic-Fit (≈2.7M members, 1,100+ clubs in 2024) because uptime is critical; switching providers often requires 3–6 months of coordination, training and can risk 2–5% revenue impact from downtime. Predictive maintenance can reduce unscheduled downtime by ~30% but demands deep data integration with vendor systems, while multi-year SLAs trade lower unit costs for guaranteed reliability.

Real estate landlords’ influence

Digital content and software vendors

Virtual classes, app platforms and access control create software switching costs for Basic-Fit, while API integrations and data portability lower lock-in but still require migration effort; vendors with unique content or analytics can command premium fees, and negotiating IP and data rights preserves strategic flexibility (Basic-Fit serves over 2.5 million members as of 2024).

- Switching costs: platform + access control

- APIs: reduce lock-in, increase transition work

- Unique content: enables higher vendor fees

- IP/data rights: key negotiating point

Scale (≈1,500 clubs, ≈3.1M members) boosts supplier leverage; downtime risk ≈2–5% rev

Basic-Fit’s scale (≈1,500 clubs, ≈3.1M members in 2024) gives strong supplier leverage for standardized equipment and volume discounts; maintenance SLAs and proprietary software create pockets of dependency, with downtime risks of ~2–5% revenue and predictive maintenance cutting unscheduled downtime ~30%; long leases (5–20 yrs) shift power to landlords but standardized fit-outs mitigate it.

| Metric | 2024 value | Impact |

|---|---|---|

| Clubs | ≈1,500 | Bulk buying power |

| Members | ≈3.1M | Repeat purchase leverage |

| Downtime risk | 2–5% rev | Supplier leverage |

| Lease terms | 5–20 yrs | Landlord power |

What is included in the product

Concise Porter's Five Forces overview tailored to Basic-Fit, uncovering competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and industry rivalry to assess pricing power, profitability risks, and strategic safeguards for the low‑cost European fitness market.

A concise, slide-ready Porter's Five Forces summary for Basic-Fit that highlights competitive pressures, supplier leverage, member churn risks and growth barriers—ideal for quick strategic decisions, investor decks, or board discussions.

Customers Bargaining Power

High price sensitivity

Budget gym members in Basic-Fit (≈3.2 million members in 2024) are highly price-sensitive and react to small fee changes. Promotions and low introductory offers have intensified member expectations for ongoing discounting. Transparent online pricing enables effortless comparisons across operators. Retention increasingly depends on proving superior value-per-euro to avoid churn.

Low switching costs

Low switching costs at Basic-Fit—driven by month-to-month and short-commitment models—make churn to nearby competitors easy; Basic-Fit reported about 3.2 million active members in 2024, highlighting a fluid customer base. Proximity and convenience often trump brand loyalty, especially in urban markets where 70% of gym visits are within 5 km. Cross-club access cushions but does not eliminate switching, while digital-only alternatives further lower exit friction.

Abundant alternatives

Consumers can choose among multiple low-cost chains, municipal gyms and niche studios; Basic-Fit reported roughly 3.0 million active members in 2024. Home fitness apps and connected-equipment markets exceeded about 3 billion USD in 2023, providing credible non-gym alternatives. This abundance raises churn risk and strengthens buyer negotiating posture. Differentiation via convenience, cleanliness and high uptime becomes essential.

Information transparency

Reviews, social media and price aggregators make Basic-Fit quality and crowding highly visible, with peak-time congestion and equipment availability directly lowering perceived value; negative feedback can cascade across regions via platforms. Rapidly spreading complaints increase customer bargaining power while data-driven capacity management and dynamic scheduling can preempt dissatisfaction.

- Visibility of crowding and real-time availability raises customer leverage; proactive capacity management reduces churn

Demand seasonality

Demand seasonality drives customer bargaining: New Year and pre-summer peaks increase buyer selectivity and deal hunting, while off-peak months raise churn risk if perceived value slips. Flexible add-ons and freeze options boost buyer leverage by lowering switching costs. Balanced pricing and targeted incentives are essential to smooth membership flows.

- Peak-driven deal sensitivity

- Off-peak churn vulnerability

- Freeze/add-on leverage

- Pricing + incentives to stabilize retention

3.2M members price-sensitive; transparency and crowding raise churn — dynamic pricing, capacity key

Basic-Fit’s ~3.2M members (2024) are highly price-sensitive with low switching costs from month-to-month contracts; transparent online pricing and visible crowding amplify churn risk. Proliferation of low-cost rivals, municipal gyms and a $3B+ home-fitness market (2023) strengthens buyer leverage. Dynamic pricing, capacity management and value-per-euro are key retention tools.

| Metric | Value |

|---|---|

| Members (2024) | ≈3.2M |

| Home-fitness market (2023) | >$3B |

| Urban visits within 5 km | ≈70% |

Same Document Delivered

Basic-Fit Porter's Five Forces Analysis

This preview is the exact Basic-Fit Porter's Five Forces Analysis you'll receive after purchase, fully formatted and ready for use. No placeholders or samples—what you see is the final deliverable. You’ll get instant access to this same document immediately after payment.

From Overview to Strategy Blueprint

Basic-Fit’s competitive landscape shows strong buyer power, intense rivalry, and low supplier leverage, with digital services and low-cost positioning shaping substitute and entry threats. This snapshot highlights key pressures but omits force-by-force ratings and visuals. The full Porter’s Five Forces Analysis uncovers detailed strengths, risks, and strategic implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Standardized equipment market

Strength and cardio equipment are largely standardized, allowing Basic-Fit to multisource from global OEMs like Technogym and Life Fitness and reduce supplier differentiation; Basic-Fit operates over 1,500 clubs and ~3.1 million members (2024), supporting scale purchasing. Proprietary ecosystems and software locks from some suppliers can create pockets of dependency. Volume-based contracts and group purchasing drive discounts and dilute individual supplier leverage.

Scale-driven purchasing leverage

Basic-Fit's scale — c.1,400 clubs and about 3.8 million members in 2024 — delivers strong purchasing leverage, enabling bulk discounts and extended payment terms; centralized procurement and multi-year supplier contracts lower per-unit hardware costs, create high supplier incentive to keep Basic-Fit as a repeat buyer, and dampen cost volatility on core equipment.

Maintenance and service dependencies

After-sales maintenance contracts confer supplier leverage for Basic-Fit (≈2.7M members, 1,100+ clubs in 2024) because uptime is critical; switching providers often requires 3–6 months of coordination, training and can risk 2–5% revenue impact from downtime. Predictive maintenance can reduce unscheduled downtime by ~30% but demands deep data integration with vendor systems, while multi-year SLAs trade lower unit costs for guaranteed reliability.

Real estate landlords’ influence

Digital content and software vendors

Virtual classes, app platforms and access control create software switching costs for Basic-Fit, while API integrations and data portability lower lock-in but still require migration effort; vendors with unique content or analytics can command premium fees, and negotiating IP and data rights preserves strategic flexibility (Basic-Fit serves over 2.5 million members as of 2024).

- Switching costs: platform + access control

- APIs: reduce lock-in, increase transition work

- Unique content: enables higher vendor fees

- IP/data rights: key negotiating point

Scale (≈1,500 clubs, ≈3.1M members) boosts supplier leverage; downtime risk ≈2–5% rev

Basic-Fit’s scale (≈1,500 clubs, ≈3.1M members in 2024) gives strong supplier leverage for standardized equipment and volume discounts; maintenance SLAs and proprietary software create pockets of dependency, with downtime risks of ~2–5% revenue and predictive maintenance cutting unscheduled downtime ~30%; long leases (5–20 yrs) shift power to landlords but standardized fit-outs mitigate it.

| Metric | 2024 value | Impact |

|---|---|---|

| Clubs | ≈1,500 | Bulk buying power |

| Members | ≈3.1M | Repeat purchase leverage |

| Downtime risk | 2–5% rev | Supplier leverage |

| Lease terms | 5–20 yrs | Landlord power |

What is included in the product

Concise Porter's Five Forces overview tailored to Basic-Fit, uncovering competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and industry rivalry to assess pricing power, profitability risks, and strategic safeguards for the low‑cost European fitness market.

A concise, slide-ready Porter's Five Forces summary for Basic-Fit that highlights competitive pressures, supplier leverage, member churn risks and growth barriers—ideal for quick strategic decisions, investor decks, or board discussions.

Customers Bargaining Power

High price sensitivity

Budget gym members in Basic-Fit (≈3.2 million members in 2024) are highly price-sensitive and react to small fee changes. Promotions and low introductory offers have intensified member expectations for ongoing discounting. Transparent online pricing enables effortless comparisons across operators. Retention increasingly depends on proving superior value-per-euro to avoid churn.

Low switching costs

Low switching costs at Basic-Fit—driven by month-to-month and short-commitment models—make churn to nearby competitors easy; Basic-Fit reported about 3.2 million active members in 2024, highlighting a fluid customer base. Proximity and convenience often trump brand loyalty, especially in urban markets where 70% of gym visits are within 5 km. Cross-club access cushions but does not eliminate switching, while digital-only alternatives further lower exit friction.

Abundant alternatives

Consumers can choose among multiple low-cost chains, municipal gyms and niche studios; Basic-Fit reported roughly 3.0 million active members in 2024. Home fitness apps and connected-equipment markets exceeded about 3 billion USD in 2023, providing credible non-gym alternatives. This abundance raises churn risk and strengthens buyer negotiating posture. Differentiation via convenience, cleanliness and high uptime becomes essential.

Information transparency

Reviews, social media and price aggregators make Basic-Fit quality and crowding highly visible, with peak-time congestion and equipment availability directly lowering perceived value; negative feedback can cascade across regions via platforms. Rapidly spreading complaints increase customer bargaining power while data-driven capacity management and dynamic scheduling can preempt dissatisfaction.

- Visibility of crowding and real-time availability raises customer leverage; proactive capacity management reduces churn

Demand seasonality

Demand seasonality drives customer bargaining: New Year and pre-summer peaks increase buyer selectivity and deal hunting, while off-peak months raise churn risk if perceived value slips. Flexible add-ons and freeze options boost buyer leverage by lowering switching costs. Balanced pricing and targeted incentives are essential to smooth membership flows.

- Peak-driven deal sensitivity

- Off-peak churn vulnerability

- Freeze/add-on leverage

- Pricing + incentives to stabilize retention

3.2M members price-sensitive; transparency and crowding raise churn — dynamic pricing, capacity key

Basic-Fit’s ~3.2M members (2024) are highly price-sensitive with low switching costs from month-to-month contracts; transparent online pricing and visible crowding amplify churn risk. Proliferation of low-cost rivals, municipal gyms and a $3B+ home-fitness market (2023) strengthens buyer leverage. Dynamic pricing, capacity management and value-per-euro are key retention tools.

| Metric | Value |

|---|---|

| Members (2024) | ≈3.2M |

| Home-fitness market (2023) | >$3B |

| Urban visits within 5 km | ≈70% |

Same Document Delivered

Basic-Fit Porter's Five Forces Analysis

This preview is the exact Basic-Fit Porter's Five Forces Analysis you'll receive after purchase, fully formatted and ready for use. No placeholders or samples—what you see is the final deliverable. You’ll get instant access to this same document immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Basic-Fit’s competitive landscape shows strong buyer power, intense rivalry, and low supplier leverage, with digital services and low-cost positioning shaping substitute and entry threats. This snapshot highlights key pressures but omits force-by-force ratings and visuals. The full Porter’s Five Forces Analysis uncovers detailed strengths, risks, and strategic implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Standardized equipment market

Strength and cardio equipment are largely standardized, allowing Basic-Fit to multisource from global OEMs like Technogym and Life Fitness and reduce supplier differentiation; Basic-Fit operates over 1,500 clubs and ~3.1 million members (2024), supporting scale purchasing. Proprietary ecosystems and software locks from some suppliers can create pockets of dependency. Volume-based contracts and group purchasing drive discounts and dilute individual supplier leverage.

Scale-driven purchasing leverage

Basic-Fit's scale — c.1,400 clubs and about 3.8 million members in 2024 — delivers strong purchasing leverage, enabling bulk discounts and extended payment terms; centralized procurement and multi-year supplier contracts lower per-unit hardware costs, create high supplier incentive to keep Basic-Fit as a repeat buyer, and dampen cost volatility on core equipment.

Maintenance and service dependencies

After-sales maintenance contracts confer supplier leverage for Basic-Fit (≈2.7M members, 1,100+ clubs in 2024) because uptime is critical; switching providers often requires 3–6 months of coordination, training and can risk 2–5% revenue impact from downtime. Predictive maintenance can reduce unscheduled downtime by ~30% but demands deep data integration with vendor systems, while multi-year SLAs trade lower unit costs for guaranteed reliability.

Real estate landlords’ influence

Digital content and software vendors

Virtual classes, app platforms and access control create software switching costs for Basic-Fit, while API integrations and data portability lower lock-in but still require migration effort; vendors with unique content or analytics can command premium fees, and negotiating IP and data rights preserves strategic flexibility (Basic-Fit serves over 2.5 million members as of 2024).

- Switching costs: platform + access control

- APIs: reduce lock-in, increase transition work

- Unique content: enables higher vendor fees

- IP/data rights: key negotiating point

Scale (≈1,500 clubs, ≈3.1M members) boosts supplier leverage; downtime risk ≈2–5% rev

Basic-Fit’s scale (≈1,500 clubs, ≈3.1M members in 2024) gives strong supplier leverage for standardized equipment and volume discounts; maintenance SLAs and proprietary software create pockets of dependency, with downtime risks of ~2–5% revenue and predictive maintenance cutting unscheduled downtime ~30%; long leases (5–20 yrs) shift power to landlords but standardized fit-outs mitigate it.

| Metric | 2024 value | Impact |

|---|---|---|

| Clubs | ≈1,500 | Bulk buying power |

| Members | ≈3.1M | Repeat purchase leverage |

| Downtime risk | 2–5% rev | Supplier leverage |

| Lease terms | 5–20 yrs | Landlord power |

What is included in the product

Concise Porter's Five Forces overview tailored to Basic-Fit, uncovering competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and industry rivalry to assess pricing power, profitability risks, and strategic safeguards for the low‑cost European fitness market.

A concise, slide-ready Porter's Five Forces summary for Basic-Fit that highlights competitive pressures, supplier leverage, member churn risks and growth barriers—ideal for quick strategic decisions, investor decks, or board discussions.

Customers Bargaining Power

High price sensitivity

Budget gym members in Basic-Fit (≈3.2 million members in 2024) are highly price-sensitive and react to small fee changes. Promotions and low introductory offers have intensified member expectations for ongoing discounting. Transparent online pricing enables effortless comparisons across operators. Retention increasingly depends on proving superior value-per-euro to avoid churn.

Low switching costs

Low switching costs at Basic-Fit—driven by month-to-month and short-commitment models—make churn to nearby competitors easy; Basic-Fit reported about 3.2 million active members in 2024, highlighting a fluid customer base. Proximity and convenience often trump brand loyalty, especially in urban markets where 70% of gym visits are within 5 km. Cross-club access cushions but does not eliminate switching, while digital-only alternatives further lower exit friction.

Abundant alternatives

Consumers can choose among multiple low-cost chains, municipal gyms and niche studios; Basic-Fit reported roughly 3.0 million active members in 2024. Home fitness apps and connected-equipment markets exceeded about 3 billion USD in 2023, providing credible non-gym alternatives. This abundance raises churn risk and strengthens buyer negotiating posture. Differentiation via convenience, cleanliness and high uptime becomes essential.

Information transparency

Reviews, social media and price aggregators make Basic-Fit quality and crowding highly visible, with peak-time congestion and equipment availability directly lowering perceived value; negative feedback can cascade across regions via platforms. Rapidly spreading complaints increase customer bargaining power while data-driven capacity management and dynamic scheduling can preempt dissatisfaction.

- Visibility of crowding and real-time availability raises customer leverage; proactive capacity management reduces churn

Demand seasonality

Demand seasonality drives customer bargaining: New Year and pre-summer peaks increase buyer selectivity and deal hunting, while off-peak months raise churn risk if perceived value slips. Flexible add-ons and freeze options boost buyer leverage by lowering switching costs. Balanced pricing and targeted incentives are essential to smooth membership flows.

- Peak-driven deal sensitivity

- Off-peak churn vulnerability

- Freeze/add-on leverage

- Pricing + incentives to stabilize retention

3.2M members price-sensitive; transparency and crowding raise churn — dynamic pricing, capacity key

Basic-Fit’s ~3.2M members (2024) are highly price-sensitive with low switching costs from month-to-month contracts; transparent online pricing and visible crowding amplify churn risk. Proliferation of low-cost rivals, municipal gyms and a $3B+ home-fitness market (2023) strengthens buyer leverage. Dynamic pricing, capacity management and value-per-euro are key retention tools.

| Metric | Value |

|---|---|

| Members (2024) | ≈3.2M |

| Home-fitness market (2023) | >$3B |

| Urban visits within 5 km | ≈70% |

Same Document Delivered

Basic-Fit Porter's Five Forces Analysis

This preview is the exact Basic-Fit Porter's Five Forces Analysis you'll receive after purchase, fully formatted and ready for use. No placeholders or samples—what you see is the final deliverable. You’ll get instant access to this same document immediately after payment.